Why Off-the-Shelf CAR-T Has an Edge After BTKi Failure

36 mins ago

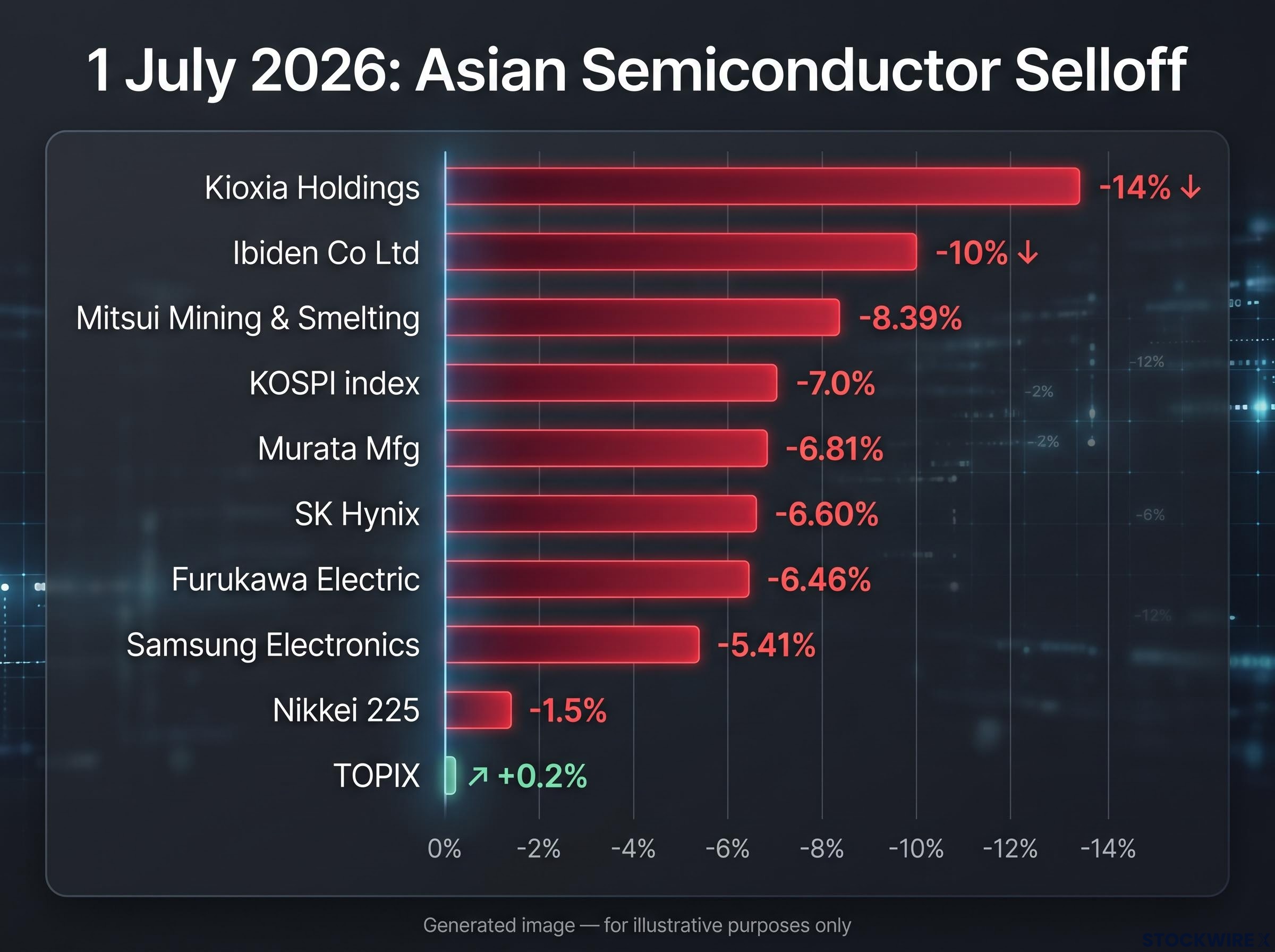

On 1 July 2026, Kioxia Holdings fell more than 14% in a single session. SK Hynix lost 6.6%. Samsung Electronics retreated to its weakest level since early June. A single day wiped out weeks of accumulated AI-rally gains across Asia’s semiconductor complex.

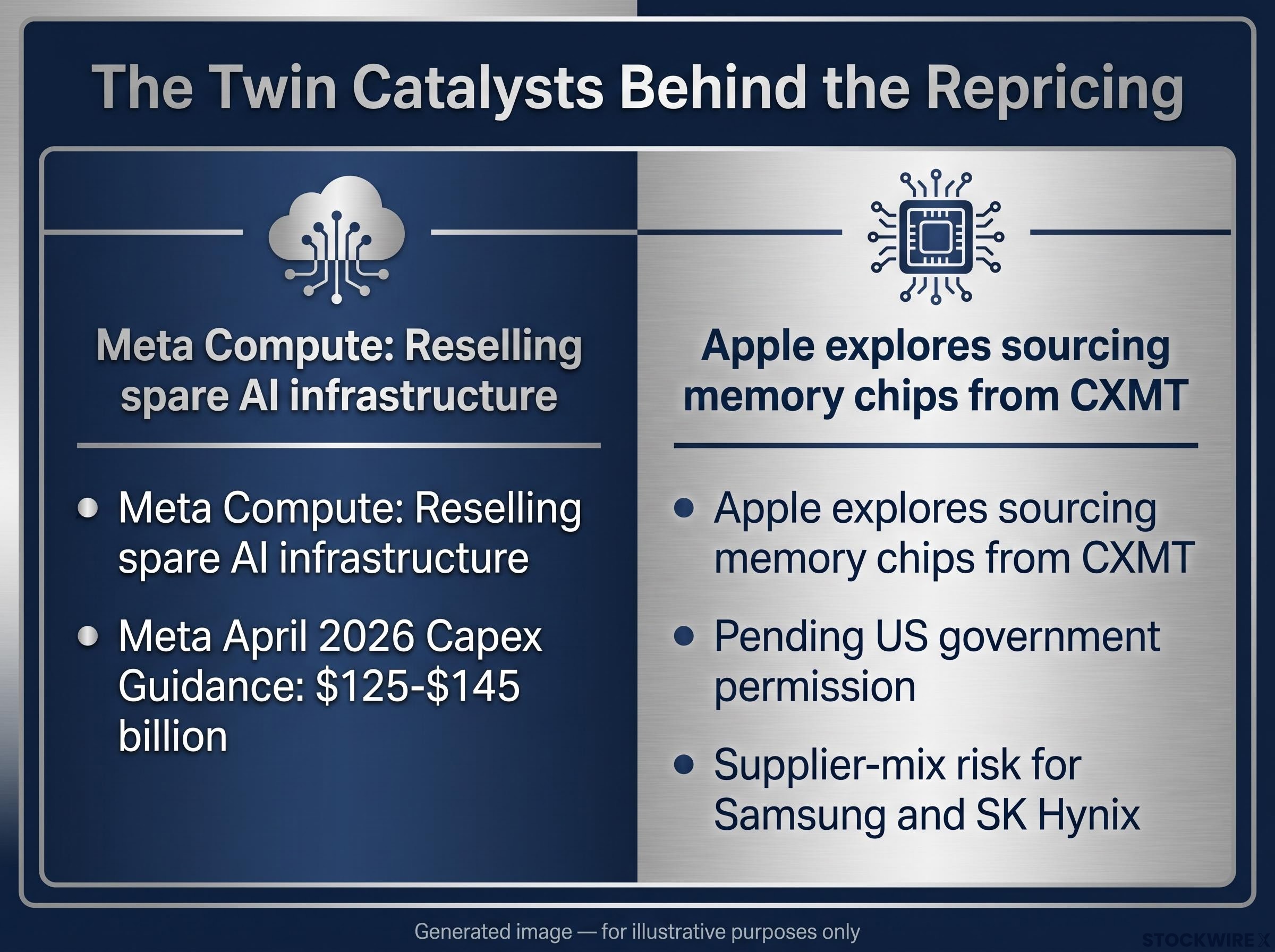

The trigger was not a profit warning, a product recall, or a macro shock. It was a report about Meta Platforms planning to sell its spare computing power, and a separate development about Apple exploring a new memory chip supplier. Neither confirmed a cut in AI infrastructure spending. Yet the reaction across Asian chip equities was immediate and severe, exposing how much of the sector’s recent valuation was built on an assumption of uninterrupted, exponential demand growth.

Here is what happened on 1 July, why these particular catalysts hit Asian semiconductor names so hard, and what the data tells you about whether this is a positioning unwind or the start of something more structural. Three specific indicators are worth watching to answer that question in the weeks ahead.

South Korea’s KOSPI benchmark dropped as much as 7% on 1 July 2026, its steepest single-session fall in several months. The damage radiated through both South Korean and Japanese chip names, but the index-level divergence in Tokyo told the real story: the Nikkei 225 fell approximately 1.5%, while the broader TOPIX edged up around 0.2%.

That split tells you the damage was concentrated in technology-exposed index constituents rather than reflecting any broad deterioration in Japan’s economic conditions. It is the first clue that positioning and sentiment are doing more work here than fundamentals.

Kioxia Holdings shed over 14% on 1 July, placing it among the steepest single-stock movers within the Nikkei 225 that session.

| Stock / Index | Session decline | Notable context |

|---|---|---|

| KOSPI | -7.0% | Steepest single-session fall in several months |

| Samsung Electronics | -5.41% | Weakest level since 8 June 2026 |

| SK Hynix | -6.60% | Lowest point since 17 June 2026 |

| Kioxia Holdings | -14%+ | Among largest Nikkei 225 constituent declines |

| Ibiden Co Ltd | -10%+ | Chip-packaging supplier |

| Mitsui Mining & Smelting | -8.39% | Materials supplier |

| Murata Mfg | -6.81% | Electronic components |

| Furukawa Electric | -6.46% | Cable and infrastructure |

The breadth of the losses across packaging, materials, and components shows how deeply the AI supply chain was de-risked in a single session.

The catalyst was not a spending cut. It was a monetisation pivot, and the distinction matters.

Bloomberg, Reuters, and The Information each confirmed that Meta is building an internal AI cloud business called Meta Compute, designed to sell excess computing capacity to external clients. The details:

None of those reports indicated confirmed capex cuts. Meta raised its 2026 capital expenditure guidance to $125-$145 billion in April 2026, and analyst estimates have referenced more than $700 billion in AI spending across big tech as the broader demand backdrop.

The Meta Compute initiative, confirmed by Bloomberg and corroborated by Reuters and The Information, targets two distinct revenue models: a hosted AI model platform comparable to AWS Bedrock, and raw GPU compute leasing closer to CoreWeave, each carrying different margin profiles and competitive implications for the broader hyperscaler market.

The implication is subtle but direct. If a hyperscaler the size of Meta is pivoting from “build as fast as possible” to “monetise what we have built,” the growth rate of incremental hardware orders could slow, even if absolute demand stays elevated. For investors holding chip stocks at AI-rally multiples, the relevant question is not whether Meta is cutting spend but whether the era of “build at any cost” is quietly giving way to “build to a return.” That shift alone could justify a multiple compression even with unit demand intact.

The second catalyst was structurally distinct. Reports corroborated by Finshots and TrendForce confirmed that Apple has approached the US government for permission to source memory chips from Chinese manufacturer CXMT, driven by AI-related memory shortages and rising prices.

Apple’s sourcing history demonstrates a consistent pattern of qualifying multiple vendors to reduce concentration risk and maintain pricing leverage. That history is exactly why the report was credible enough to move South Korean equities before any order was confirmed.

Apple’s supplier diversification history follows a consistent pattern across processors, displays, and baseband chips: the company qualifies multiple vendors, uses the threat of switching to extract pricing concessions, and occasionally executes partial shifts that permanently reshape incumbent revenue streams.

The distinction that matters here is between supplier-share displacement (what this threatens) and aggregate demand reduction (what this does not). Apple looking for a new vendor does not mean it is buying fewer chips. It means the share of revenue flowing to Samsung and SK Hynix could shrink.

Even a partial shift in Apple’s memory sourcing would represent a high-volume customer relationship changing. For Samsung and SK Hynix specifically, any reduction in Apple’s share of their revenue is directly relevant to near-term earnings models. That supplier-mix risk stacked on top of the demand-growth question from the Meta story, which is why South Korean names were hit harder than the broader Nikkei average on the same day.

When a sector drops this sharply on catalysts that do not confirm actual spending cuts, the first question is whether the macro backdrop broke at the same time. It did not.

Three data points argue against fundamental deterioration:

Both Micron Technology and SanDisk Corporation had each lost in excess of 10% during the prior overnight session before Asian markets opened on 1 July. Cross-regional correlation in crowded semiconductor names routinely produces moves that overshoot the underlying catalyst; when the largest US memory name drops double digits overnight, Asian counterparts follow reflexively.

The US futures recovery while Asian chip names were still falling hard tells you that US equity markets had already processed the catalyst and moved on. The Asian session was amplifying a US overnight move through reflexive correlation rather than independently pricing new information. That does not mean the concerns are invalid. It means the mechanism behind the magnitude matters when deciding how to respond.

Bank of America’s semiconductor positioning data, published in May 2026, showed active long-only overweight in the sector at approximately 20%, half the 40% peak recorded at the 2017 cycle high, a level that is elevated but inconsistent with the indiscriminate crowding typically associated with speculative tops.

The AI chip rally was built on one core assumption: near-unlimited short-term hyperscaler demand with minimal return-on-investment scrutiny. That assumption supported multiples that priced in exponential growth, not cyclical growth.

The shift from “build at scale” to “build for returns” compresses valuation multiples even when unit demand stays elevated, because the implied growth rate changes. A stock priced for 30% compound annual chip demand growth does not hold its multiple if the trajectory flattens to 15%, even though 15% is still strong growth.

Meta’s $125-$145 billion capex range for 2026 illustrates the scale of prior investment the market had been extrapolating forward. If other hyperscalers, Microsoft, Google, or Amazon, adopt similar compute-resale models or begin emphasising utilisation over expansion on upcoming earnings calls, the market will have to price a cyclical rather than exponential capex trajectory.

IDC’s semiconductor market forecasts project the global market exceeding $1 trillion in 2026, with hyperscaler capital expenditure rising roughly 70% year over year to approximately $600 billion, the demand baseline that chip valuations across Asia had been pricing in before the 1 July session.

If you hold chip stocks at multiples that price in exponential demand growth, the question is no longer whether AI spending is real but whether the growth rate assumed in your entry price is still defensible. That is a harder question to answer today than it was on 30 June.

This article is for informational purposes only and should not be considered financial advice. Investors should conduct their own research and consult with financial professionals before making investment decisions. These statements are speculative and subject to change based on market developments and company performance.

Rather than watching every headline, these three data points arrive in a roughly sequential order and each one answers a different piece of the puzzle:

These three data points will not arrive simultaneously, but tracking them in sequence gives you a structured way to distinguish between a sentiment reset that has already run its course and a repricing that has further to go. Contract DRAM and HBM pricing movements, particularly any shortening of contract tenors, are worth monitoring alongside them as a supply-side signal of declining order visibility.

For investors wanting a structured framework for deciding when to reduce chip exposure rather than reacting to individual sessions, our dedicated guide to semiconductor cycle timing covers the five-indicator sequence that tracks the transition from demand-driven pricing power to supply-wave correction, with specific attention to DRAM and HBM oversupply risk in 2028-2029.

The 1 July session is best read as a painful positioning unwind in a crowded AI hardware trade, not a confirmed structural collapse in chip demand. Neither catalyst, Meta’s compute monetisation plan nor Apple’s supplier exploration, confirmed a cut in AI infrastructure spending.

What did change is the narrative. The assumption of infinite, unquestioned demand growth gave way to something more nuanced: still-strong but ROI-conscious growth, where hyperscalers begin optimising what they have built rather than expanding indefinitely. That is a real and durable shift, even if unit demand stays elevated.

The question for anyone holding chip stocks at current multiples is no longer whether AI spending is real. It is whether the growth rate baked into your entry price remains defensible as the hyperscaler complex enters a more mature, returns-focused phase.

—

Two reports triggered the selloff: Meta Platforms was confirmed to be building an internal AI cloud business called Meta Compute to resell spare computing capacity, and Apple was reported to be seeking US government approval to source memory chips from Chinese manufacturer CXMT. Neither report confirmed a cut in AI infrastructure spending, but both raised questions about the growth-rate assumptions baked into chip valuations.

Meta Compute is an internal Meta Platforms programme designed to sell excess AI computing capacity to outside buyers, confirmed by Bloomberg, Reuters, and The Information on or around 1 July 2026. It matters for chip investors because it signals a potential shift from aggressive hardware expansion to monetising existing infrastructure, which could compress the implied growth rate for incremental chip orders even if absolute spending stays high.

Samsung Electronics fell 5.41% to its weakest level since 8 June 2026, while SK Hynix dropped 6.60% to its lowest point since 17 June 2026. Kioxia Holdings was the steepest faller, shedding more than 14% in the single session.

No, the Apple CXMT report signals potential supplier-share displacement, not a reduction in total chip purchases. Apple buying from CXMT would mean the revenue share flowing to Samsung and SK Hynix could shrink, even if Apple's overall memory volumes stay the same or grow.

The three key indicators are: Micron's next forward guidance update (which will signal whether memory order visibility is intact), the US government's decision on Apple's CXMT sourcing request (which will determine how far South Korean incumbent supply-chain risk actually progresses), and the language used by Microsoft, Google, and Amazon on upcoming earnings calls (listen for 'utilisation optimisation' versus continued 'capacity expansion' framing to gauge whether Meta's monetisation pivot is industry-wide or idiosyncratic).