How to Run a Scenario-Based Stock Valuation Analysis

14 mins ago

In November 2025, a single trader controlled up to 73% of the daily trading volume in three ASX-listed small-cap stocks, artificially distorting prices before regulators intervened. That trader, Behzad Eghrari, was sentenced to 15 months imprisonment. Most retail investors caught in a manipulation scheme never receive that kind of resolution.

Market manipulation is not a theoretical risk on the Australian Securities Exchange. ASIC treats it as an enduring enforcement priority, and prosecution records from 2021 through 2025 show a consistent pattern: small-cap stocks, coordinated accounts, social media promotion, and retail investors left holding devalued positions. Understanding what manipulation looks like in practice is the first line of defence for any investor.

This article explains how the most common manipulation tactics work at a mechanical level, what warning signs appear before a scheme reaches its conclusion, how front-running specifically breaches the trust relationship between broker and client, and what ASIC’s enforcement powers mean for investor protection in practice.

Every time an investor checks a stock’s price or reviews its trading volume, they rely on an assumption they rarely examine: that those numbers reflect genuine buying and selling by real participants with real intent. Price discovery, the process through which markets determine what a security is worth, only functions when the activity behind it is authentic.

Market manipulation attacks that assumption directly. When trading volume is fabricated or prices are artificially moved, the signals every other investor depends on become unreliable. The harm extends beyond the immediate victims of a scheme; it degrades the information environment that all participants use to make decisions.

Under the Corporations Act 2001 (Cth), sections 1041A and 1041B define manipulation as intentional conduct that creates a false or misleading appearance of trading activity or artificially affects the price of financial products. ASIC has described the damage in direct terms: manipulation undermines “honest participants” and erodes public confidence in the financial system.

ASIC’s enforcement priorities explicitly list market integrity misconduct, including insider trading, continuous disclosure breaches, and market manipulation, as a standing focus area, providing the regulatory foundation for the prosecutions that have resulted in imprisonment sentences across multiple ASX small-cap cases.

“Misconduct damaging market integrity, including market manipulation, is an enduring enforcement priority for ASIC.”

That framing matters. It positions manipulation not as a niche compliance issue but as a direct threat to the infrastructure every Australian investor relies on.

Four tactics appear repeatedly in Australian enforcement records. Each distorts a different part of the market’s information system, and each leaves an observable trace that investors can learn to identify.

| Tactic | How it works | Observable signal | Typical target |

|---|---|---|---|

| Wash trading | Simultaneous buy-sell activity in the same security to simulate volume without genuine change in ownership | Inflated volume figures that misrepresent liquidity | Low-liquidity small-cap stocks |

| Spoofing | Placing large orders with no intention of execution to manipulate perceived order book depth, then cancelling before fill | Artificial price pressure that vanishes when orders disappear | Securities with visible order books |

| Pump-and-dump | Accumulating a position, promoting it through false or exaggerated claims to attract buyers, then selling at inflated prices | Price spike detached from any ASX announcement | Thinly traded small-cap stocks |

| Front-running | Trading ahead of a known pending client order to profit from the anticipated price movement | Unusual positioning just before large order execution | Any security with large institutional order flow |

The Eghrari case illustrates how volume distortion works in practice. His trades accounted for up to 73% of total daily trading volume across Investigator Resources Limited (ASX: IVR), Silver Mines Ltd (ASX: SVL), and Lumos Diagnostics Holdings Ltd (ASX: LDX). That level of concentration in small-cap stocks created a misleading picture of genuine market interest.

Gabriel Govinda, who operated under the online alias “Fibonarchery,” demonstrated the social media dimension. In May 2023, Govinda pleaded guilty to 23 counts of market manipulation and received 2.5 years imprisonment. The alias itself pointed to the promotion vehicle: coordinated online activity designed to recruit buyers into positions the manipulator intended to exit.

Pump-and-dump schemes are particularly effective in low-liquidity markets, where relatively small amounts of capital can generate outsized price movements.

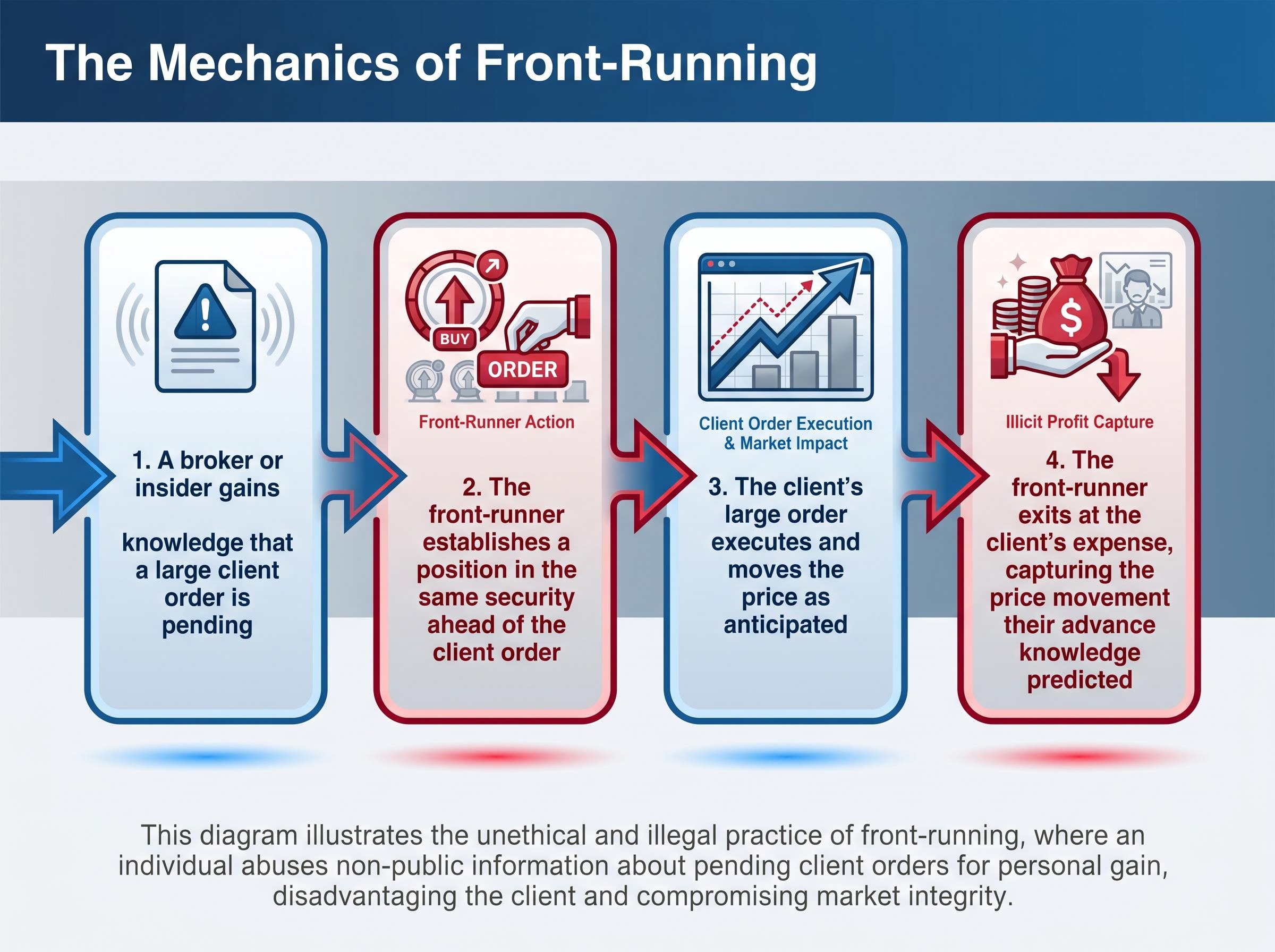

When an investor places a large order through a licensed broker, they trust that the broker will execute it faithfully. Front-running inverts that trust. It exploits the broker’s privileged access to non-public order flow information, turning the client’s own trading activity into a profit opportunity for the person handling it.

The mechanics follow a specific sequence:

The harm is not abstract. Every cent the front-runner captures comes directly from the client’s execution quality. The client pays a worse price because someone with a duty to act in their interest traded against them instead.

What distinguishes front-running from other manipulation tactics is that it requires a position of trust. Wash trading and spoofing exploit public market mechanisms. Front-running exploits the specific relationship between a client and the person handling their order.

The Quantum Resources conspiracy case (involving Don Evans, Avrohom Kimelman, and Benjamin Cooper, prosecuted between 2021 and 2023) demonstrated how privileged insider positioning and market manipulation intersect. Sentences ranged from 12 to 18 months imprisonment across the three defendants, with Kimelman (then CEO and director) receiving the longest sentence.

Front-running carries dual legal exposure. Under the Corporations Act 2001 sections 1041B-1041E, it constitutes a market manipulation offence carrying criminal penalties of up to 15 years imprisonment. It also represents a breach of fiduciary duty to the client whose order was exploited.

Civil penalties can reach $1.65 million for an individual (5,000 penalty units at $330 per unit as of May 2026), or three times the benefit obtained and detriment avoided, whichever is greater. ASIC holds both investigation and prosecution authority for these offences.

Each of the following warning signs has appeared in documented Australian manipulation cases. They function best as diagnostic questions applied in real time, before capital is committed.

The obligation to verify price movements against ASX announcements is grounded in something more than good practice: continuous disclosure obligations legally require listed companies to release any market-sensitive information as soon as they become aware of it, meaning a price spike with no corresponding announcement is not merely suspicious but potentially a signal that the market is operating on fabricated rather than disclosed information.

The Scamwatch Targeting Scams report for 2025, published by the ACCC in March 2026, provides the authoritative source for the $837.7 million investment scam loss figure and the $2.18 billion total scam losses recorded across Australia that year, confirming the scale of financial harm now amplified by AI-generated deepfake content.

“This practice is even more damaging in small-cap securities, where even small trades can trigger significant price swings.”

Resources for verification include ASIC MoneySmart’s guidance on pump-and-dump scams (moneysmart.gov.au/investment-warnings/pump-and-dump-scams) and detecting share scams (moneysmart.gov.au/investments/share-investing/detecting-share-scams).

ASIC’s enforcement authority under the Corporations Act 2001 covers the full pipeline: surveillance, investigation, referral for prosecution, and pursuit of civil penalties. The agency works alongside the Office of the Director of Public Prosecutions (Commonwealth), which handles criminal prosecutions.

ASIC’s market surveillance capability depends on accurate transaction-level data flowing from market participants; when that data is corrupted, as in Macquarie Securities’ 14-year misreporting of up to 1.5 billion short sale transactions, the regulator’s ability to detect the abnormal volume patterns that characterise manipulation schemes is directly compromised.

The Eghrari case illustrates how this pipeline operates in practice. ASIC’s investigation led to charges filed on 14 March 2025 (Release 25-039MR). By November 2025 (Release 25-302MR), Eghrari had been convicted and sentenced to 15 months imprisonment, released immediately on a recognisance order requiring two years of good behaviour. The elapsed time from charge to sentencing was approximately eight months.

That timeline points to a realistic limitation. Enforcement happens after harm has already occurred. Investors who bought into manipulated stocks during the scheme’s active phase may have already absorbed losses before ASIC’s intervention produced a public outcome. The deterrence value is real, but it does not eliminate risk for those caught early in a manipulation.

ASIC’s active focus areas as of 2025 include small-cap securities manipulation, coordinated multi-account trading, and social media-coordinated pump-and-dump schemes. Civil proceedings against COFCO International Australia Pty Ltd and COFCO Resources SA for futures market manipulation, filed in July 2024 (Release 24-163MR), remain ongoing as of May 2026.

Penalties operate on two tracks: criminal and civil. Criminal prosecution can result in imprisonment of up to 15 years. Civil penalties are calculated as the greater of a flat penalty unit figure or three times the benefit obtained and detriment avoided by the offender.

| Offender type | Penalty category | Maximum penalty | Example case |

|---|---|---|---|

| Individual | Criminal | 15 years imprisonment | Govinda: 2.5 years |

| Individual | Civil | $1.65 million (5,000 penalty units) or 3x benefit | Eghrari: 15 months (criminal track) |

| Corporation | Civil | $16.5 million (50,000 penalty units), 3x benefit, or 10% annual turnover | COFCO: proceedings ongoing |

The three-times-benefit formula means that penalties can exceed the flat unit calculation significantly where large profits were extracted from the manipulation. This structure is designed to ensure that the financial consequences of market manipulation exceed its rewards. Current enforcement reports are available at asic.gov.au/about-asic/news-centre/reports/enforcement-reports/.

The debate over whether penalties deter institutional misconduct is not abstract: when Macquarie Securities received a $35 million civil penalty for 14 years of short sale misreporting affecting up to 1.5 billion transactions, critics argued the figure was financially immaterial to a firm of that scale, raising the same structural question the three-times-benefit formula in manipulation cases is designed to answer.

The red flags and enforcement patterns described throughout this article translate into a repeatable set of verification habits. Applied consistently, these actions function as a personal protection protocol rather than a one-off checklist.

This article is for informational purposes only and should not be considered financial advice. Investors should conduct their own research and consult with financial professionals before making investment decisions.

The enforcement record is clear. Eghrari received 15 months imprisonment. Govinda received 2.5 years. Kimelman received 18 months. ASIC has demonstrated a consistent willingness to prosecute market manipulation across small-cap securities, coordinated schemes, and futures markets.

ASIC’s enforcement posture has expanded well beyond equities markets: the regulator secured a $10 million Federal Court penalty against Binance Australia in 2026 and won a landmark case against Kraken’s Australian operator in 2024, establishing that the same design and distribution obligations protecting retail investors in traditional securities markets now apply across crypto derivative platforms.

The limitation is equally clear. The timeline between a manipulation scheme’s peak activity and its prosecution means retail investors cannot rely on regulatory action alone as their first protection. The most consistent warning sign across all documented Australian cases is abnormal volume relative to a stock’s normal liquidity profile. It is the single most accessible diagnostic available to retail investors, and it requires nothing more than checking the numbers before committing capital.

The combination of ASIC’s enforcement infrastructure and an investor’s own verification habits creates the protective environment Australia’s markets are designed to deliver. For ongoing resources, ASIC MoneySmart (moneysmart.gov.au) provides current guidance on identifying scams, and ASIC’s tip-off service allows investors to report suspicious activity directly into the enforcement pipeline.

Market manipulation on the ASX refers to intentional conduct that creates a false or misleading appearance of trading activity or artificially affects the price of financial products, as defined under sections 1041A and 1041B of the Corporations Act 2001. Common tactics include wash trading, spoofing, pump-and-dump schemes, and front-running.

A pump-and-dump scheme involves a manipulator accumulating a position in a thinly traded stock, promoting it through false or exaggerated claims to attract buyers, then selling at the inflated price and leaving other investors with devalued holdings. These schemes frequently target low-liquidity ASX small-cap stocks and are often coordinated through social media.

Key warning signs include abnormal trading volume concentration in a low-liquidity stock, price spikes with no corresponding ASX announcement, unsolicited investment tips via social media or messaging platforms, pressure tactics urging immediate action, and fake celebrity endorsements or deepfake videos promoting specific stocks.

In Australia, criminal prosecution for market manipulation can result in imprisonment of up to 15 years, while civil penalties for individuals can reach $1.65 million or three times the benefit obtained, whichever is greater. Recent cases include Behzad Eghrari sentenced to 15 months and Gabriel Govinda sentenced to 2.5 years imprisonment.

Investors can report suspected market manipulation directly to ASIC through its online tip-off service at asic.gov.au, and these whistleblower reports feed directly into ASIC's enforcement pipeline. ASIC holds full authority to investigate, pursue civil penalties, and refer cases to the Commonwealth Director of Public Prosecutions for criminal charges.