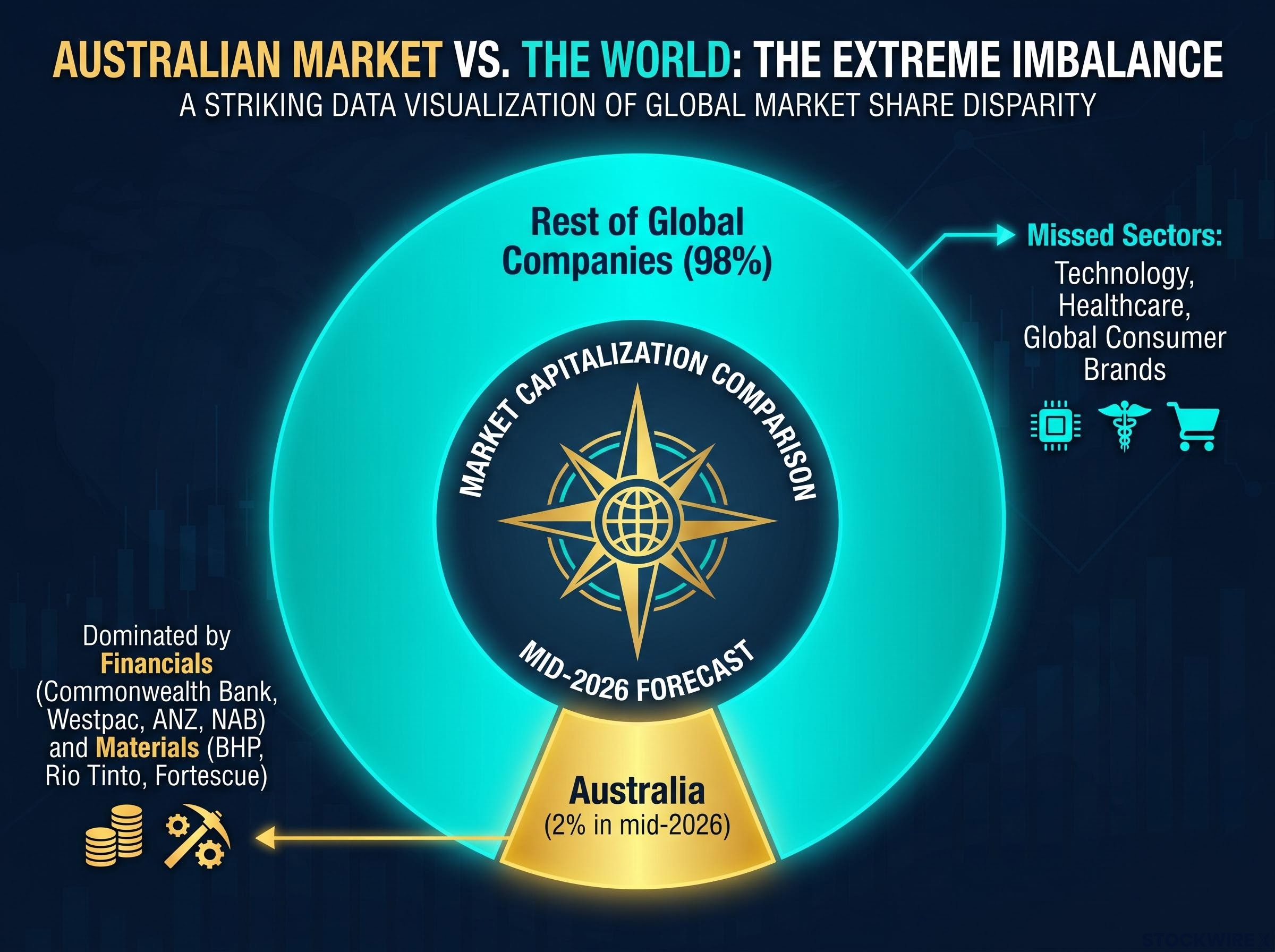

At roughly 2% of total global share market capitalisation, Australia occupies a very small slice of the world’s listed equity universe as of mid-2026. Looked at from the other direction, an ASX-only portfolio effectively ignores the remaining 98% of global companies, concentrating every dollar of your equity allocation in a single country’s market.

The gap matters more than it used to. The ASX’s index composition is heavily weighted toward financials and materials, with the big four banks and major miners commanding an outsized share of returns. Sectors such as technology, healthcare, and global consumer brands, which have been the primary engines of wealth creation internationally over the past decade, barely feature. Going global is not about chasing performance. It is about owning assets that do not all move in the same direction at the same time.

Here is the specific decision framework to work out how much of your portfolio should sit offshore, whether ETFs or direct shares suit your situation, and how to build a global allocation you can actually maintain.

Why the ASX alone leaves most Australian investors structurally exposed

The structural problem starts with concentration. The ASX is dominated by two sectors: financials (led by Commonwealth Bank, Westpac, ANZ, and NAB) and materials (led by BHP, Rio Tinto, and Fortescue). These names drive a disproportionate share of index returns, which means your portfolio’s fate is heavily tied to Australian banking margins, commodity cycles, and domestic economic conditions.

ASX 200 concentration risk is more severe than the index’s 200-stock label implies: financials and materials alone account for more than 50% of the index by market-cap weight, meaning a single large-cap event, such as Commonwealth Bank’s 10%-plus decline in May 2026, produces a measurable drag across the entire portfolio.

The S&P/ASX 200 sector composition data from S&P Dow Jones Indices shows financials at approximately 33% and materials at approximately 27% of the index as of mid-2026, confirming that these two sectors alone account for well over half of the benchmark your ASX-only portfolio tracks.

Australia represents approximately 2% of global share market capitalisation. An ASX-only portfolio is an enormous implicit bet that the Australian economy will continue to outperform 98% of the world’s listed companies, and most investors have never consciously made that bet.

When your entire equity allocation sits on the ASX, three consequences follow:

- Limited sector exposure: The index composition itself means you hold very little in technology or healthcare, two sectors that have driven the bulk of global equity gains. This is a structural feature of the ASX, not a matter of opinion.

- Currency concentration: All of your equity wealth is denominated in Australian dollars, which ties your returns to a single currency’s trajectory.

- Missed global growth sectors: The world’s largest consumer brands, semiconductor manufacturers, and pharmaceutical companies are listed offshore. You do not own them.

Understanding this gap shifts the question from “should I invest internationally?” to “how much, and in what form?”

When big ASX news breaks, our subscribers know first

How much of your portfolio should actually go global?

The instinct is to look for a single correct number. There is not one. But there is a well-supported range that gives you a starting point to calibrate rather than guess.

Research cited by Chris Brycki, Founder and CEO of Stockspot, indicates that allocating somewhere in the 40-60% range to domestic equities and the remaining 40-60% to international equities has historically produced an attractive combination of returns and risk reduction for Australian investors. Strictly following global market-cap weights would push Australian shares to a token position of around 2% of your portfolio. For investors based here, that approach is both unrealistic and tax-inefficient, as it takes no account of the franking credit system that benefits Australian shareholders.

At the extremes, the costs are clear. A 100% international portfolio sacrifices franking credit efficiency and can increase volatility. A 100% Australian portfolio is the structural concentration problem you just read about.

Matching your allocation to your situation

Where you sit within the 40-60% range is not a guess. It is a function of your tax bracket, your proximity to retirement, and how much of your total wealth is already tied to the Australian economy through property and employment. If you own a home in Sydney and work for an Australian employer, you already have significant exposure to the domestic economy before you buy a single share.

| Investor profile | Suggested split | Primary rationale |

|---|---|---|

| High tax bracket, income-focused, near or in retirement | 60% Australia / 40% international | Maximises franking credit benefits and stable AUD income |

| Long accumulation horizon, heavy existing Australian asset exposure | 40% Australia / 60% international | Offsets home bias from property and employment; less reliant on franking credits |

Neither profile is “right” in the abstract. The right one is the one that matches your actual circumstances.

What international ETFs actually give you (and what they cost)

An ASX-listed international ETF lets you buy exposure to hundreds or thousands of overseas companies in a single trade, using Australian dollars. One purchase might track the MSCI World ex-Australia index (covering developed markets globally) or the MSCI Emerging Markets index, giving you a slice of companies across dozens of countries and sectors without needing to open a foreign brokerage account or convert currency.

The simplicity of ETFs sits in three specific layers:

- Diversification is built into the instrument. You do not need to select individual stocks. One broad ETF spreads your money across countries, sectors, and thousands of companies, dramatically reducing single-company risk.

- Research burden is minimal. You are not following foreign earnings seasons or analysing individual businesses in unfamiliar regulatory environments. The return is the index minus fees, and broad international ETFs commonly charge management fees measured in basis points, not percentages.

- Tax and administration are handled largely by the fund manager. The ETF manager deals with foreign withholding tax and currency conversions behind the scenes. You report the components shown on your annual tax statement rather than tracking foreign tax obligations directly.

For most investors, the fact that an ETF cannot beat the index is not a concession. It is a feature. Reliably participating in global market returns at near-zero cost is a better expected outcome than attempting stock selection in markets where even professional managers rarely outperform over the long term.

Broad international ETFs such as VGS at 0.18% per annum and IVV at 0.04% per annum are the two instruments most commonly used by Australian investors to access the technology, healthcare, and consumer sectors that the ASX structurally under-represents, and both are available on the ASX without requiring a foreign brokerage account.

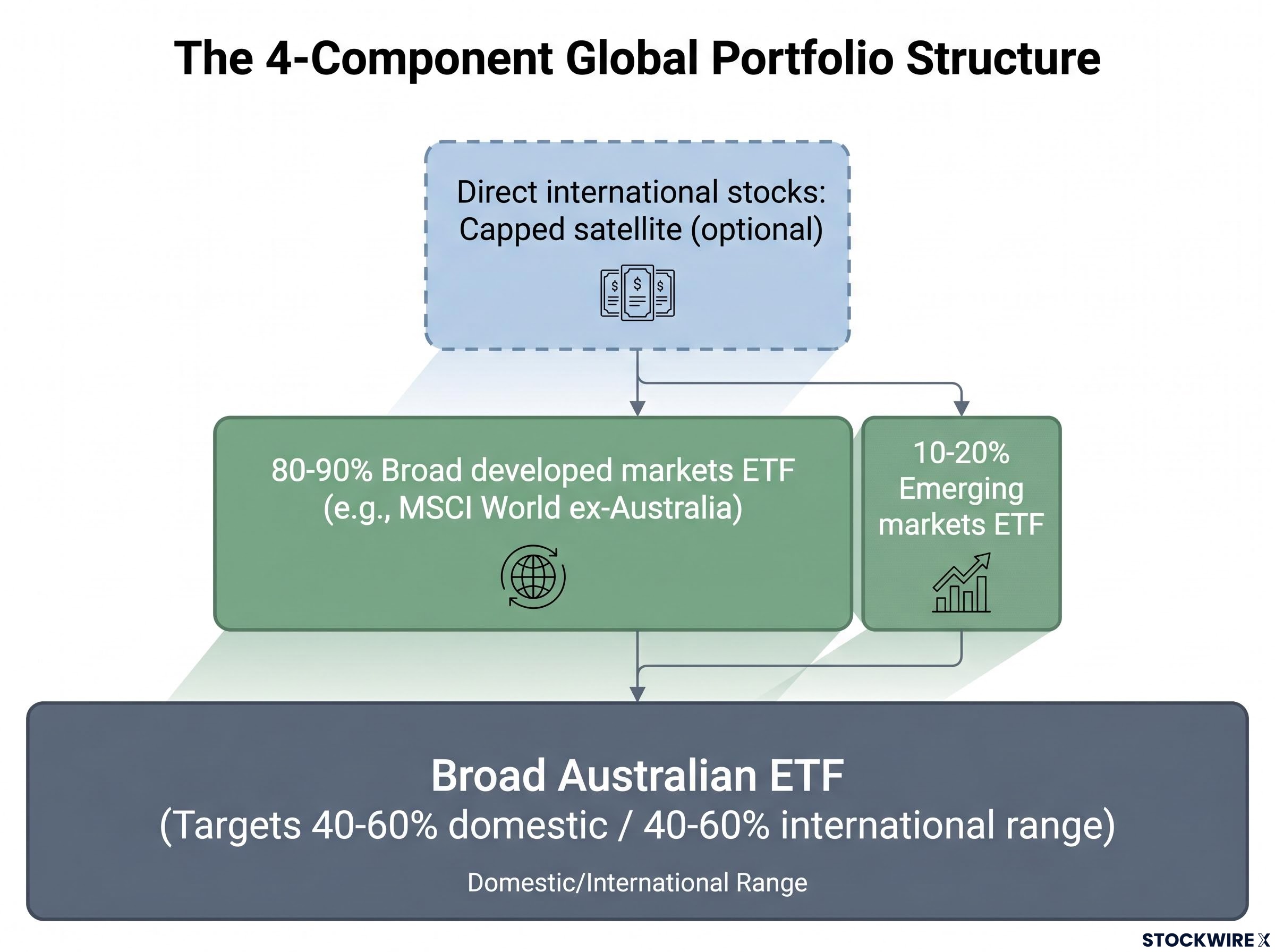

A practical international sleeve does not need dozens of funds. An allocation of 80-90% in a broad developed markets ETF and 10-20% in an emerging markets ETF covers most of what you need.

Tax and admin: what the fund handles and what you still need to do

With an ASX-listed international ETF, foreign withholding tax and currency conversions are processed by the fund manager rather than falling to you directly. Your annual ETF tax statement sets out the foreign income and offset figures you need. You still have reporting obligations on your Australian tax return for those foreign income components, but you are not personally reconciling withholding rates, converting transactions into AUD, or navigating the tax rules of each overseas market.

That is a meaningfully lighter burden than managing direct foreign shares, a point the next section makes concrete.

The honest case for direct international stock picking (and its limits)

Direct stock picking has genuine appeal, and pretending otherwise would not serve you. Owning specific companies feels tangible. You can target businesses or niches that no off-the-shelf ETF captures. And a concentrated, high-conviction portfolio can outperform a broad index, if the research process behind it is genuinely rigorous.

Those are the real advantages. Here are the honest costs:

- Research and monitoring burden. Doing serious analysis on foreign businesses means grappling with different time zones, unfamiliar regulatory environments, and local competitors you have never heard of. That is demanding for even a handful of stocks, let alone the 20-30 typically required for meaningful diversification.

- Concentration risk. Most retail investors who go global via direct shares end up with a cluster of US technology names. That is not a global portfolio. It is a concentrated bet on a single country and sector that will underperform badly if that theme falls from favour. If you call this “international diversification,” you are carrying more risk than you realise.

- Tax and currency complexity. For US shares, you need to complete a W-8BEN form to claim the treaty withholding rate of 15% on most dividends under the Australia-US tax treaty (current as of 2026). You must track your AUD cost base using exchange rates at both purchase and sale dates. Every additional market adds a separate layer of rules.

The Australia-US tax treaty dividend provisions confirm that withholding tax on dividends paid to Australian residents is capped at 15% of the gross dividend amount, the rate the W-8BEN form allows you to claim rather than the higher default rate that applies without it.

If your research process relies primarily on social media, podcasts, or financial headlines, you do not have a genuine analytical edge in international markets. Treat direct international stocks as entertainment and size them accordingly.

Direct stocks can work as a small, deliberate satellite sitting on top of a diversified core. They are rarely the right foundation for a global portfolio.

ETFs, direct shares, and the tax gap between them

The tax comparison between ETFs and direct shares is where the implementation decision becomes concrete. Neither approach eliminates foreign income reporting for Australian investors. The difference is who does the administrative work and how much of it falls on you.

| Tax consideration | ASX-listed international ETF | Direct foreign shares |

|---|---|---|

| Foreign withholding tax | Handled by the fund | Investor’s responsibility (e.g., W-8BEN for US shares) |

| Foreign income reporting | Annual tax statement from fund; investor reports components | Investor tracks and reports directly |

| Foreign tax offset | Typically handled via annual ETF tax statement | Investor calculates and claims directly |

| AUD cost base tracking | Not required at stock level | Required for every purchase and sale using FX rates |

| Complexity per additional market | Minimal | Adds a new layer of rules for each market |

All ATO foreign income reporting requirements, W-8BEN obligations, franking credit rules, and foreign tax offset provisions referenced above are current as of June 2026.

The row most investors underestimate is AUD cost base tracking. Every direct foreign share transaction requires you to record the exchange rate at purchase and again at sale, then calculate your capital gain or loss in Australian dollars. Across multiple markets, multiple transactions, and multiple years, this becomes a substantial compliance commitment.

The practical difference is not that ETFs are tax-free. They are not. It is that ETFs shift the operational complexity from you to the fund manager, which for most people represents dozens of hours of compliance work saved each tax year.

Hedged or unhedged? The currency decision most investors skip

When you buy an international ETF, you are also making a currency decision, whether you realise it or not. Most investors default to unhedged without understanding what that means.

An unhedged ETF exposes you to movements between the Australian dollar and foreign currencies. If the AUD falls against the US dollar, your returns improve in AUD terms. If the AUD rises, your returns are dampened. An unhedged ETF adds a second source of return variability on top of the underlying share market movement.

A hedged ETF uses financial instruments to reduce this currency exposure, producing returns closer to the underlying index in AUD terms. This costs a small ongoing fee and creates a slight drag over long periods.

Unhedged may suit you if:

- Your investment horizon is 10-plus years

- You are in the accumulation phase

- You can tolerate some return variability from currency movements

Hedged may suit you if:

- You will be spending the money in AUD within 5-7 years

- You are a retiree drawing income in AUD who wants less currency-driven volatility

- You have a very large international allocation where FX swings would meaningfully move your total wealth

Practical rule of thumb for the hedging decision

If your investment horizon is decades and you are not spending the money soon, unhedged is the sensible default. Currency movements over long periods tend to average out, and the hedging cost is a known drag on a benefit that may not materialise.

Investors with very large international allocations, where a sharp AUD move would meaningfully shift total portfolio value, may want to hedge a portion even on a longer horizon. But for most people in the accumulation phase, unhedged is simpler, cheaper, and historically adequate.

Investors wanting to model the actual return impact before committing to one structure will find our dedicated guide to hedged vs unhedged ETF returns useful: it examines the 13-percentage-point performance gap between HNDQ and NDQ over the year to May 2026, explains the FX forward mechanics behind currency hedging, and sets out the conditions under which each structure has historically come out ahead.

Building a global portfolio that is actually practical to maintain

The preceding sections gave you the components. Here is how they fit together into a structure you can implement this week.

- Start with a broad developed markets ETF. One fund tracking something like the MSCI World ex-Australia index forms the core of your international sleeve. This single holding gives you exposure to thousands of companies across the US, Europe, Japan, and other developed markets. Allocate 80-90% of your international sleeve here.

- Add an emerging markets complement. A small allocation of 10-20% of your international sleeve to an emerging markets ETF broadens your exposure beyond developed economies. Two funds handle the entire international side.

- Pair with a broad Australian ETF. Your domestic allocation captures franking credit benefits and Australian economic exposure. Target the 40-60% domestic / 40-60% international range that matches your profile from the earlier section.

- Add direct international stocks only as a capped satellite (optional). If you have genuine analytical interest, discipline, and a real research process, a small allocation to individual international stocks can sit on top of the ETF core. It supplements the diversified foundation. It never replaces it.

The right question is not how much upside you want from direct stocks, but whether a total loss on any single position would materially damage the portfolio. If the answer is yes, the satellite is too large.

That four-component structure, two international ETFs, one domestic ETF, and an optional direct stock satellite, is enough. You do not need dozens of country or sector funds. Simplicity is what makes a portfolio maintainable over decades.

Choosing the right approach for your situation

For most Australian investors, broad international ETFs are the right core vehicle. They deliver built-in diversification, fees measured in basis points, and substantially simpler tax administration than direct foreign shares. Direct stocks have a legitimate role, but only as a small, deliberate satellite for investors who have the time, interest, and a genuine research process.

Three variables should drive your final decision:

- Analytical edge. Do you have a genuine research process for the specific markets you want to access, or is your conviction based on enthusiasm and headlines?

- Tax and admin tolerance. Are you willing to track AUD cost bases, file W-8BEN forms, and manage foreign income reporting across multiple markets as an ongoing commitment, not just once?

- Existing allocation baseline. Have you already established a sensible domestic/international split, or are you bolting on international stocks without a framework?

The investor who builds an ETF core first and adds direct stocks later, if at all, is making the more defensible sequencing decision. The core protects you from the consequences of being wrong on individual stocks, while the satellite gives you room to express high-conviction views without jeopardising the foundation.

International equity outperformance is no longer a theoretical case: emerging markets ex-China delivered approximately 31.5% year-to-date versus approximately 9.3% for the S&P 500 ETF as of May 2026, with Yardeni Research’s data showing a historically wide valuation gap of 21.3x forward P/E for US equities versus 13.7x for the rest of the world.

Your next step is straightforward. Confirm your Australian/international allocation target using the profiles above. Select one or two broad ETFs to build the core. Then decide whether direct stocks belong in your satellite, or not at all.

This article is for informational purposes only and should not be considered financial advice. Investors should conduct their own research and consult with financial professionals before making investment decisions.