Why Buffett Only Needed 5 Great Opportunities in 60 Years

13 hrs ago

Most “global” ETFs are already more than half American. If you hold one, your international equity exposure is overwhelmingly US large-cap, whether you chose that weighting or simply inherited it. That is not necessarily wrong, but it is worth knowing whether it was a decision or a default.

Australian investors building international equity exposure through the ASX have a straightforward alternative. Pair one ETF covering everything outside the United States with one covering the US directly, and choose the split yourself. The two building blocks are VEU (Vanguard All-World ex-US Shares Index ETF) for international markets beyond American shores, and either IVV (iShares S&P 500 ETF) or NDQ (Betashares Nasdaq 100 ETF) for the US sleeve.

This guide walks you through exactly how the two-ETF structure works, what each fund holds, how to choose your US versus non-US split, and what the practical setup looks like, from currency exposure to rebalancing. By the time you finish, you will be able to build a global portfolio using ASX ETFs with an allocation you have chosen deliberately rather than accepted by default.

The defining feature of VEU is what it deliberately leaves out. The fund tracks the FTSE All-World ex US Index, a free-float, market-cap weighted index (meaning each company’s weight reflects its publicly tradeable shares, scaled by its total market value) that covers both developed and emerging markets outside the United States. Every company listed in New York is excluded. What remains is roughly the rest of the investable world.

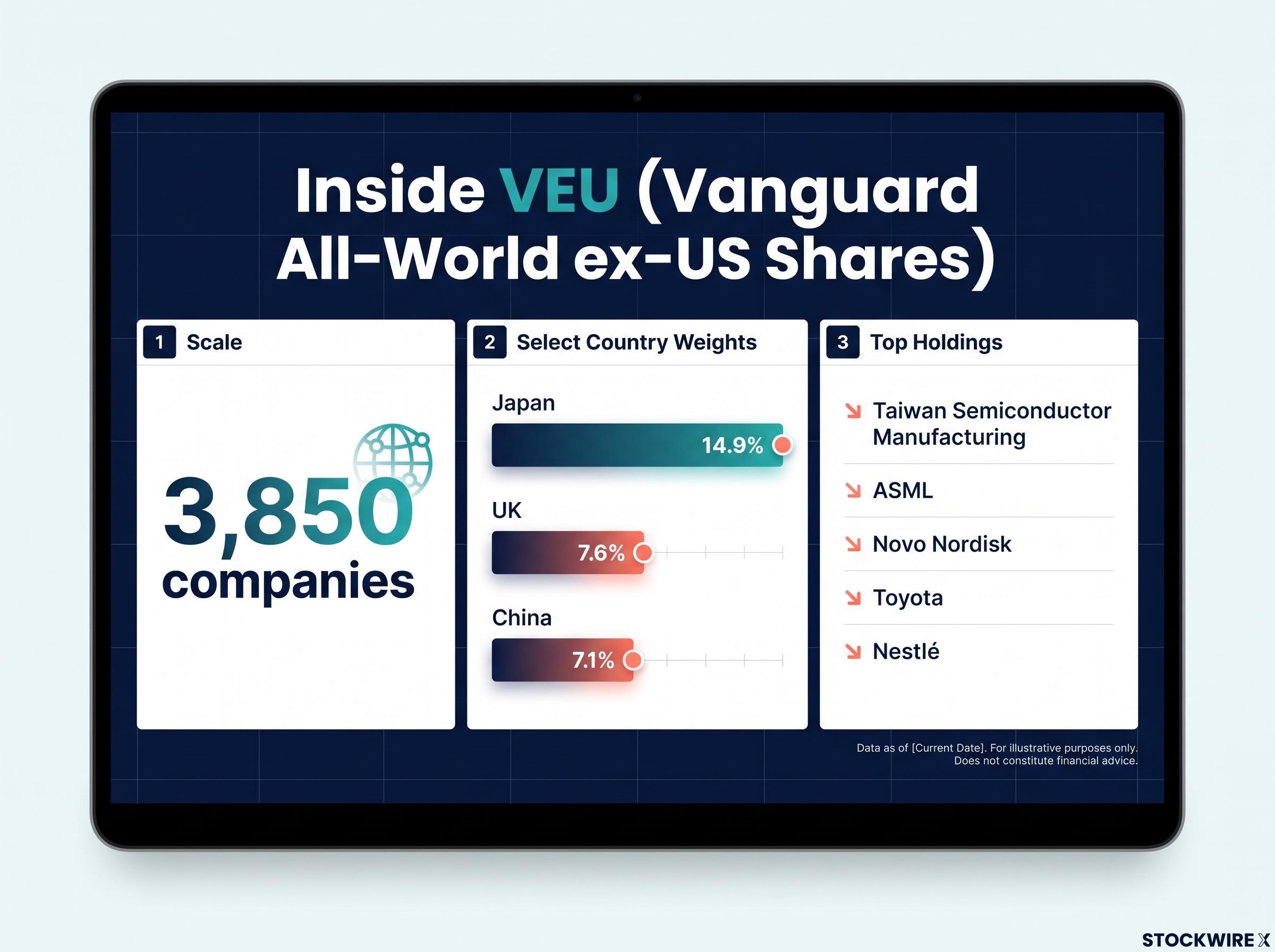

That “rest” is substantial. VEU holds approximately 3,850 companies across:

The top holdings read like a roster of the largest non-American companies on earth: Taiwan Semiconductor Manufacturing, ASML, Novo Nordisk, Toyota, and Nestlé. Country weightings give you a sense of the geographic spread: Japan at approximately 14.9%, the UK at approximately 7.6%, and China at approximately 7.1%, with broad exposure stretching across Europe, the Asia-Pacific, and Latin America.

As of 31 May 2026, the fund’s asset allocation sits at approximately 93% international equities, roughly 4% Australian equities, and small amounts of cash and listed property.

The cost of accessing all of this is almost negligible.

Management fee: approximately 0.04% per annum

The Indirect Cost Ratio is approximately 0.07%. For context, you would need to hold more than $100,000 in VEU before your annual management fee reached $40.

On the income side, VEU has delivered a 5-year average dividend yield of approximately 2.5-2.6% per annum, fully unhedged. That “unhedged” detail matters: your distributions arrive in Australian dollars, but their value reflects the underlying foreign currencies. When the AUD weakens against those currencies, your income rises in AUD terms. When the AUD strengthens, it falls. The fee and breadth together tell you something practical: you are getting multi-market exposure to nearly 3,850 companies for a cost that rounds to zero, which is why VEU works as a portfolio building block rather than a standalone curiosity.

VEU’s five-year return profile sits above 10% annualised alongside NDQ and VGS, and all three trade on the ASX in Australian dollars through a standard brokerage account, which gives you a direct comparison of how VEU performs relative to its most common portfolio partners.

Before you add anything international, consider what your portfolio probably already looks like. If you are a typical Australian self-directed investor, your equity holdings are concentrated in two stories.

Vanguard Australia research on home country bias shows that Australian investors have historically held a disproportionate share of domestic equities relative to Australia’s weight in global market-cap indices, reducing exposure to international return sources that have outperformed in multiple market cycles.

What a typical Australian portfolio already holds:

What VEU adds:

The gap is not small. Entire regions and sectors that represent major parts of the global economy, European healthcare, Japanese precision manufacturing, emerging-market consumer growth, are simply absent from a portfolio built around domestic financial stocks and American technology companies.

The structural gap in ASX composition explains much of this divergence: financials and materials together exceed 50% of ASX 200 market-cap weight, and the index carries no large-cap technology companies and no semiconductor exposure, making it unable to participate in the themes that have driven global outperformance in 2026.

Markets that do not move in lockstep with the S&P 500 or ASX 200 reduce your portfolio’s concentration risk. European industrials led returns during the commodity supercycle of the early 2000s. Japanese manufacturers and exporters have outperformed in periods of yen weakness and global trade expansion. Emerging markets have delivered their strongest relative performance when structural growth themes, expanding working-age populations, rising middle-class consumption, and infrastructure build-out, have been their primary drivers.

These themes are largely absent from a portfolio built around Australian financials and US technology. For you, that means large parts of the global economy’s growth story are not represented in your holdings. Names like ASML, Novo Nordisk, and Toyota are not niche picks; they are among the largest companies in the world, and they are missing from the typical Australian investor’s portfolio entirely.

The concept is simple enough to sketch on the back of an envelope. You hold one ETF for US equities, one ETF for everything else, and you choose the split between them.

Your US-side options come down to two:

IVV tracks the S&P 500 Index: 500 large US-listed companies spread across all major sectors. It gives you broad, diversified US exposure, mixing growth and value names, and functions as a core holding.

NDQ tracks the Nasdaq-100 Index: heavily weighted to US technology and communication services, more growth-oriented, and more volatile. Choosing NDQ over IVV as your US sleeve is not a neutral decision. It means you are explicitly tilting your entire global portfolio toward US tech growth, and you should make that call consciously rather than by default.

Here is what a market-like starting point looks like:

| ETF | Index tracked | Holdings (approx.) | Role in portfolio | Allocation |

|---|---|---|---|---|

| IVV | S&P 500 | 500 | Core US large-cap | 60% |

| VEU | FTSE All-World ex US | 3,850 | Developed + emerging ex-US | 40% |

The outcome: exposure to approximately 3,850 ex-US companies via VEU plus 500 US large caps via IVV, covering most investable global markets with a split you have chosen rather than inherited.

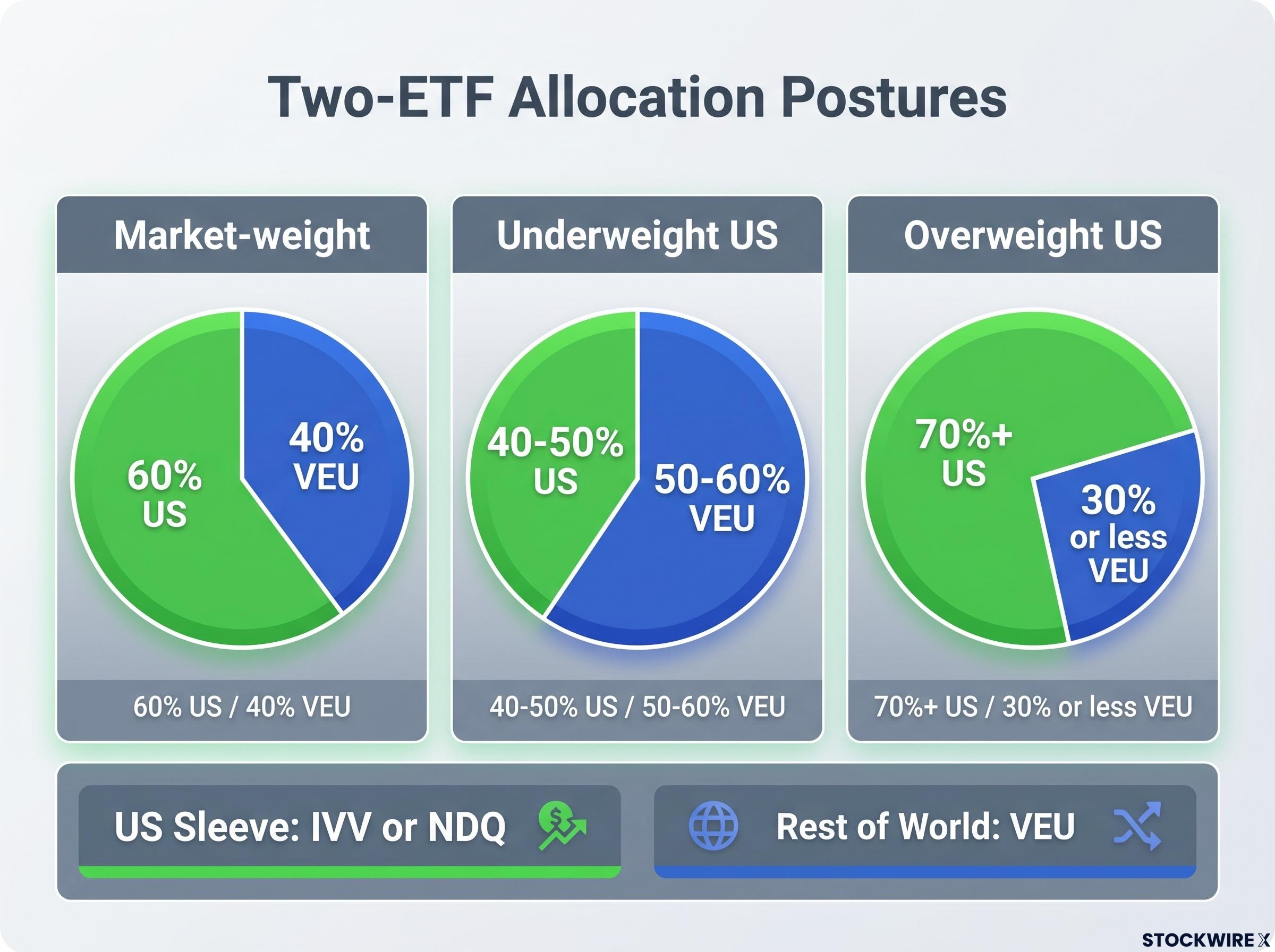

Three allocation variations give you structured options:

Global market-cap indices currently allocate roughly 60-65% to the US and 35-40% to the rest of the world. That gives you a neutral reference point, not a prescription.

The real question is whether you have a view on that weighting or not. Here are the three postures and the reasoning behind each:

| Allocation posture | US ETF allocation | VEU allocation | Suits investors who… |

|---|---|---|---|

| Market-weight | 60% | 40% | Want broad global exposure without taking a geographic bet |

| Underweight US | 40-50% | 50-60% | See better value or stronger diversification in non-US markets |

| Overweight US | 70%+ | 30% or less | Have conviction in US earnings growth and innovation leadership |

None of these is the “correct” answer. The point is that you are explicitly choosing your US weight rather than accepting whatever a single global fund’s market-cap rules happen to produce.

If you currently hold only an S&P 500 ETF, your international equity sleeve is 100% US-weighted. That is itself an allocation decision, whether you made it deliberately or not. The two-ETF structure does not tell you what the right number is. It gives you the mechanism to set it yourself and adjust it over time as your views evolve.

The single global ETF case is genuine. One holding gives you automatic market-cap rebalancing, broad diversification, and zero decisions about regional splits. For an investor who does not have a view on geographic allocation and values simplicity above all else, it works.

The limitation is equally genuine. Geographic weights in a single global fund are fixed by market size, not by your preference. At current valuations, that means accepting 60% or more in US equities by default. You cannot dial it down or up without selling and buying something different.

| Criteria | Single global ETF | VEU + US ETF |

|---|---|---|

| Holdings required | One | Two |

| Geographic control | None (market-cap determined) | Full (you set the US vs non-US split) |

| Rebalancing approach | Automatic via index | Manual (annual or drift-based) |

| Best suited for | Investors who want zero geographic decisions | Investors who want explicit allocation control |

The complexity increase is modest: two tickers instead of one, with the same broad global coverage. The flexibility gain is meaningful: you can swap the US-side ETF (IVV to NDQ or vice versa) or adjust the split over time without changing your overall portfolio architecture.

The honest question is whether you have an actual view on your US versus non-US weighting. If you do, the two-ETF approach is simply the mechanism that lets you act on it. If you do not, a single global fund serves you without penalty.

Your ETF portfolio structure, specifically the number of funds you hold and the asset allocation between them, has a greater influence on long-term outcomes than any individual fund selection decision, a principle that applies whether you are running two funds or six.

Strategy is one thing. What happens once you hold these funds is another.

Currency exposure is the most commonly misunderstood element. VEU, IVV, and NDQ are unhedged on the ASX, which means AUD fluctuations directly affect the value of your holdings in Australian dollar terms. A weaker AUD amplifies your overseas returns; a stronger AUD reduces them. Hedged versions of international ETFs exist and offer more stable AUD returns, but they typically carry higher total costs.

The natural buffer: Unhedged international exposure has historically provided Australian investors a cushion during domestic economic downturns. When Australian conditions deteriorate, the AUD typically weakens, lifting the value of your overseas holdings at the same time. Your international sleeve tends to rise in AUD terms precisely when your domestic sleeve is under pressure.

Tax considerations require attention but not alarm. Foreign withholding taxes apply to distributions from international ETFs, and tax reporting differs from purely domestic funds. The Product Disclosure Statement for each fund outlines these implications, and Australian investors benefit from checking the relevant PDS and considering specialist tax advice for their personal situation.

Rebalancing keeps your allocation on track. If you are targeting a 60/40 split, market movements will cause drift over time. The preferred method avoids triggering unnecessary capital gains events:

For investors who want a detailed walkthrough of the rebalancing execution process, our dedicated guide to portfolio rebalancing for Australian investors covers the super and SMSF-specific pathways that make rebalancing more tax-efficient than selling inside a taxable account, including the 5% drift threshold most Australian advisers recommend as a trigger.

This article is for informational purposes only and should not be considered financial advice. Investors should conduct their own research and consult with financial professionals before making investment decisions.

The two-ETF approach is not more sophisticated than a single global fund. It is more intentional. That distinction matters only if you have a view on geographic concentration you want to act on.

This approach suits you if:

If none of those describe you, a single global ETF is a perfectly sound alternative, and knowing that is itself a product of thinking through the decision deliberately.

For investors who do want the control, starting with a 60/40 IVV/VEU split mirrors global market-cap weighting and requires minimal ongoing decisions. Both IVV and VEU are available on major Australian brokers and accessible to retail investors. It is a low-friction entry point that you can adjust as your conviction develops.

The investor who reads this guide and decides a single global fund is sufficient for their needs has still gained something. You are now making that choice deliberately rather than by default, which is the actual goal of intentional portfolio construction.

The Product Disclosure Statements for each ETF and licensed financial advice are the appropriate resources for personal investment decisions. Past performance does not guarantee future results.

VEU is the Vanguard All-World ex-US Shares Index ETF, which tracks the FTSE All-World ex US Index and holds approximately 3,850 companies across developed and emerging markets outside the United States, including Japan, the UK, China, and India, at a management fee of around 0.04% per annum.

Pair VEU for non-US international exposure with either IVV (S&P 500) or NDQ (Nasdaq-100) for US exposure, then choose your own split, such as 60% IVV and 40% VEU to mirror global market-cap weighting, and rebalance annually by directing new contributions to the underweight fund.

A single global ETF automatically allocates roughly 60% or more to US equities by market-cap rules, giving you no control over that weighting; VEU deliberately excludes the US, so pairing it with a separate US ETF lets you set the US versus non-US split yourself and adjust it over time.

No, all three ETFs are unhedged on the ASX, meaning AUD fluctuations directly affect the value of your holdings in Australian dollar terms; a weaker AUD amplifies overseas returns, while a stronger AUD reduces them.

An annual rebalancing check is a common cadence; the preferred approach is to direct new contributions toward the underweight ETF first, and only sell holdings to rebalance when drift exceeds a 5-10 percentage point threshold from your target allocation.