- Approved Full Article:According to market data, Microsoft, Alphabet, Amazon, and Meta Platforms currently command a combined valuation exceeding $10 trillion. According to index data, they account for roughly 17% of the S&P 500 index, meaning their performance dictates the trajectory of institutional portfolios globally. Their late April 2026 reporting disclosures arrive at a defining moment for broad market stability.

The four technology hyperscalers are committing an estimated $650 billion to artificial intelligence infrastructure this year alone. As these corporate budgets stretch to accommodate historic hardware procurement, derivatives markets are forecasting notable post-earnings share price adjustments.

A thorough tech earnings analysis provides investors with a necessary framework to evaluate whether current options pricing accurately captures the true volatility risks. Market participants must assess if the derivative premiums adequately reflect the fundamental pressures associated with massive capital expenditures and heavily leveraged semiconductor supply chains.

Deciphering Implied Volatility in Megacap Technology Derivatives

Options markets establish a quantitative baseline of market expectations leading into corporate disclosures. As of late April 2026, derivatives trading implies specific post-earnings moves for the major technology hyperscalers.

The current megacap tech stock volatility fundamentally reshapes traditional index dynamics, turning broad market exposure into a highly concentrated thematic bet on artificial intelligence.

Pricing data indicates traders are anticipating a share price adjustment of 7.4% for Meta Platforms and 6.7% for Microsoft. Expectations for Amazon sit at a 6.5% implied move, while Alphabet displays the lowest anticipated volatility at 5.6%.

These current derivative pricing expectations present a compelling contrast when measured against historical baseline averages. According to historical data, over the prior twelve reporting cycles, Amazon has averaged a 6.0% post-earnings move, whereas Meta has historically averaged an 8.4% swing. According to market data, the broader market benchmark has seen an overarching 100% expansion since the October 2022 cycle commenced, fundamentally raising the valuation floor for these equities.

Understanding the gap between expected and historical volatility allows investors to identify whether option premiums are currently cheap or expensive. If current pricing underestimates the historical baselines, market participants may be exhibiting unwarranted complacency regarding the upcoming disclosures. Underpricing historical volatility leaves equity holders highly vulnerable to abrupt downside corrections if financial results deviate from consensus.

This pricing dynamic enables more precise hedging strategies ahead of imminent corporate disclosures. Institutional investors closely monitor these implied moves to construct portfolios that can absorb sudden valuation shifts without forcing liquidation.

| Company | Options-Implied Move (April 2026) | 12-Quarter Historical Average |

|---|---|---|

| Meta Platforms | 7.4% | 8.4% |

| Microsoft | 6.7% | N/A |

| Amazon | 6.5% | 6.0% |

| Alphabet | 5.6% | N/A |

When big ASX news breaks, our subscribers know first

The Mechanics of Artificial Intelligence Capital Expenditure

The relationship between historic capital expenditure and stock valuation sits at the centre of the current reporting cycle. Hyperscaler capital expenditure refers to the money allocated to build, upgrade, and maintain the physical computing infrastructure required to process complex data.

For artificial intelligence, this expenditure extends far beyond traditional servers. Companies must construct massive data centres, secure specialised processing chips, and install advanced liquid cooling systems to manage the extreme heat generated by continuous computational workloads.

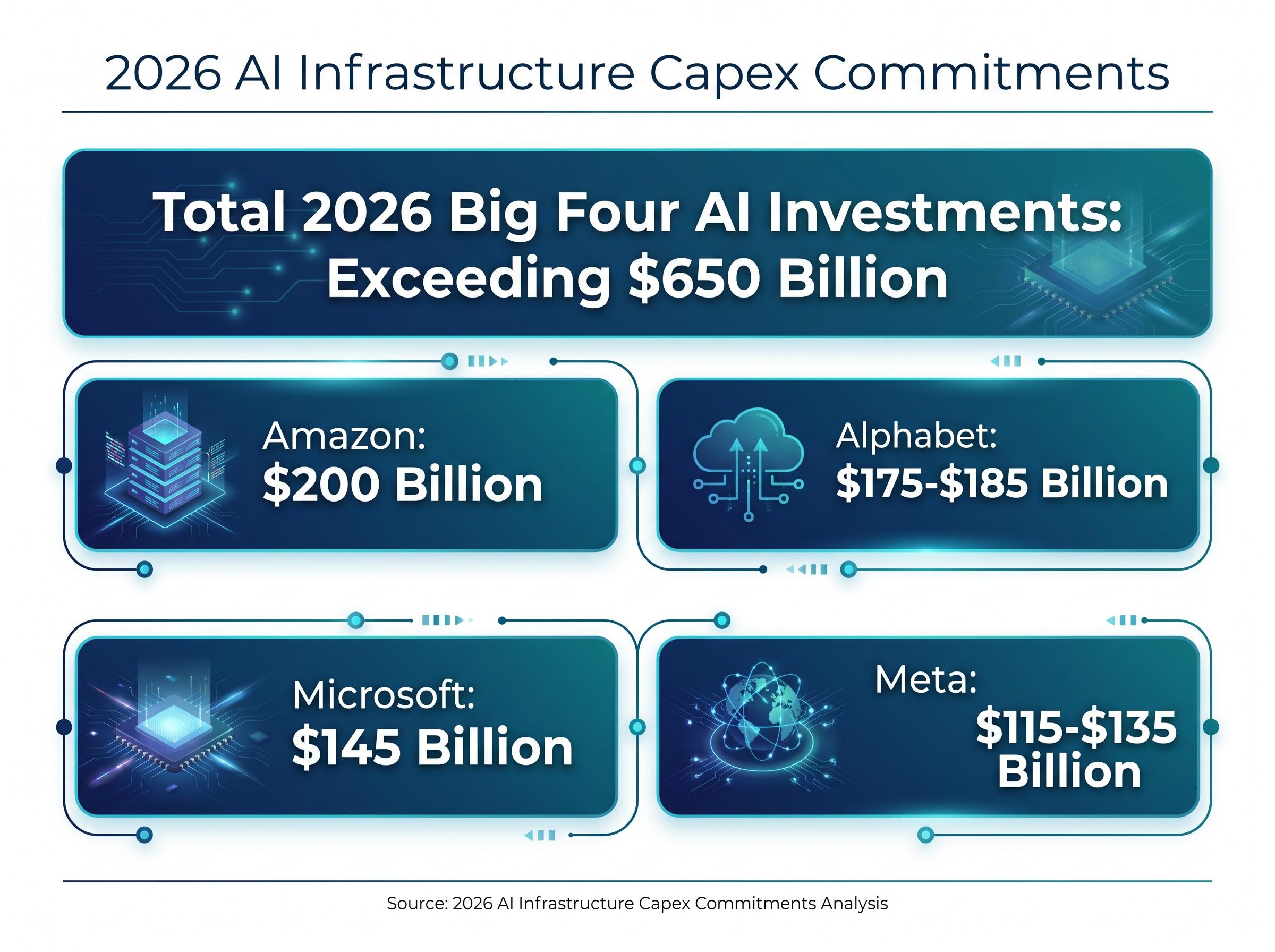

The scale of this infrastructure build-out has accelerated at an unprecedented rate. Industry consensus confirms the Big Four hyperscalers are on track for combined artificial intelligence investments exceeding $650 billion in 2026.

Recent Goldman Sachs forecasts project that this infrastructure boom could push total capital commitments to nearly $700 billion, cementing these technology conglomerates as the dominant concentration risk within the broader equity market.

Amazon is directing $200 billion toward infrastructure, representing a 50% year-over-year increase allocated mostly to AWS to support surging workloads. Alphabet has committed $175-$185 billion, directed heavily toward Gemini AI, Vertex AI, and Google Cloud infrastructure. Microsoft maintains a $145 billion run-rate to scale Azure computing, support its OpenAI partnership, and expand Copilot tools. Meta is investing $115-$135 billion to advance Llama model development and fortify its artificial intelligence-driven advertising systems.

Cash Flow Pressures and Investor Timelines

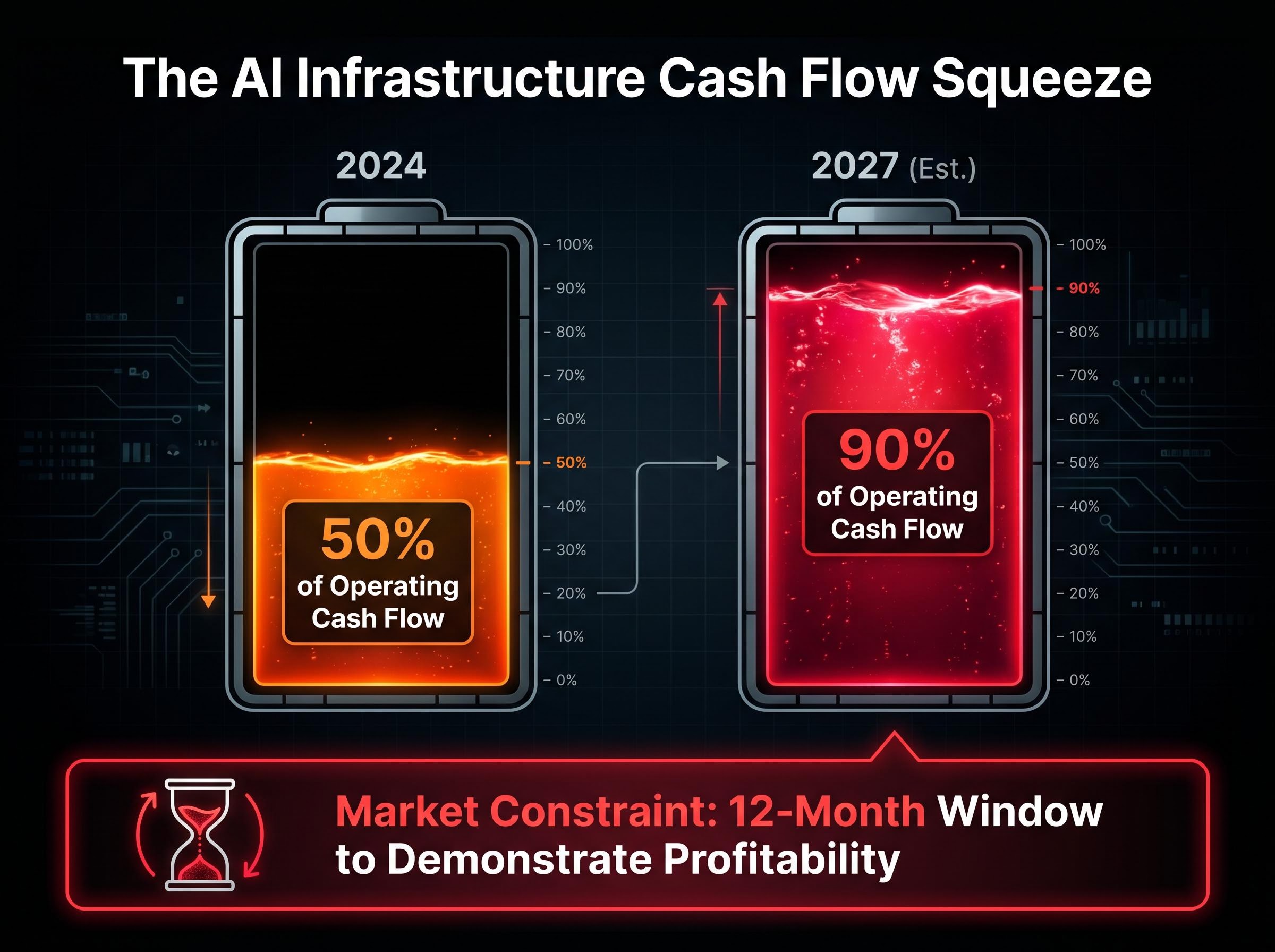

The financial burden of this continuous infrastructure procurement is drastically altering corporate balance sheets. According to industry estimates, market projections suggest infrastructure expenditures will jump from consuming 50% of hyperscaler operating cash flow in 2024 to an estimated 90% by 2027.

This trajectory severely restricts the timeframe technology conglomerates have to prove these build-outs are yielding actual top-line growth. The transition from abstract expenditure figures into concrete operating costs means investors must soon see a tangible return on investment.

According to industry reports, market strategists believe these companies face a strict 12-month window to demonstrate infrastructure profitability. This foundational constraint clarifies why the market is intensely scrutinising corporate balance sheets, as the timeline directly informs portfolio risk management.

Supply Chain Ripple Effects on Semiconductor Valuations

Massive downstream spending by technology giants creates amplified, leveraged volatility across the entire hardware ecosystem. Aggressive hardware procurement by the hyperscalers has catalysed record momentum for semiconductor manufacturers.

This dynamic establishes a direct correlation between hyperscaler earnings guidance and immediate pricing reactions across artificial intelligence equity ecosystems. In early 2026, the Philadelphia SE Semiconductor Index (SOX) surged to record highs, increasing 39% during a historic 16-day rally.

Sustained demand for processing chips has transformed these supply chain dependencies into high-beta investment vehicles. According to market data, a curated portfolio of fifty artificial intelligence-focused equities advanced by 27.2% between late March and late April 2026, highlighting the concentration of capital moving into hardware suppliers.

However, this concentrated momentum also exposes recent sector vulnerabilities. Hardware suppliers face outsized drawdowns if the major technology firms miss their user acquisition or income objectives.

Industry Revenue Projections Semiconductor sector revenue is projected to grow by 57% year-over-year in 2026, according to industry supply chain data, driven entirely by sustained hyperscaler demand.

The semiconductor ecosystem heavily relies on major industry players to fabricate and design these complex components. If cloud providers signal a deceleration in data centre expansion, the manufacturers carrying inventory for these projected orders will absorb the immediate financial shock.

Any reduction in hyperscaler infrastructure budgeting will pass directly to the manufacturers, potentially unwinding the recent sector rallies. Investors learn to look beyond the immediate earnings of consumer-facing technology firms, as these supply chain dependencies offer critical warning signals for the broader market.

Investors exploring the secondary impacts of hyperscaler budgets will find our detailed coverage of semiconductor stock valuations useful, as it breaks down the specific multi-year timelines required to transition initial hardware orders into sustainable cloud monetization.

Identifying Mispriced Risks in the Intelligence Supercycle

A significant gap remains between derivative market complacency and the fundamental challenges of value creation in the current cycle. There is intense broader market scrutiny regarding squeezed cash flows versus the immediate return on investment from these infrastructure builds.

Companies must deliver specific, measurable commercial targets to justify the elevated valuations of major cloud providers. Microsoft demonstrated this baseline by reporting Azure cloud computing growth of 33% year-over-year in Q3 FY25, noting that artificial intelligence services contributed 16 points to that expansion. The software provider is actively working toward a $25 billion artificial intelligence revenue target by the end of FY26.

The official Q3 financial disclosures from Microsoft validate this specific cloud revenue attribution, offering a clear blueprint for how hyperscalers must transparently report the commercial impact of their infrastructure investments.

Despite these early indicators, analyst perspectives highlight growing commercial friction. Gartner analyst Ewan McIntyre emphasises the broader value creation challenges inherent in this intelligence supercycle, noting the market is actively questioning how quickly historic infrastructure spending must translate into sustainable profitability to avoid a broader equity correction.

Investors should track specific performance indicators during corporate disclosures to validate their investment thesis:

- Cloud growth attribution: The exact percentage of server revenue directly tied to new artificial intelligence workloads rather than legacy migrations.

- Digital ad revenue expansion: Evidence that integrated machine learning models are demonstrably increasing advertiser return on spend.

- Forward capital expenditure guidance: Any downward revisions in future infrastructure spending plans that might signal market saturation.

- Operating margin trajectories: The impact of elevated server depreciation costs on overall corporate profitability.

Strategic Positioning for the 2026 Technology Reporting Cycle

A distinct tension exists between massive 2026 capital expenditures and the relatively subdued options-implied volatility. If hyperscalers fail to demonstrate immediate cloud and advertising revenue growth, current option premiums may prove significantly underpriced.

Any reduction in infrastructure budgeting by industry leaders will likely trigger immediate downward pricing reactions across the entire semiconductor supply chain. The hardware manufacturers that benefited from the aggressive early 2026 procurement rallies remain highly vulnerable to deferred hyperscaler spending.

Maintaining disciplined portfolio allocations during the late April reporting schedule requires looking past top-line earnings beats to scrutinise underlying cash flow projections. Investors must carefully evaluate whether the anticipated commercial returns justify the sustained infrastructure costs required to compete in the sector.

This article is for informational purposes only and should not be considered financial advice. Investors should conduct their own research and consult with financial professionals before making investment decisions. Past performance does not guarantee future results. Financial projections are subject to market conditions and various risk factors.