Zscaler shares have fallen roughly 30% since the company’s most recent earnings release, settling near $126 per share and extending a year-to-date decline of approximately 31% as of late April 2026. The peculiar detail: the quarter itself was not poor. Revenue, adjusted operating profitability, and adjusted earnings per share all surpassed management’s own prior guidance. A stock that beats on every reported metric and then sheds a third of its value is not reacting to what just happened. It is repricing what comes next. The combination of decelerating annual recurring revenue (ARR) growth guidance, a near-total absence of new customer momentum, two senior sales leadership departures, and accelerating competitive pressure from Palo Alto Networks has shifted the market’s read from high-growth compounder to maturing platform under pressure. What follows is a framework for evaluating what the selloff reveals operationally, how structural the competitive threats are, and whether the post-drop valuation offers a reasonable entry point or reflects a deteriorating business story.

Why the market punished a beat-and-guide quarter

The contradiction between strong execution and a collapsing share price disappears once the mechanics of high-multiple growth stock pricing are made explicit. Zscaler beat its own guidance. That is the backward-looking fact. The forward-looking fact is what repriced the stock.

Growth-stage SaaS companies trade on the slope of future revenue expansion, not the current quarter’s reported numbers. A downward revision to the growth trajectory reprices the entire discounted cash flow model in a single session; every future year’s revenue, margins, and terminal value compress simultaneously.

The contradiction between strong execution and a collapsing share price is a direct consequence of growth stock valuation mechanics: when a high-multiple SaaS company trades on the slope of future revenue expansion rather than current earnings, a downward guidance revision compresses the entire discounted cash flow model simultaneously, repricing every future year of revenue, margins, and terminal value in a single session.

The specific guidance numbers that triggered the selloff:

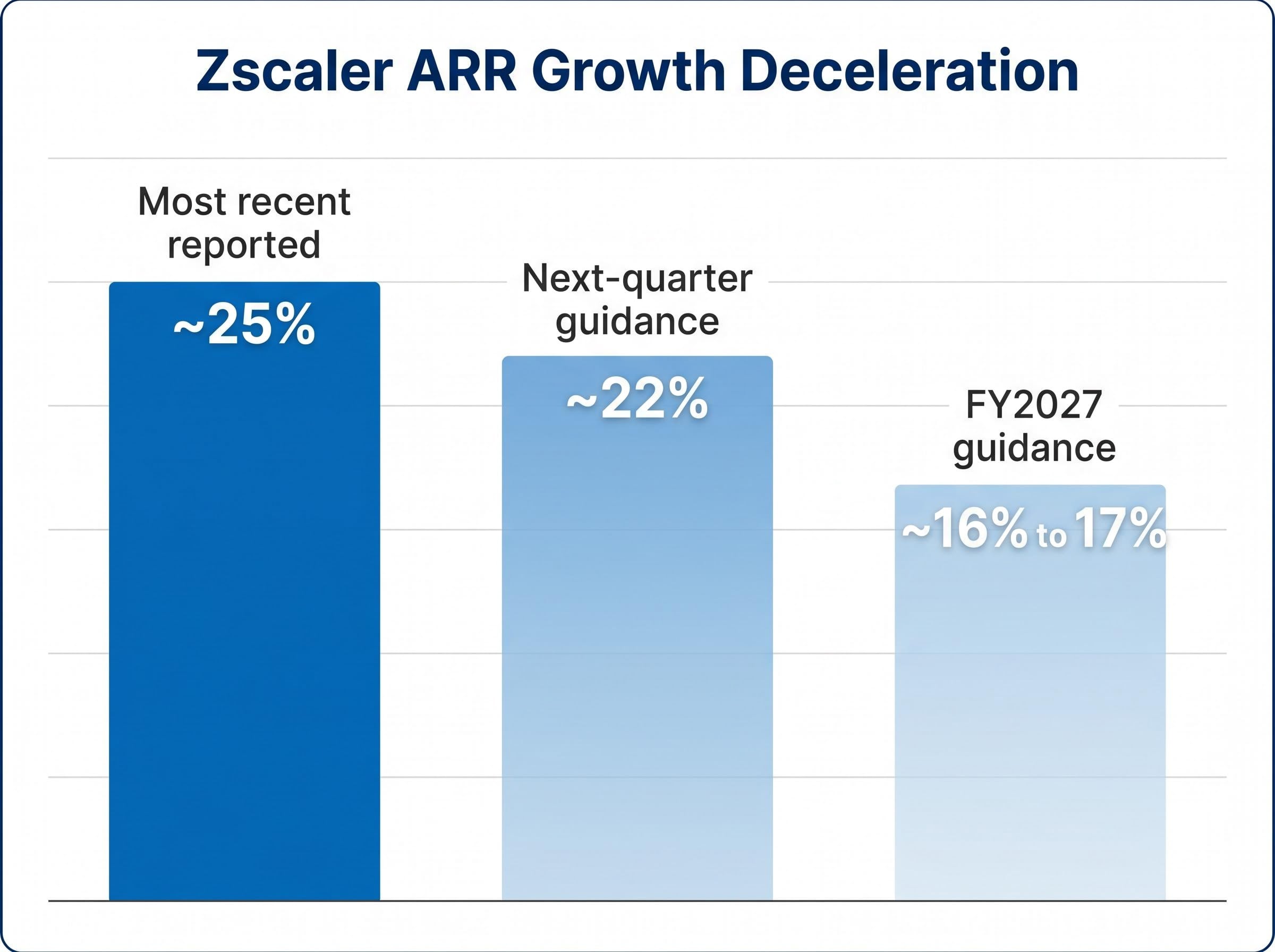

- Most recent reported ARR: approximately $3.5 billion, growing at roughly 25%

- Next-quarter ARR growth guidance: approximately 22%, a clear step down

- Fiscal year 2027 ARR growth guidance: approximately 16% to 17%, a material deceleration from the recently reported pace

FY2027 ARR growth guidance: approximately 16% to 17%. This single figure, more than any other data point in the earnings release, anchors the market’s concern about where the growth curve is headed.

At a post-decline price of approximately $126 and an implied market capitalisation of roughly $20 billion, the stock now trades at approximately a 4% free cash flow yield. The market is not punishing a bad quarter. It is repricing a slower future.

When big ASX news breaks, our subscribers know first

Zscaler’s Stalled New Logo Growth Outweighs High Retention

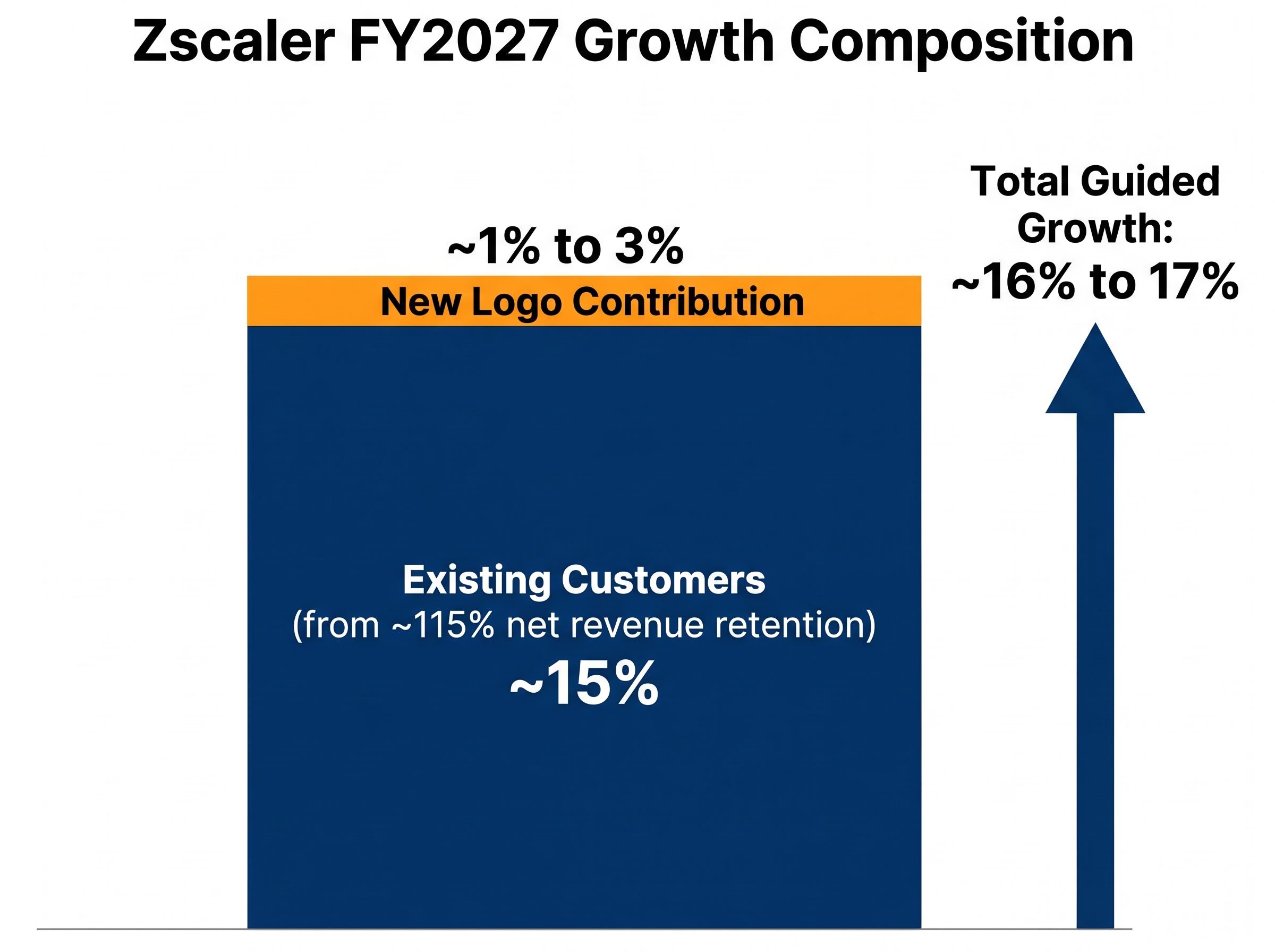

Zscaler’s net revenue retention rate of approximately 115% is a genuinely strong metric. It means existing customers are projected to increase their spending by roughly 15% per year, with no new client additions required to hit that figure. For a platform with deep enterprise integrations, that level of retention reflects real switching costs and product stickiness.

The problem is arithmetic, not narrative.

What net revenue retention actually tells you

Walk through the implied contribution of new logos to total growth:

- Net revenue retention of approximately 115% implies the existing customer base, on its own, contributes roughly 15% annual ARR growth.

- Total ARR growth guidance for FY2027 is approximately 16% to 17%.

- The residual new logo contribution is therefore approximately 1% to 3%, the gap between what expansion revenue delivers and what the total guided growth rate promises.

A 1% to 3% new logo contribution is not a temporary soft patch. Management explicitly acknowledged new customer acquisition as a persistent challenge and built deliberately cautious new customer assumptions into FY2027 guidance. The existing base is holding; the pipeline of new enterprise accounts is not.

A business that grows almost entirely from its installed customer base is durable until the day retention declines. When the new logo engine is barely contributing, any downward pressure on expansion revenue, whether from budget consolidation, competitive displacement, or macroeconomic tightening, lands directly on the top-line growth rate with no new customer cushion to absorb it.

Rule of 40 scoring provides a parallel lens on the same deceleration: combining ARR growth of approximately 16%-17% with normalised free cash flow margins places Zscaler near but not clearly above the 40-point threshold, a range where the market has historically applied a meaningful valuation discount relative to peers above 50.

Zero-based security: how Zscaler’s architecture became its strategic moat (and its ceiling)

To evaluate whether the competitive threats facing Zscaler are cosmetic or structural, a reader needs to understand what the company actually sells and why it won large enterprises in the first place.

Zero-trust network access (ZTNA) and Secure Access Service Edge (SASE) represent a shift in how companies protect their networks. Traditional security models assumed that anyone inside the corporate network perimeter, behind the firewall, could be trusted. ZTNA inverts that assumption. Every user, device, and connection is verified individually before access is granted, with traffic routed through a cloud-based proxy that checks identity and context in real time.

Zscaler built a pure-cloud SASE and ZTNA platform before incumbents like Cisco and Palo Alto Networks had credible cloud-native alternatives. That first-mover position allowed the company to win large enterprise contracts rapidly, particularly among organisations with distributed workforces and complex access requirements.

The current tension is straightforward. Enterprise buyers are increasingly consolidating their security vendors for both budget and operational efficiency. That trend favours broad-platform players over focused point solutions.

| Attribute | Pure-Play ZTNA (Zscaler) | Consolidated Platform (Palo Alto) |

|---|---|---|

| Product breadth | Focused on SASE/ZTNA | Broad security portfolio including SASE |

| Buyer preference trend | Under pressure from consolidation | Benefiting from consolidation demand |

| Switching cost | High (deep integration) | High (platform lock-in) |

| Pricing leverage | Weakening as alternatives mature | Strengthening with bundle economics |

The architecture that gave Zscaler its early advantage, a purpose-built cloud proxy with no legacy hardware dependencies, is now also its constraint. Enterprises that once valued specialisation are increasingly asking whether a single vendor can deliver ZTNA alongside endpoint, firewall, and cloud security in one contract.

Competitive Headwinds: Palo Alto and Netskope Apply Pressure

The competitive threat to Zscaler is not a single assault. It is a pincer movement, with each flank exploiting a distinct weakness in the company’s go-to-market coverage.

From above: Palo Alto Networks. The original source analysis reported Palo Alto’s comparable SASE solution generating approximately $1.5 billion in revenue at roughly 40% growth, outpacing Zscaler’s equivalent rate. Broader disclosure from Palo Alto’s fiscal Q3 2025 earnings (reported 20 May 2025) showed Next-Generation Security ARR reaching $5.1 billion, up 34% year-over-year, though SASE is not broken out as a standalone line item within that figure. The competitive framing is consistent: Palo Alto’s broader platform is increasingly favoured by enterprises consolidating vendors, drawing top-of-market deals away from focused ZTNA providers.

The Palo Alto fiscal Q3 2025 earnings release confirmed Next-Generation Security ARR reached $5.1 billion, up 34% year-over-year, providing the primary disclosure from which analysts have drawn comparisons to Zscaler’s decelerating growth trajectory.

Palo Alto’s SASE-equivalent business was reported at approximately 40% growth, a pace that directly outstrips Zscaler’s decelerating ARR trajectory.

From below: Netskope. Zscaler management acknowledged limited sales coverage in the mid-market segment, characterised as companies with approximately 2,000 to 10,000 users. This is precisely where Netskope competes, and it has reportedly achieved growth rates exceeding Zscaler’s in that tier, though specific quantitative metrics for Netskope are not publicly confirmed.

The two-front pressure connects directly to the new logo weakness documented above:

- Upper market: Consolidation-driven losses to Palo Alto, which offers a broader bundle at the enterprise tier

- Mid-market: Coverage-gap-driven losses to Netskope, which targets the segment Zscaler has underinvested in

- Structural implication: When top-of-market deals migrate to consolidators and mid-market deals go to focused competitors, new logo acquisition stalls structurally, not cyclically

Recovery, then, is not simply a matter of hiring additional sales representatives. It requires a product strategy response at the top and a go-to-market coverage expansion at the bottom, simultaneously.

Sales leadership exits and the go-to-market confidence question

Two senior sales executives departed Zscaler during the third fiscal quarter. At the time of disclosure, one replacement had been made; recruitment for the second position was described as ongoing.

In isolation, executive departures are routine. In context, they warrant closer examination. When simultaneous senior sales exits occur alongside decelerating growth guidance and acknowledged new logo weakness, the question shifts from “why did they leave?” to “what does the pattern suggest?”

Possible readings include internal disagreement about the achievability of forward targets, reduced confidence in competitive positioning against Palo Alto and Netskope, or misalignment between compensation structures and the growth trajectory the business can realistically deliver. None of these interpretations can be confirmed from available sourcing, and each departure may reflect individual circumstances unrelated to the broader story.

The analytical value lies not in overinterpreting either departure, but in reading them as a third data point alongside two already established signals. Morgan Stanley issued a bearish downgrade of Zscaler that contributed to the extended year-to-date decline of approximately 31% as of 27 April 2026, though the precise rating, revised price target, and exact date of the note are not confirmed in available sourcing.

Three corroborating signals now sit in sequence:

- New logo acquisition contributing only approximately 1% to 3% of growth

- Two-front competitive pressure from Palo Alto (above) and Netskope (below)

- Two senior sales leadership departures during a quarter of guided deceleration

No single signal is definitive. The pattern, however, is harder to dismiss.

What the numbers say about buying at $126 and the acquisition wildcard

At approximately $126 per share and an implied market capitalisation of roughly $20 billion, the post-selloff price invites a straightforward valuation question: is the business now cheap enough to compensate for the risks?

Free cash flow yield at the post-decline price: approximately 4%. This is the anchor metric for a standalone valuation assessment.

A discounted earnings model using 15% annual revenue growth and approximately 20% normalised future margins does not yield a strongly attractive standalone entry point. If those assumptions hold on a per-diluted-share basis, existing shareholders could achieve high single-digit to low-teens annualised returns. That is adequate but not exceptional for a stock carrying the risk profile outlined in the preceding sections.

| Scenario | Assumed growth or exit mechanism | Implied return or premium | Key risk |

|---|---|---|---|

| Standalone base case | ~15% annual revenue growth, ~20% normalised margins | High single-digit to low-teens annualised | Growth decelerates further; margins take longer to reach 20% |

| Acquisition scenario | Strategic takeout (Cisco identified as plausible acquirer) | ~20% to 30% premium above current prices | No confirmed approach; timing entirely speculative |

The acquisition scenario deserves consideration as optionality rather than thesis. Jay Chaudhry, Zscaler’s founder and CEO, has a documented record of four prior company exits. Cisco, which previously acquired Splunk, has been identified as a plausible strategic acquirer. A 20% to 30% premium above current prices is considered plausible in a takeout scenario. However, no confirmed M&A approach or strategic review has been reported by any major financial outlet. Over a five-year horizon, the stock has declined approximately 35%.

The honest read: standalone valuation math produces adequate, not compelling, returns under base-case assumptions. The acquisition scenario adds genuine optionality but carries no verifiable probability.

For investors wanting to place the Zscaler acquisition scenario in a wider market context, our full explainer on AI-driven software M&A examines the $1.2 trillion in legacy tech acquisitions recorded in early 2026, the motivations driving large-cap acquirers like Cisco, and which platform categories are attracting the highest strategic premiums.

This article is for informational purposes only and should not be considered financial advice. Investors should conduct their own research and consult with financial professionals before making investment decisions. Financial projections referenced above are subject to market conditions and various risk factors. Past performance does not guarantee future results.

A structurally sound business at a crossroads, not a broken one

The bull case compresses into a single paragraph. Zscaler operates a $3.5 billion ARR business with 115% net revenue retention, a cloud-native architecture that carries genuine switching costs, and a founder-CEO with a documented history of building and exiting companies. The business has not stopped compounding. It has slowed.

The bear case is equally direct. New logo acquisition is structurally weak, contributing an estimated 1% to 3% of growth. Two-front competitive pressure from Palo Alto and Netskope is not a quarter-specific phenomenon. Sales leadership is in transition. FY2027 guidance of approximately 16% to 17% ARR growth implies the deceleration has not bottomed.

Which narrative wins will be determined by a short list of forward signals:

Bull case signals:

- Quarterly new logo additions stabilise or reaccelerate

- Mid-market coverage expansion produces measurable pipeline growth

- ARR growth guidance for subsequent quarters stabilises above 16%

Bear case signals:

- Palo Alto SASE revenue trajectory continues to outpace Zscaler’s ARR growth

- Net revenue retention compresses below 115%, removing the expansion cushion

- Second sales leadership vacancy remains unfilled through the next earnings cycle

The selloff is not irrational. Neither is the case for monitoring the stock. The variables above are what separate a value opportunity from a deteriorating franchise, and they will become visible quarter by quarter, not in a single headline.

—