VGS Leads Vanguard ETF Pack With 14% FY26 Capital Return

4 hrs ago

Most retail investors can tell you what a bank’s dividend yield is. Very few can explain whether that yield is being generated from a position of strength or structural fragility. Three numbers answer that question: Net Interest Margin (NIM), Return on Equity (ROE), and the Common Equity Tier 1 (CET1) capital ratio. These are the metrics that separate informed bank stock analysis from surface-level screening.

Australian bank stocks sit among the most widely held equities by retail investors, yet the figures that reveal a bank’s underlying health are routinely overlooked in favour of simpler signals like yield or share price momentum. With ASX regional banks including Bendigo and Adelaide Bank (ASX: BEN) and Bank of Queensland (ASX: BOQ) posting meaningfully different results from the majors, understanding how to read these figures has become increasingly useful. This guide explains what NIM, ROE, and CET1 actually measure, how each is calculated, what current ASX sector benchmarks look like, and how to apply all three diagnostically using BEN’s most recent results as a worked example.

Bank stocks look simple. They pay reliable dividends, report familiar-sounding earnings figures, and trade on price-to-earnings ratios like any other equity. Yet they routinely behave in ways that confuse investors using standard industrial-company tools, and the reason is structural.

Banks are balance-sheet businesses. The product being sold is money itself. Lending income accounted for approximately 87% of BEN’s total revenue in its most recent full year, illustrating why the lending spread dominates bank economics in a way that no single revenue line dominates an industrial company. Traditional metrics like EBIT margin or standalone P/E ratios were designed for businesses that manufacture goods or deliver services; they are largely inadequate as standalone diagnostic tools for an institution whose profitability, efficiency, and safety are intertwined with regulatory capital requirements.

PE ratios for bank stocks carry a structural problem that does not apply to industrial companies: a single provision movement or one-off remediation charge can shift reported earnings by hundreds of millions of dollars without any change in the underlying lending business, making the ratio an unreliable standalone signal for sector comparisons.

That interconnection is precisely why regulators, credit analysts, and bank equity specialists use a dedicated set of metrics. Three cover the dimensions that matter most:

Each metric answers a different question. Together, they form a diagnostic picture that dividend yield alone cannot provide.

The concept is mechanically simple. Banks borrow money (through deposits and wholesale funding) at one rate and lend it out at a higher rate. NIM captures that spread: interest income minus interest expense, divided by average interest-earning assets, expressed as a percentage.

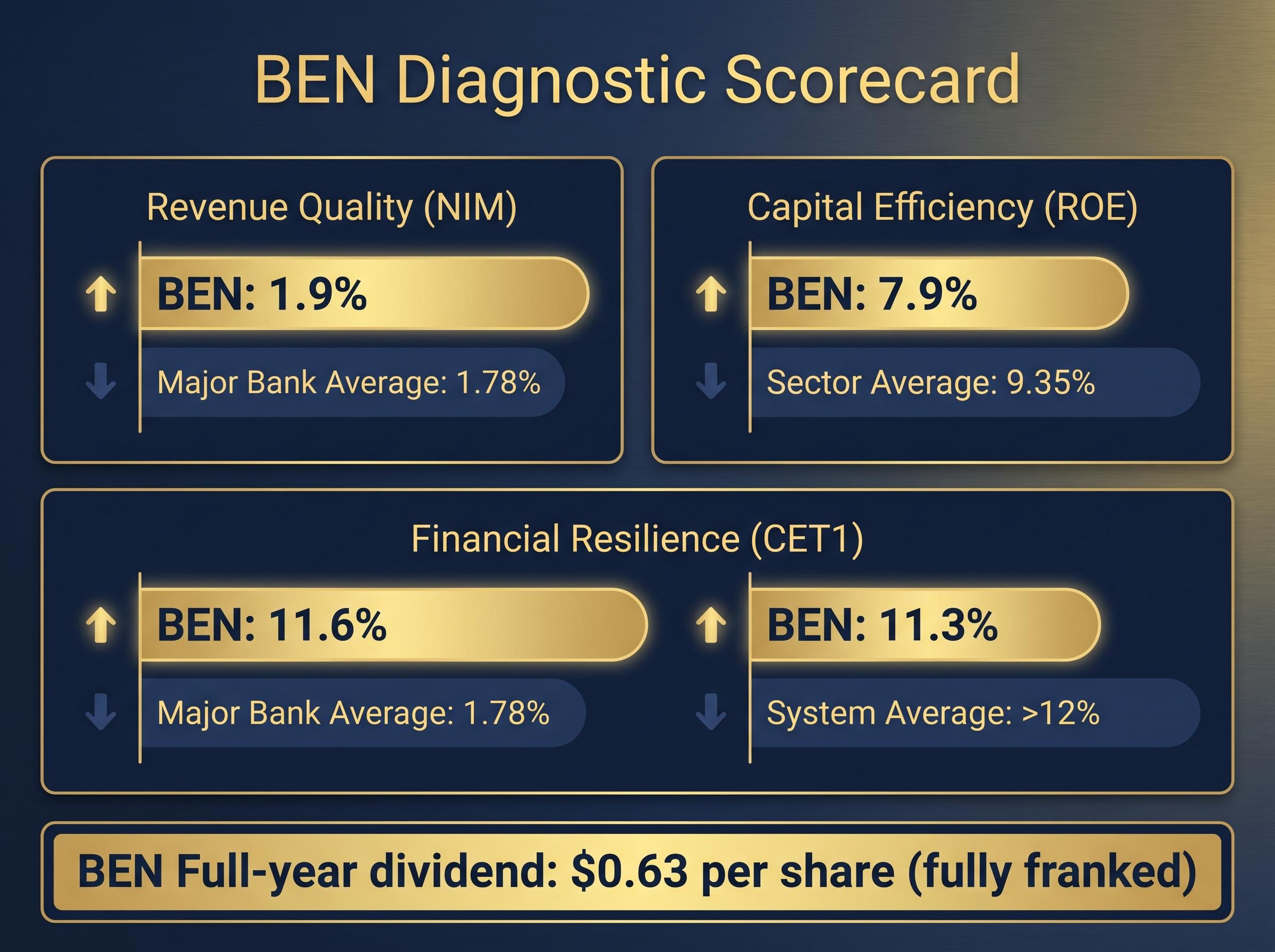

A NIM of 1.9% means the bank earns roughly 1.9 cents of net interest revenue for every dollar of interest-earning assets on its books. That figure belongs to BEN, which reported a 1.9% NIM for its most recent full year, above the ASX major bank average of 1.78% according to Rask calculations.

| Bank | NIM | Period |

|---|---|---|

| BEN | 1.90% | Most recent full year |

| BOQ | 1.64% | FY25 (August 2025) |

| Major bank average | 1.78% | Rask calculations |

The spread looks stable, but it is far more volatile and competitively contested than it first appears.

Early in the RBA’s hiking cycle, loan yields repriced faster than deposit costs. Banks earned more on every variable-rate mortgage before savers demanded matching increases on their term deposits. NIM expanded.

Then the second phase arrived. Competition for term deposits and at-call savings intensified. Customers shifted from low-cost transaction accounts to higher-yield deposit products. Regional banks like BEN and BOQ felt this compression more acutely than the majors because they rely more heavily on term deposits and wholesale funding rather than large, low-cost transactional deposit bases.

The RBA Financial Stability Review on net interest margins documents how deposit competition and funding cost shifts during rate cycles compressed NIM across advanced economy banks in the first half of 2024, providing a macroprudential context for the compression pattern observed at ASX regional banks.

“When the RBA raises rates, banks earn more on loans, but if they have to pay much more to keep deposit customers, the benefit to NIM is eroded.” — Morningstar Australia

BOQ’s trajectory illustrates the pattern clearly. Its NIM declined from 1.72% in FY23 to 1.64% in FY24 before stabilising at 1.64% in FY25, suggesting the compression reached a new equilibrium rather than continuing to worsen. A sustained NIM above peers signals pricing power and a stickier deposit base. A falling NIM signals competitive pressure that will flow through to earnings.

NIM movement and its earnings implications are not always reflected in headline profit figures on the day of a result, as NAB’s H1 2026 experience demonstrated: its NIM expanded 3 basis points to 1.81% on improved deposit outcomes, a positive signal for revenue quality, yet the share price still fell nearly 3% as markets focused on other elements of the disclosure.

ROE answers an intuitive question: how much profit does the bank generate per dollar of shareholders’ equity? The calculation is net profit attributable to ordinary shareholders divided by average ordinary shareholders’ equity, expressed as a percentage.

For banks, that number carries a structural nuance. Banks are naturally leveraged businesses, meaning they operate with far more borrowed money relative to equity than a typical industrial company. Their ROE reflects both operational efficiency and the amount of capital they choose (or are required) to hold. A bank holding more CET1 capital than required will typically report a lower ROE, all else equal, because the same profit is spread across a larger equity base.

ASX bank disclosures almost universally use cash ROE as the primary metric rather than statutory ROE. Cash ROE strips out the amortisation of intangibles and one-off items, providing a cleaner view of recurring profitability.

A bank can lift ROE by reducing its capital base (increasing leverage) rather than by improving underlying profitability. That distinction matters. It is why ROE must always be read alongside the CET1 ratio, which directly measures how much loss-absorbing capital the bank holds.

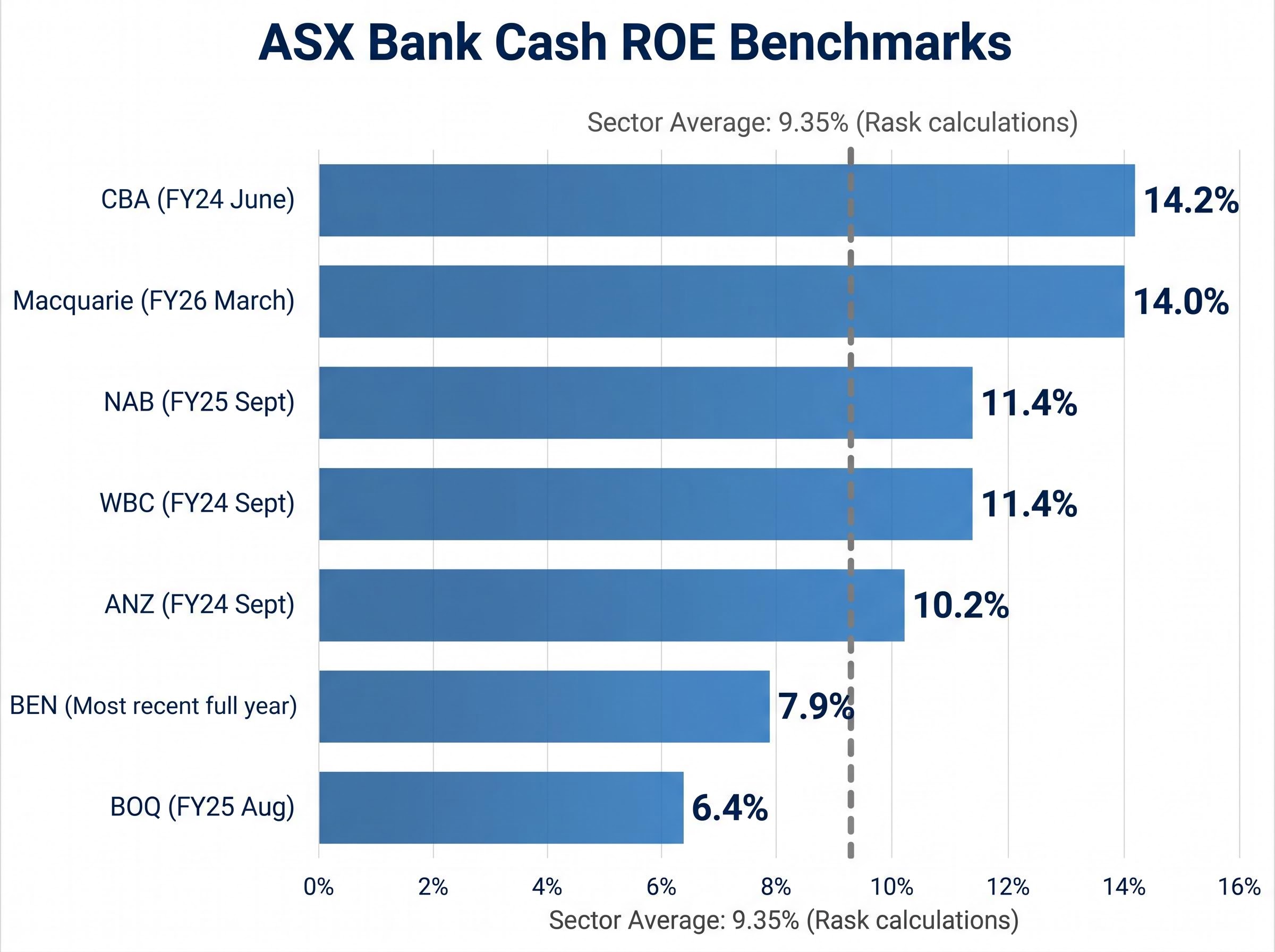

| Bank | Cash ROE | Period |

|---|---|---|

| CBA | 14.2% | FY24 (June 2024) |

| Macquarie | 14.0% | FY26 (March 2026) |

| NAB | 11.4% | FY25 (September 2025) |

| WBC | 11.4% | FY24 (September 2024) |

| ANZ | 10.2% | FY24 (September 2024) |

| BEN | 7.9% | Most recent full year |

| BOQ | 6.4% | FY25 (August 2025) |

BEN’s 7.9% ROE sits below the sector average of 9.35% (Rask calculations), while BOQ’s 6.4% cash ROE (up 70bps from FY24) remains at the bottom of the peer group. Macquarie Group’s 14.0% group ROE for FY26 contextualises the upper end of the range, though its diversified business model (not purely banking NIM) explains the structurally higher return profile. Persistently low ROE relative to peers signals either a structural cost disadvantage, excess capital, or pricing weakness, and each of those diagnoses carries different investment implications.

If ROE measures efficiency, CET1 answers the more fundamental question: what happens to this bank if loans start going bad?

The CET1 ratio is Common Equity Tier 1 capital, which consists of paid-up share capital plus retained earnings minus regulatory deductions, divided by risk-weighted assets. Risk-weighted assets assign different weightings to different loan types based on their probability of default; a residential mortgage carries a lower risk weight than an unsecured business loan.

Under the capital reforms effective 1 January 2023, APRA requires major banks to hold CET1 ratios of at least 10.25-10.75% including buffers. Regional banks face somewhat lower minimums but are still expected to maintain meaningful buffers above those floors. APRA has not announced new higher CET1 minimums specifically targeting regional banks since January 2024, though any APRA-driven increase in operational risk capital or mortgage risk weights could pressure regionals’ CET1 headroom even without a formal minimum change.

APRA’s unquestionably strong capital framework, effective from 1 January 2023, established the updated CET1 benchmarks and prudential standards that now define the minimum capital expectations for all authorised deposit-taking institutions operating in Australia.

APRA’s 2023-24 stress test confirmed that under severe scenarios, CET1 ratios fell materially but remained above minimum requirements for almost all banks. System-wide, the CET1 ratio sat above 12% on an APRA basis as of the December 2024 quarter.

| Bank | CET1 Ratio | APRA Basis | Period |

|---|---|---|---|

| Macquarie | 12.8% | Level 2 | March 2026 |

| BEN | 11.3% | APRA | Most recent full year |

| BOQ | 10.94% | APRA | FY25 (August 2025) |

According to Livewire Markets, BEN and BOQ are both above APRA minimums but typically hold smaller absolute buffers than the major banks. A CET1 below peers does not automatically signal danger, but it does mean the bank has less room to absorb credit losses or regulatory capital increases before operational adjustments become necessary. The practical implications of a below-peer CET1 ratio include:

The ROE-CET1 trade-off is direct. Holding more capital than required protects depositors and reduces insolvency risk, but it dilutes ROE because profit is spread across a larger equity base. Investors evaluating bank stocks need to decide where they sit on that spectrum.

Individually, each metric delivers a partial verdict. Together, they produce a coherent diagnostic picture.

BEN’s three most recent readings place the bank in a specific position within the ASX banking sector:

The internal logic connecting the three is worth examining. BEN’s above-average NIM suggests its core lending operations generate competitive spreads. Yet the below-average ROE indicates something is preventing that revenue strength from flowing through to shareholder returns, whether that is a higher cost base (BEN operates over 500 community branches and agencies), capital drag, or both. The below-average CET1 relative to the system means BEN has less buffer than some peers, which is relevant context when assessing dividend sustainability and growth capacity. BEN’s full-year dividend of $0.63 per share (fully franked) sits against that capital and earnings backdrop.

For income-oriented investors, the grossed-up yield on a fully franked bank dividend can be materially higher than the headline cash figure quoted on most broker screens, a gap that widens significantly for pension-phase SMSF members who receive excess franking credits as a direct ATO cash refund rather than a tax offset.

The diagnostic value comes from reading all three together. A single strong metric does not produce an unambiguous buy signal. The framework reveals where the gaps are and, critically, why they exist.

The concepts above convert into a repeatable process. The next time an ASX bank reports results, apply these three steps in sequence:

Where to find each metric: NIM is typically disclosed in the Group Performance Summary or Net Interest Income slide of an investor presentation. ROE appears in the Group Performance Summary. CET1 is disclosed in the Capital section. BOQ provides a useful peer comparison for BEN given their similar regional positioning, while Macquarie Group serves as a useful upper-bound contrast on ROE, noting that its diversified business model explains its structurally higher return profile.

When a metric reads as an outlier, the following diagnostic questions help identify the cause:

NIM, ROE, and CET1 are not independent signals. They are three lenses on the same institution, and reading them together reveals whether a bank’s profitability is structurally sound, adequately capitalised, and efficiently run. A strong NIM paired with a weak ROE raises a different set of questions than a strong ROE paired with a thin CET1 buffer. The diagnostic value lives in the combination.

These three metrics form the analytical layer that precedes any valuation work. Understanding what a bank earns, how efficiently it converts that revenue to shareholder returns, and how safely it operates is the necessary foundation before assessing whether the share price is cheap or expensive. A dividend discount model, for instance, relies on the earnings capacity and capital sustainability that NIM, ROE, and CET1 collectively reveal.

For investors ready to convert the three-metric diagnostic into an actual price, our dedicated guide to valuing ASX bank stocks with a DDM walks through a full Dividend Discount Model using BOQ’s verified FY2025 figures, including how to adjust the required return for a below-average ROE and how to gross up the dividend for franking credits before arriving at an indicative fair value.

The framework applies to any ASX bank result, whether BEN, BOQ, or the next major bank reporting period. Bookmark this guide for reference during the next reporting season, and use it as the diagnostic step before reaching for a valuation calculator.

This article is for informational purposes only and should not be considered financial advice. Investors should conduct their own research and consult with financial professionals before making investment decisions.

Net Interest Margin is the difference between the interest income a bank earns on loans and the interest it pays on deposits and funding, divided by its average interest-earning assets. It measures how profitably a bank is managing its core lending spread, with a higher NIM generally indicating stronger pricing power.

The CET1 (Common Equity Tier 1) ratio measures a bank's core equity capital relative to its risk-weighted assets, showing how much of a loss-absorbing buffer the bank holds. APRA requires Australian major banks to maintain CET1 ratios of at least 10.25-10.75% including buffers, and a ratio close to that floor signals limited room to absorb credit losses, support dividend growth, or fund buybacks.

Start by checking NIM against sector peers and the bank's own recent trend to assess revenue quality, then compare ROE to both peer averages and the risk-free rate to gauge capital efficiency, and finally review CET1 against APRA minimums and the bank's stated target range to assess financial resilience. Reading all three together reveals whether a bank's profitability is structurally sound before any valuation work begins.

A bank can raise its ROE by reducing its capital base, effectively increasing leverage, rather than by genuinely improving profitability. This is why ROE must always be assessed alongside the CET1 ratio, which reveals whether the equity base supporting that return is adequate or has been reduced to a level that increases financial risk.

Regional banks like Bendigo and Adelaide Bank and Bank of Queensland rely more heavily on term deposits and wholesale funding rather than large, low-cost transactional deposit bases, making their NIMs more sensitive to deposit competition during rate cycles. This structural difference explains why BOQ's NIM declined from 1.72% in FY23 to 1.64% in FY25 as deposit competition intensified following the RBA's hiking cycle.