Owning VGE as your emerging markets ETF means your portfolio contains no Samsung Electronics, no SK Hynix, and no other South Korean equity. Meanwhile, another investor on the same exchange holding a different emerging market ETF may have close to 10% of their money sitting in South Korean stocks. Same category label. Same asset class. An entire country’s difference.

The gap exists because the index provider sitting beneath each fund determines which countries qualify as “emerging” in the first place. The ASX-listed ETF market offers multiple emerging markets products that appear identical on the label but can diverge by an entire nation, and most investors never look past the category name to find out why.

Here is a framework for understanding what your emerging market ETF actually decides on your behalf, so that the next time you compare products, your selection reflects a conscious choice rather than an accidental one.

The same label, very different fund

Most investors treat “emerging markets” as a standardised category. Pick any ETF with that label, and you get roughly the same thing. That assumption is wrong, and the divergence is not marginal.

Three index providers dominate global equity benchmarking. Each defines emerging markets using its own eligibility criteria:

- MSCI evaluates market accessibility, size and liquidity requirements, and regulatory environment to determine country classification

- FTSE Russell applies its own framework covering market and regulatory environment quality, custody and settlement procedures, dealing conditions, and derivatives availability

- S&P Dow Jones uses a separate methodology assessing market capitalisation, annual turnover, and qualitative factors including market accessibility and regulatory stability

The choice of index provider flows directly into country weightings, sector exposure, and currency risk, shaping the returns your fund actually delivers. Two ASX-listed emerging market ETFs carrying identical category labels can end up holding completely different countries, not merely different weightings of the same ones.

Selecting an emerging market ETF without examining the underlying index provider means handing a consequential portfolio construction decision to whoever wrote the label, rather than making it yourself.

Currency risk adds another layer that the index methodology debate often obscures: all major ASX-listed EM ETFs are unhedged, so your effective return from emerging market investing combines equity performance with the movement of multiple EM currencies against the Australian dollar simultaneously.

When big ASX news breaks, our subscribers know first

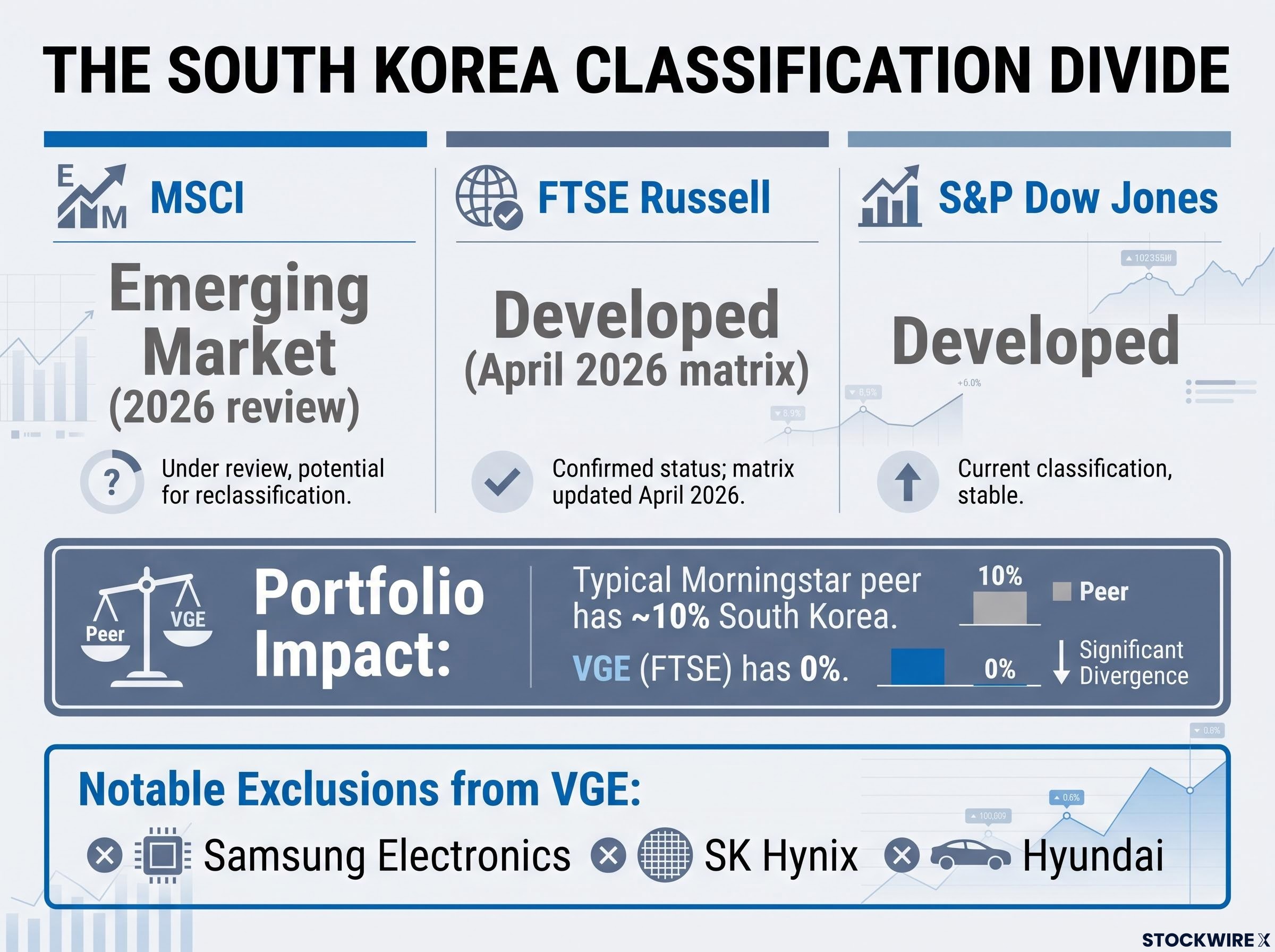

Why South Korea is the sharpest illustration of the divergence

The abstract becomes concrete with one country: South Korea.

MSCI classifies South Korea as an emerging market (as of the 2026 market classification review). FTSE Russell classifies it as developed (as per the FTSE Equity Country Classification matrix, April 2026). S&P Dow Jones also classifies it as developed. The split is well-documented and represents the single most material divergence between emerging market index families.

The direct consequence for your portfolio is stark. Since VGE follows a FTSE index, South Korean stocks do not appear in its holdings at all, while the typical fund in its Morningstar peer category puts around 10% of assets there. That is not a rounding error; it means the two funds are making structurally different bets on where emerging market returns will come from.

There is a secondary consequence most investors miss entirely. If you use FTSE-based indices for both your developed and emerging market allocations, South Korea appears in your developed market sleeve and you have zero South Korean exposure classified as emerging. If you mix FTSE for developed markets with MSCI for emerging markets, you may inadvertently double-count South Korea across both. Neither outcome is wrong, but it should be deliberate.

Your developed market allocation is the other half of the classification equation: VGS, the most widely held international equity ETF on the ASX, tracks the MSCI World ex-Australia Index, which classifies South Korea as developed and includes it, meaning investors combining VGS with VGE hold zero double-counted South Korean exposure but investors combining VGS with an MSCI-based emerging market fund will.

| Index Provider | South Korea Classification | China A-Shares Approach | Notable Inclusions/Exclusions |

|---|---|---|---|

| MSCI EM | Emerging market | Partial inclusion via inclusion factor | Includes South Korea; large- and mid-cap focus |

| FTSE EM All Cap China A Inclusion | Developed market (excluded from EM) | Partial inclusion via stepped inclusion factor | Excludes South Korea; all-cap coverage |

| S&P EM | Developed market (excluded from EM) | Separate inclusion criteria | Excludes South Korea; own liquidity screens |

A 10-percentage-point gap in South Korean exposure is not a tracking difference you can ignore. It means two funds in the same category are constructing fundamentally different portfolios.

What VGE actually owns, and how the FTSE index is built

Having established what VGE does not own, here is what it does.

The fund tracks the FTSE Emerging Markets All Cap China A Inclusion Index. That name carries specific meaning worth unpacking. “All cap” means the index includes large-, mid-, and small-cap stocks, not just the largest companies. This gives it a broader base than indices limited to large- and mid-cap names only. “China A Inclusion” refers to the partial inclusion of mainland-listed Chinese shares (known as A-shares) into the index, a mechanism that has been stepped up gradually over time.

The index covers companies across more than 20 emerging economies, capturing roughly the top 98% of eligible market capitalisation. In practice, that translates to approximately 6,300 individual company positions, according to the latest available factsheet data.

The dominant country allocations tell you where your money actually sits:

- China, Taiwan, and India are the heaviest weightings, collectively representing the majority of the index

- Brazil, South Africa, Saudi Arabia, Thailand, Mexico, and Malaysia follow at lower single-digit weights

Country weight figures shift as markets move. You should consult the current VGE factsheet for up-to-date allocations, but the general picture of China, Taiwan, and India dominating is consistent across reporting periods.

The China A-shares inclusion mechanism is worth pausing on. When FTSE adjusts its inclusion factor for A-shares, every fund tracking that index inherits the change automatically, without any active decision by the fund manager. Your effective portfolio changes each time the index provider updates its methodology. Even a purely passive emerging market investment is subject to ongoing decisions by the index provider.

Cost comparison: VGE carries a Total Cost Ratio (TCR) of 0.48% per annum, compared to a category average of approximately 0.99% per annum. That cost advantage is meaningful, but it does not resolve the methodology question. A cheaper fund that tracks a different definition of emerging markets is not automatically the better choice; it depends on whether that definition matches what you want to own. (Note: verify TCR against current PDS before relying on this figure.)

How the South Korea gap flows through to performance

The performance implication follows directly from the structural logic. When South Korean equities move differently from the rest of the emerging markets universe, MSCI-based and FTSE-based funds will diverge. The direction is mechanical: the fund that holds South Korea participates in its performance, and the fund that does not, does not.

The stocks absent from VGE are far from obscure. Samsung Electronics and SK Hynix rank among the world’s most significant semiconductor businesses, while Hyundai operates as one of Asia’s largest industrial conglomerates. Across strong semiconductor cycles, these names have driven a meaningful share of regional equity returns, and VGE’s structure means it captures none of that contribution.

When South Korean equities outperform the rest of the emerging market universe, MSCI-based funds will tend to outperform FTSE-based funds. When South Korea underperforms, the reverse holds. None of this reflects poorly on VGE as a product. The fund carries a Morningstar Bronze Medalist Rating, recognising the quality of its execution and its low-cost delivery of its stated objective. Any gap in returns relative to MSCI-based peers is a consequence of index methodology, not a shortcoming in how the fund is run.

If you see VGE trail an MSCI-based peer during a technology rally, recognise that as a predictable structural outcome of the index it tracks, not a signal to switch funds without understanding why.

The core reframe: Choosing a passive product embeds active decisions about country and sector exposure. The label “passive” describes how the fund selects securities within its index. It does not describe the choice of index itself.

The next major ASX story will hit our subscribers first

Five questions to ask before choosing an emerging markets ETF

You now understand the problem. Here is how to apply the framework yourself, with any emerging market ETF on any exchange.

- Which index does this fund track?

Fund documents disclose the benchmark explicitly. This is the foundational question; everything else follows from it.

- How does this index classify South Korea?

Given the MSCI versus FTSE divergence, this single question carries a roughly 10% weighting difference between funds in the same peer category.

- What are the top country weightings and concentration?

Reviewing the factsheet reveals whether the fund is heavily concentrated in China, Taiwan, and India, and whether South Korea is present or absent.

- Am I benchmarking this fund against the right peer group?

Comparing a FTSE-based fund to an MSCI-based peer group produces apparent under- or outperformance that is purely methodological. Performance comparisons are only meaningful within the same index family.

- Do I have overlapping or conflicting exposures across my portfolio?

If your developed market allocation treats South Korea as developed and your emerging market allocation treats it as emerging (or vice versa), you may be double-counting or entirely missing that country. Cross-checking index families across your whole portfolio is where the most common mistakes hide.

The South Korea double-counting scenario is one instance of a broader problem: portfolio concentration risk that is invisible at the label level but becomes apparent only when you map the actual country and sector exposures across your total allocation, including both developed and emerging market sleeves.

The objective is not to identify a single “correct” emerging market index. Each definition reflects a legitimate set of judgments about market classification. The objective is to make the choice consciously rather than by default, so that you know what you own and why.

Choosing your emerging markets exposure with your eyes open

Picking an index is itself a portfolio construction decision, one that gets carried out through passive mechanics but is no less consequential for it. Treating that choice as a neutral default does not make it neutral; it simply makes it unexamined.

The methodology question is also ongoing, not a one-time check. FTSE’s China A-shares inclusion factor has been stepped up gradually, and further adjustments will change the effective portfolio of every fund tracking that index. Reclassifications, new market additions, and inclusion factor changes mean the fund you hold today may shift over time as the index provider updates its framework.

The due-diligence threshold for selecting an emerging market ETF should include three things alongside the cost comparison most investors already make: the underlying index provider, the index’s country classification methodology, and a cross-portfolio exposure map that shows whether countries like South Korea appear once, twice, or not at all across your total allocation. VGE’s 0.48% TCR versus the category’s approximately 0.99% average matters, but it does not tell you what you own.

The ASX-listed ETF market offers multiple emerging market products without prominent labelling of the underlying index provider. Adding index methodology to your checklist alongside cost and past returns is not performing more complex analysis. It is simply asking the question that determines what you actually own.

For readers wanting to translate the index methodology framework into a full portfolio structure, our comprehensive walkthrough of ETF portfolio construction for Australian investors covers asset allocation, the developed-plus-emerging market split, and the fee compounding implications of each decision across a long investment horizon.

This article is for informational purposes only and should not be considered financial advice. Investors should conduct their own research and consult with financial professionals before making investment decisions. Past performance does not guarantee future results.