Most investors treat buying a market decline as one of the safer things they can do. Years of rapid recoveries have reinforced the instinct: prices fall, you buy, they bounce, you profit. It feels close to automatic. But the buy the dip strategy carries a specific failure mode that price charts do not reveal, and it has cost retail investors more money than most realise. A dip can be rational to buy or it can be a slow-motion capital destruction event, and the difference between the two is never visible on the screen. The investor’s real task is not to spot the decline; it is to diagnose its cause. By the end of this piece, you will have a clear mental model for separating temporary sentiment-driven pullbacks from genuine fundamental deterioration, and a practical set of questions to work through before you deploy capital into any falling asset.

Why buying the dip has a seductive logic

For broad, diversified equity indices, the historical record genuinely supports patient buying during drawdowns. Markets have repeatedly recovered from steep declines and compounded over time. If you bought the S&P 500 or MSCI World during any major correction over the past several decades and held for the long term, you were rewarded more often than not.

Long-term compounding is the reason the dip-buying instinct has any validity at all for broad diversified indices: the second decade of a compounding investment generates nearly double the dollar gains of the first decade on the same capital, which means patient buyers of index dips are being rewarded by mathematics as much as by market recovery.

That track record is where the cognitive leap happens. If buying dips works for diversified markets, the assumption quietly extends to any asset after any decline. A tech stock falls 30% and it feels like a sale. A thematic ETF drops through a round number and the reflex kicks in.

The post-2020 period entrenched this tendency further. Pullbacks were followed by recoveries quickly enough that investors began treating each bout of weakness as a near-guaranteed entry point. That sequence repeated with enough consistency that it shifted from being an observation about markets to feeling like a reliable rule of thumb.

That conditioning is the root of the problem.

“A lower price is not proof of value; it is just proof something went down.”

The fact that this approach works for diversified indices does not mean it works for every asset in every decline. Conflating the two is the specific error the rest of this article will help you avoid.

When big ASX news breaks, our subscribers know first

Not all dips are the same: the two types of decline every investor must distinguish

The surface appearance of every dip is identical: a price that used to be higher is now lower. What separates a buying opportunity from a capital trap lives entirely beneath the chart. Your job, before you commit a single dollar, is to identify which of two categories the decline belongs to.

Sentiment-driven pullbacks

These are declines caused by forces external to the business itself. Broad macro fears, geopolitical headlines, risk-off flows, or forced selling push prices lower even though the underlying asset is fundamentally intact. Earnings power is still there. The balance sheet is healthy. The competitive position has not changed. The investment thesis still makes sense.

The price moved because investors got nervous, not because the asset broke. Once sentiment stabilises, these assets tend to recover, and buying into that weakness can be rational.

Fundamental deterioration

Here, the decline is the market doing its job. Revenues are rolling over. Debt costs are rising. Pricing power has evaporated. The margin structure is worsening. Management credibility is damaged.

When investors buy because “it used to be at $100, so $40 must be a bargain,” they are anchoring, a cognitive error where you measure value against a historical level rather than against what the asset is actually worth given its current fundamentals. The apparent discount is an illusion created by looking backward instead of forward.

Knowing which category a decline belongs to is the difference between adding exposure at a genuine discount and throwing good money after a permanently impaired asset.

| Attribute | Sentiment-driven pullback | Fundamental deterioration |

|---|---|---|

| Primary cause | Macro fears, geopolitics, risk-off flows | Eroding revenues, rising debt, broken model |

| Earnings outlook | Broadly intact | Declining or collapsing |

| Balance sheet signal | Healthy, manageable leverage | Stressed, rising refinancing risk |

| Likely next move | Recovery once sentiment stabilises | Further repricing as fundamentals worsen |

Peloton and the anatomy of a value trap

Peloton reached a peak closing price of US$167.42 on 13 January 2021. The pandemic had created an extraordinary demand surge for home fitness equipment, and the stock priced in a future where that demand would persist. It did not.

Once reopening gathered pace across 2021 and into 2022, the conditions that had inflated Peloton’s valuation went into reverse. Customers returned to gyms, subscription growth stalled, costs mounted, and what had looked like a durable shift in consumer behaviour turned out to be a temporary one. The result was a prolonged, multi-stage deterioration in the underlying business.

At each new lower price level, the stock looked cheap relative to the prior peak. Down 40% from the high felt like a discount. Down 60% felt like a steal. Down 80% felt like the kind of generational buying opportunity that social media investors urged each other not to miss. Each level triggered the same reflex: it was so much higher before, so this must be value.

It was not. The investors who averaged down were not buying at the wrong price point. They were asking the wrong question.

The wrong question: “Is this cheaper than it was?” The right question: “Is this cheap given what the business is actually worth now?”

That distinction is everything. The share price did not fall because sentiment briefly turned against a healthy business. It fell because the business itself had changed, and the market was working through the implications of that change one downward revision at a time. Investors who anchored to the prior high rather than asking what the company was worth at its new run rate kept buying into a repricing that had fundamental logic behind it.

Peloton is not an outlier cautionary tale. It is a template for how value traps form, and the pattern it followed is repeatable in any asset whose original growth story was built on a tailwind that has since reversed.

Value traps, assets that appear statistically cheap because their price has fallen sharply while their underlying earnings power has structurally collapsed, represent the most dangerous failure mode of dip-buying, and the analytical challenge of separating them from genuine bargains is the same problem that has occupied value investors for decades.

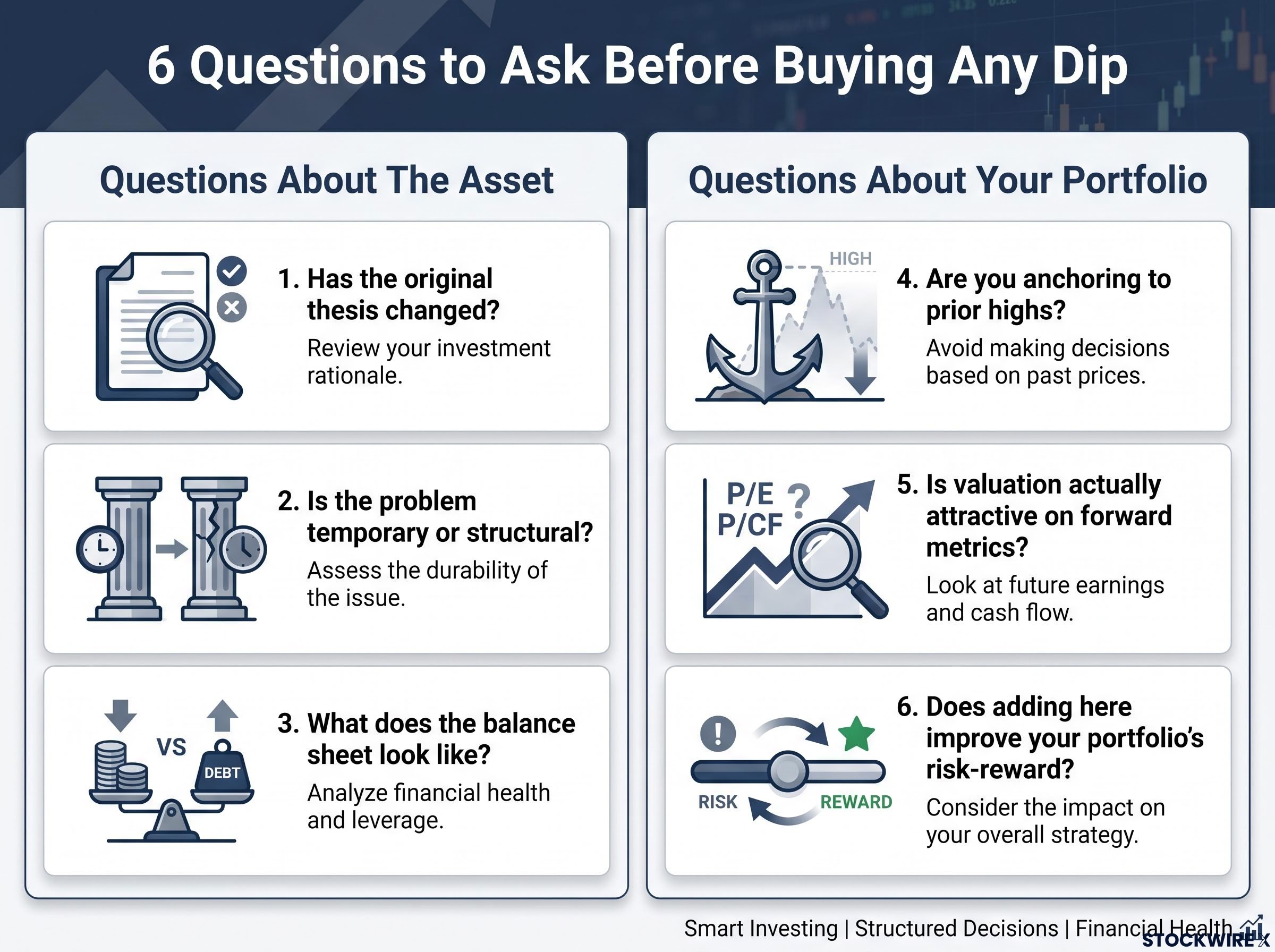

Six questions to ask before buying any dip

Recognising the two types of decline is the mental model. What follows is the practical tool: six questions to work through in sequence before you deploy capital into any falling asset. No single answer is a green light or red flag on its own. It is conviction across multiple questions that separates disciplined dip-buying from reactive impulse buying.

Questions about the asset

- Has the original thesis changed? Why did you own or consider this asset in the first place? Are the drivers, growth, margins, competitive moat, capital allocation, still intact? If the reason for owning it has changed or disappeared, a lower price does not fix that.

- Is the problem temporary or structural? A temporary problem looks like one bad quarter, cyclical softness, or a transient macro shock. A structural problem looks like a shrinking market, permanent loss of pricing power, technological disruption, or a broken business model. Buying the dip fits the former. It does not fit the latter.

- What does the balance sheet look like? Check cash versus debt, the debt maturity profile, interest costs, and refinancing risk. A weak business with heavy leverage is far more likely to be a trap than a similar business with net cash and operational flexibility.

Questions about your own thinking and portfolio

- Are you anchoring to prior highs? Is the attraction mainly that it “used to be at $100, so $40 is cheap”? Or does your forward analysis at $40, looking at prospective cash flows, growth outlook, and risk profile, justify a good expected return? If the argument is mostly backward-looking, anchoring is likely driving the decision.

- Is valuation actually attractive on forward metrics? Evaluate price against earnings, free cash flow, or book value adjusted for the new reality. A stock can be down 70% and still be expensive if earnings have collapsed by more than 70%. The percentage decline tells you nothing on its own; forward valuation metrics tell you everything.

Intrinsic value estimation, using discounted cash flow projections, comparable transaction multiples, or earnings power value calculations, gives investors a forward-anchored reference point that replaces the backward-looking comparison to prior highs that drives most anchoring errors.

- Does adding here improve your portfolio’s risk-reward? Think carefully about whether committing capital at this level genuinely shifts your portfolio’s expected return relative to the risk you are taking on. Consider how concentrated your position would become, how much of your existing exposure this overlaps with, and whether you could hold through a further decline without being forced to exit. If any of those considerations gives you pause, the apparent opportunity may not hold up under scrutiny.

If you can answer the first three questions with confidence and the last three with honesty, you will make materially better deployment decisions than the majority of investors who act on price movement alone.

When the index dip and the single-stock dip are not the same decision

A common mistake in dip-buying is to treat a broad index decline as equivalent to a fall in an individual stock. Both show up as a lower price on a chart, but the underlying risk profiles are quite different, and the amount of analytical work each demands is not remotely comparable.

A 10% pullback in a broad diversified index like the S&P 500 or MSCI World typically reflects macro or risk-off sentiment spread across hundreds of businesses. Long-term returns are driven by global economic growth, and diversification distributes risk across companies, sectors, and geographies. No single thesis being wrong can sink the vehicle. The recovery depends on broad economic forces, not on any one company getting its strategy right.

A 10% decline in a single stock, sector ETF, or narrow thematic fund is a different proposition entirely. Recovery depends on a specific thesis being intact: the business must still be competitive and profitable, the sector must still have a viable growth path, and the original rationale for owning it must still hold. There is no diversification to buffer a wrong call.

Dimensional Fund Advisors research on individual stock performance found that only a minority of individual stocks survive and outperform the market over long periods, with the median stock underperforming the index, a finding that helps explain why the diversified index dip and the single-stock dip carry such different statistical profiles.

The analytical burden is proportional to concentration. The narrower the vehicle, the more you need fundamental conviction rather than just a chart that went down. Before you buy any dip, the first question is not whether the price is attractive. It is what kind of vehicle you are looking at, because that determines how much work the decision actually requires.

| Attribute | Broad index dip | Single-stock or narrow thematic dip |

|---|---|---|

| Risk distribution | Spread across hundreds of holdings | Concentrated in one thesis or sector |

| Recovery driver | Broad economic growth and sentiment | Specific business or theme remaining viable |

| Analytical burden | Moderate: macro and valuation assessment | High: deep fundamental analysis required |

| Typical buying rationale | Long-term allocation at improved entry | Conviction that the thesis is intact |

The dip is a question, not an answer

A falling price is not a buy signal. It is an invitation to analyse. The quality of that analysis, not the speed of your response, determines whether the decision is disciplined or impulsive.

The strategy works. It works for the right assets, in the right circumstances, when the decline is driven by sentiment rather than structural damage. You now have both the mental model (two types of decline) and the practical checklist (six diagnostic questions) to identify those circumstances before you commit capital.

The next time an asset in your portfolio or watchlist falls, resist the reflex. Instead of reaching for the buy button, reach for the diagnostic question: why did this go down? If the answer is temporary sentiment and the fundamentals are intact, the dip may well be your opportunity. If the answer is structural deterioration, the dip is the market telling you something important, and the smartest move is to listen.

Investors curious about how much the difference between disciplined patience and reactive trading actually costs over time, in dollar terms and across realistic holding periods, will find our deep-dive into reactive versus passive investing outcomes illustrates the gap with a controlled 30-year simulation using identical monthly contributions across all three approaches.

This article is for informational purposes only and should not be considered financial advice. Investors should conduct their own research and consult with financial professionals before making investment decisions.