How Index Inclusion Quietly Reshapes Your Super Portfolio

14 hrs ago

Most ASX investors know the big four banks by name, but a dividend yield and a recognisable logo are not the same thing as a genuinely resilient business. Three companies that consistently appear in conversations about long-term compounding on the ASX occupy very different sectors, and that difference is the point.

Goodman Group, ResMed, and Wesfarmers each benefit from structural growth themes that are unlikely to reverse in a five- or ten-year window: the demand for digital infrastructure and logistics real estate, the global underdiagnosis of sleep apnoea, and the defensive spending patterns that sustain dominant retail franchises. These are not short-term momentum plays.

Here is a clear picture of what makes each company competitively resilient, what the key risks look like with clear eyes, and a practical framework for deciding whether any ASX blue-chip candidate belongs in your own portfolio.

You probably know Goodman Group as a property company. That label still applies, but it misses the strategic shift that has quietly repositioned the business at the centre of the global AI infrastructure buildout.

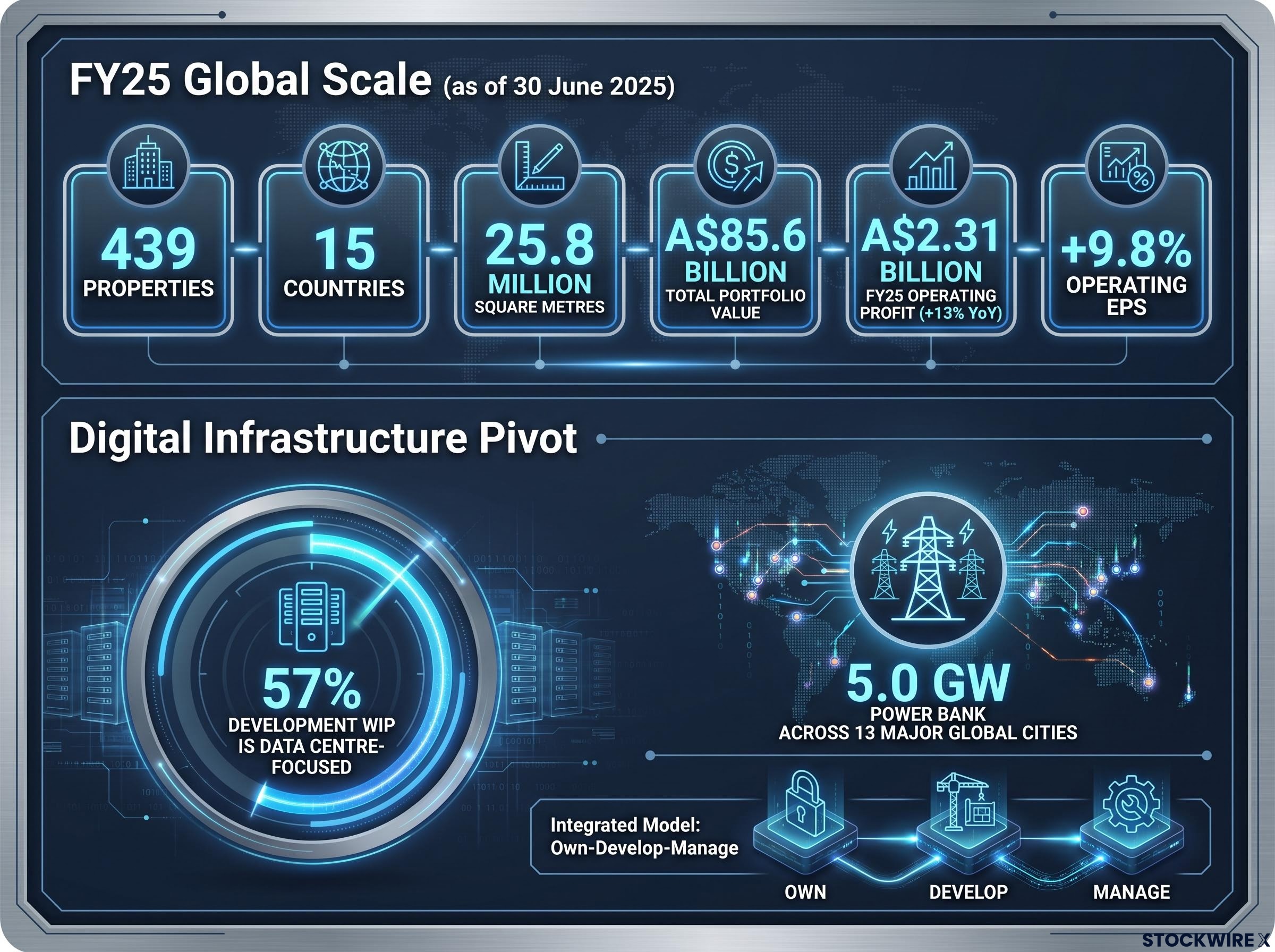

As of 30 June 2025, Goodman managed 439 properties across 15 countries, with 25.8 million square metres under management and a total portfolio value of A$85.6 billion. FY25 operating profit came in at A$2.31 billion, up 13% year-on-year, with operating EPS rising 9.8%. Those are strong numbers for a property group, but the composition of the development pipeline is what separates Goodman from a standard real estate investment trust.

57% of Goodman’s development work in progress is now data centre-focused, supported by a 5.0 GW power bank across 13 major global cities.

That power bank is the detail worth pausing on. Hyperscalers and enterprise cloud operators need sites with reliable power access in well-connected locations. Goodman has pre-positioned itself for that demand at a moment when it is structurally accelerating, anchored in contracted infrastructure pipelines rather than speculative projections.

AI infrastructure investment on the ASX spans several distinct models, including colocation operators, property groups, and network services providers, with Goodman sitting within the property layer of a broader structural build cycle that analysts project will require more than A$26 billion in new Australian data centre capacity by 2030.

The business runs an integrated Own-Develop-Manage model, which means it earns development profits on the way up, management fees from institutional partners on an ongoing basis, and rental income across the property lifecycle. When development activity slows, those recurring income streams continue to underpin earnings.

Goodman’s competitive moat rests on three pillars:

Key risks to watch:

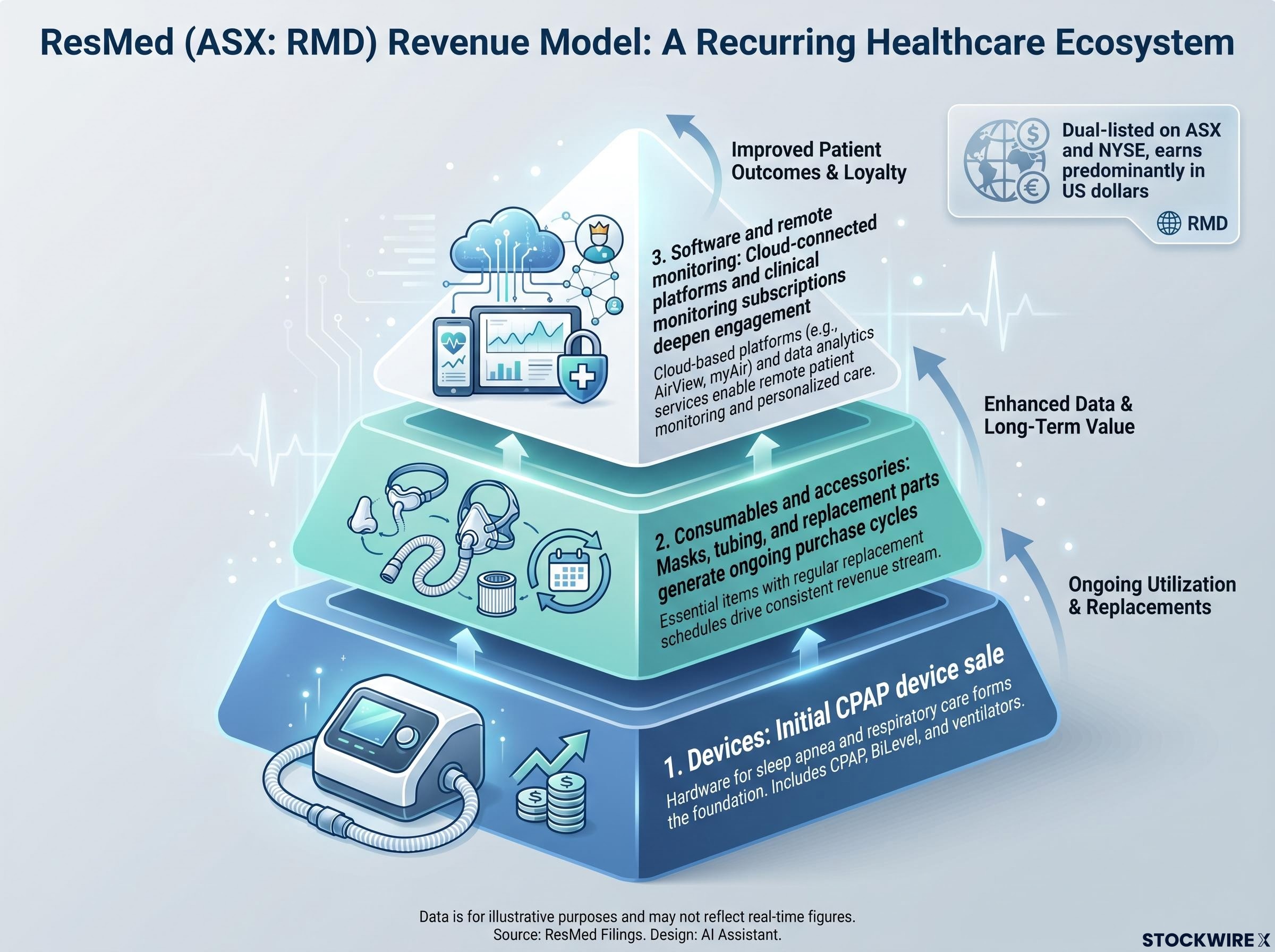

The most important number in ResMed’s investment case is not a revenue figure or a margin. It is the size of the population that has sleep apnoea but does not yet know it. A significant portion of people with the condition remain undiagnosed, and that gap represents a structural demand driver, not a near-term catalyst that fades once it plays out.

As diagnosis rates improve through better public awareness and expanded screening access, ResMed’s addressable market grows. That is a fundamentally different dynamic from a company selling into a mature, fully penetrated market.

ResMed is dual-listed on the ASX and the NYSE, giving Australian investors access to a global healthcare franchise that earns predominantly in US dollars, providing a degree of natural currency diversification.

The revenue model is where the recurring quality becomes clear. There are three distinct layers, and each builds on the one before it:

That combination of underdiagnosis at scale and a recurring accessory and software revenue model means ResMed’s earnings base is likely to widen for years as diagnostic pathways improve. This is a different risk profile from a company reliant on one-time equipment purchases.

Key risks to consider:

You already know Bunnings. You have probably been to Kmart this year. That familiarity is part of the investment case for Wesfarmers, but it is not the whole story.

The less visible strength is management’s track record of capital allocation discipline, the judgment applied to buying, improving, and sometimes divesting businesses when they no longer fit the portfolio. The Coles demerger in 2018 remains the clearest example: Wesfarmers traded short-term earnings scale for long-term shareholder value, a decision that compounded quietly but powerfully over time.

| Division | What it does | Primary competitive strength |

|---|---|---|

| Bunnings | Home improvement and hardware retail | Dominant market share, dense store network, deep trade relationships |

| Kmart & Target | Value-focused general merchandise and apparel | Private-label sourcing, supply chain efficiency, on-trend positioning |

| Officeworks | Office supplies, technology, and education products | Category breadth and multi-channel presence |

| WesCEF & Industrials | Chemicals, energy, fertilisers, and safety distribution | Diversified industrial inputs with defensive demand characteristics |

Bunnings is the anchor franchise. Its store network density, trade customer relationships, and brand strength function as a structural barrier to entry that no competitor has meaningfully threatened. Kmart, meanwhile, has repositioned itself as a destination for value-oriented, on-trend products backed by efficient private-label sourcing, carving out a clear position in the value-retail segment.

Wesfarmers carries a relatively conservative balance sheet and maintains a consistent dividend history. For the long-term investor, the Coles demerger precedent matters as much as the current portfolio composition, because it demonstrates a willingness to make disciplined decisions about what stays and what goes.

Key risks to keep in mind:

Cyclical and defensive allocation decisions are particularly relevant to a portfolio anchored around Wesfarmers, whose earnings are sensitive to Australian consumer sentiment even as its dominant retail brands provide a degree of insulation that pure discretionary cyclicals cannot claim.

The three companies above share certain qualities, but the more useful takeaway is the evaluation process itself. Here are five questions you can apply to any ASX company before committing capital.

Evaluating any ASX stock before committing capital requires separating business quality from share price valuation, a discipline that fund managers consistently identify as the most common failure point for retail investors who buy strong brands at prices that eliminate the return potential.

| Question | Why it matters |

|---|---|

| Does the company have a defensible competitive position? | Protects margins and market share, making earnings more resilient over time |

| Is demand structurally supported, not purely cyclical? | Structural trends like digitisation and ageing demographics make growth more durable |

| Are cash flows recurring or resilient? | Enables reinvestment, supports dividends, and powers compounding |

| Has management demonstrated disciplined capital allocation? | Determines whether earnings translate into long-term shareholder value |

| Are key risks identifiable and manageable? | Ensures you invest with clear eyes and realistic expectations |

Running any ASX blue-chip candidate through these five questions before buying tells you whether you are paying for genuine quality or simply for familiarity. That distinction determines whether a quality stock becomes a quality investment at the price you pay.

Here is how the three profiled companies map against the framework:

Goodman, ResMed, and Wesfarmers operate in different sectors, but the structural qualities are consistent. Each occupies a leading position in a market with durable tailwinds, generates recurring or resilient cash flows, and is managed by teams with demonstrated capital allocation discipline.

They also share one constraint worth naming clearly: all three frequently trade at valuation premiums relative to ASX averages. That premium reflects quality, but it also means entry price matters. Patience in buying often improves long-term outcomes, even when the underlying business is strong.

Long-term portfolio construction is not about identifying perfect companies. It is about pairing genuine quality with a rational purchase price and a multi-year holding mindset. The framework above gives you a repeatable way to test whether any blue-chip candidate earns its place in your portfolio, or whether you are simply paying for a name you recognise.

For investors wanting to understand how recurring cash flows from companies like Wesfarmers and ResMed can be systematically reinvested over multi-decade horizons, our comprehensive walkthrough of dividend compounding strategy covers payout ratio analysis, free cash flow sustainability, and reinvestment mechanics with worked examples.

This article is for informational purposes only and should not be considered financial advice. Investors should conduct their own research and consult with a licensed financial professional before making investment decisions.

ASX blue chip stocks are shares in large, well-established Australian companies with a track record of stable earnings, strong market positions, and consistent dividends. Examples include Goodman Group, ResMed, and Wesfarmers, each of which holds a leading position in its sector with durable competitive advantages.

Goodman Group has pivoted significantly toward data centre development, with 57% of its work in progress now data centre-focused and a 5.0 GW power bank across 13 major global cities. That positioning places it at the centre of the global AI infrastructure buildout, not just the traditional logistics real estate cycle.

A significant portion of people with sleep apnoea remain undiagnosed, meaning ResMed's addressable market expands as diagnostic pathways improve over time. Layered on top of that is a recurring revenue model built on consumables, accessories, and software subscriptions that generate ongoing income long after the initial device sale.

The clearest example is the 2018 Coles demerger, where Wesfarmers traded short-term earnings scale for long-term shareholder value, a decision that compounded meaningfully over time. That track record signals management is willing to make difficult portfolio decisions rather than simply holding assets for size.

The five questions are: does the company have a defensible competitive position, is demand structurally supported rather than purely cyclical, are cash flows recurring or resilient, has management demonstrated disciplined capital allocation, and are key risks identifiable and manageable. Applying this framework separates genuine business quality from the familiarity of a well-known brand.