SpaceX raised more money in a single initial public offering than Saudi Aramco, Alibaba, and Rivian combined. Then, on its second day of trading, the stock surged another 19.6%. As of 16 June 2026, SpaceX’s market capitalisation is approaching $3 trillion, placing a company that was entirely unavailable to public investors just days ago alongside Apple, Nvidia, and Alphabet in the upper tier of global equities. The pace and scale of this move have no real modern precedent. What follows breaks down the mechanics behind the surge, examines what the price action genuinely signals versus what it does not, and provides retail investors with a framework for thinking about whether and how to engage with a stock in active price-discovery euphoria.

From private rocket company to a $3 trillion market in 72 hours

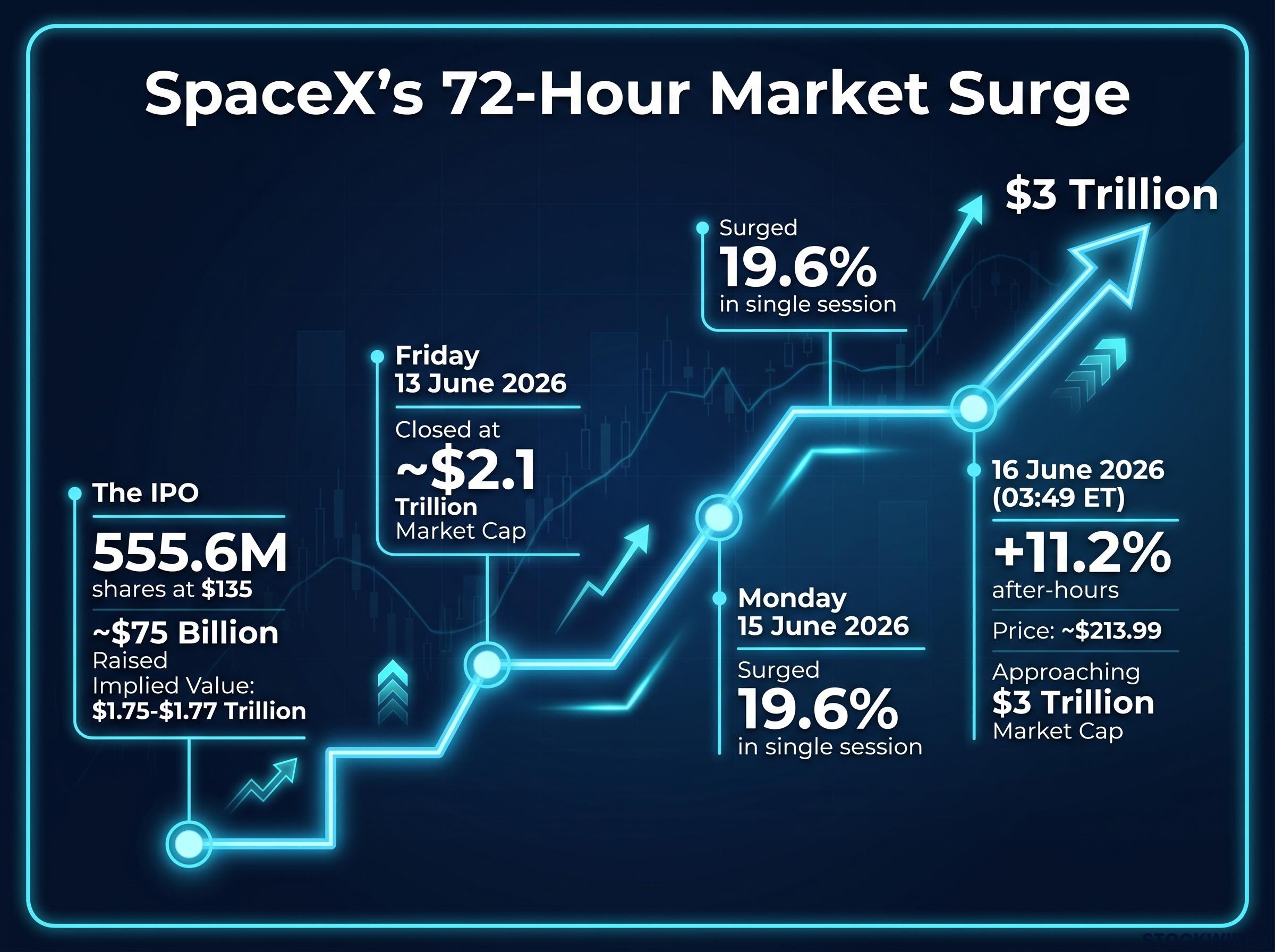

The numbers speak first. SpaceX sold approximately 555.6 million shares at $135 each, raising roughly $75 billion and implying a Day 1 valuation of approximately $1.75-$1.77 trillion. What followed was a three-stage escalation that compressed what normally takes months of price discovery into a single long weekend.

SpaceX’s $75 billion raise and $1.75 trillion target valuation were confirmed via multiple major financial outlets when the confidential S-1 filing details became public, establishing the pricing parameters that underpinned Day 1 demand and set the floor for subsequent after-hours appreciation.

- Friday 13 June 2026: SpaceX completed its IPO debut, closing with a market capitalisation of approximately $2.1 trillion.

- Monday 15 June 2026: Shares surged 19.6% in a single session as institutional and retail demand overwhelmed available supply.

- Early hours of 16 June 2026: After-hours trading added another 11.2%, pushing the price to approximately $213.99 per share by 03:49 ET, with market capitalisation approaching $3 trillion.

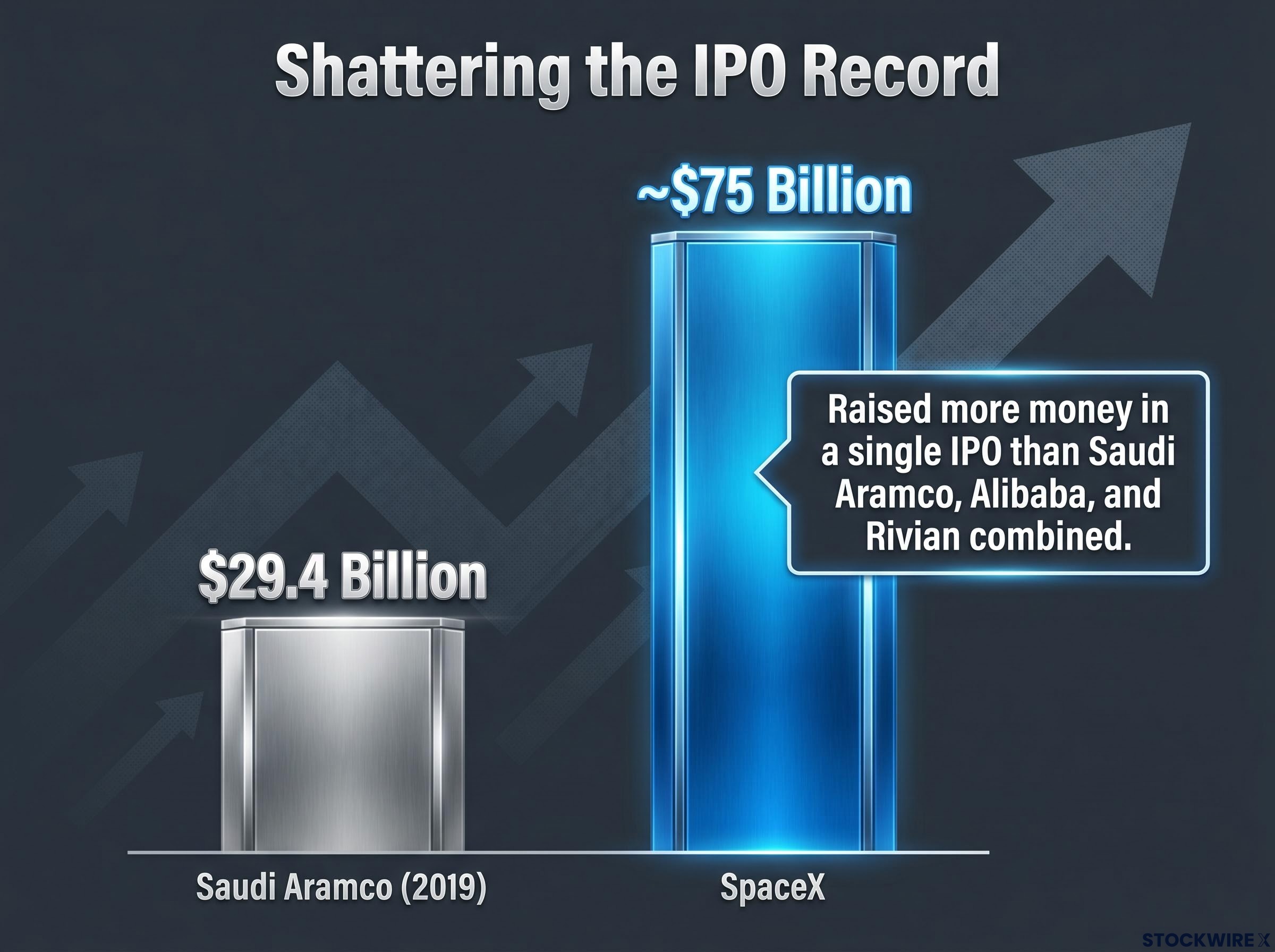

For context: Saudi Aramco’s 2019 IPO, the previous record holder, raised $29.4 billion. SpaceX more than doubled that figure in a single offering.

That comparison alone captures the scale. A company that did not exist on public exchanges last week now sits in the same valuation tier as firms that took decades to reach comparable levels.

When big ASX news breaks, our subscribers know first

Why investors are buying SpaceX at almost any price right now

The surge is not a single force. It is three distinct demand mechanics operating simultaneously, each with its own logic and its own expiry date.

- Pent-up access demand. SpaceX stayed private far longer than a typical company of its scale. Institutional and retail investors watched reusable rockets, Starlink’s rollout, and government contracts for years without any liquid way to participate. The IPO released that accumulated appetite into a single window.

- Narrative premium. SpaceX sits at the intersection of space infrastructure, satellite broadband, defence contracts, AI-enabled systems, and longer-horizon speculation about lunar and Martian economies. Any one of these themes individually commands high multiples; combined, they allow models projecting enormous total addressable markets.

- Index inclusion anticipation. At multi-trillion-dollar valuations, SpaceX would quickly become a top-weighted name in benchmarks such as the S&P 500. Passive funds tracking those benchmarks would then be obligated to buy shares regardless of internal valuation views. Traders front-run that mechanical demand before formal inclusion is confirmed, creating self-reinforcing upward pressure.

The index inclusion mechanics at play here differ materially between the two major US benchmarks: the NASDAQ 100 operates a fast-entry rule that can seat a qualifying new listing in approximately 15 trading days, while the S&P 500 imposes a minimum 12-month seasoning requirement alongside simultaneous profitability, market capitalisation, and liquidity gates, meaning passive funds tracking each benchmark face structurally different timelines for absorbing a name like SpaceX.

SpaceX operates across four distinct revenue segments at very different maturity stages, launch services, Starlink broadband, Direct-to-Cell wholesale infrastructure, and AI compute, and applying a single valuation multiple across all of them is one of the most common analytical errors investors make when assigning a number to a company this structurally complex.

The index inclusion mechanics for S&P 500 eligibility require a company to meet profitability thresholds and float requirements before formal addition, meaning the front-running of passive fund demand that traders are executing now precedes any confirmed committee decision by weeks or months.

Each of these forces is real. Each is also finite. Pent-up demand exhausts itself once existing buyers are positioned. Index-driven buying is mechanical and temporary. Narrative premiums can deflate quickly when sentiment shifts. In the first week after an IPO, the story often moves the stock as much as the fundamentals.

What an IPO surge tells you, and what it does not

Strong early momentum carries genuine information. It also carries assumptions that investors tend to smuggle in without realising it.

The 19.6% single-session gain and 11.2% after-hours move confirm broad institutional enthusiasm, effective underwriter pricing that left upside on the table, and active price discovery as large funds establish positions. These are legitimate positives.

The line falls at what that momentum does not confirm. A stock rising sharply does not mean the current price equals intrinsic value. It does not mean the appreciation rate is sustainable. And it does not mean the stock is low-risk simply because demand is high. Periods of maximum market attention often coincide with maximum valuation uncertainty. History across large, high-profile IPOs shows that 30-50% drawdowns frequently occur at some point as early buyers recycle gains and insiders eventually gain liquidity.

| What the surge signals | What the surge does not signal |

|---|---|

| Broad institutional enthusiasm for the business | That the current price equals long-term intrinsic value |

| Effective underwriter pricing that drove demand | That the rate of appreciation is sustainable |

| Active price discovery is underway | That valuation certainty has been established |

| SpaceX is widely viewed as a defining asset | That high demand equals low risk |

The distinction matters because conflating momentum with certainty is where most post-IPO losses originate.

The SpaceX IPO valuation picture was already complex before a single share traded publicly: the company posted a $4.28 billion net loss on $4.69 billion in Q1 2026 revenue, meaning the $1.75-$2 trillion pricing range implied roughly $1.8 trillion in optionality above any fundamentals-anchored estimate, a gap that now widens further as the market capitalisation approaches $3 trillion.

A framework for retail investors evaluating a momentum-driven IPO

Analysis without a decision framework is spectating. What follows is a four-step process that replaces emotional reaction with deliberate structure.

- Separate the business from the stock. SpaceX is a remarkable company with real revenue, defensible technology, and deep government relationships. None of that automatically makes the stock a good trade at a near-$3 trillion valuation today. Evaluating SpaceX now is about this price versus plausible long-term cash flows, not about whether the rockets are impressive.

- Define the time horizon explicitly. A 10-plus-year investor tolerating large drawdowns is making a structurally different bet than someone with a 1-3 year horizon. The same stock can be appropriate for one and inappropriate for the other simultaneously.

- Set position size before entry. Define a maximum allocation, 1-5% of a portfolio as a reference point, that would not cause financial or emotional distress at a 30-40% drawdown. Consider scaling in over time rather than committing all capital after a parabolic move.

- Assess the information edge honestly. Major institutions are running detailed models on Starlink economics, launch cadence, and capital expenditure. Most retail investors are not. Humility about that asymmetry is a risk control, not a concession.

“A great company can be a poor investment at the wrong price.”

Most individual investors are hurt more by oversized positions entered during emotional market moments than by imprecise entry timing. The variables within an investor’s control, position size, time horizon, and thesis clarity, deserve more attention than the variables that are not.

What SpaceX’s debut means for every large private company watching

Step back from the individual stock and the structural signal comes into focus. SpaceX’s reception demonstrates that public markets can still absorb and reward complex, capital-intensive, late-stage private companies at scale. That pushes back against the narrative that the most valuable companies will stay private indefinitely.

Other large private firms are watching closely. Companies in AI, infrastructure, and deep technology are likely to view this debut as evidence that public markets will pay up for the right growth profile and story. The practical implications for investors follow directly:

Market absorption capacity for the next wave of mega-listings is already a live concern: Standard Chartered’s global CIO warned in early June 2026 that SpaceX, Anthropic, and OpenAI, collectively valued at approximately $3.5 trillion and all targeting public listings within a compressed mid-to-late 2026 window, could trigger genuine digestion difficulties as institutional capital is redirected from existing holdings to fund successive allocations.

- More mega-IPOs over the next market cycle as private companies recalibrate their public-listing timelines.

- More situations where story-driven valuations run ahead of fundamentals in the early post-listing period.

- A growing need to distinguish long-term compounders from hot listings, applying the same analytical framework used here to each new name that arrives.

SpaceX has set a new benchmark for what is possible in public markets. Every large private company considering a listing, and every investor who will evaluate them, now operates in a different context.

Immense potential and serious valuation risk are not mutually exclusive

SpaceX is a defining asset of this market era, and that status cuts both ways. The market is already pricing in extraordinary future growth across multiple industries simultaneously. Future returns from this level depend less on whether SpaceX succeeds and more on how much it exceeds already-lofty expectations, a much harder hurdle.

The defensible strategies remain consistent: treat SpaceX as a high-volatility satellite position rather than a core holding; align exposure with a genuine long time horizon and a tolerance for drawdowns that holds in practice, not just in theory; and build a written investment thesis that would survive a 40% drawdown before making any allocation decision.

The story is extraordinary. The principles are not. The discipline required to invest well in a stock like this is the same discipline required in any high-momentum, high-attention moment.

This article is for informational purposes only and should not be considered financial advice. Investors should conduct their own research and consult with financial professionals before making investment decisions. Past performance does not guarantee future results, and financial projections are subject to market conditions and various risk factors.