What the Broadcom Drop Reveals About AI Stock Valuations Now

2 hrs ago

Bank of America’s semiconductor analyst Vivek Arya has put a $1,550 price target on Micron and is making an explicit argument that the market is applying the wrong framework to value it. The call prices Micron’s stock not as a commodity memory business but as a structural AI infrastructure play, and the gap between that target and where the stock trades is the thesis itself.

The timing matters. Arya’s note, published on 6 July 2026, arrived alongside broad premarket gains across the memory sector, turning a single-stock call into a sector-wide signal. This is not a routine price target nudge. It is a valuation framework built around a re-rating argument: that AI has permanently changed what memory does, what it earns, and what investors should pay for it.

Here is what the thesis actually says, what the valuation maths reveals, and which numbers will settle the debate over the next 12-18 months.

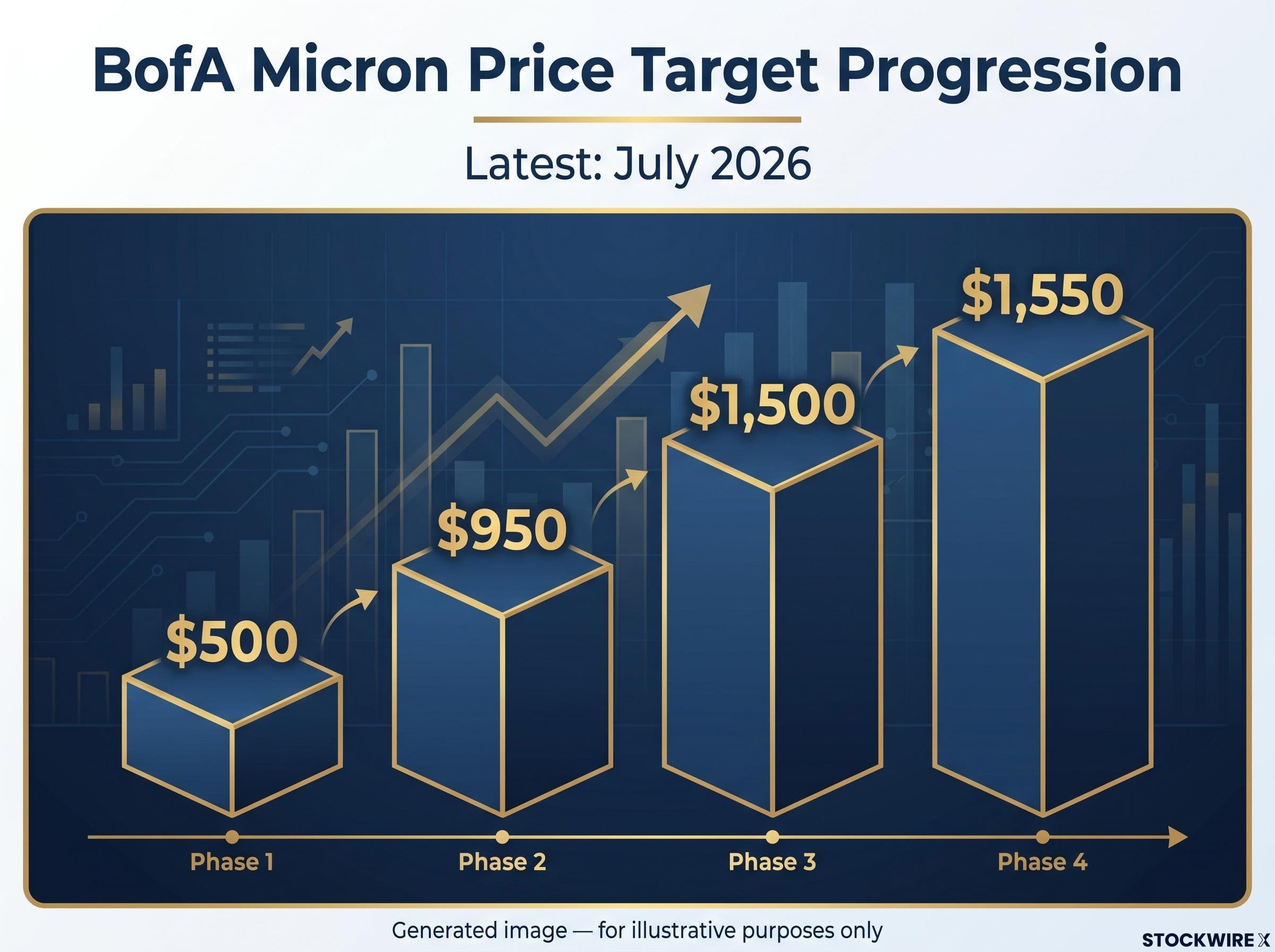

In a July 2026 note, Bank of America’s Vivek Arya maintained his Buy rating on Micron while raising his 12-month price target to $1,550, the latest in a series of upward revisions reflecting growing conviction in the structural role of memory within AI infrastructure.

BofA Rating: Buy, $1,550 price target (Vivek Arya, July 2026 reaffirmation)

The target progression tells its own story: $500, then $950, then $1,500, now $1,550. Each step reflected BofA’s growing conviction that memory’s role in AI infrastructure is structural, not cyclical.

Premarket trading on 6 July 2026 showed the market reading the note as a sector call, not a Micron-specific update:

The fact that Western Digital and Seagate moved alongside Micron tells you the market is treating this as a structural memory sector thesis. That breadth of response is the signal worth noting.

The sector-wide repricing that preceded Arya’s July note was itself driven by converging supply signals: sold-out HBM capacity through 2027, a threatened Samsung labour action, and reduced probability of Chinese memory producers gaining equipment access through US-China trade negotiations.

At the time of Arya’s note, Micron was trading at approximately 10x forward earnings. His $1,550 target implies roughly 11x FY27 earnings based on BofA’s non-GAAP EPS estimate of approximately $140. Even at the bull case target, the implied multiple sits below average.

The compression is not random. It is the market embedding a cyclicality discount into Micron’s price. When investors view earnings as peak-cycle rather than durable, they refuse to apply a sustainable multiple. The earnings number in the denominator looks strong, but the market treats it as temporary, so the price-to-earnings ratio (how much investors pay per dollar of expected profit) stays low. This is the denominator problem at the heart of the disagreement.

| Valuation Metric | BofA Model | Market Pricing | Context |

|---|---|---|---|

| FY27 Non-GAAP EPS | ~$140 | N/A | BofA internal estimate |

| Implied P/E at target | ~11x FY27 | ~10x forward | Both below historical averages |

| AI/HBM segment multiple | ~27x CY27 P/E | Blended lower | Aligned with AI compute peers |

Arya values Micron’s AI/HBM business at approximately 27x CY27 P/E, aligned with the multiples applied to AI compute peers rather than commodity memory names.

Whether that cyclicality discount is justified is the entire question. If earnings prove durable through CY28 as Arya projects, the discount erodes. If they revert, the market was right to apply it.

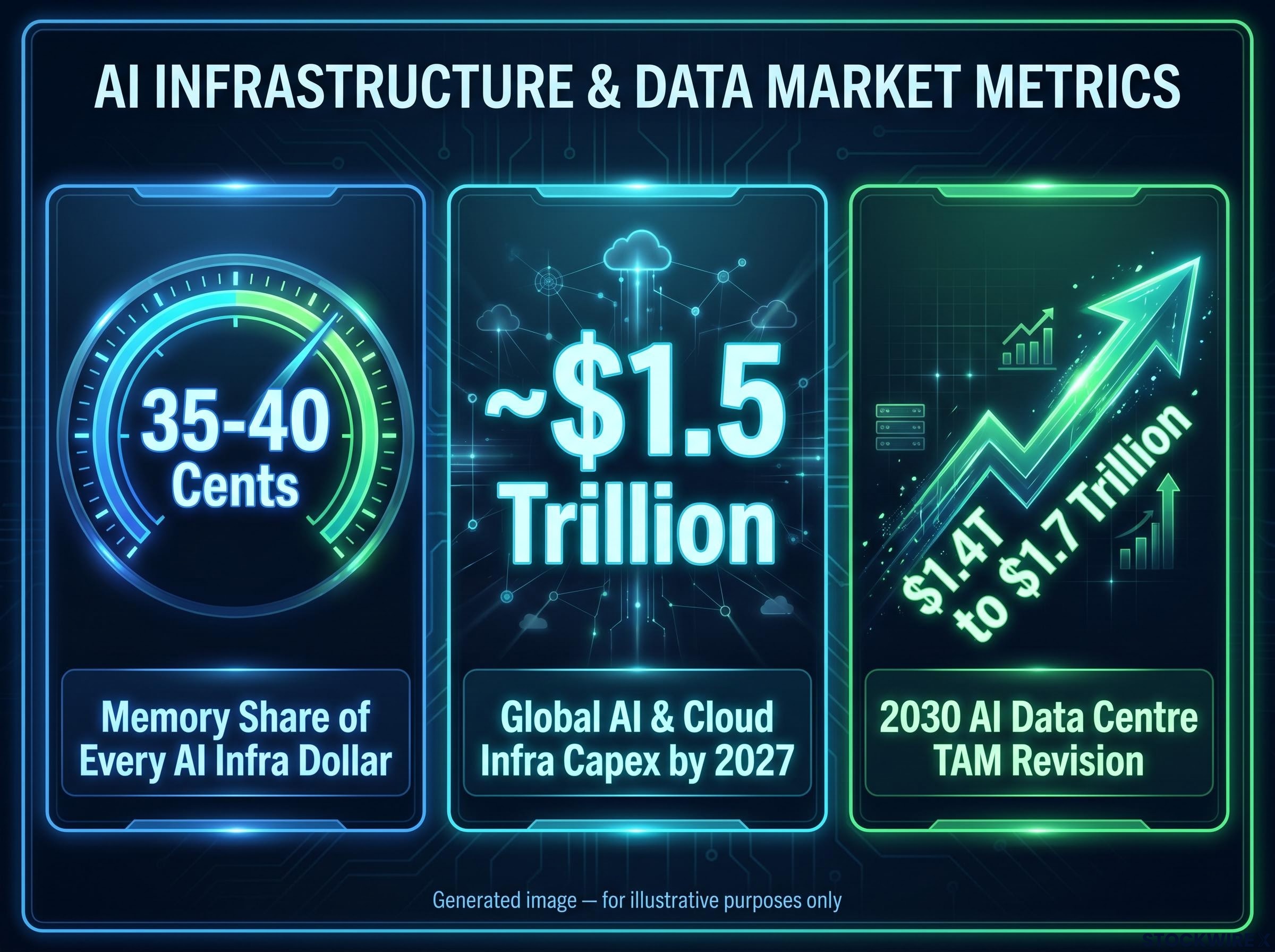

According to Arya’s internal modelling, memory’s contribution to cloud AI capital expenditure has climbed to around 35-40%, a figure he places at roughly two to three times what that share looked like historically. The reason is mechanical: AI training and inference workloads require orders of magnitude more memory bandwidth than traditional compute tasks. Every AI accelerator rack needs more memory, and it needs faster memory.

That demand concentrates on a specific product: HBM, or high-bandwidth memory. HBM is a type of memory stacked vertically and packaged directly alongside AI processors to deliver the data throughput those chips require. It commands a significant price premium over conventional DRAM because the manufacturing process is more complex and the customer base is willing to pay for performance.

The structural differentiators that support the pricing argument:

HBM supply concentration among Samsung, SK Hynix, and Micron has reached the point where the entire sector’s 2026 output was reported as sold out by April, a market structure that supports the pricing premium Arya applies to Micron’s AI segment valuation.

If memory captures that share of AI spending and only three or four manufacturers can supply the premium product, the commodity label starts to look outdated. That is the foundation Arya builds on.

Bringing meaningful new cleanroom capacity online takes 2-3 years. That lead time is the mechanical reason supply cannot flood the market in the near term, even if competitors wanted to ramp aggressively.

Samsung’s capital expenditure discipline adds another constraint. In prior memory cycles, capacity additions came faster and drove oversupply crashes that crushed pricing. This time, the combination of longer lead times, more capital-intensive manufacturing, and deliberate spending restraint is limiting the supply-side response. Arya argues this makes the current cycle structurally different from its predecessors.

Arya’s thesis rests on a sum-of-parts framework that splits Micron into two distinct businesses. The AI/HBM segment receives approximately 27x CY27 P/E, aligned with what the market pays for AI compute peers. The legacy DRAM/NAND business receives a lower, cyclical multiple reflecting its commodity characteristics.

The implication is straightforward: when the market applies a single blended multiple to the combined business, the AI/HBM segment’s premium valuation gets diluted by the commodity segment. The stock trades cheaper than the parts warrant.

| Segment | Valuation Multiple | Key Driver | Earnings Stability |

|---|---|---|---|

| AI/HBM Business | ~27x CY27 P/E | Hyperscaler demand, HBM supply concentration | Projected stable through CY28 |

| Legacy DRAM/NAND | Lower, cyclical basis | Traditional compute, mobile, automotive | Subject to historical cyclicality |

Arya anchors the AI segment premium on three data points:

This framework is Arya’s argument that you are buying an AI company and a legacy memory company in the same stock, and the market is pricing both as if they were the same business.

Arya is explicit about the primary risk in his own note. Elevated memory pricing acts as a tax on data centre capital expenditure. If pricing stays too high for too long, it suppresses demand in price-sensitive end markets.

Arya frames high memory prices as a potential “tax on data centre capex”, a mechanism by which the bull case’s own success could become its headwind.

The risk factors that could unwind the thesis:

The fact that Arya includes the demand destruction risk in his own note tells you this is not a risk he dismisses lightly. BofA’s target has also been revised upward multiple times across the cycle, which raises a fair question: is conviction rising on new evidence, or are targets chasing momentum? Any position in Micron requires weighing both sides of that question.

This article is for informational purposes only and should not be considered financial advice. Investors should conduct their own research and consult with financial professionals before making investment decisions.

The next 12-18 months of earnings calls are the proving ground. Three metrics from Arya’s framework will either confirm or challenge the structural upgrade narrative:

HBM contract pricing in 2027 will likely be the single sharpest test of Arya’s durability argument: Bernstein projects a 2-2.5x increase in contract prices for that year, an increase that amplifies approximately fourfold at the hyperscaler purchase level once GPU vendors apply their margin targets.

If HBM allocation is growing and hyperscaler commitments are extending, the market may begin applying a higher multiple to the AI segment. That is when the re-rating Arya describes would actually show up in the stock price.

Past performance does not guarantee future results. Financial projections are subject to market conditions and various risk factors. BofA’s price target is a 12-month estimate subject to revision.

The core tension is clean. BofA’s $1,550 target implies the market will eventually price Micron’s AI/HBM business on AI compute multiples rather than commodity memory multiples. The market’s current ~10x forward multiple implies it will not, at least not yet.

The gap between ~10x (market) and ~27x (BofA’s AI segment target) represents two entirely different theories of what kind of company Micron has become.

The UBS re-rating in May 2026 established a comparable precedent for what analyst-driven multiple expansion looks like in practice: a 204% price target increase to $1,625 pushed Micron past a $1 trillion market cap within a single session, with the thesis anchored to the same HBM supply concentration and long-term agreement structures Arya cites.

Arya’s thesis is about when, not whether. If earnings remain stable through CY28 and HBM share grows as projected, the cyclicality discount erodes over time and the re-rating follows. The price target progression from $500 to $1,550 across the AI cycle reflects BofA’s view that the evidence is accumulating in that direction.

This is a thesis built for an investor with a 12-18 month horizon, someone willing to hold through volatility while the proving-ground data accrues on quarterly earnings calls. Whether the evidence confirms or challenges the re-rating argument, the three metrics above are where you will see it first.

HBM, or high-bandwidth memory, is a type of memory stacked vertically and packaged directly alongside AI processors to deliver the data throughput those chips require. It commands a significant price premium over conventional DRAM, and Micron is one of only a handful of manufacturers capable of producing it at leading-edge scale, which is central to Bank of America's bull case.

Bank of America analyst Vivek Arya set a 12-month price target of $1,550 on Micron in July 2026, maintaining a Buy rating and arguing the stock should be valued on AI compute multiples rather than commodity memory multiples.

The market is applying a cyclicality discount to Micron's earnings, treating projected profits as peak-cycle rather than durable. Arya argues this discount is the mispricing: if HBM earnings prove stable through CY28 as he projects, the low multiple is not justified and a re-rating follows.

Arya himself flags that elevated memory pricing acts as a tax on data centre capital expenditure, potentially suppressing demand in price-sensitive segments like mobile and automotive. Historical memory cycles have also ended through a combination of demand weakness and new capacity additions, and there is no guarantee the current cycle escapes that pattern.

Arya identifies three proving-ground metrics: HBM allocation updates showing whether Micron is winning supply agreements with hyperscalers, the trajectory of strategic versus spot pricing, and whether hyperscalers are extending or shortening their forward commitment windows.