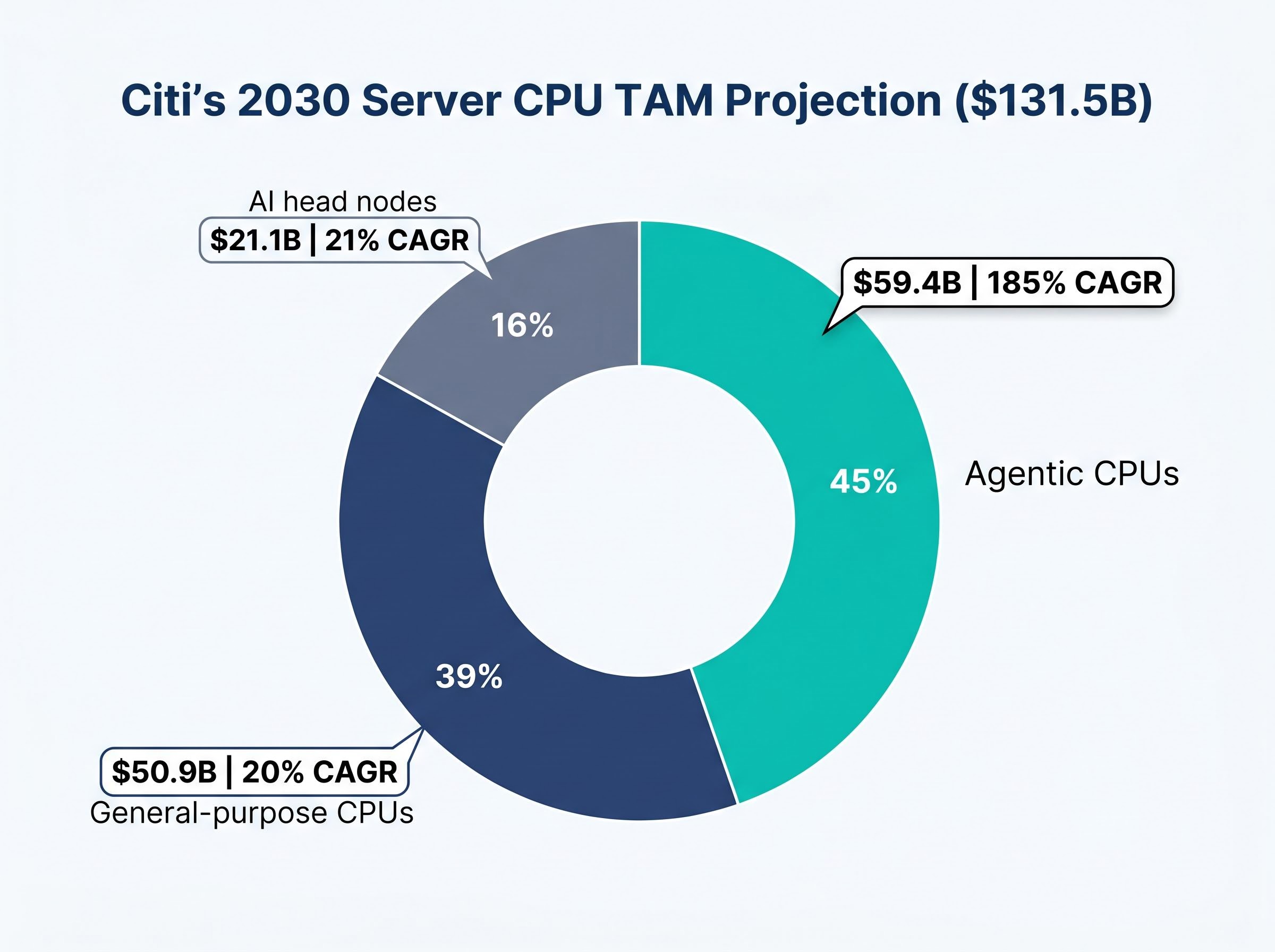

Citi published a server CPU total addressable market (TAM) model on 18 May 2026 that projects the market will grow from $29.3 billion in 2025 to $131.5 billion by 2030. The engine behind that expansion is a category that barely existed in prior forecasts: agentic CPUs, a segment Citi models at a 185% compound annual growth rate (CAGR), reaching $59.4 billion and accounting for roughly 45% of the total server CPU market by the end of the decade. The server CPU market has long been treated as a mature, slow-growth segment overshadowed by GPU spending. Citi’s three-segment framework challenges that assumption directly, carving out agentic AI as a structurally distinct demand driver that forces a rethink of where data centre infrastructure dollars will flow over the next four years. What follows is a breakdown of Citi’s model, a benchmark against competing forecasts from AMD, ARM, and UBS, an explanation of what agentic CPU demand actually means in infrastructure terms, and a translation of the market-share projections into investor-relevant implications for Intel and AMD.

How Citi’s three-segment model reframes the entire server CPU market

For most of the past decade, server CPUs were the line item nobody watched. GPU spending dominated AI infrastructure narratives, and server processors grew at single-digit rates that barely registered in portfolio allocation models. Citi’s 18 May 2026 note dismantles that framing by splitting the market into three distinct segments, each with materially different growth trajectories.

General-purpose CPUs, the segment investors already know, are projected to reach $50.9 billion by 2030 at a 20% CAGR. AI head nodes, the processors that sit alongside GPU clusters managing data preprocessing and model serving, reach $21.1 billion at a 21% CAGR. Neither figure is negligible, but neither rewrites the investment thesis.

The agentic CPU segment does. Citi projects it will grow at a 185% CAGR to $59.4 billion by 2030, making it roughly 45% of the total market. The analytical significance is not just the number; it is the taxonomy itself. No prior public sell-side model formally carved out agentic CPUs as a discrete commercial category with its own CAGR.

The scale of divergence: Citi’s agentic CPU segment alone, at a 185% CAGR, grows nearly nine times faster than the conventional server CPU segments in the same model.

| Segment | 2030 TAM | CAGR | Share of Total Market |

|---|---|---|---|

| General-purpose CPUs | $50.9B | 20% | ~39% |

| AI head nodes | $21.1B | 21% | ~16% |

| Agentic CPUs | $59.4B | 185% | ~45% |

Investors who have been allocating around GPU spending alone are operating with an incomplete infrastructure map. Citi’s model suggests the CPU layer may absorb nearly as much capital by decade’s end.

When big ASX news breaks, our subscribers know first

What agentic AI actually demands from a CPU

The standard understanding of AI infrastructure is straightforward: GPUs handle training and inference, CPUs handle everything else. For traditional single-pass large language model (LLM) inference, that division holds. A user submits a prompt, the GPU generates a response, and the CPU’s role is limited to data preprocessing and routing.

Agentic AI workloads operate differently. Instead of a single model call, an AI agent executes multi-step tasks: retrieving information from databases, calling external tools and APIs, maintaining state across interactions, and orchestrating sequences of decisions. The compute profile shifts substantially.

The key differences between the two workload types are:

The CPU-to-GPU deployment ratio, historically running as wide as 1:8 in favour of GPUs, is compressing toward parity as agentic orchestration layers require dedicated processing capacity that GPU clusters are not designed to provide; three simultaneous May 2026 earnings reports from Arm, AMD, and Intel confirmed that this compression is a structural procurement shift rather than a cyclical fluctuation.

- Traditional inference: GPU-dominated, relatively stateless, single-pass model calls, smooth and predictable compute demand

- Agentic workloads: Multi-step orchestration across tools and databases, stateful session management, bursty and irregular compute profiles, high volumes of API calls and business logic validation

- CPU content: Agentic systems run many smaller concurrent agents rather than single large model calls, amplifying CPU parallelism demands

Why orchestration and retrieval layers are CPU-bound, not GPU-bound

The frameworks that coordinate agentic workflows, such as LangChain and LlamaIndex, run on CPU infrastructure surrounding the GPU cluster rather than on the GPU itself. Vector databases used for retrieval-augmented generation (RAG), where an agent searches a knowledge base before responding, are similarly CPU-intensive. Vendors including Pinecone, Weaviate, and Milvus have noted high CPU utilisation in RAG deployments for search, embedding management, and query routing.

Nvidia CEO Jensen Huang has described AI agents as requiring significant CPU and system resources for retrieval, orchestration, and input/output operations surrounding GPU-based model execution, in commentary at GTC events through 2024-2025. It is worth noting that “agentic CPU” as a commercial segment is Citi’s framing; public industry sources more commonly refer to “AI agents” or “autonomous agents.” No published quantitative CPU-to-GPU ratio for agentic workloads is publicly available as of May 2026.

How Citi’s forecast stacks up against AMD, ARM, and UBS

Citi’s $131.5 billion figure does not exist in isolation. Four named sources have published 2030 server CPU TAM estimates, and the spread between them signals both the opportunity’s scale and the analytical uncertainty surrounding it. Ranked from lowest to highest:

- ARM: approximately $100 billion by 2030, framed around AI and cloud workloads broadly (ARM investor materials, 2023-2024)

- AMD management: greater than $120 billion by 2030, with a 35%+ CAGR for AI-driven segments (AMD Q1 2026 earnings, May 2026)

- Citi: $131.5 billion by 2030 (18 May 2026)

- UBS: approximately $170 billion by 2030, citing agentic AI workload orchestration as a primary driver (UBS research note, 5 May 2026)

| Source | 2030 Server CPU TAM Estimate | Key Methodology Note |

|---|---|---|

| ARM | ~$100B | Broadly framed around AI/cloud; does not isolate agentic demand |

| AMD | >$120B | Management commentary; 35%+ blended CAGR without agentic breakout |

| Citi | $131.5B | Only model to formally carve out agentic CPUs as a discrete segment |

| UBS | ~$170B | Most bullish estimate; cites agentic orchestration as primary driver |

The methodological distinction matters. Only Citi formally isolates agentic CPUs as a discrete segment with its own CAGR. AMD’s management commentary aligns directionally but uses a blended growth figure. ARM’s estimate predates the current agentic framing entirely. No sell-side firm has publicly contested or corroborated Citi’s specific $131.5 billion TAM and 185% agentic CAGR as of the publication date.

Investors examining the ARM forecast more closely will find our full explainer on the Arm supply gap and its implications for the CPU market, which details how aggregate hyperscaler demand for Arm’s AGI CPU exceeded $2 billion against secured supply of roughly half that figure, a constraint that directly limits how quickly ARM-based architectures can absorb their projected share of agentic workloads.

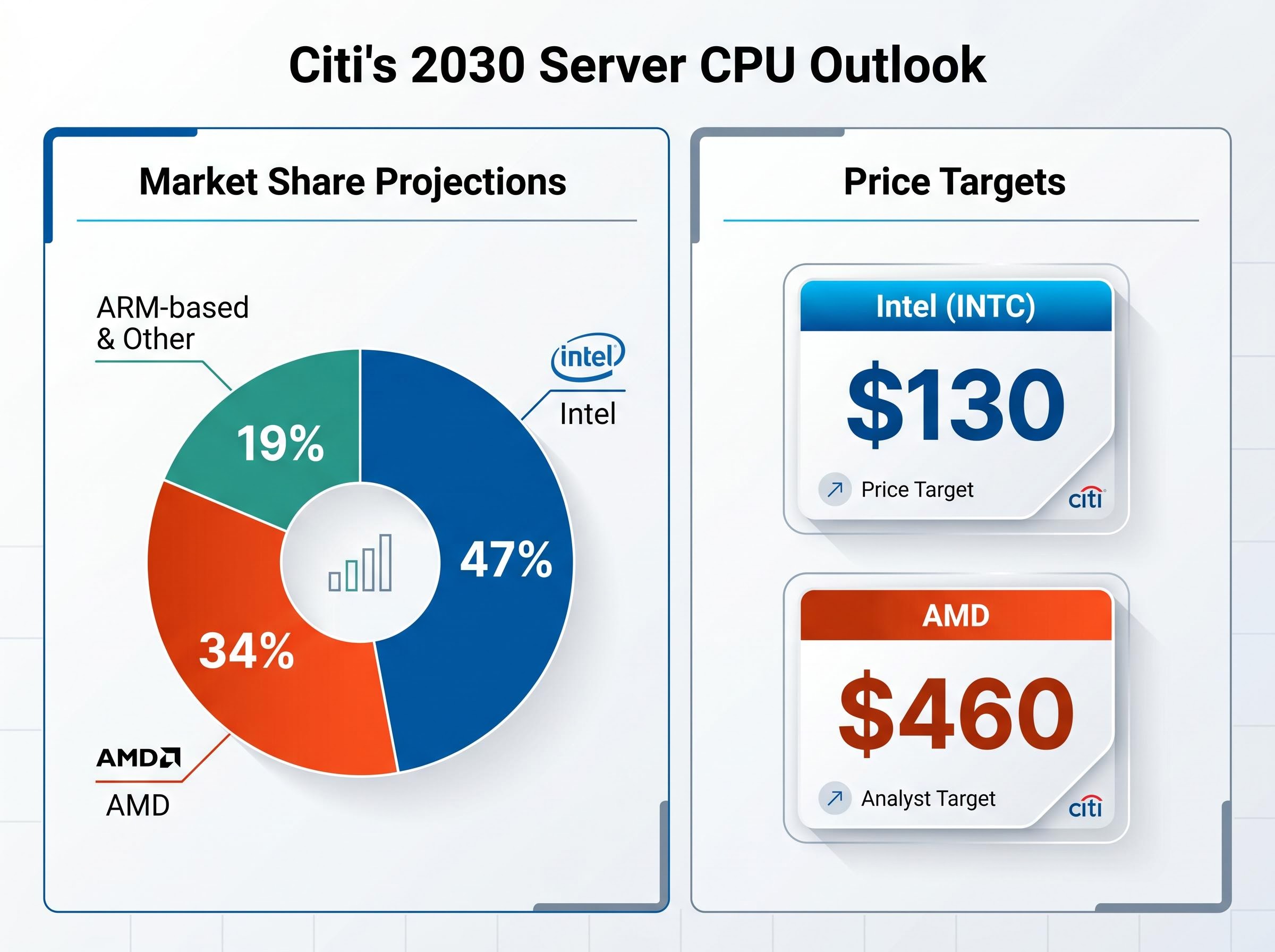

Market share implications for Intel and AMD by 2030

Citi’s model does more than size the market. It allocates it. The projected split, Intel at 47%, AMD at 34%, and ARM-based and other architectures at 19%, carries specific implications for how investors should think about the two largest US-listed server CPU names.

Citi price targets: Intel (INTC) at $130; AMD at $460

Intel’s share leadership in the model is notable precisely because it cuts against the prevailing narrative of AMD’s EPYC processors steadily eroding Intel’s data centre position. Citi’s framework suggests that agentic CPU demand at hyperscale may disproportionately benefit Intel’s installed-base scale and enterprise sales infrastructure. The note also identifies Intel’s Mount Evans IPU ASIC division as an upside driver, with Google as a confirmed customer and Anthropic cited in Citi’s channel checks as a potential extension of that relationship (not independently confirmed as of 18 May 2026).

AMD’s agentic AI upside and the MI450 deployment signal

AMD’s 34% share projection rests on two pillars: the continued momentum of its EPYC Turin-class server CPU roadmap built on advanced TSMC process nodes, and its expanding AI accelerator portfolio. AMD confirmed the Instinct MI450 launch on 24 February 2026, with production shipments scheduled for 2H 2026 in rack-scale Helios configurations paired with 6th Gen EPYC CPUs.

Meta is the publicly confirmed large-scale MI450 deployment partner. Citi’s channel checks suggest Anthropic as a potential MI450 customer, though this has not been confirmed in public disclosures as of 18 May 2026. The MI450 ramp serves as evidence that AMD can compete for the infrastructure contracts agentic AI spending is expected to generate, reinforcing the 34% share projection.

The AMD and Meta expanded strategic partnership announcement confirmed Meta as the primary large-scale deployment partner for the Instinct MI450, giving AMD a publicly anchored reference customer for its rack-scale Helios infrastructure at the moment agentic AI spending is projected to accelerate most sharply.

Why 185% CAGR projections require a calibrated reading

A 185% CAGR is an extraordinary figure. The architectural arguments supporting elevated agentic CPU demand are qualitatively well-supported, as outlined above. The risk lies in the assumptions required to translate qualitative demand signals into a precise dollar figure four years out.

Three categories of assumption are embedded in the projection:

Enterprise agentic AI deployment rates are a critical variable in translating Citi’s architectural case into realised CPU revenue, with current data placing production agentic deployments at roughly 17% of enterprises as of April 2026, well below the adoption velocity that a 185% CAGR would require to materialise on schedule.

- Enterprise adoption rate: The speed at which organisations deploy production agentic AI systems rather than pilot projects

- CPU content per deployment: The amount of CPU infrastructure required per agentic deployment relative to GPU spend, a ratio no public source has quantified through May 2026

- Architectural durability: Whether orchestration and retrieval layers remain CPU-bound or migrate to GPU or custom silicon as the technology matures

No enterprise case study with explicit CPU/GPU sizing data for agentic workloads has been published publicly through mid-May 2026. The quantitative foundation for the agentic segment remains a working estimate.

Citi’s model is a terminal forecast built on channel checks and architectural reasoning. It has not yet been confirmed by hyperscaler capital expenditure disclosures that break out CPU infrastructure at the segment level. The note was published 18 May 2026, and the forecast runs to 2030 across a technology environment where product roadmaps and architectural choices shift materially within 12-18 month cycles.

This does not invalidate the thesis. It calibrates it. Commercial-intent investors evaluating semiconductor positions need both the structural case and its material uncertainties to size exposure appropriately.

The next major ASX story will hit our subscribers first

The $131.5 billion question: how to position around a structural shift that is still early

Citi’s framework points to a server CPU market undergoing structural reclassification, with agentic AI as the primary mechanism and two public equities, Intel and AMD, carrying the largest addressable exposure. The cross-firm consensus brackets the opportunity: ARM at approximately $100 billion, AMD management above $120 billion, Citi at $131.5 billion, and UBS at approximately $170 billion. Directional agreement is broad-based, even where the precise agentic contribution remains contested.

The question is not whether the server CPU market is repricing. The question is at what velocity, and on what timeline.

Four signals that will confirm or challenge the agentic CPU thesis

- AMD MI450 production ramp: Shipment velocity in 2H 2026 and any agentic AI attribution in AMD’s Q2 2026 earnings commentary

- Hyperscaler capex disclosures: Whether AWS, Google, or Microsoft Azure begin separating CPU infrastructure from GPU line items in capital expenditure reporting

- Intel Xeon 6 trajectory: Volume shipments of Sierra Forest and Granite Rapids variants, and any publicly disclosed agentic AI workload wins in enterprise or cloud deployments

- AMD Advancing AI event: Anticipated for July 2026 per Citi channel checks (not yet formally confirmed by AMD), and whether Anthropic’s hardware relationship with AMD is publicly disclosed

A new CPU supercycle or an ambitious model: the answer will arrive by 2027

Citi’s note is not a revision of an existing forecast. It is the introduction of a new analytical category, and that distinction matters more than the headline number. The $131.5 billion TAM sits within a range of $100 billion to $170 billion from named sources, suggesting the directional case for a server CPU renaissance has broad-based support, even if the agentic segment’s precise contribution remains a working hypothesis.

The specific CAGR will shift. Product roadmaps will accelerate or stall. Hyperscaler capex disclosures will either validate or complicate the CPU-bound thesis. Investors who build positions around the structural shift rather than the specific 185% figure will be better positioned to hold through the forecast uncertainty that runs to 2030.

Semiconductor supercycle indicators from the May 2026 rally, including Intel reaching a 26-year all-time high and Bank of America projecting $975 billion in global chip sales for 2026, suggest the market has already begun pricing a structural CPU renaissance, which raises the practical question of how much of the agentic CPU upside is already reflected in current valuations before Citi’s terminal figures are confirmed.

This article is for informational purposes only and should not be considered financial advice. Investors should conduct their own research and consult with financial professionals before making investment decisions. Financial projections referenced in this article are subject to market conditions and various risk factors. Past performance does not guarantee future results.