From a sub-$1 stock in FY20 to a compounding total return that independent data places above 500% over five years, Southern Cross Electrical Engineering (ASX: SXE) has produced one of the most consequential growth stories on the ASX in the past half-decade. Company disclosures cite a figure approaching 680%, though the precise number depends on the measurement window and methodology used.

The June 2026 capital raise and contract announcement cycle brought SXE to wider attention, but the single-day headlines obscure a more interesting question: what operational and strategic decisions actually produced this outcome, and are those conditions still intact? This analysis unpacks the business engine behind SXE’s compounding performance, examining the revenue and earnings trajectory, the manufacturing capability, the contract pipeline, the balance sheet construction, and the conditions required to reach management’s $100 million EBITDA target in FY27. The aim is to provide a framework for assessing whether SXE’s structural advantages are durable, not just a read on last week’s price move.

The financial record that makes SXE worth examining closely

Start with two numbers. Revenue has grown at a compound annual rate of 11.5% since FY20. Net profit has compounded at 19.5% over the same period. When earnings grow faster than revenue for five consecutive years, the signal is operating leverage: a business extracting more profit from each incremental dollar of work won.

The acceleration is recent and ongoing. Revenue rose from approximately $464.7 million in FY23 to $551.9 million in FY24 and then to $801.5 million in FY25. Net profit after tax followed: approximately $20.1 million, $21.9 million, and $31.7 million across the same three years. Return on equity improved from approximately 11% to approximately 15.5% over that span, reflecting a business generating progressively higher returns on its capital base.

The earnings led the share price, and the operational choices led the earnings. That sequence, not the headline return figure, is the analytical starting point for any forward assessment of SXE.

| Metric | FY23 | FY24 | FY25 |

|---|---|---|---|

| Revenue | ~$464.7M | ~$551.9M | ~$801.5M |

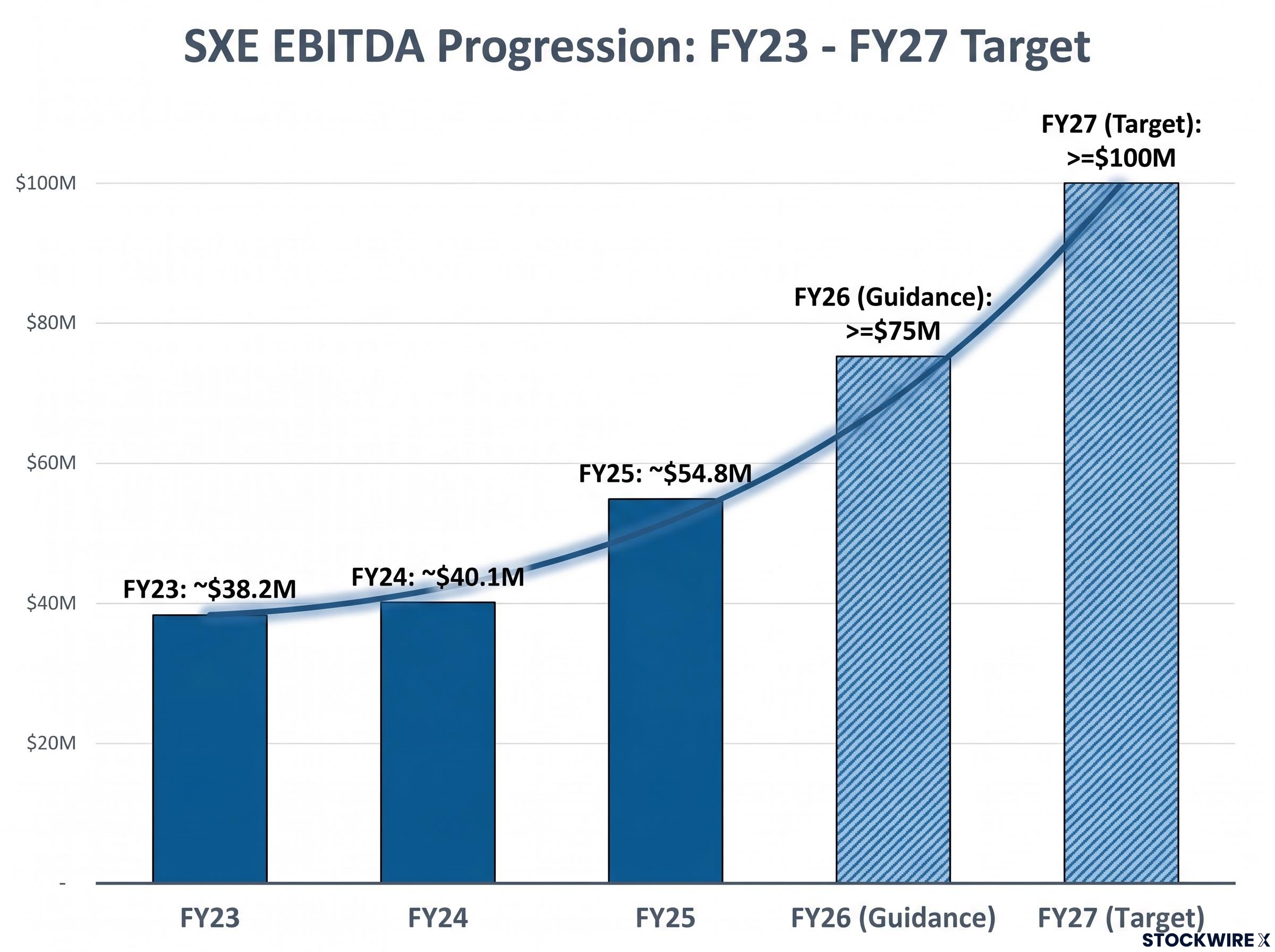

| EBITDA | ~$38.2M | ~$40.1M | ~$54.8M |

| NPAT | ~$20.1M | ~$21.9M | ~$31.7M |

For investors assessing whether SXE warrants further analysis, the financial trajectory confirms the performance is substantiated at the net profit and return-on-equity level, not just at the share price level.

When big ASX news breaks, our subscribers know first

What SXE actually does, and why the structural timing matters

On a project site, SXE looks like a specialist electrical contractor. Teams of electricians and instrumentation technicians install the wiring, control systems, and communications infrastructure that allow large-scale industrial and commercial facilities to operate. The work is technically demanding, heavily regulated, and difficult to replicate at scale because it requires deep bench strength of qualified tradespeople and supervisory capability across geographically dispersed sites.

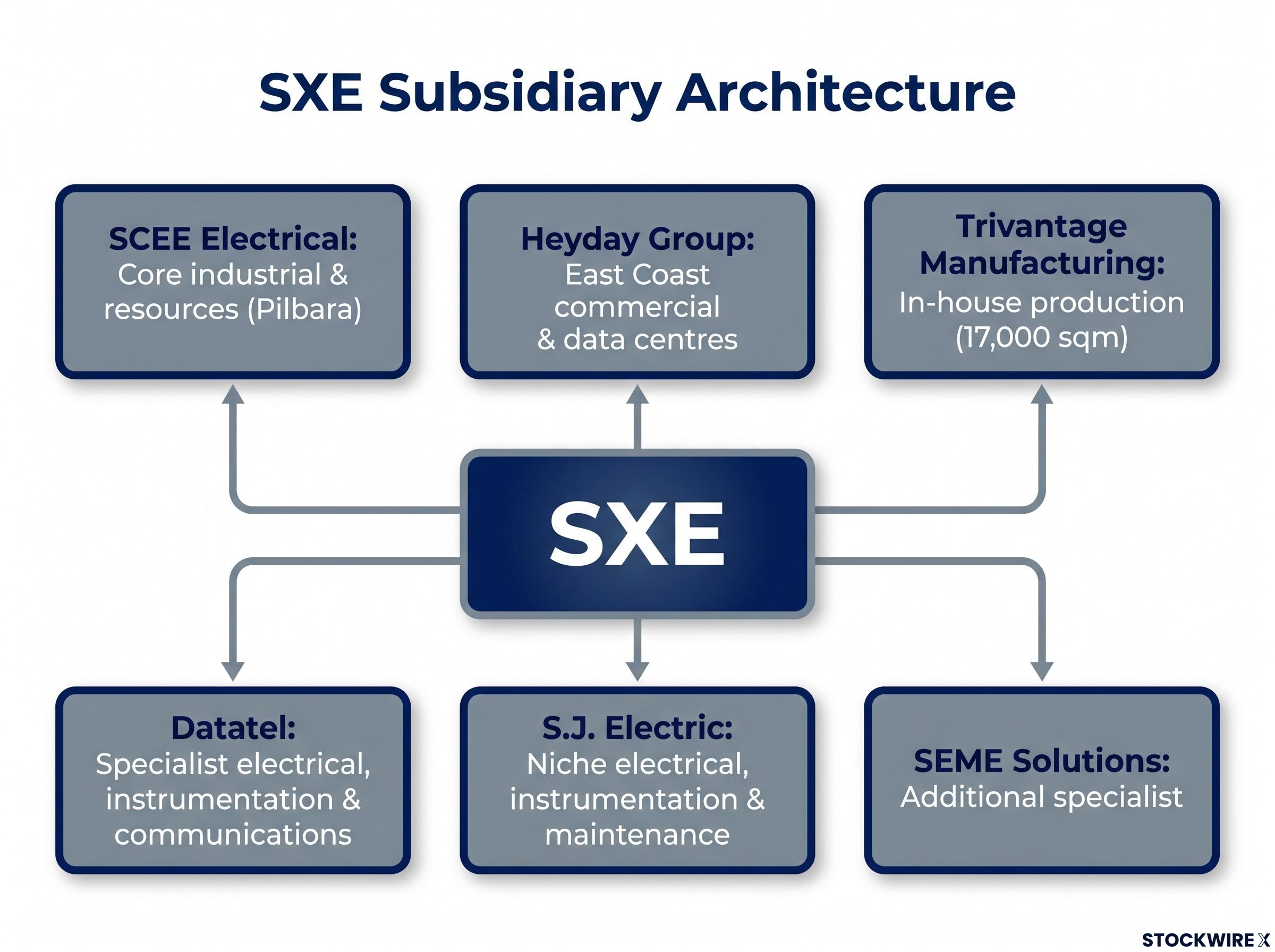

Beneath that project-level work sits a deliberately designed subsidiary architecture:

- SCEE Electrical: core industrial and resources capability, including Pilbara operations

- Heyday Group: East Coast commercial and data centre projects

- Trivantage Manufacturing: in-house production of switchboards and electrical assemblies

- Datatel: specialist electrical, instrumentation, and communications services

- S.J. Electric: niche electrical, instrumentation, and maintenance services

- SEME Solutions: additional specialist segment

This structure gives SXE coverage across four converging demand streams in Australia:

- Hyperscale data centres: cloud infrastructure and AI-related compute build-out, with Australia’s construction cycle earlier and less mature than the US or Europe, implying a longer runway for specialist electrical demand

- Renewable energy generation and grid connections: a decade-plus investment cycle in generation, transmission, and grid-scale storage

- Transmission and distribution network upgrades: structural infrastructure investment across the national electricity network

- Sustained resources capex: including the Pilbara and critical minerals, with the resources sector investing in decarbonisation infrastructure

The end-market diversification functions as a deliberate cyclical hedge. When resources spending pauses, data centre and infrastructure work absorbs the capacity. When commercial construction softens, government-backed infrastructure and resources fill the gap. The diversification is by design, not corporate sprawl.

SXE is not the only ASX electrical infrastructure stocks story attracting attention as Australia’s data centre capacity build-out accelerates; peers including Genus Plus (GNX) and SKS Technologies are competing for a similar pool of contracted work, and the competitive dynamics between these businesses offer useful context for assessing which operators carry the deepest structural moat.

The manufacturing expansion that changed SXE’s competitive position

The contract wins that draw investor attention are often the downstream outcome of a less visible upstream decision. For SXE, that decision was the expansion of Trivantage Manufacturing.

Trivantage produces low-voltage (LV) switchboards, skids, and electrical assemblies, the type of manufactured components that large data centre and resources projects require in volume, on tight timelines, and to exacting specifications. SXE more than doubled its manufacturing floor space to 17,000 square metres, building the capacity to supply these components in-house rather than relying on third-party fabricators with unpredictable lead times.

The strategic logic runs deeper than cost savings. When SXE wins a major project, Trivantage can supply the manufactured product internally, giving the group control over both the installation labour and the physical components being installed. Pure-labour contractors cannot offer this to blue-chip clients who increasingly prioritise delivery certainty over lowest sticker price.

The physical bottlenecks in data centre construction, particularly power availability and switchboard supply chain constraints, are precisely the layer where Trivantage’s in-house LV skid production delivers its competitive advantage, because clients facing long lead times on manufactured electrical components have a direct commercial incentive to consolidate installation and fabrication with a single capable contractor.

Vertical integration gives SXE a competitive position that deepens with each project: manufactured product carries higher margin, is more repeatable, and embeds the company deeper in the client’s supply chain beyond a single construction cycle.

Why manufactured product changes SXE’s margin profile

The economics of manufactured product differ from project labour in three ways. Margins are structurally higher because the product carries embedded IP and production efficiency gains. Revenue is more repeatable because the same skid design can be produced for multiple sites. And the relationship with the end client becomes stickier, because specifying SXE’s manufactured components into a facility design creates switching costs for subsequent phases of work.

This manufacturing capability is the less obvious factor behind the margin expansion implied by earnings growing faster than revenue.

Three contract wins that make the strategy visible across all fronts simultaneously

On 15-16 June 2026, SXE announced three contracts totalling more than $150 million in new work. The point is not just the dollar figure. Each contract confirms a different strategic vector, and the fact that all three activated in a single announcement cycle is analytically distinct from a typical contract update.

| Entity | Client / Project | Scope Summary | Strategic Significance |

|---|---|---|---|

| Heyday Group | NextDC S4 (via Multiplex) | Early-stage electrical and communications works at major East Coast data centre | Confirms East Coast data centre capability with a tier-one operator |

| Trivantage Manufacturing | Major data centre operator | LV skid supply; completion expected FY27 | Validates manufacturing expansion with high-margin, repeatable product revenue |

| SCEE Electrical | Rio Tinto, Pilbara | Three-year Master Construction Agreement for EIC works across Pilbara iron ore operations; extension options; covers sustaining capital, brownfields expansion, end-of-life replacement | Quality signal: specialist EIC work for a tier-one miner in a technically demanding region |

The Rio Tinto agreement warrants particular attention. A three-year Master Construction Agreement with extension options is a relationship structure, not a transactional contract. Winning specialist electrical, instrumentation, and communications work in the Pilbara for a tier-one miner serves as a credential that reinforces SXE’s position across the broader resources pipeline.

Rio Tinto Pilbara maintenance agreements have become a reliable indicator of an industrial contractor’s standing in the resources sector, with Monadelphous securing a five-year, $300 million deal for similar Pilbara iron ore operations in early 2026, a structural comparison that illustrates how tier-one miners award multi-year relationship contracts rather than transactional work to operators who demonstrate consistent safety and technical performance.

The simultaneous activation of data centre, manufacturing, and resources capabilities in a single cycle is what distinguishes this from a routine order-book update. It is the strategy made visible.

The balance sheet architecture behind a $100 million EBITDA target

The EBITDA progression tells a clear story: approximately $38.2 million in FY23, $40.1 million in FY24, $54.8 million in FY25, guidance of at least $75 million for FY26, and a target of at least $100 million for FY27.

Management has set FY27 EBITDA guidance of at least $100 million, building on a base that has already compounded from $38.2 million in three years.

The step from $54.8 million to $100 million requires the same rate of growth the business has already demonstrated across FY23-FY25. It is not an acceleration; it is a continuation.

Three conditions need to hold for the target to be reached:

- Sustained double-digit revenue growth: recent history (mid-teens growth from $464.7 million to $801.5 million in two years) suggests the business can maintain this pace across cycles

- Stable or modestly improving margins: manufacturing integration, operating leverage on a larger workforce, and a contract mix shift toward larger, longer-duration projects all support this structurally

- Capital and balance sheet support: total bank and bonding facilities of approximately $200 million (including a $50 million revolving credit facility and a $50 million acquisition facility), a net cash position with gearing of approximately negative 39% as of FY25, and a $150 million equity raise announced in June 2026 collectively provide substantial financial headroom

The appointment of a Chief Operating Officer for East Coast operations signals leadership depth being built to match the growth trajectory. The East Coast hosts the bulk of Australia’s data centre pipeline and major infrastructure investment.

The binding constraint on the target is not capital. It is labour. The Australian electrical, instrumentation, and communications sector is structurally short of qualified electricians and instrumentation technicians. SXE’s scale and diversified footprint provide recruiting and retention advantages over smaller peers, but workforce capacity remains the variable most likely to determine how smoothly the earnings trajectory matches the target.

Whether the conditions that built the five-year return are still in place

The structural tailwinds that supported SXE’s growth from FY20 have not weakened. Australia’s data centre construction cycle is arguably more supportive now than when SXE began its growth phase, with the build-out earlier and less mature than in the US or Europe. The decade-plus investment cycle in renewables and transmission continues to accelerate. Resources capex, particularly in the Pilbara and critical minerals, has entered a sustained investment phase in decarbonisation infrastructure.

The five-year return was not a single-cycle windfall. It was the product of five compounding operational decisions:

- Manufacturing build-out through Trivantage, creating a vertically integrated capability

- Subsidiary structure and end-market diversification, hedging against single-cycle exposure

- Balance sheet discipline, maintaining a net cash position while expanding facilities

- End-market selection, positioning the business at the intersection of four secular demand streams

- Leadership depth, including the East Coast COO appointment to match geographic growth

The $150 million equity raise announced in June 2026 represents the most recent evidence of management’s confidence in the forward pipeline.

The questions that matter more than the five-year return figure

The question for investors conducting SXE company analysis is not whether the historical performance is impressive. The question is whether the conditions that produced it remain structurally intact, and whether the $100 million EBITDA pathway is realistic at the assumed growth rate. The financial trajectory, the manufacturing moat, the contract evidence, and the balance sheet architecture examined in this analysis provide the framework for forming that view.

For investors wanting to place SXE’s FY27 guidance in the context of the broader sector re-rating, our deep-dive into the ASX industrials structural rally examines six companies that hit 52-week highs in the week ending 12 June 2026, including a detailed analysis of why SXE’s FY27 EBITDA growth guidance of above 33% diverged from consensus estimates of approximately 9%, a gap that represents either a substantial analyst upgrade catalyst or a demanding execution bar.

What SXE’s five-year compounding tells investors about the next phase

The earnings led the share price, and the operational choices led the earnings. That causal sequence is the only durable basis for a forward view on SXE. Investors who understand the manufacturing investment, the subsidiary architecture, and the balance sheet construction are better positioned to assess whether the $100 million EBITDA target represents a realistic continuation of demonstrated growth or an aspiration that outpaces the business’s capacity to deliver.

The primary source documents for confirming the specific financial figures referenced throughout this analysis are SXE’s June 2026 ASX announcements, investor presentation, and debt facility disclosure. Investors are encouraged to review these materials directly before forming an investment view.

This article is for informational purposes only and should not be considered financial advice. Investors should conduct their own research and consult with financial professionals before making investment decisions. Financial projections discussed in this analysis are subject to market conditions and various risk factors, and past performance does not guarantee future results.