BofA Survey: AI Crowding Hits All-Time High as Inflation Fear Surges

19 mins ago

SpaceX went public on 12 June 2026, raising $75 billion at a $1.77 trillion valuation. By the close of its first trading day, the company had surpassed both Saudi Aramco and Tesla in initial market capitalisation rankings, crossing the $2 trillion threshold on opening-day demand alone. For Canadian investors holding S&P 500 ETFs, Nasdaq-100 ETFs, or global all-in-one products like VEQT or XEQT, the instinct may be to treat this as someone else’s news. That instinct may not hold. Index operators are reportedly revising eligibility rules to accommodate SpaceX’s entry into major benchmarks, and once any inclusion is confirmed, passive funds must buy in automatically, at whatever price the market sets. What follows is an explanation of how that mechanism works, which Canadian ETF products are exposed, what the Tesla precedent reveals about scale, and what specific decisions remain unresolved.

The raw scale of the listing is difficult to overstate. SpaceX priced at $135 per share, opened near $150, and closed its first session around $161, pushing the company’s market capitalisation above $2 trillion on the strength of institutional and retail demand combined.

Key facts from the debut:

Record-setting raise: The $75 billion raised by SpaceX surpassed every previous IPO in history by total funds raised, placing the listing in a category of its own by that measure.

Those headline figures explain why index operators cannot simply look the other way. A company at this scale, once publicly listed, becomes a structural question for every passive fund benchmarked to a market-cap-weighted index. But total market capitalisation is not the figure that determines index weight. Free-float market capitalisation, the value of shares freely tradable by the public, is what matters. The size of Elon Musk’s retained stake means the investable slice is meaningfully smaller than $2 trillion, and that distinction makes everything that follows conditional rather than settled.

An inflation-adjusted Aramco comparison complicates the record claim: Aramco’s 2019 valuation converts to roughly $2.21 trillion in 2026 dollars, meaning SpaceX’s $1.77 trillion implied valuation does not surpass Aramco’s peak in real purchasing-power terms even as it sets a clear nominal record for capital raised.

The Guardian’s live IPO coverage confirmed a closing price of $160.95 and a market capitalisation of $2.1 trillion at the end of the first session, corroborating the record-setting scale that forces index operators to treat SpaceX as a structural question rather than a routine new listing.

Market-cap-weighted indexes require every constituent fund to hold each company in proportion to its free-float weight. There is no element of fund manager discretion in this process. If a company enters the S&P 500 at a 2% weight, every S&P 500 index fund must allocate 2% of its assets to that stock, regardless of whether the fund manager considers the valuation attractive.

The eligibility criteria that govern which companies qualify for inclusion are set by index operators, and they cover several dimensions:

SpaceX’s founder-controlled structure raises the same class of issues that prompted index methodology adjustments in prior cases. The question is not whether SpaceX is large enough. It is whether its governance and float characteristics satisfy rules that were written before a company of this structure reached this scale.

As of 16 June 2026, no formal inclusion decision has been published by S&P Dow Jones Indices, Nasdaq, MSCI, or FTSE Russell. Index operators are reportedly revising rules to accommodate SpaceX’s entry, but no finalised changes are public. The free-float classification, which determines the actual index weight, may take months to settle as post-IPO lockup periods expire and liquidity data accumulates. The possible inclusion weight range sits at an estimated 1-3% of the S&P 500, contingent entirely on that classification.

Three channels connect Canadian investor portfolios to a potential SpaceX index inclusion, and the exposure varies meaningfully across them.

| ETF Category | Example Canadian ETFs | Benchmark Index | Estimated SpaceX Exposure (Illustrative) | Notes |

|---|---|---|---|---|

| S&P 500 | VFV, ZSP, XUS, XSP | S&P 500 | 1-3% of ETF assets | Depends on free-float classification |

| Nasdaq-100 | QQC, XQQ, ZNQ | Nasdaq-100 | Proportionally larger than S&P 500 | Growth-company concentration amplifies weight |

| Global All-in-One | VEQT, XEQT, XAW, ZGRO | MSCI World / ACWI / FTSE | Under a few percent of total portfolio | U.S. stocks typically represent 50-65% of these indexes |

| Canadian-Only | XIU, ZCN, VCN | S&P/TSX Composite | Zero | SpaceX is U.S.-listed; no direct exposure |

For a Canadian investor with 40-60% of their portfolio allocated to U.S. index ETFs, a 2% SpaceX weight in the S&P 500 would translate to roughly 0.8-1.2% of total portfolio value, acquired without a single direct trade. The Nasdaq-100 effect is proportionally larger given that index’s growth-company concentration. Canadian-only equity index funds tracking the S&P/TSX Composite carry zero direct SpaceX exposure; the company is U.S.-listed and will not appear in domestic benchmarks.

The Nasdaq 100 fast-entry rule allows a qualifying new listing to join the index in approximately 15 trading days, compared with the S&P 500’s minimum 12-month seasoning requirement, meaning Nasdaq-tracking ETFs could acquire SpaceX exposure many months before any S&P 500 fund is required to move.

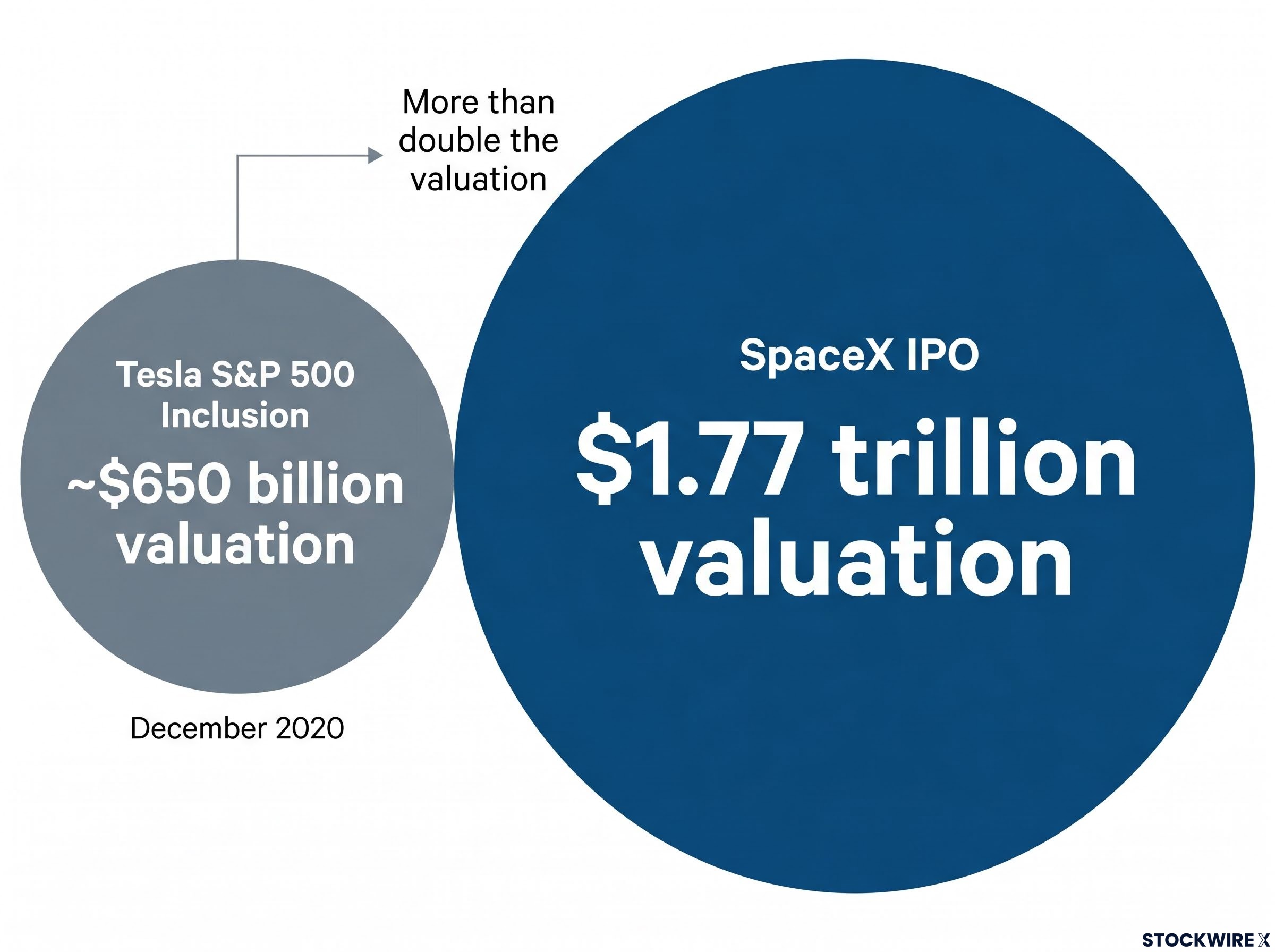

When Tesla entered the S&P 500 in December 2020, it carried a valuation of approximately $650 billion, making it one of the largest single additions in the index’s history at that time. Index funds were required to purchase tens of billions of dollars of Tesla stock within a compressed window. The result was a sharp price run-up into the inclusion date, followed by elevated volatility afterward.

The scale of that forced buying was quantified in real time, with AP News reporting on Tesla’s S&P 500 entry estimating that institutional funds faced obligations exceeding $80 billion in Tesla purchases within a narrow window, a figure that underscores why the mechanics of index inclusion matter far beyond the company being added.

The mechanics played out in a way that mattered for existing holders. Investors who already held S&P 500 ETFs before the inclusion announcement effectively acquired Tesla at a lower blended entry price through their existing positions. Those who purchased the same ETFs near the peak of inclusion-driven flows paid higher effective prices for Tesla exposure inside the fund.

SpaceX’s $1.77 trillion IPO valuation was more than double Tesla’s approximately $650 billion valuation at its S&P 500 inclusion, suggesting the magnitude of index-driven buying flows could be considerably larger if the eligibility path clears.

The timing implication is straightforward: investors already holding index ETFs before a confirmed SpaceX inclusion may benefit from gradual accumulation at pre-inclusion prices, while those buying into index ETFs around the inclusion event itself may pay elevated effective prices for SpaceX exposure. This is a pattern observed with Tesla, not a guarantee. It depends entirely on whether eligibility is confirmed and on how the market prices in the event in advance.

Three demand forces drove the post-IPO surge to near $3 trillion: pent-up access demand from investors who had no route into SpaceX as a private company, a multi-theme narrative premium spanning defence, connectivity, and space infrastructure, and active front-running of anticipated S&P 500 and Nasdaq 100 index inclusion by institutional desks.

A volatile, founder-controlled company in a capital-intensive, geopolitically sensitive industry representing 1-3% of a broad index is a genuine concentration consideration. The concern is not hypothetical. SpaceX-specific risk factors that distinguish it from most existing mega-cap index constituents include:

The symmetry argument, however, deserves equal weight. Apple, Microsoft, and Nvidia already occupy comparably large single-name positions in the same indexes through the same market-cap weighting mechanism. SpaceX’s inclusion, if it occurs, would be a continuation of that rule set, not a departure from it.

US index fund concentration had already reached historically extreme levels before SpaceX listed, with five mega-cap names controlling roughly 23% of the broad market index as of mid-April 2026, meaning any SpaceX inclusion adds to a structure that institutional strategists at Morgan Stanley, JPMorgan, and Goldman Sachs had each already flagged as a potential correction catalyst.

For passive investors who conclude that the concentration is worth managing, practical options include:

The appropriate posture is awareness rather than portfolio restructuring, unless the confirmed index weight becomes large enough to conflict with individual risk parameters.

Several unresolved decisions will determine whether and how SpaceX enters passive investors’ portfolios. In priority order:

SpaceX trades in U.S. dollars, so any exposure acquired through Canadian-listed ETFs carries USD currency risk. If the Canadian dollar strengthens against the USD, the SpaceX position (and all other U.S. holdings) will be worth less in Canadian-dollar terms. SpaceX currently pays no dividends, so U.S. withholding tax is not an immediate concern. If dividends are introduced in the future, RRSP holders may benefit from holding U.S.-listed ETF versions (such as IVV, VTI, or QQQ) for tax-treaty efficiency under the Canada-U.S. treaty.

The SpaceX listing is a landmark event whose portfolio consequences for passive investors depend on eligibility decisions not yet made. Preparation is more useful than reaction.

Two practical takeaways apply. First, identify which ETFs in a given portfolio would carry automatic SpaceX exposure by checking the underlying benchmark index each fund tracks. Second, monitor the specific eligibility announcements from S&P Dow Jones, Nasdaq, MSCI, and FTSE Russell that will determine whether, and at what weight, that exposure arrives.

For most broadly diversified investors, the SpaceX position, even at 1-3% of a major index, would be one element of a portfolio already navigating large single-name concentrations in Apple, Microsoft, and Nvidia. The question is whether that level of concentration is acceptable given individual risk tolerance, not whether it is unprecedented.

This article is for informational purposes only and should not be considered financial advice. Investors should conduct their own research and consult with financial professionals before making investment decisions. Forward-looking statements regarding index inclusion are speculative and subject to change based on decisions by index operators and evolving market conditions.

Index inclusion is the process by which a newly public company is added to a market-cap-weighted benchmark like the S&P 500, requiring every fund tracking that index to automatically buy the stock in proportion to its weight. SpaceX's $2 trillion-plus market capitalisation after its 12 June 2026 debut makes it large enough to warrant consideration by major index operators, though eligibility is not yet confirmed.

Canadian ETFs benchmarked to the S&P 500 (such as VFV, ZSP, and XUS), the Nasdaq-100 (such as QQC and XQQ), and global all-in-one products (such as VEQT and XEQT) would all acquire SpaceX exposure automatically upon confirmed inclusion, with Canadian-only funds like XIU and VCN carrying zero exposure since SpaceX is U.S.-listed.

The estimated inclusion weight sits in the range of 1-3% of the S&P 500, depending on how index operators classify SpaceX's free-float market capitalisation, which is smaller than its total market cap due to Elon Musk's retained stake.

When Tesla joined the S&P 500 in December 2020 at a roughly $650 billion valuation, institutional funds faced estimated buying obligations exceeding $80 billion in a narrow window, driving a sharp price run-up into the inclusion date followed by elevated volatility. SpaceX's IPO valuation was more than double Tesla's at inclusion, suggesting the scale of forced buying could be considerably larger.

Investors should check the underlying benchmark index each ETF tracks and then monitor formal announcements from S&P Dow Jones Indices, Nasdaq, MSCI, and FTSE Russell on rule changes and inclusion timelines, as well as updated holdings notices from providers such as Vanguard Canada, BlackRock iShares Canada, and BMO ETFs.