A 5-Step Framework for Valuing Slowing Growth Stocks

10 hrs ago

Most investors know that profit matters. Fewer know that profit and cash are not the same thing, and that the gap between them is where business quality is often hiding.

Free cash flow is the metric sophisticated investors use to distinguish companies that genuinely generate money from those that merely report it on paper. A growing number of ETFs, including the Betashares Global Cash Flow Kings ETF (ASX: CFLO), now use this metric as the central filter for building portfolios. Understanding what free cash flow is, and why it matters, gives you a lens that extends well beyond any single fund.

This guide builds that lens from the ground up: what free cash flow actually measures, how it differs from accounting profit, why ETFs built around it behave differently from standard index funds, and what to check before adding one to your portfolio. Here is the framework for making an informed decision about whether a free cash flow ETF belongs in your portfolio.

A company can report a profit and still be running out of cash. That is not a contradiction; it is a feature of how accounting works. And it is the single most important gap for you to understand before evaluating any investment built around cash flow.

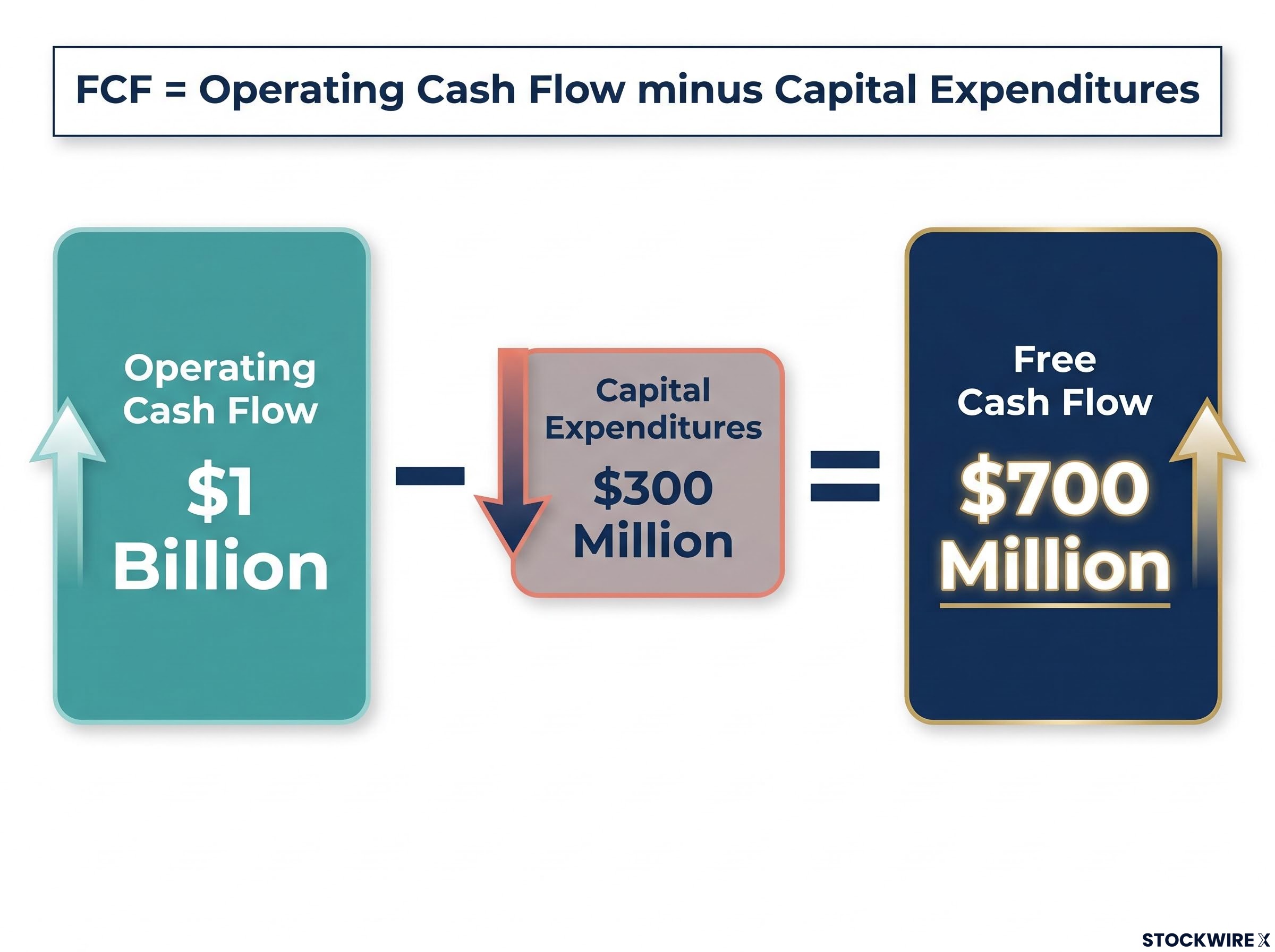

Free cash flow (FCF) strips away the accounting layer and measures something simpler: how much actual cash a business generates after it has paid for the equipment, property, and infrastructure it needs to keep operating. The formula is straightforward.

FCF = Operating Cash Flow minus Capital Expenditures

To make that concrete: a company generating $1 billion in operating cash flow and spending $300 million on capital expenditures produces $700 million in free cash flow. That is real money the business can use however it chooses.

Strong free cash flow signals several things about a business:

Accounting earnings can be shaped by non-cash items such as depreciation (spreading the cost of an asset over many years) and amortisation (doing the same for intangible assets like patents). Accrual accounting, where revenue and expenses are recorded when earned or incurred rather than when cash changes hands, adds another layer of abstraction.

The result is that a company can look profitable on its income statement while its actual cash position is deteriorating. FCF cuts through that. It measures real money moving through the business, which is harder to adjust through accounting choices.

That gap between reported profit and actual cash flow is where business quality hides, and understanding it changes how you read any company’s financial story.

Once you understand what free cash flow is, the next question is practical: what can a business actually do with it? The answer is where the concept shifts from accounting to competitive advantage.

Companies with strong FCF have five primary options, roughly in order of balance sheet logic:

The common thread across all five is financial flexibility. A business generating strong free cash flow does not need to ask permission from lenders or shareholders to fund its next move.

Cash-generative companies do not need to borrow or dilute shareholders to fund their next move. That independence is a competitive advantage, not just a balance sheet metric.

This is why institutional investors treat high FCF as a quality signal, not merely a value signal. When markets contract and credit tightens, cash-generative businesses can keep operating and investing while peers with thin margins and low cash generation are constrained. That asymmetry is exactly what a cash-flow-screened ETF is designed to capture.

Everything you have read so far is the investment thesis. CFLO is the practical application.

The Betashares Global Cash Flow Kings ETF is a rules-based, index-tracking factor ETF that uses free cash flow metrics as its primary selection filter. It is not an actively managed fund where a portfolio manager picks stocks based on discretion. Instead, CFLO tracks a published index with defined rules for which companies qualify, how they are weighted, and when the portfolio is rebalanced.

Among the fund’s representative holdings, you will find capital-light, high-margin businesses such as Visa (NYSE: V) and Costco (NASDAQ: COST) sitting alongside technology giants like NVIDIA (NASDAQ: NVDA), each selected because of their strong cash generation relative to peers.

CFLO’s index methodology defines specific criteria a company must meet to be included, weighted, and retained during rebalancing. This rules-based approach means the cash flow screen does the filtering, not a manager’s subjective judgment. You should review the published index methodology directly before investing to understand exactly what “cash flow king” means in practice.

ASIC Regulatory Guide 282 sets the disclosure and operational obligations that ETF issuers must meet for ASX-listed products, covering portfolio transparency, liquidity requirements, and market-making arrangements that underpin the structure of funds like CFLO.

Knowing that CFLO is a factor ETF, not a standard index fund, tells you something important: its returns will diverge from a broad market index by design. That divergence is the point.

A quality screen shares meaningful philosophical ground with a cash flow screen: both tilt away from capital-intensive businesses toward companies with durable earnings, low leverage, and high returns on invested capital, though the specific metrics each methodology prioritises can produce noticeably different sector and stock-level outcomes.

To see how this plays out structurally, here is how CFLO compares to other common ETF types:

| ETF Type | Primary Selection Criterion | What It Prioritises |

|---|---|---|

| Market-cap index fund | Company size (total market value) | Broad market representation |

| Growth ETF | Revenue or earnings growth rate | Expansion potential |

| Dividend ETF | Dividend yield or payout history | Income distribution |

| Cash flow ETF (e.g. CFLO) | Free cash flow generation | Financial quality and flexibility |

Many beginner investors assume all ETFs are broadly similar. Understanding the structural difference between a factor ETF and a market-cap index fund is one of the most important steps in setting realistic return expectations and knowing what role any fund plays in your portfolio.

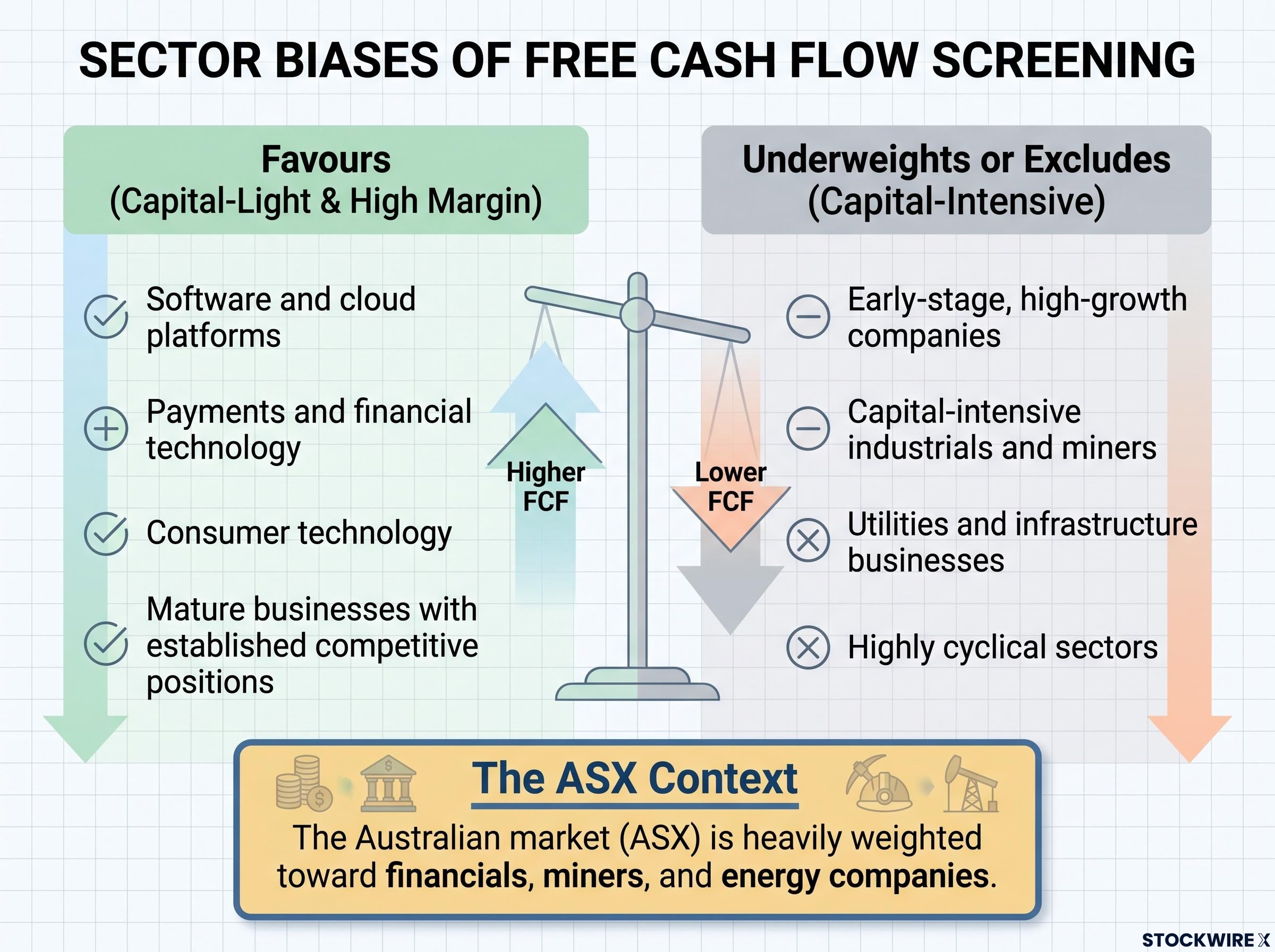

A free cash flow filter does not select from every corner of the market equally. It is a deliberate tilt, and the sectors it favours (and avoids) tell you a lot about what you are actually buying.

FCF screens naturally favour capital-light business models, the types of companies that generate high margins without needing to spend heavily on physical infrastructure:

Conversely, FCF screens tend to underweight or exclude:

This is not a flaw. It is the filter working as intended. You are not buying the broad market with CFLO; you are intentionally tilting toward businesses that convert revenue into cash efficiently.

For Australian investors with existing ASX exposure, this tilt carries a specific benefit. The ASX is heavily weighted toward financials, miners, and energy companies. A global FCF-screened fund like CFLO provides meaningful diversification away from those sectors precisely because it underweights the types of businesses that dominate the local market.

ASX sector concentration is the structural backdrop that makes a global FCF-screened fund a meaningful complement to a domestic portfolio rather than a redundant one: financials and materials together account for roughly half the S&P/ASX 200 by weight, the exact sectors a cash flow screen systematically underweights.

That complementary profile is worth understanding before you invest, because it shapes whether CFLO adds genuine diversification to what you already hold or simply duplicates exposures you have elsewhere.

Every strength has a corresponding vulnerability. Understanding the specific risks of a cash-flow-screened ETF is what separates informed conviction from accidental exposure.

Four risks deserve your attention before investing:

Factor cycle risk is one of the most commonly underestimated forces in a quality-tilted portfolio: academic evidence supports the long-run premium, but live investors routinely abandon strategies during multi-year underperformance stretches, selling at exactly the wrong point in the cycle.

Foreign currency movements are independent of business performance. The Australian dollar strengthening against the US dollar, for example, reduces the value of USD-denominated holdings when translated back to Australian dollars, even if those businesses are performing well. This adds a layer of volatility that does not exist in a purely domestic ETF.

A five-year-plus holding mindset is not just a rule of thumb for CFLO. It is the minimum time frame needed to survive a full factor cycle and allow both the cash-flow thesis and currency fluctuations to smooth out. Shorter holding periods introduce the real risk of buying during a period of quality-factor underperformance and selling before the cycle turns.

Understanding the concept is one thing. Running a structured checklist before committing capital is what turns understanding into an informed decision.

Before adding CFLO, or any factor ETF, to your portfolio, work through these six items:

Total cost of ownership extends meaningfully beyond the headline management expense ratio: tracking difference, bid-ask spreads, and brokerage commissions all compound silently over long holding periods, and a fund with a lower stated fee can still deliver a worse net outcome if its execution quality is poor.

Running this checklist is not about finding reasons not to invest. It is about confirming that CFLO’s specific design genuinely adds something your existing holdings do not already provide.

Portfolio positioning principle: Start with broad, low-cost global or Australian index ETFs as your core holding. Consider CFLO as a deliberate quality tilt or satellite position alongside them, not as a total market replacement.

The practical test is simple: does this fund’s sector, country, and factor profile genuinely add diversification to what you already hold? If the answer is yes, and the fee, methodology, and concentration profile are acceptable, you have a sound basis for proceeding.

This article is for informational purposes only and should not be considered financial advice. Investors should conduct their own research and consult with financial professionals before making investment decisions. Past performance does not guarantee future results, and factor ETF returns are subject to market conditions and various risk factors.

The most valuable thing you take from this guide is not a view on CFLO specifically. It is the free cash flow framework itself.

That framework applies far beyond a single ETF. You can use it to evaluate individual stocks, compare competing funds, and stress-test the quality of any portfolio. The question “does this business actually generate cash?” is one of the most reliable filters available to a self-directed investor, and it works regardless of which product you are assessing.

Businesses that convert revenue into real cash over time are, by definition, creating genuine economic value for their owners.

Cash generation is the mechanism through which businesses ultimately reward shareholders, whether through dividends, buybacks, or compounding reinvestment. A portfolio built around that principle has a sound philosophical foundation, even if factor cycles mean it will not outperform in every period.

FCF-screened ETFs are not a guaranteed outperformer. Quality tilts require patience, and factor cycles will test your conviction. But for investors who understand what they own and why, they represent a coherent, evidence-grounded approach to quality-oriented global investing.

Walking away with the FCF framework means every investment decision you make from this point forward has a more rigorous analytical foundation, whether or not you ever buy a single unit of CFLO.

—

A free cash flow ETF is a factor ETF that selects and weights companies based on their ability to generate cash after capital expenditures, rather than using market capitalisation or dividend yield as the primary filter. The goal is to concentrate the portfolio in businesses with genuine financial flexibility and durable earnings quality.

Free cash flow measures actual cash a business generates after paying for the equipment and infrastructure it needs to operate, while accounting profit includes non-cash items like depreciation and amortisation and is recorded on an accrual basis. A company can report strong profit while its real cash position is deteriorating, which is why FCF is a more reliable quality indicator.

FCF screens naturally tilt toward capital-light businesses such as software platforms, payments and fintech, and consumer technology, while underweighting capital-intensive sectors like mining, utilities, and early-stage growth companies that reinvest heavily and generate low or negative free cash flow.

The four key risks are factor cycle risk (quality strategies can underperform growth for extended periods), valuation risk (high-FCF companies often trade at premium valuations), currency risk (CFLO holds global equities priced in foreign currencies that move independently of business performance), and concentration risk from large positions in a handful of mega-cap names.

CFLO is best used as a deliberate quality tilt or satellite position alongside a core holding of broad, low-cost global or Australian index ETFs, not as a total market replacement. The practical test is whether its sector, country, and factor profile adds genuine diversification to what you already hold, particularly relevant for Australian investors already concentrated in ASX financials and materials.