Why a BoJ Rate Hike Hasn’t Stopped the Yen Carry Trade

11 hrs ago

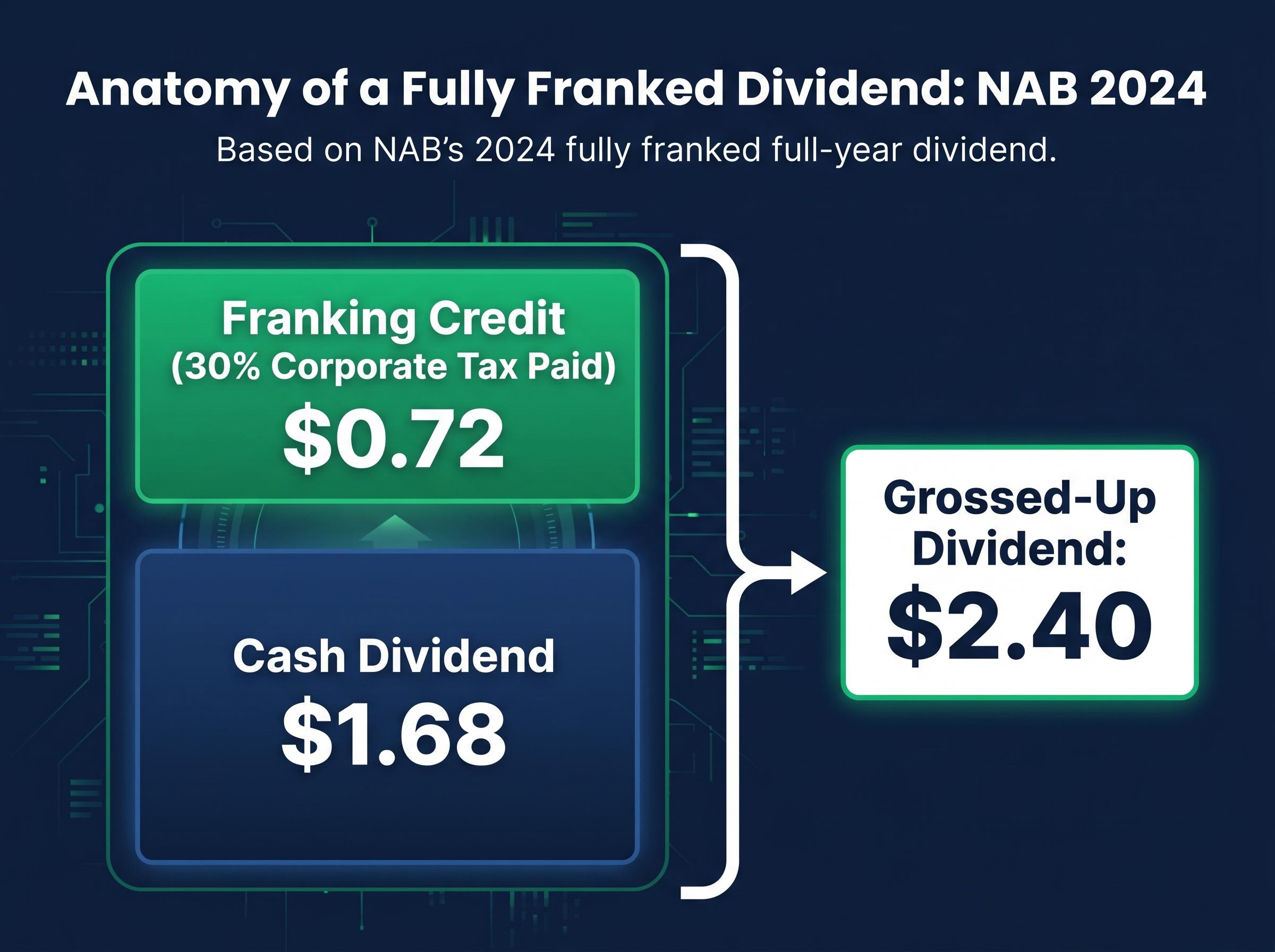

A fully franked $1.68 cash dividend from National Australia Bank is worth $2.40 to the right investor. The difference, $0.72 per share, is not a rounding error. It is a structural feature of the Australian tax system that determines how income-generating shares are valued, compared, and selected for portfolios built around after-tax yield. Franking credits sit inside nearly every major ASX bank dividend, yet the concept is routinely overlooked by investors who evaluate shares on headline yield alone. With the major banks consistently paying fully franked dividends, understanding the gross value of those distributions matters directly to decisions about which income assets to hold and at what price. This article explains how the dividend imputation system works, who qualifies to benefit, how to calculate the grossed-up value of a franked dividend, and what happens to a share valuation when franking credits are properly incorporated. NAB’s 2024 dividend is used as a working case study throughout.

The problem is straightforward. A company earns profit and pays corporate tax on it. The remaining profit is distributed to shareholders as a dividend. Those shareholders then pay personal income tax on the dividend they receive. The same dollar of profit has been taxed twice: once in the company’s hands at 30%, and again in the investor’s hands at their marginal rate.

Australia’s dividend imputation system was designed to eliminate that double taxation. When a company pays corporate tax and then distributes a dividend, it can attach franking credits representing the tax already paid. Those credits pass through to the shareholder as a redeemable tax offset.

A “fully franked” dividend means 100% of the applicable corporate tax has been credited to the distribution. NAB’s 2024 full-year dividend was 100% fully franked. A partially franked dividend carries credits for only a portion of the tax paid, and an unfranked dividend carries none.

Three components make up a franked dividend:

Cash dividends and attached franking credits are both assessable income. A tax offset equal to the franking credit amount is then applied against tax payable.

The Australian Taxation Office treats both the cash and the credit as income. The credit then functions as an offset, reducing the investor’s tax bill by the amount of corporate tax already paid on that profit. For investors who understand this mechanism, it changes how every fully franked dividend is evaluated.

The formula is a single division. It converts a cash dividend into its pre-tax equivalent by reversing the corporate tax that was deducted before the payout reached the investor.

Grossed-Up Dividend = Cash Dividend ÷ (1 − Corporate Tax Rate)

Applied to NAB’s 2024 dividend, the arithmetic proceeds in three steps:

The table below summarises the breakdown.

| Dividend Component | Amount Per Share |

|---|---|

| Cash Dividend | $1.68 |

| Franking Credit | $0.72 |

| Grossed-Up Dividend | $2.40 |

Rask Media’s valuation analysis, published 27 August 2024, used these same figures in its NAB assessment: $1.68 cash, $2.40 grossed-up. Once investors can perform this calculation themselves, they can compare income-generating assets on a consistent after-tax basis rather than relying on headline cash yields that systematically understate franked returns.

The company’s franking level determines how much credit is attached. The investor’s personal tax position determines how much of that credit is worth anything. These are two separate variables, and conflating them is one of the most common errors in dividend analysis.

The benefit segments into clear tiers, from most-benefited to least.

| Investor Type | Tax Rate | Franking Credit Outcome |

|---|---|---|

| SMSF in pension phase | 0% | Potentially fully refundable |

| Low-income individual | Below 30% | Partial refund or offset |

| Standard earner | 30% | Full offset, no refund |

| High-income earner | Above 30% | Partial offset against higher marginal rate |

| Non-resident | N/A | Generally no benefit |

Self-managed super funds in pension phase face a 0% tax rate on earnings. The full $0.72 franking credit on each NAB share can be claimed as a cash refund from the ATO, effectively converting a corporate tax payment into personal income for the fund. This makes franked bank shares among the most tax-efficient assets an SMSF in pension phase can hold.

The ATO exempt current pension income rules define the zero-tax treatment that applies to earnings from assets supporting retirement-phase income streams, confirming the structural basis for the full refundability of franking credits that SMSFs in pension phase receive.

Lower-income investors whose marginal rate sits below 30% receive either a reduced tax bill or a partial cash refund where the credit exceeds their liability. High-income earners still benefit, but the credit only offsets the gap between the corporate rate and their marginal rate. No refund is generated.

The genuine surprise for many investors encountering this system for the first time is the refundability mechanism.

The mechanics of claiming and maximising franking credits extend beyond the grossed-up formula, covering the 45-day holding rule, the small shareholder exemption, and the ATO’s automatic refund process introduced for Australians over 60 from the 2024-25 tax year.

Where franking credits exceed an investor’s total tax liability, the excess is refundable as cash from the ATO.

NAB’s shareholder tax documentation confirms that excess credits may be refundable depending on the investor’s tax position. For zero-tax entities, this is not merely a tax reduction. It is a cash-generation mechanism, and it materially changes the effective yield calculation.

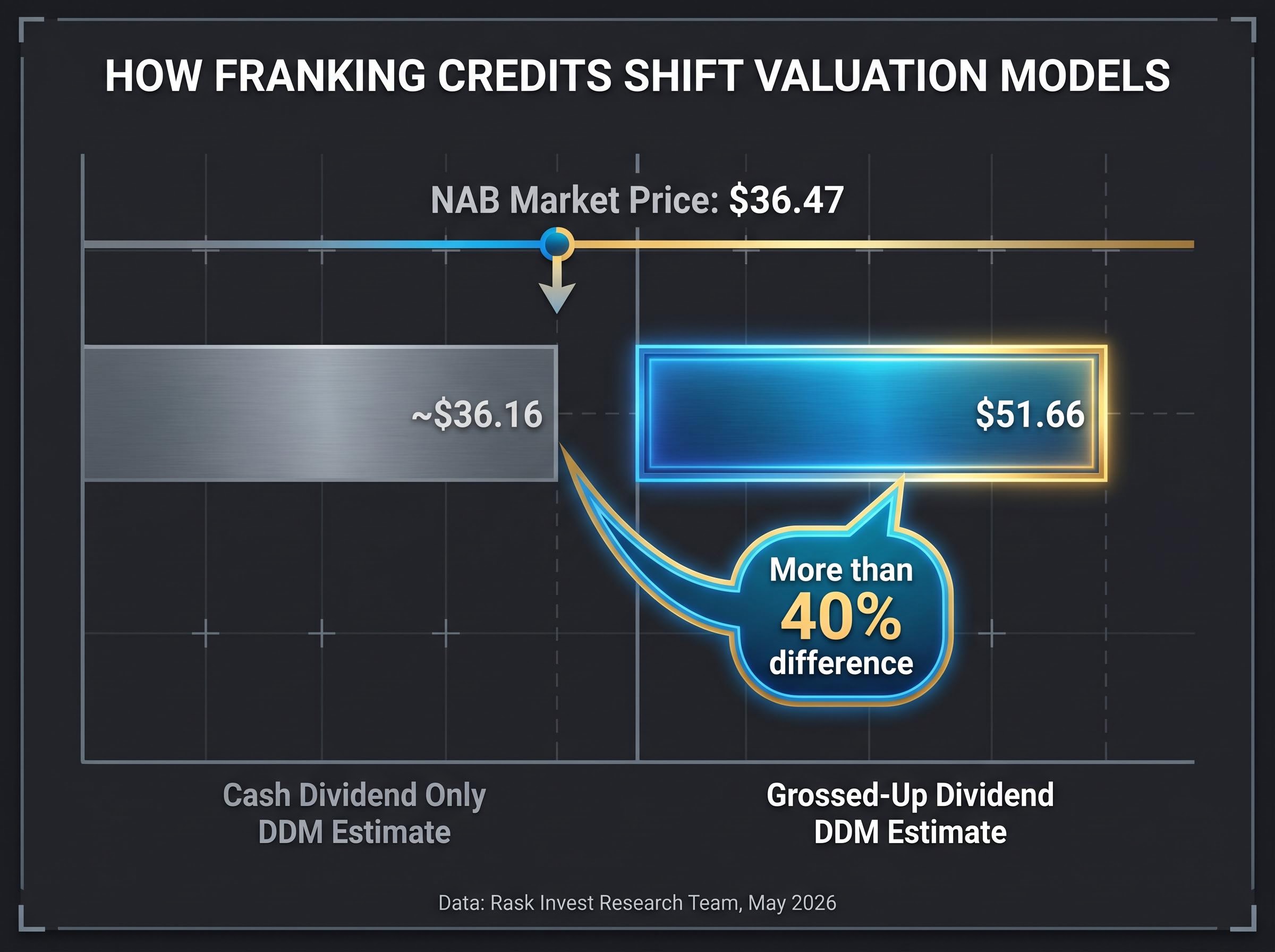

Franking credits do not only change the income an investor receives. They change what a share is worth in a valuation model.

A dividend discount model (a method for estimating a share’s value based on its future dividend payments, discounted back to today’s dollars) takes a dividend figure as its primary input. When the input is the cash dividend alone, the output reflects cash-only value. When the input is the grossed-up dividend, the output reflects the full economic value of the distribution to an eligible investor.

The difference is not marginal. Using forecast-adjusted figures from Rask Invest Research Team analysis (published May 2026), the NAB valuation comparison is stark.

| Valuation Basis | Dividend Input | DDM Estimate |

|---|---|---|

| Cash dividend only | per share | Approximately $36.16 |

| Grossed-up dividend | per share | $51.66 |

With NAB’s share price at $36.47 at the time of that analysis, the cash-only model suggested the shares were trading near fair value. The grossed-up model suggested the market price sat more than 40% below the after-tax value of the income stream for eligible investors.

That is not a rounding difference. For investors who can fully utilise the franking credit, the grossed-up valuation implies the market price may not fully reflect the after-tax value of the distribution.

The $51.66 figure is relevant only to Australian tax-resident investors who can fully utilise or receive a refund of the franking credit. Foreign investors, high-income earners who cannot receive refunds, and investors holding shares through certain structures may see a materially different effective valuation.

The market price reflects the blended demand of all investor types, not just those who benefit most from imputation. This is why the gap between the two valuations persists: the market does not price exclusively for the most tax-advantaged holder.

Franking credits improve the after-tax income calculation. They say nothing about whether the underlying dividend will continue to be paid, grow, or shrink.

A fully franked dividend from a bank whose credit losses are rising, whose net interest margin is compressing, or whose consumer lending book is deteriorating is still a deteriorating income stream, regardless of the tax offset attached to it. The grossed-up yield calculation answers a tax question, not a business quality question.

Policy risk also remains part of the investment landscape. The 2019 federal election saw a prominent proposal to restrict cash refunds for excess franking credits. According to Morningstar Australia, that debate remains embedded in investor memory, particularly among retirees and SMSFs who depend on those refunds as a component of their income strategy.

The dividend imputation system remains intact, but the refundability of excess franking credits continues to be politically sensitive, particularly for retirees and SMSFs who rely on cash refunds as part of their income strategy.

As of May 2026, no active legislative proposal to alter the system has been identified. The risk is not imminent, but it is not zero.

Before treating the grossed-up yield as a valuation conclusion, investors should examine qualitative factors that determine whether the dividend itself is sustainable:

Investors who understand where franking credit analysis ends and fundamental business analysis begins are better positioned to avoid overpaying for a tax feature attached to a weakening income stream.

Headline cash yield is an incomplete measure for Australian tax-resident investors evaluating franked shares. The grossed-up yield is the more relevant figure for anyone who can apply or receive the franking credit.

At NAB’s $36.47 price reference, the difference is material. The cash dividend of $1.68 produces a headline yield of approximately 4.6%. The grossed-up dividend of $2.40 produces an effective yield of approximately 6.6%. An investor comparing NAB against an unfranked alternative at 5% headline yield would draw the wrong conclusion from cash figures alone.

Grossed-up yields across the Big Four banks follow the same arithmetic as the NAB example but land at materially different absolute figures depending on each bank’s cash payout level, franking percentage, and share price at the time of comparison.

Research reviewed by the Australian Accounting Standards Board confirms that franking credits influence both investor behaviour and corporate payout decisions, though academic studies have not produced a single consensus on their precise market value. Commentary from Kalkine and Morningstar consistently identifies franked bank dividends as central to Australian income investing strategy, particularly for retirees and SMSFs.

ANU research on dividend imputation and share pricing identifies how the imputation system influences both corporate payout decisions and investor behaviour, while acknowledging that empirical studies have not converged on a single consensus value for franking credits in market pricing models.

The practical process for any investor assessing a franked dividend involves three steps:

The grossed-up yield and valuation shift are powerful inputs, but they sit inside a broader analytical process. The typical investment process begins with qualitative research into strategy, management quality, and macroeconomic conditions before quantitative modelling refines the estimate.

The $1.68 cash dividend that becomes $2.40 for an eligible investor is real and material. It can shift a valuation estimate by more than 40%. It can convert a corporate tax payment into a cash refund for a zero-tax entity. But it remains one variable in a complete investment picture, not the picture itself.

For eligible Australian investors, the grossed-up dividend is the economically correct figure to use in yield calculations and valuation models. A fully franked dividend is worth more than its cash face value to any investor whose marginal tax rate sits at or below 30%, and is potentially worth the most to SMSFs in pension phase where the entire credit may be refunded as cash.

Understanding where an investor sits in the tax-position framework (zero-tax, low-tax, high-tax, or non-resident) is the prerequisite for assessing whether a fully franked dividend is as valuable as the headline figure implies. Investors who have not previously calculated their grossed-up yield on bank holdings have an immediate, concrete action available to them: run the formula, check their tax position, and compare the result against every unfranked alternative in their portfolio.

For investors ready to move from individual stock analysis to portfolio-level strategy, our dedicated guide to ASX dividend portfolio construction covers payout ratio screening, ex-dividend date mechanics, dividend reinvestment plan compounding, and how to identify dividend traps before a cut destroys the income thesis.

This article is for informational purposes only and should not be considered financial advice. Investors should conduct their own research and consult with financial professionals before making investment decisions.

Franking credits are tax offsets attached to dividends paid by Australian companies, representing corporate tax already paid on the underlying profit. When you receive a franked dividend, the attached credit reduces your personal income tax liability, and in some cases the excess credit is refunded as cash by the ATO.

Divide the cash dividend by 0.70 for a fully franked dividend paid at the 30% corporate tax rate. For example, NAB's $1.68 cash dividend divided by 0.70 equals a grossed-up value of $2.40 per share, with $0.72 representing the attached franking credit.

Self-managed super funds (SMSFs) in pension phase benefit most because their tax rate is 0%, meaning the full franking credit can be claimed as a cash refund from the ATO. Low-income investors also benefit significantly, while non-residents generally receive no benefit from franking credits.

Franking credits materially increase the effective yield of a fully franked dividend for eligible investors. Using NAB's figures at a $36.47 share price, the cash yield is approximately 4.6%, but the grossed-up yield is approximately 6.6%, meaning a comparison against an unfranked 5% yield would be misleading if only cash figures are used.

Yes, using the grossed-up dividend instead of the cash dividend as the input to a dividend discount model can shift the valuation estimate substantially. Analysis of NAB showed a cash-only DDM estimate of approximately $36.16 versus a grossed-up estimate of $51.66, a difference of more than 40% for eligible investors.