Morningstar vs Markets: a 125-Point Gap in the US Rate Outlook

1 hr ago

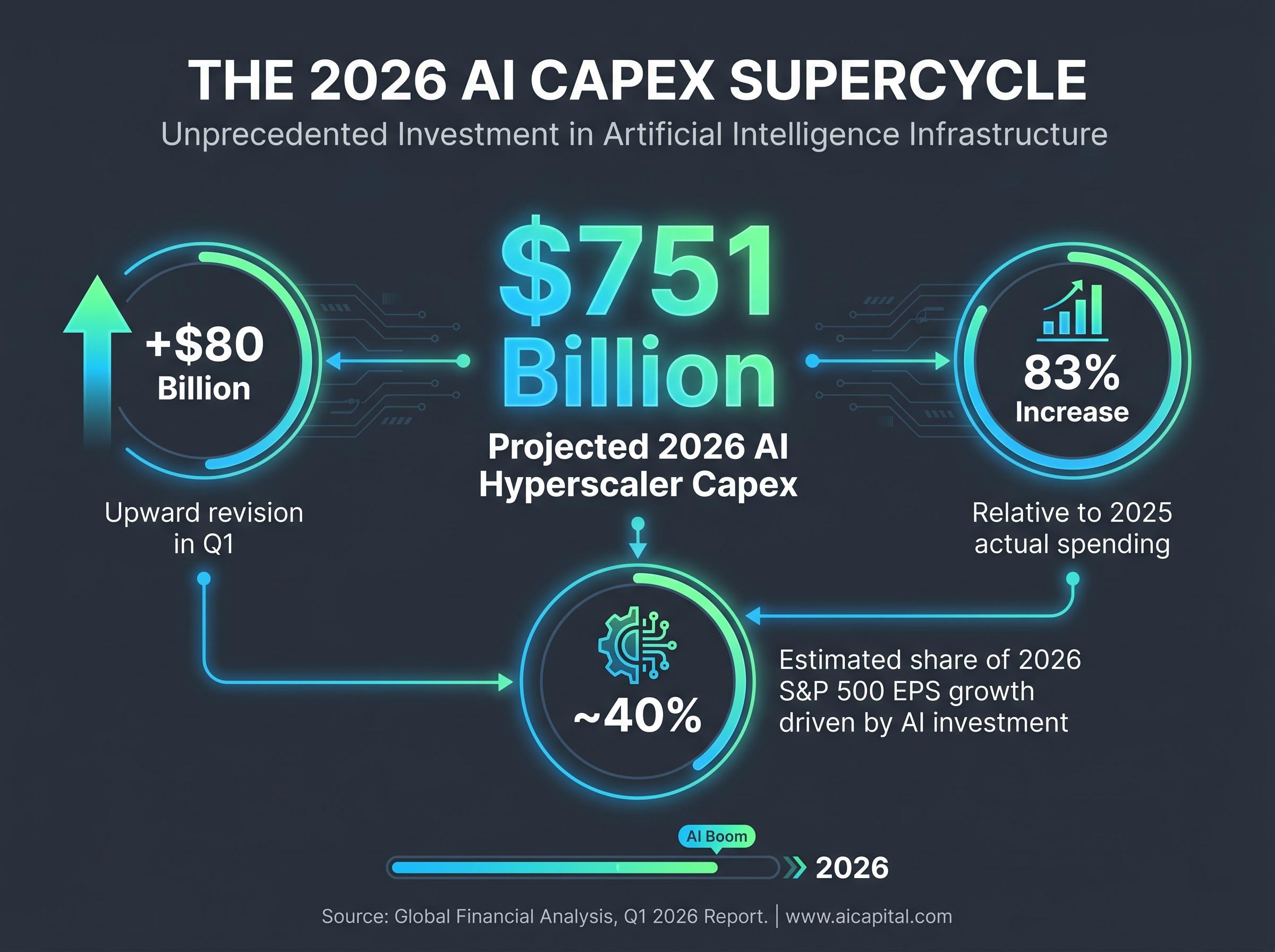

With 63% of S&P 500 companies having reported first-quarter 2026 results, Goldman Sachs analyst Ben Snider identified something that had not occurred in 25 years outside the COVID reopening period: this few companies missing earnings estimates. The observation lands against a backdrop where four mega-cap technology firms posted combined revenue growth of 20% and profit growth of 61%, while a single quarter produced an $80 billion upward revision to 2026 AI hyperscaler capital expenditure projections. The story of US corporate earnings this season is not simply that companies beat expectations. It is where the beating is concentrated and what is driving it.

What follows covers Goldman Sachs’s same-day analysis of Q1 2026 earnings, the individual hyperscaler results powering the index, what the $751 billion AI capex figure means for forward earnings estimates, and where institutional caution flags are being raised.

Four companies are responsible for an outsized share of the S&P 500’s earnings momentum this quarter. Amazon, Alphabet, Meta, and Microsoft collectively delivered 20% revenue growth and 61% profit growth in Q1 2026, according to Goldman Sachs, making them the season’s standout segment by a wide margin.

The individual results fill in the picture.

| Company | Q1 2026 Revenue | YoY Revenue Growth | EPS Beat Margin | Key AI Driver |

|---|---|---|---|---|

| Amazon | $181.5B | +17% | 70.6% | AWS (+28%) |

| Alphabet | $109.9B | +22% | 93.6% | Google Cloud growth |

| Meta | $56.3B | +33% | Beat estimates | AI-driven ad targeting |

| Microsoft | $82.89B | +18% | ~12% | Azure (+40%) |

Alphabet’s 93.6% EPS beat was the widest of the group. Amazon’s 70.6% beat came alongside AWS revenue acceleration that exceeded Wall Street’s most optimistic estimates. Meta posted the fastest top-line growth at 33%, while Microsoft’s Azure segment grew 40%, reinforcing its position as the largest enterprise AI cloud platform.

Goldman Sachs’s Snider noted that investor scrutiny has shifted toward revenue growth as the primary indicator of whether AI investments are generating measurable returns. Earnings-per-share beats confirm profitability; revenue beats confirm demand.

All four companies provided forward guidance reinforcing continued AI capital expenditure, extending the investment thesis beyond a single-quarter result. The signal from management commentary was uniform: spending is not decelerating.

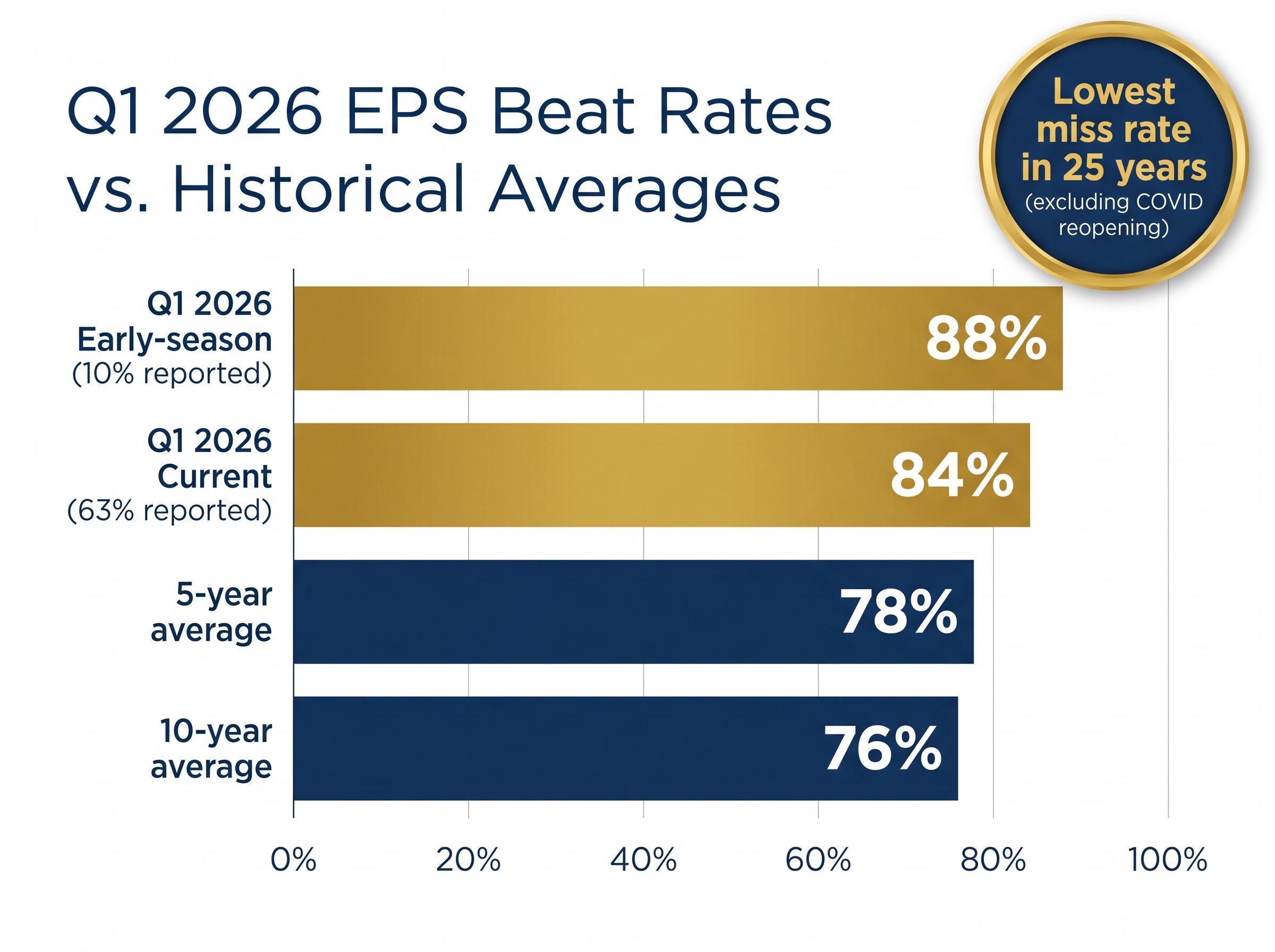

The headline achievement is striking. As of 4 May 2026, with 63% of S&P 500 constituents having reported, the proportion of companies missing EPS estimates hit a 25-year low, excluding the COVID reopening quarter, according to Goldman Sachs’s Snider.

Goldman Sachs analyst Ben Snider flagged that Q1 2026 produced the lowest EPS miss rate in 25 years, outside the pandemic reopening period, with 63% of S&P 500 companies having reported.

Underlying that headline sits a caveat worth absorbing. Aggregate EPS growth came in at 25%, but Goldman Sachs cautioned that figure is inflated by non-recurring items. Stripping those out, underlying EPS growth was 16%, a strong number but materially different from the headline. This represents the sixth consecutive quarter of double-digit year-on-year earnings growth.

Current-season beat rates in context:

The reward for beating estimates has been atypically modest this season. Companies delivering positive surprises saw smaller stock price reactions than historical norms, a signal that strong results were already priced in by institutional investors before reporting began.

Options market pricing ahead of results had already signalled the magnitude of the potential move: derivatives positioned for 5%-7% post-earnings price swings across Alphabet, Amazon, Meta, and Microsoft collectively, creating a $750 billion potential valuation shift that explained why institutional positioning was unusually concentrated before a single report had been filed.

The number at the centre of Goldman Sachs’s forward analysis is $751 billion: the firm’s projected 2026 AI hyperscaler capital expenditure figure, attributed to analyst Ben Snider. Three data points frame the scale:

That $80 billion single-quarter revision is the figure that matters most for forward earnings models. It signals acceleration beyond even recent consensus assumptions.

Goldman Sachs’s analysis indicates that risks to the firm’s S&P 500 EPS estimates are skewed to the upside, driven by the AI capex spending surge and its flow-through effects across the earnings base.

The earnings transmission mechanism is direct. When hyperscalers commit capital to AI infrastructure, that spending flows as revenue to the companies building and supplying the infrastructure: semiconductor manufacturers, data centre operators, power infrastructure providers, and enterprise software vendors. Positive EPS revisions follow across that supply chain. Goldman Sachs estimates AI investment could drive approximately 40% of S&P 500 EPS growth in 2026, a figure that gives the capex cycle broad index-level significance.

Broader Wall Street estimates reinforce the direction. JPMorgan, Morgan Stanley, and other firms project combined big-four hyperscaler capex exceeding $700 billion, with Goldman Sachs’s own firm-level estimate at $667 billion before the analyst-level $751 billion figure from this earnings-season analysis.

The AI capex trajectory toward 2027 extends the cycle well beyond the current earnings season: analyst projections see combined hyperscaler spending crossing $1 trillion annually, sustained in part by $121 billion in hyperscaler debt issuance in 2025 and an estimated $100 billion more projected for 2026, raising structural questions about debt-funded infrastructure sustainability alongside the revenue acceleration story.

AI hyperscaler capex refers to the capital spending by cloud platform operators, specifically Amazon (AWS), Alphabet (Google Cloud), Meta, and Microsoft (Azure), on the physical and digital infrastructure required to run AI workloads. This includes data centre construction, chip procurement (GPUs and custom silicon), networking equipment, and energy capacity.

The mechanism through which this spending produces earnings growth across the broader market follows a straightforward sequence:

Goldman Sachs estimates this transmission mechanism could account for approximately 40% of S&P 500 EPS growth in 2026. Forward guidance from all four hyperscalers confirmed no deceleration in planned spending, and some analyst projections see combined hyperscaler capex exceeding $1 trillion by 2027.

A portion of the hedge fund and analyst community remains cautious about AI capex monetisation timelines. Some institutional investors have rotated away from pure-play AI names on the basis that spending commitments are outpacing measurable revenue returns.

The Q1 2026 results across all four hyperscalers are the first concrete evidence that the investment cycle is producing measurable top-line return. Whether that trajectory holds remains an open question rather than an answered one.

The broader Q1 2026 earnings season tells a more nuanced story than the mega-cap technology headline suggests.

Goldman Sachs’s own Q1 2026 results illustrated the mixed picture within financials. The firm reported EPS of $17.55 (beating estimates) on revenue of $17.23 billion (also a beat), yet the stock fell approximately 4% on weakness in FICC trading and rising expenses.

Goldman Sachs flagged that analyst margin forecasts across most sectors have been revised downward due to commodity input cost pressure, providing a counterweight to the technology outperformance narrative.

Elevated energy prices, US-Iran tensions, and Eurozone inflation running at approximately 3.3% remain active macro headwinds. The Q2 2026 outlook projects continued double-digit earnings growth with sector participation broadening into financials and industrials, but commodity cost pressure on margins is the risk that diversified S&P 500 investors should weigh against the AI tailwind.

The earnings data is constructive. The positioning data warrants attention.

Goldman Sachs’s U.S. Equity Sentiment Indicator registered a reading of 1.7 as of 4 May 2026, a level the firm historically associates with below-average market returns over the subsequent two-to-eight-week horizon.

The context for that elevated reading is the S&P 500’s approximately 14.87% rally from late March through early May 2026, one of the sharpest short-term advances since April 2020. Goldman Sachs maintains a year-end S&P 500 target of 7,600, implying approximately 6% upside from late-April levels.

The tension Goldman Sachs’s analysis presents is worth naming directly: genuine earnings strength, an AI capex tailwind accelerating faster than consensus, and a near-term sentiment positioning risk are all simultaneously true. Hedge funds have increased exposure to non-technology sectors amid AI monetisation timeline uncertainty, suggesting institutional capital is already recalibrating even as headline earnings remain strong.

For investors with shorter time horizons, the sentiment indicator is the most actionable signal. It does not contradict the earnings story; it contextualises it. The market has moved substantially to price in strong results, reducing the near-term return potential even as the fundamental picture remains constructive.

Investors who want to cross-reference Goldman Sachs’s elevated sentiment reading against a second institutional framework will find our dedicated guide to the BofA Sell Side Indicator covers the 55.6% April reading in detail, including the 1.9-percentage-point gap from a historic sell signal, the narrow market breadth context, and what contrarian frameworks historically imply for 12-month forward returns from this level.

Q1 2026 produced a record-low miss rate, mega-cap technology dominance, an $80 billion upward AI capex revision, and a Goldman Sachs sentiment reading that counsels near-term caution. These signals do not all point in the same direction, and that tension is itself the message.

The forward picture holds both tailwinds and headwinds. Q2 2026 consensus projects continued double-digit earnings growth with broadening sector participation. Commodity cost pressure and geopolitical uncertainty remain live risks to margin assumptions across non-technology sectors.

The most durable signal from Goldman Sachs’s analysis is structural: the AI capex supercycle, now at $751 billion projected for 2026, is generating measurable revenue returns at the hyperscaler level. That is the first concrete evidence that the investment cycle is translating into earnings, not just spending. Whether the broader market has already priced that evidence is the question that separates the near-term outlook from the longer-duration thesis.

Investors wanting to map the specific risks and opportunities across the remainder of 2026 will find our full explainer on Q1 2026 earnings season implications covers the capital rotation into small-caps and value, the forward P/E compression risk at approximately 19.8x, and the ISM Prices Paid signal that could force the Federal Reserve to delay easing.

This article is for informational purposes only and should not be considered financial advice. Investors should conduct their own research and consult with financial professionals before making investment decisions. Past performance does not guarantee future results, and financial projections are subject to market conditions and various risk factors.

The AI capex supercycle refers to the surge in capital spending by hyperscalers like Amazon, Alphabet, Meta, and Microsoft on AI infrastructure including data centres, chips, and energy systems. Goldman Sachs estimates this spending could drive approximately 40% of S&P 500 EPS growth in 2026, making it a key driver of broader US corporate earnings beyond just the technology sector.

Amazon, Alphabet, Meta, and Microsoft collectively delivered 20% revenue growth and 61% profit growth in Q1 2026, with individual highlights including Alphabet's 93.6% EPS beat, Meta's 33% top-line growth, AWS growing 28%, and Azure expanding 40%.

Goldman Sachs's U.S. Equity Sentiment Indicator registered 1.7 as of 4 May 2026, a level the firm historically associates with below-average market returns over the subsequent two-to-eight-week horizon, suggesting near-term caution even as the fundamental earnings picture remains constructive.

With 63% of S&P 500 companies having reported, 84% beat EPS estimates, well above the five-year average of 78% and the ten-year average of 76%, representing the lowest miss rate in 25 years outside the COVID reopening period according to Goldman Sachs analyst Ben Snider.

Goldman Sachs projects total 2026 AI hyperscaler capital expenditure at $751 billion, an $80 billion upward revision made during the Q1 2026 earnings season alone, representing an 83% increase relative to 2025 actual spending levels.