The Memo That Halved Meta’s AI Infrastructure Cost Estimate

3 hrs ago

Global hyperscalers committed more than US$150 billion in combined capital expenditure during 2024 alone, the vast majority directed at physical infrastructure to power artificial intelligence workloads. Yet for all the attention paid to the software layer, to the models, the chatbots, the autonomous agents, the investment bottleneck sits further down the stack. Data centres are being constrained by power availability, not construction timelines. Energy storage demand is accelerating faster than grid planners anticipated. And in Australia, regulators have formally identified data centres as a structural driver of electricity demand, reshaping grid investment requirements across the eastern seaboard. A cohort of ASX-listed companies sits directly in the path of that capital flow, spanning data centre operators, energy generators, storage providers, and construction contractors. What follows maps the physical bottlenecks shaping AI infrastructure investment, connects them to Australian grid realities, and identifies the listed companies where demand is most likely to translate into durable earnings.

The scale of capital now flowing into AI infrastructure is difficult to overstate. Meta guided 2024 capex to US$35-40 billion, driven by servers and data centres for AI, and confirmed that capital expenditure in 2025 and 2026 is expected to continue rising. Microsoft spent approximately US$14 billion in a single quarter (the March 2024 quarter), with management indicating capex would “grow materially on a sequential basis” through FY2025. Amazon deployed US$48 billion in total capex during 2023, with CFO Brian Olsavsky flagging “meaningful” year-on-year increases for AWS infrastructure. Alphabet stated that 2024 capex would be “notably larger” than 2023’s US$32.3 billion.

Alphabet’s capex signal for 2024, described as “notably larger” than US$32.3 billion, offered no upper bound, reflecting a sector-wide pattern where the commitment is explicit but the ceiling is not.

These are not projections. They are committed corporate budgets, backed by board-level capital allocation decisions at four of the world’s largest companies.

The hyperscaler capex commitments recorded here represent 2023 and 2024 reference points; by Q1 2026, Amazon, Microsoft, Alphabet, and Meta had collectively spent US$130 billion in a single quarter, pushing full-year 2026 combined guidance to approximately US$725 billion and placing the cumulative trajectory well above what most infrastructure planners modelled even twelve months earlier.

The physical world, however, has not kept pace. Grid connection queues stretch years in most developed markets. Data centre capacity in key hubs is fully contracted. In the months preceding May 2026, users of Anthropic’s Claude observed sustained service degradation, attributed to demand exceeding available data centre capacity: a live, consumer-facing signal that the infrastructure gap is not abstract.

| Company | Reference Capex Figure | Year/Period | Forward Signal |

|---|---|---|---|

| Meta | US$35-40bn (guidance) | 2024 | 2025 and 2026 expected to rise further |

| Microsoft | ~US$14bn (single quarter) | Q3 FY2024 | Material sequential growth flagged |

| Amazon | US$48bn (total capex) | 2023 | Meaningful YoY increases for AWS |

| Alphabet | US$32.3bn (reference base) | 2023 | “Notably larger” in 2024 |

Three categories of physical constraint sit between this capital and its deployment: power availability, data centre capacity, and energy storage. Each represents both a bottleneck and an investment opportunity.

For much of 2023, the conversation about AI scaling centred on semiconductor supply. Could TSMC produce enough advanced chips? Would export restrictions constrain access? Those questions remain relevant, but they are no longer the binding constraint. Compute capacity is now limited primarily by energy and grid connection, not chip fabrication.

The mechanism is specific. AI data centres require firm, reliable, high-density power, often 50MW or more per facility, delivered continuously. Existing grid infrastructure in most markets was not designed to deliver that density at that speed. Grid connection approvals alone can take two to four years in major markets, and that timeline assumes the underlying transmission capacity exists.

The energy storage market reflects this pressure. According to the International Energy Agency’s Electricity 2024 report, global battery storage capacity reached approximately 42GW at end-2023, with battery storage investment doubling year-on-year in 2023. BloombergNEF projects total global energy storage capacity (excluding pumped hydro) could grow almost 30-fold from 2022 to 2030. The IEA’s World Energy Investment 2024 report expects battery storage investment to top US$50 billion by 2030.

Hyperscaler grid bypass strategies, where technology companies contract directly with on-site or behind-the-meter generators to circumvent slow-moving grid connection queues, represent one response to the timeline constraint that grid connection approvals create, and companies pursuing this model have demonstrated multi-year revenue growth independent of traditional utility infrastructure.

Three categories of energy infrastructure stand to benefit most directly:

Reports from industry sources indicate that current annual orders for energy storage systems may already exceed total worldwide known installed capacity, though AI-specific storage demand figures are not separately quantified in primary sources.

Intermittent renewable generation creates a structural mismatch with the 24/7 uptime requirements of AI data centres. Solar output drops to zero at night. Wind is variable. For a facility requiring uninterrupted power at 50-100MW, that intermittency is not a planning nuisance; it is a fundamental constraint.

Hyperscalers’ own 24/7 clean energy commitments compound this dynamic. Rather than reducing the need for storage, these commitments accelerate it; meeting a round-the-clock renewable target requires enough battery or pumped hydro capacity to cover every hour that wind and solar cannot.

The infrastructure pressure on Australian grids is not theoretical. Regulatory and planning bodies have formally incorporated data centres as a structural demand driver in their current operative frameworks.

AEMO’s Draft 2026 Integrated System Plan, released in December 2025, treats data centres as a key structural demand driver under the Step Change scenario, with multi-GW contributions projected by the 2030s. The 2024 Electricity Statement of Opportunities explicitly identified data centres and hydrogen as “significant new demand” expected to increase electricity consumption and peak demand in New South Wales and Victoria in particular.

AEMO’s 2024 Electricity Statement of Opportunities quantifies an Accelerated Data Centre Growth sensitivity projecting nearly 10 TWh of additional load by 2033-34, with New South Wales and Victoria absorbing the largest share, providing the regulatory basis for the transmission and storage investment requirements now flowing through the eastern seaboard grid.

Transgrid has stated that “data centres, population growth and electrification are fuelling unprecedented increases in electricity demand in Greater Sydney.”

The Australian Financial Review reported in July 2024 that forecasts suggest data centres could consume up to 20% of NSW power by the 2030s, a projection that, while subject to revision, signals the directional scale of demand.

Four states have documented data centre demand pressure:

A hyperscale or AI-ready data centre is not simply a large building with servers. It requires high-density power, measured in megawatts of IT load, along with advanced cooling systems capable of managing the heat output of dense GPU clusters. It requires fibre-optic network connectivity, physical security meeting government and enterprise standards, and land with planning approval in locations close enough to grid substations to make high-voltage connection feasible.

The development timeline compounds the challenge. Grid connection approvals, environmental assessments, planning permissions, and construction lead times mean that new capacity can take three to five years to come online from the point capital is committed. Power availability, not construction speed, is typically the longest lead-time item.

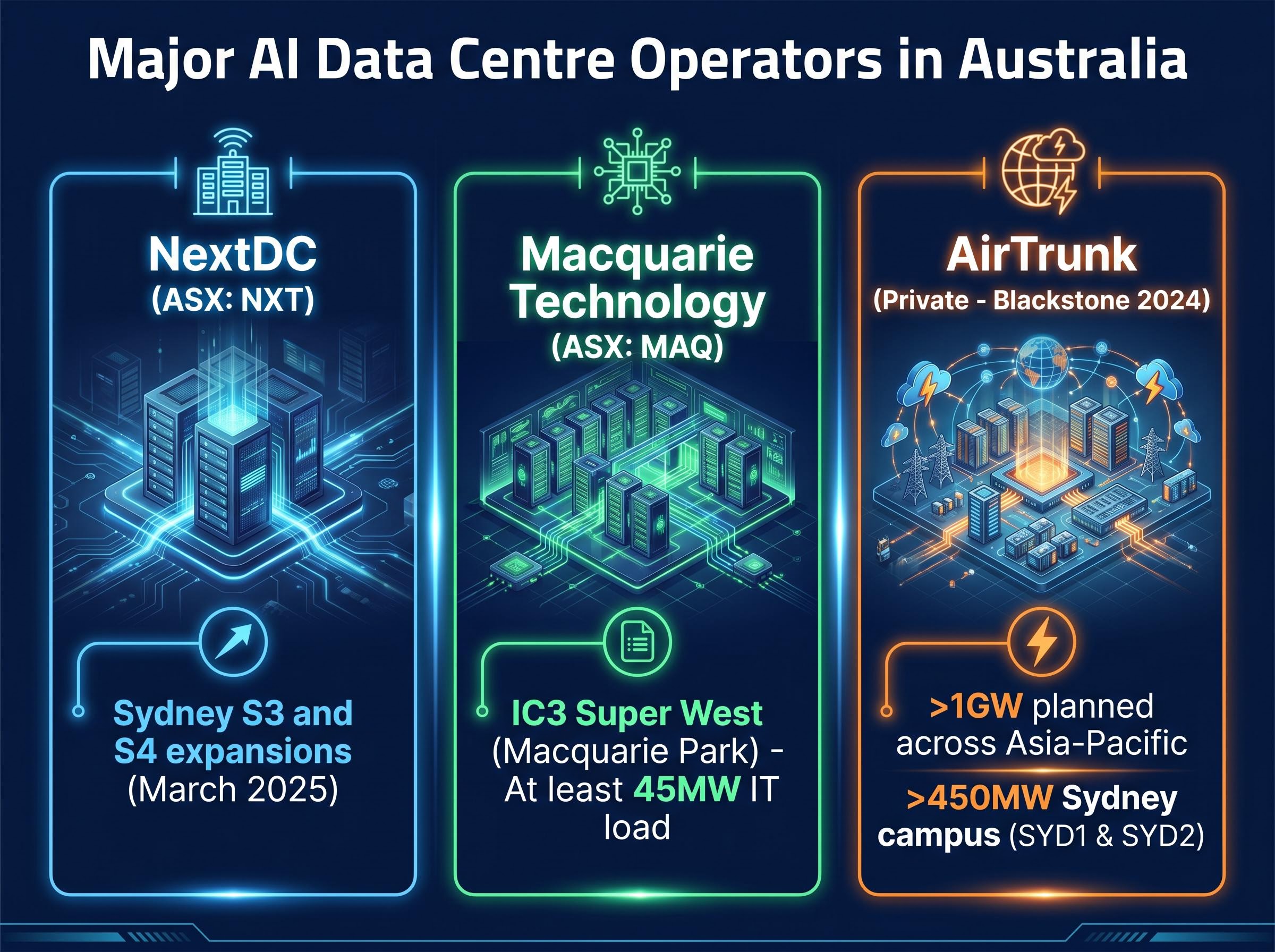

Three operators are most actively expanding AI-capable data centre capacity in Australia:

AirTrunk is not ASX-listed, making NextDC and Macquarie Technology Group the primary direct-equity access points for Australian investors seeking exposure to the physical data centre build-out.

For investors wanting to assess the specific financials behind NextDC’s Western Sydney build, our full explainer on the NextDC S4 expansion covers the 250MW contract, the A$2.2 billion capital raise structure (including A$1.5 billion in equity and A$1.7 billion in hybrid securities anchored by CDPQ), and the FY27 capex forecast of approximately A$5.0 billion that underpins the company’s forward order book projections.

The ASX offers a layered set of exposures to the AI infrastructure theme, organised here by proximity to the core bottlenecks.

Following Altium’s acquisition by Renesas Electronics in 2024 and subsequent delisting, the ASX has limited direct exposure to AI hardware and chip-making. The infrastructure angle represents the most accessible local entry point for the AI investment theme.

| Company (ASX Code) | Sector Role | Primary AI Infrastructure Exposure | Exposure Type |

|---|---|---|---|

| NextDC (NXT) | Data centre operator | Hyperscale and AI workload hosting, contracted capacity | Direct |

| Macquarie Technology (MAQ) | Data centre operator | AI-ready sovereign data centres, high-density racks | Direct |

| AGL Energy (AGL) | Generation and storage | Large-scale battery pipeline, firming capacity for grid | Adjacent |

| Origin Energy (ORG) | Generation and storage | Generation portfolio, battery and pumped hydro plans | Adjacent |

| APA Group (APA) | Gas infrastructure | Gas pipeline and peaker capacity for transitional firming | Adjacent |

| Downer Group (DOW) | Construction and engineering | Data centre and energy infrastructure construction | Adjacent |

| NRW Holdings (NWH) | Construction and engineering | Civil and electrical infrastructure for large projects | Adjacent |

| Lendlease (LLC) | Construction and development | Large-scale construction capability for data centre programmes | Adjacent |

The distinction between direct and adjacent exposure is worth calibrating carefully. NextDC and Macquarie Technology derive revenue directly from contracted data centre capacity. AGL, Origin, and APA benefit from rising energy demand, but that demand is not exclusively AI-driven. The construction names, including Downer, NRW Holdings, and Lendlease, have been identified by J.P. Morgan and local brokers as potential beneficiaries of large-scale data centre construction activity, though their exposure is mixed and not always precisely quantifiable.

The structural thesis is clear. The risks require equal specificity.

Supply chain layer positioning matters more than model-level outcomes for data centre investors: when DeepSeek’s efficiency gains triggered an 11% single-session drop in DigiCo and a 9.4% drop in NextDC in January 2025, the subsequent recovery illustrated that aggregate compute demand, not which model wins, determines revenue for the physical facilities that process all AI workloads.

The AI software boom is generating demand that only physical infrastructure can satisfy. The bottlenecks in power availability, data centre capacity, and energy storage are not temporary friction points; they are the investable expression of a structural mismatch between digital ambition and physical reality.

In Australia, that mismatch is already documented. AEMO, Transgrid, and state-level planning bodies have formally incorporated data centre demand into their operative frameworks. NextDC, Macquarie Technology, AGL, Origin, and a cohort of energy and construction names are positioned along the capital flow, with varying degrees of directness and certainty.

For investors seeking to act on this thesis, near-term information events include AEMO’s final 2026 Integrated System Plan (expected June 2026) and results announcements from NextDC and Macquarie Technology. Independent research on the specific names outlined here, calibrated against the risks in timing, concentration, and demand precision, is the logical next step.

This article is for informational purposes only and should not be considered financial advice. Investors should conduct their own research and consult with financial professionals before making investment decisions. Forward-looking statements regarding infrastructure demand, energy storage growth, and company performance are subject to market conditions and various risk factors. Past performance does not guarantee future results.

AI infrastructure investment refers to capital deployed into the physical assets that power artificial intelligence workloads, including data centres, energy storage, and grid upgrades. For ASX investors, this matters because Australian-listed companies in data centre operations, energy generation, and construction are directly positioned along the capital flow from global hyperscalers spending hundreds of billions annually.

NextDC (NXT) and Macquarie Technology Group (MAQ) are the primary ASX-listed companies with direct exposure, as both derive revenue from contracted data centre capacity and are actively expanding AI-ready facilities in Australia. Adjacent exposures include AGL Energy, Origin Energy, APA Group, Downer Group, NRW Holdings, and Lendlease across energy and construction.

AI data centres require firm, continuous, high-density power of 50MW or more per facility, and grid connection approvals alone can take two to four years in major markets. Construction timelines are a secondary constraint; the underlying transmission capacity and regulatory approval process for grid connections is what limits how quickly new data centre capacity can come online.

AEMO's Draft 2026 Integrated System Plan treats data centres as a key structural demand driver, and the 2024 Electricity Statement of Opportunities formally identified data centres as significant new demand in New South Wales and Victoria. AEMO's Accelerated Data Centre Growth sensitivity projects nearly 10 TWh of additional load by 2033-34, providing the regulatory basis for major transmission and storage investment across the eastern seaboard.

Key risks include narrow concentration in listed names (NextDC and Macquarie Technology carry most direct exposure, meaning valuations may already reflect the theme), timeline and regulatory risk from grid connection and planning approvals stretching years, and uncertainty in demand projections since AEMO does not isolate AI-specific workloads from broader data centre load in its planning documents.