How to Value Westpac Shares Using PE and DDM

55 mins ago

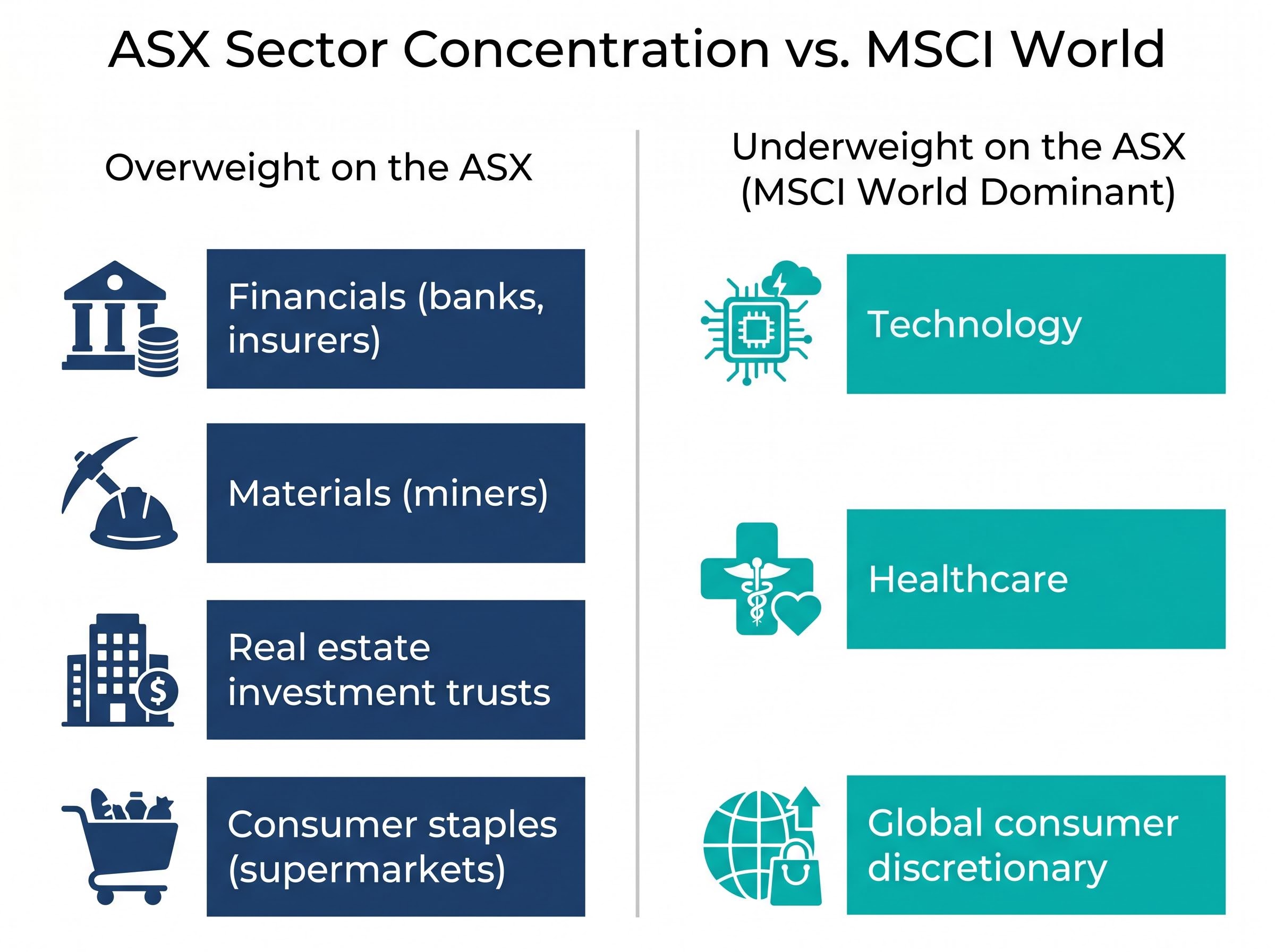

The ASX contains roughly 2,000 listed companies, yet a portfolio built across the top holdings would be overwhelmingly weighted toward four industries: banks, miners, supermarkets, and real estate. For Australian investors who believe they are diversified because they hold a local index fund, this sector concentration is the structural blind spot that a global quality ETF is designed to address.

Technology and healthcare have driven the majority of global equity returns over recent market cycles, yet an ASX-only allocation quietly excludes investors from those growth engines. The rise of rules-based, quality-screened global ETFs listed on the ASX gives retail investors a direct mechanism to fill that gap, without requiring the expertise to individually evaluate hundreds of international companies. This article explains what a global quality ETF actually is, how the quality screening philosophy works, which ASX-listed options exist, what the genuine trade-offs are, and how to think about whether this kind of allocation fits a broader portfolio.

A standard ASX index fund feels diversified. It holds dozens of companies across multiple industries. Look closer, though, and the sector composition tells a different story.

The ASX is dominated by financials and materials. Banks and mining companies account for the largest share of the index by market capitalisation, and when property trusts and consumer staples (primarily supermarkets) are added, the concentration becomes stark. The sectors that have generated the most significant wealth globally over the past decade are either absent or structurally underweight.

ASX 200 concentration risk extends further than most investors realise: VanEck research shows that just two stocks have historically represented approximately 22% of a typical cap-weighted Australian equity portfolio, meaning a single large-cap event can produce a meaningful drag across the entire index.

The contrast with the MSCI World Index makes the gap visible:

The technology sector alone represents a larger share of the MSCI World Index than any single sector represents on the ASX, yet Australian investors holding only domestic equities have minimal direct exposure to it.

This is not a temporary anomaly. The ASX reflects the structure of the Australian economy: a resource-rich, bank-heavy market with limited representation in the industries driving global innovation. An investor holding only Australian equities is not poorly invested. They are, however, structurally absent from the sectors that have compounded most aggressively at a global level.

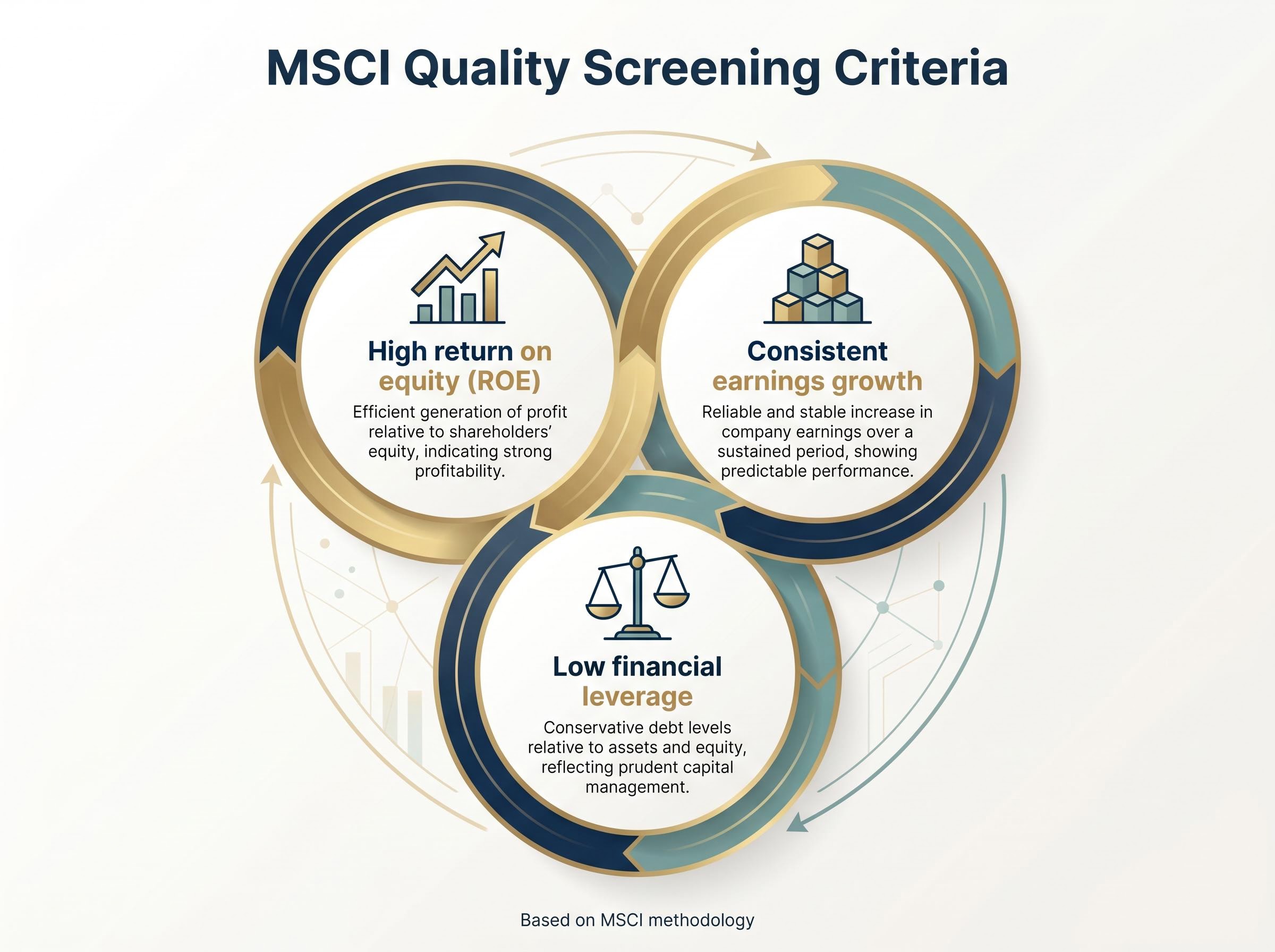

The assumption is intuitive: large, well-known companies are good investments. But financial quality, as a measurable characteristic, has nothing to do with brand recognition or market capitalisation.

Rules-based quality screening evaluates companies against three specific financial criteria:

These three metrics, as used in MSCI’s quality methodology, capture something distinct from size. A company can be among the largest in the world and still fail quality screens if its earnings are cyclical, its balance sheet is heavily leveraged, or its return on equity is inconsistent.

A standard index fund selects holdings by company size. If a business is large enough, it stays in the index regardless of whether its earnings are volatile, its debt levels are elevated, or its returns on equity are declining.

Cap-weighted index construction is the mechanism that makes this concentration self-reinforcing: as large companies grow, their index weight increases and index-tracking funds must buy more of them, regardless of whether those companies continue to meet any quality or earnings criterion.

Quality screening applies a financial filter on top of the universe. It selects for characteristics associated with business durability rather than sheer scale. The result is a portfolio tilted toward companies with durable competitive advantages: businesses that compound returns over time because their financial foundations support it, not because their market capitalisation once reached a threshold.

The term “rules-based” is specific and worth understanding. It means no individual fund manager is making discretionary calls about which companies belong in the portfolio. The index methodology defines the screening criteria. The ETF tracks the index. Inclusion and exclusion are governed by measurable financial characteristics, not subjective judgement.

The role of the index provider, in this case MSCI, is to set and maintain those criteria. When company financials change (earnings decline, leverage increases, or return on equity deteriorates), the index reconstitution process updates the portfolio accordingly. This happens systematically, on a defined schedule, across the full universe of eligible securities.

The key structural features of the mechanism:

QUAL, the VanEck MSCI International Quality ETF, tracks the MSCI World ex Australia Quality Index. That index holds 294 securities and applies quality screens across developed market equities outside Australia. Holdings include globally recognised businesses such as Nvidia, Apple, and Microsoft, illustrating the type of companies the screen captures. The fund excludes Australian-listed companies by design, making it a clean complement to an existing ASX allocation.

When an investor buys a rules-based quality ETF, they are not delegating stock selection to a portfolio manager’s intuition. They are buying a transparent, repeatable methodology that can be evaluated once and then held with confidence that it will be applied consistently.

Three quality-focused global ETFs are readily available on the ASX, each with distinct characteristics. A fourth option, IQLT from iShares, has been identified but key data points remain unverified at the time of writing.

| ETF Ticker | Provider | Management Fee | Hedged/Unhedged | Key Feature |

|---|---|---|---|---|

| QUAL | VanEck | 0.40% p.a. | Unhedged | $8.49 billion in net assets; 294 securities; inception October 2014 |

| QLTY | BetaShares | 0.35% p.a. | Unhedged | International equities screened for quality characteristics |

| HQLT | BetaShares | 0.35% p.a. | AUD-hedged | Hedged version of QLTY; removes currency exposure |

The fee range across these products sits at 0.35%-0.40% p.a. That is meaningfully higher than broad passive MSCI World ETFs available on the ASX, which typically carry management fees in the range of 0.07%-0.20% p.a. The premium reflects the cost of the quality screening methodology applied on top of the base universe.

The distinction between hedged and unhedged matters. HQLT removes AUD/USD currency exposure from returns, isolating the underlying equity performance. QUAL and QLTY leave currency exposure intact, meaning the Australian dollar’s movement against major currencies directly affects returns.

Note: Funds under management figures for QLTY and IQLT were not independently confirmed at the time of research. Investors should consult each fund’s current product disclosure statement or factsheet for the most accurate figures.

Quality ETFs are not risk-free instruments, and three genuine limitations deserve direct acknowledgement:

The cyclical lag issue is the most commonly misunderstood. Quality stocks, by definition, are financially stable businesses. During periods of high risk appetite, capital often rotates toward more speculative names, and quality strategies trail. This is not a malfunction; it is a structural feature of the factor. QUAL’s six-month return of -2.76% as at April 2026 illustrates that the fund experiences short-term drawdowns and is not a defensive instrument in all conditions.

The fee drag is straightforward arithmetic. An investor choosing QUAL at 0.40% p.a. over a broad MSCI World ETF at 0.07%-0.20% p.a. pays an additional 0.20%-0.33% p.a. for the quality factor tilt. Over a decade or more, that differential compounds. The implicit bet is that quality factor outperformance will exceed this cost. It is not guaranteed.

The management fee differential between quality-screened ETFs and the cheapest broad-market alternatives is more consequential than it appears in isolation: across the 12 largest global equity ETFs on the ASX, costs range from 0.03% to 1.35% per annum, and combined costs consumed more than 25% of one actively managed fund’s three-year net gains.

QUAL’s 10-year annualised return of 14.94% p.a. (as at April 2026) demonstrates that the quality factor has delivered meaningful long-term compounding, but this figure reflects a specific historical period and does not guarantee future results.

Currency risk affects all unhedged international allocations. If the Australian dollar strengthens against the US dollar and other major currencies, unhedged returns are reduced in AUD terms, regardless of how the underlying equities perform. HQLT exists specifically for investors who want to isolate this variable.

Understanding the product is one step. Knowing where it fits is another.

A global quality ETF addresses a specific problem: the ASX’s sector concentration. It is a complement to domestic equity exposure, not a replacement for it. The construction logic follows three steps:

QUAL’s three-year annualised return of 15.82% p.a. and five-year annualised return of 13.02% p.a. (as at April 2026) indicate that the quality factor has compounded meaningfully over medium-to-long horizons. The fund’s $8.49 billion in net assets reflects significant adoption by Australian investors. Past performance, however, does not guarantee future results, and quality strategies are designed for long-term holding horizons rather than short-term tactical trades.

Unhedged exposure means AUD/USD fluctuations directly affect returns in Australian dollar terms. If the Australian dollar weakens, unhedged returns are amplified. If it strengthens, returns are reduced. For investors with a long time horizon, this currency diversification can serve as a natural hedge against domestic economic weakness.

Hedged versions such as HQLT remove this variable, making performance more directly reflective of the underlying company returns. The trade-off is the loss of that natural currency diversification, along with a slightly different risk profile. Neither approach is inherently superior; the decision depends on the investor’s view of currency movements and their tolerance for an additional source of return variability.

The ASX’s structural sector concentration is a permanent feature of the market, not a temporary anomaly. Banks and miners will continue to dominate the local index because they reflect the structure of the Australian economy. For investors seeking exposure to the global sectors driving long-term wealth creation, that concentration gap needs to be addressed directly.

Global quality ETFs represent one of the most accessible mechanisms available. Rules-based financial screening replaces the impossible task of individually evaluating hundreds of international companies with a transparent, repeatable methodology. The trade-offs are real: fee drag, cyclical lag risk, and currency exposure all require consideration.

Investors who have followed this explanation are now equipped to read product disclosure statements, compare management fees across available options, and evaluate whether a quality ETF allocation aligns with their time horizon and portfolio goals. The blind spot does not fix itself. Addressing it is a deliberate decision.

For investors ready to extend their international allocation beyond a single quality ETF, our full explainer on diversifying beyond the ASX covers how MOAT’s durable competitive advantage screen and VAE’s Asia-Pacific exposure can serve as complementary satellite positions around a broad-market or quality-factor core.

This article is for informational purposes only and should not be considered financial advice. Investors should conduct their own research and consult with financial professionals before making investment decisions. Past performance does not guarantee future results.

A global quality ETF is a rules-based fund that selects international company holdings using measurable financial criteria, typically high return on equity, consistent earnings growth, and low financial leverage, rather than simply tracking companies by market size.

A standard index fund selects holdings based on market capitalisation, meaning large companies stay in the index regardless of their earnings stability or debt levels, while a quality screen applies a financial filter that excludes companies with volatile earnings, high leverage, or declining returns on equity.

Three readily available options are QUAL from VanEck (0.40% p.a., unhedged, with approximately $8.49 billion in net assets), QLTY from BetaShares (0.35% p.a., unhedged), and HQLT from BetaShares (0.35% p.a., AUD-hedged).

The three key trade-offs are cyclical lag (quality strategies can underperform during speculative rallies), fee drag (quality ETFs charge 0.35%-0.40% p.a. compared to 0.07%-0.20% for broad-market alternatives), and currency risk for unhedged options, where AUD movements affect returns independently of equity performance.

The ASX is heavily concentrated in financials, materials, real estate, and consumer staples, with minimal exposure to technology and healthcare, which are the sectors that have driven the majority of global equity returns over recent market cycles.