What the Broadcom Drop Reveals About AI Stock Valuations Now

2 hrs ago

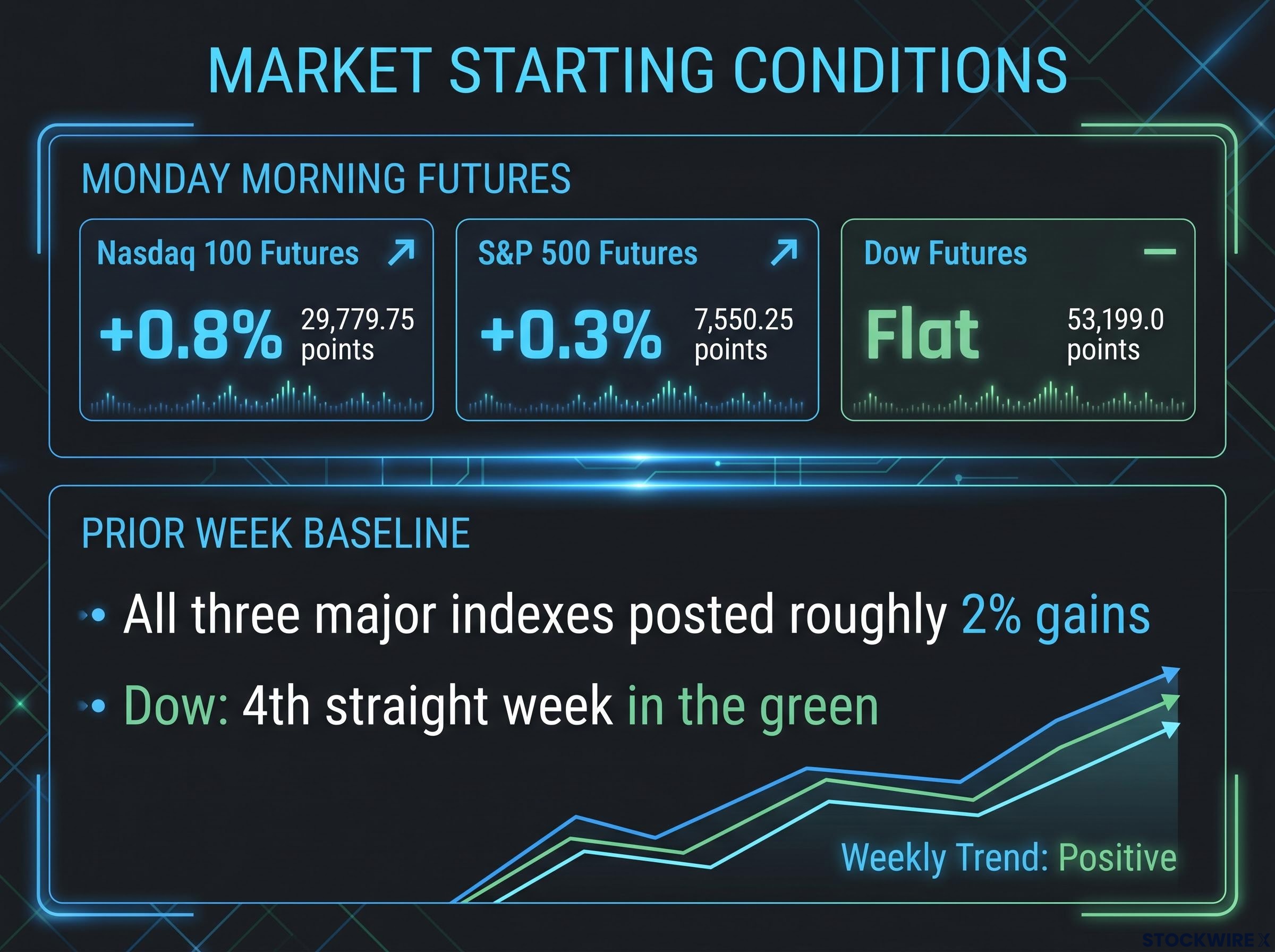

U.S. equity futures are climbing again on Monday morning, but this week the market faces something the prior week did not: hard data that will either validate the rally or expose it.

Three catalysts converge between now and Friday. Wednesday brings the publication of the Fed’s internal deliberations from its June policy meeting. PepsiCo and Delta Air Lines are among the earliest major companies to post Q2 2026 results. And the Dow Jones Industrial Average has strung together four straight weeks of gains, the most recent of which carried it to a record close on lighter-than-usual holiday trading.

The question is whether fundamentals back up what prices are already saying. Here is what actually matters in each of these three catalysts, and how they combine into one coherent risk picture for the stock market this week.

All three major indexes posted roughly 2% gains in a holiday-shortened week. The Dow notched a fresh record close to complete its fourth straight week in the green. The S&P 500 and Nasdaq Composite matched the pace. Monday morning futures reflected the mood:

The optimism is real. So is the arithmetic that comes with it. Markets at record or elevated levels are effectively pre-pricing a benign path for both Fed policy and corporate earnings. That compresses the margin for error.

The asymmetry is straightforward. The upside scenario this week requires both the Fed minutes and early earnings to cooperate simultaneously. A pullback requires only one catalyst to disappoint. Monday’s futures move looks positive on the surface, but a market already pricing in good news needs more than good news to keep advancing. It needs no bad news from either catalyst.

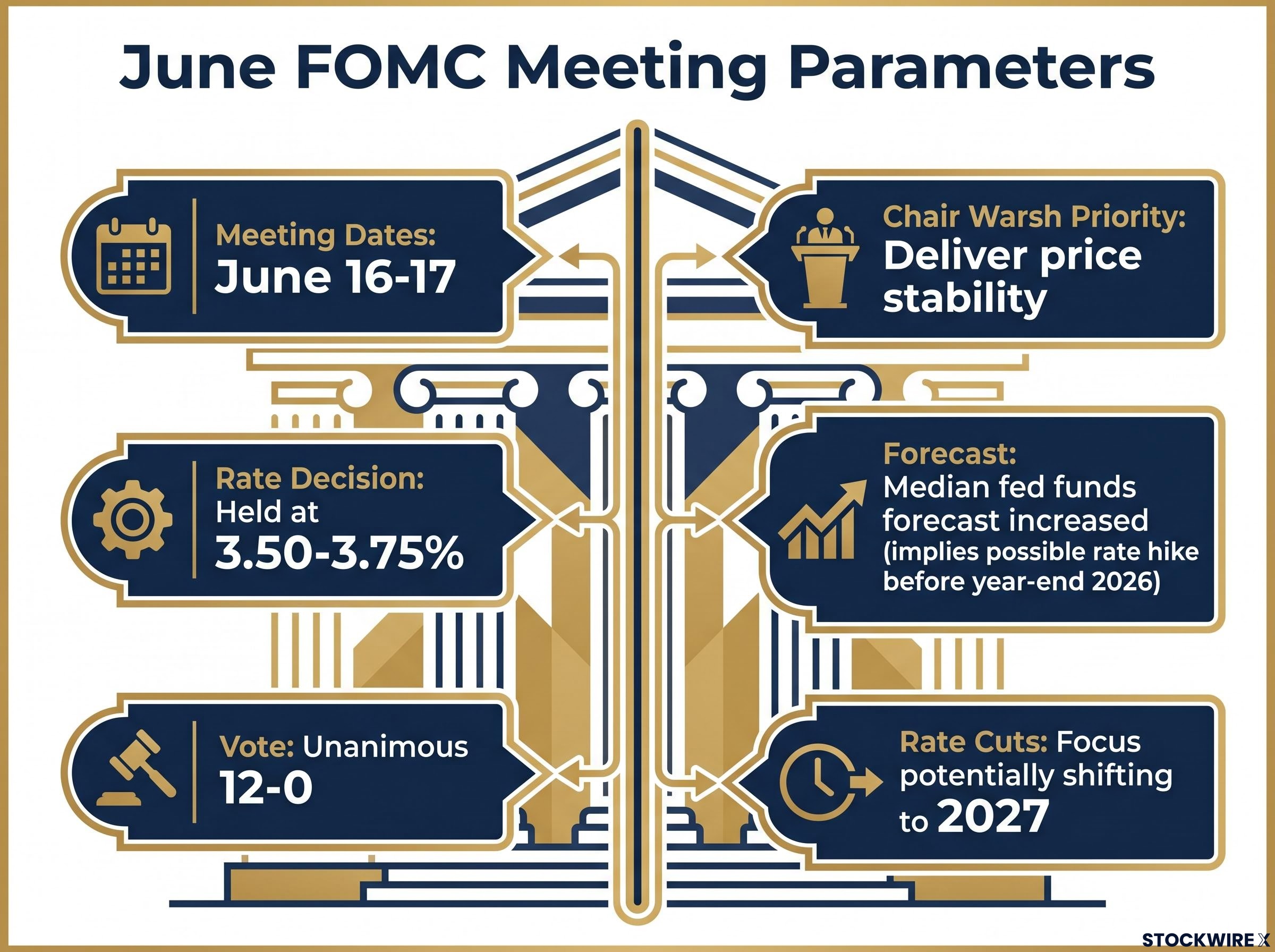

The June 16-17 FOMC meeting ended with rates held at 3.50-3.75% on a unanimous 12-0 vote. But unanimity on the decision does not mean unanimity on the outlook, and the minutes, scheduled for Wednesday, are where the internal debate becomes visible.

What the minutes document actually does is reveal how divided or aligned the committee was on the conditions required for either cuts or further tightening. The rate decision itself was already known. The internal temperature is what moves markets.

Chair Warsh’s commitment to “deliver price stability” was described as unambiguous and unanimous.

That language sets the ceiling. But the June median fed funds forecast increased, implying the possibility of one rate hike before year-end 2026. The April minutes already showed a shift away from an easing bias, with “many participants” preferring to remove language suggesting imminent cuts. The softer-than-forecast June employment figures published the previous week introduce a counterweight: by mid-June the committee may well have been factoring in that labour market cooling when framing its outlook.

The April FOMC dissents, four votes against the majority position and the most at any single Fed meeting since 1992, established the internal fault lines that Wednesday’s June minutes will either deepen or resolve, making the prior release essential context for reading the committee’s current temperature.

Three specific signals investors will scan for on Wednesday:

A unanimous vote to hold is not the same as a unified committee. The debate captured in Wednesday’s release is where the signal sits.

The transmission mechanism is direct. Fed minutes signal the likely path of discount rates, which are the rates used to calculate how much future corporate earnings are worth today. Growth and technology stocks are most sensitive because their earnings are weighted furthest into the future; small changes in the discount rate produce large swings in how those future profits are valued now.

Growth stock valuations are mechanically sensitive to discount rate changes because a larger share of their total expected cash flows sits further in the future, meaning even a modest shift in rate expectations produces an outsized compression in present value that shorter-duration assets do not experience.

The June median fed funds forecast increased, creating a hawkish ceiling on interpretation. The bar for rate cuts has moved higher, with investors potentially looking to 2027 and beyond for clearer normalisation signals. Historical patterns show that minutes releases surprising in either direction can generate meaningful short-term equity moves, particularly in tech and rate-sensitive growth names.

Federal Reserve Bank of New York research on FOMC minutes provides empirical evidence that minutes releases generate measurable moves in Treasury rates, stock prices, and exchange rates, with volatility and trading volume rising sharply in the hours following publication.

The softer June jobs report may act as a moderating factor. If the committee was already incorporating labour market weakness by mid-June, the minutes could read less hawkish than the median rate forecast implies. That distinction matters for sector positioning.

| Minutes Tone | Rate Expectation Signal | Sectors Most Affected | Likely Direction |

|---|---|---|---|

| Dovish | Cuts possible sooner; growth concerns rising | Tech, growth, rate-sensitive equities | Positive; valuations expand |

| Neutral / Split | No clear bias; data-dependent stance | Broad market, sector rotation | Consolidation; rotation not direction |

| Hawkish | Further hike on the table; inflation priority | Tech, growth names pressured; defensives benefit | Negative; capital moves to short-duration assets |

If you hold growth or tech stocks, the Wednesday release is not background noise. It is the single most important pricing event of the week, and understanding which direction the committee leaned in June tells you whether your current sector allocation still makes sense.

Neither PepsiCo nor Delta Air Lines sits among the largest index weights. That is precisely why their early reports carry disproportionate informational value. Together they span consumer staples and discretionary travel, providing a cross-section of consumer behaviour that larger tech heavyweights cannot offer.

The signals to watch are volumes versus pricing. Specifically:

Strong volumes with stable margins would tell you the middle-income consumer remains resilient. Weak volumes or margin compression would raise questions about consumer fatigue that would ripple through the broader staples sector.

Delta’s report offers a different lens on the same consumer. The signals to watch:

At record valuations, markets are not simply looking for headline beats. Forward guidance affirmations or upgrades are what sustain current price levels. A guidance cut from either company in the first week of earnings season would not just move those two stocks. It would signal to the broader market that management teams are less confident about the second half than prices currently imply, and that reappraisal would likely spread.

Forward guidance as the primary market mover is a structural feature of elevated-valuation environments, not just a Q2 2026 dynamic: when the S&P 500 is already priced for strong growth, backward-looking beats have already been discounted, and only the outlook for future quarters moves prices in either direction.

| Scenario | Fed Minutes Tone | Early Earnings Signal | Likely Market Response |

|---|---|---|---|

| Bull | Cautious, data-dependent, limited appetite for hikes | Beats with stable or raised guidance | Rally extends; trend-followers add risk; new highs |

| Base | Split committee, no clear directional bias | In-line results, modest guidance tweaks | Consolidation near current levels; sector rotation |

| Risk | Hawkish, inflation risk elevated, hike possible | Miss or guidance cut from early reporters | Pullback from records; defensives and short-duration benefit |

Broad market breadth in the prior week, with all three indexes gaining roughly 2%, suggests genuine risk appetite improvement rather than narrow speculation. That tilts the base case slightly closer to bullish than bearish.

But the tails are fatter than usual. Chair Warsh has reinforced a strong price-stability commitment. The median rate path for 2026 increased. Indexes are already at or near records. And systematic and momentum strategies tend to add exposure during multi-week rallies, creating potential for amplified moves in either direction.

Crowded equity positioning adds another amplifier to the asymmetric risk profile: Wolfe Research and BofA data from May 2026 both confirmed U.S. equity exposure had reached its most extended levels since late 2021, with concentration in AI and tech names that are precisely the ones most sensitive to a hawkish minutes surprise.

The upside requires both catalysts to cooperate. The downside requires only one to disappoint. At record valuations, that is an asymmetric risk profile.

The scenario framework is not about prediction. It is about knowing in advance what Wednesday’s headline means for your positions so you are not making reactive decisions under pressure.

Three things to monitor this week, in order of timing:

Some things can be known now: the starting conditions, the asymmetric risk profile, and the sectors most exposed to Wednesday’s release. What cannot be known until the data arrives is the committee’s actual tone and whether management confidence matches what prices already imply.

This is not a week to chase last week’s gains. It is a week to stress-test current positioning against the three scenarios above, and to let the data do its work before drawing conclusions.

This article is for informational purposes only and should not be considered financial advice. Investors should conduct their own research and consult with financial professionals before making investment decisions.

Forward-looking statements about Federal Reserve policy direction, earnings outcomes, and market scenarios are speculative and subject to change based on economic data and market developments.

The FOMC minutes are a detailed record of the Federal Reserve's internal policy deliberations, published three weeks after each meeting. They reveal how divided or aligned committee members were on inflation, rate cuts, or further hikes, and because they signal the likely path of discount rates, they directly affect the valuations of growth and tech stocks, which are most sensitive to changes in those rates.

All three major indexes gained roughly 2% in a holiday-shortened week, with the Dow Jones Industrial Average notching a fresh record close to complete its fourth consecutive week of gains. Monday morning futures extended that momentum, with Nasdaq 100 futures advancing 0.8% to 29,779.75 and S&P 500 futures edging 0.3% higher to 7,550.25.

PepsiCo and Delta are early reporters that together span consumer staples and discretionary travel, offering a cross-section of consumer behaviour that large-cap tech stocks cannot. At record valuations, forward guidance from these companies carries more weight than the headline beat: a guidance cut from either would signal that management teams are less confident about the second half than current prices imply, and that reappraisal would likely spread across the broader market.

The three key signals are whether the committee weighted inflation risk more heavily than labour market softness, whether any explicit thresholds for policy changes were discussed, and whether the hawkish tilt visible in the April minutes intensified or softened by June. The June median fed funds forecast already increased, implying a possible rate hike before year-end 2026, so any dovish counterweight from the softer June jobs data would be a meaningful shift.

The bull case requires cautious Fed minutes and earnings beats with stable or raised guidance, which would extend the rally to new highs. The base case sees a split committee and in-line results, producing consolidation and sector rotation near current levels. The risk case combines a hawkish minutes tone with a guidance cut from early reporters, which would trigger a pullback from record levels with defensives and short-duration assets likely to benefit.