What Blackstone’s AI Restructure Reveals About Its $1.3T Strategy

18 mins ago

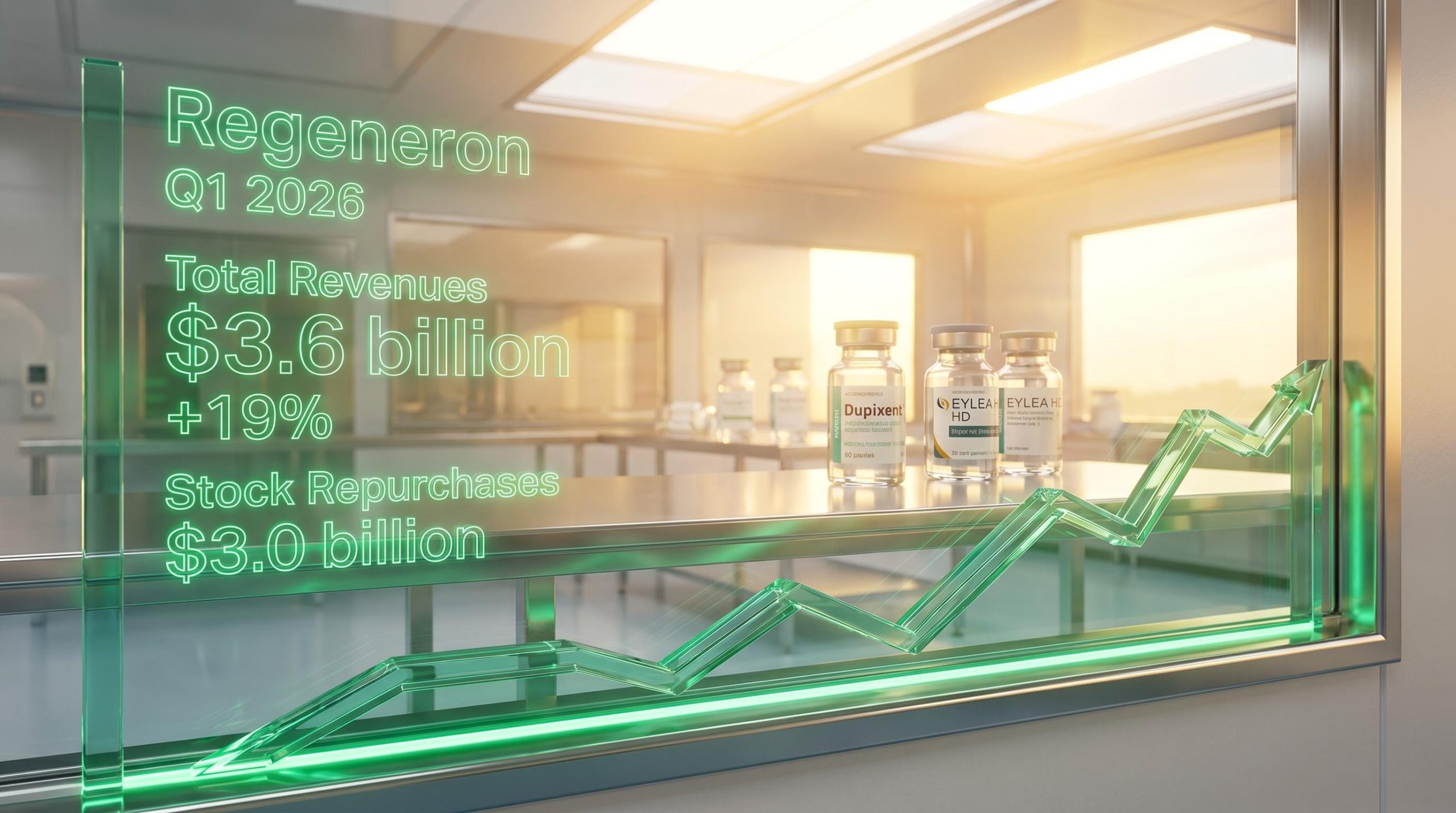

Regeneron reported its first-quarter financials on 29 April 2026, beating Wall Street estimates and announcing an unexpected $3.0 billion stock repurchase programme. The Regeneron earnings announcement arrives at an important juncture for the biotechnology firm. The company is actively navigating intense US market competition and managing a major product transition phase.

The market immediately absorbed the implications of the top-line beat. Investors have closely monitored the company’s cash generation capabilities amid increasing competition. By authorising this capital return strategy, management signaled strong internal confidence in their forward trajectory.

What follows is a comprehensive breakdown of the first-quarter financials, underlying product performance metrics, and the specific impact of an international manufacturing disruption on the company’s annual profitability.

The sheer scale of the financial beat established an immediate narrative of corporate health. Total revenues reached $3.6 billion, representing a 19% year-over-year increase that comfortably exceeded consensus projections. Non-GAAP earnings per share climbed 15% to $9.47, outperforming estimates.

The official SEC Form 10-Q provides the foundational regulatory data for these quarterly figures, detailing the precise calculations behind both the top-line revenue and the adjusted earnings metrics.

Management reinforced this financial momentum through aggressive capital return initiatives. The company executed $803 million in first-quarter stock repurchases and authorised a new $3.0 billion buyback programme in April 2026. This large authorisation serves as a direct internal endorsement of the company’s valuation and forward cash flow projections.

The gap between non-GAAP and GAAP figures requires specific attention. The company recorded a $102 million In-Process Research and Development charge tied to recent equity and collaboration deals. This specific charge reduced GAAP EPS by exactly $0.82, bringing the official GAAP net income figure down 10% to $727 million.

| Financial Metric | Q1 2026 Actual | Wall Street Estimate | Year-Over-Year Change |

|---|---|---|---|

| Total Revenues | $3.6 billion | N/A | +19% |

| Non-GAAP EPS | $9.47 | N/A | +15% |

| GAAP EPS | $6.75 | N/A | -7% |

| Stock Repurchases | $803 million | N/A | N/A |

Top-line revenue only tells part of the story. The underlying product data reveals a deliberate tug-of-war between legacy therapies and new high-growth formulations. The company’s transition strategy is yielding tangible results despite mounting competitive pressures.

The successful market uptake of the newer high-dose formulation represents a major defensive victory. US biopharma experts view this product transition highly positively. The data shows clear growth trajectories across the core portfolio.

Dupixent global sales reached $4.9 billion, representing a 33% year-over-year increase. EYLEA HD US net sales surged 52% to $468 million. Legacy EYLEA total US sales declined 10% to $941 million. Libtayo global sales hit $438 million, marking a 54% increase.

Top-line numbers are heavily supported by these specific growth engines. The managed decline of the legacy vision portfolio is proceeding exactly as management modeled.

While major players defend their blockbusters against generics, smaller biotechnology firms often target orphan blinding eye diseases where no approved treatments currently exist, creating entirely new uncontested markets.

Retail investors must understand the mechanics of patent cliffs to properly evaluate this quarter’s numbers. When a legacy drug loses patent protection, competitors introduce biosimilars that capture market share through aggressive discounting. This biosimilar rivalry directly forced a drop in specific traditional formulation earnings.

To defend its market position, the company secured Food and Drug Administration (FDA) approval for an extended-dosing formulation. Based on the PULSAR and PHOTON clinical trials, the new therapy allows for dosing intervals of up to 20 weeks. This extended schedule makes the newer treatment highly attractive to both patients and physicians, reducing the clinical burden.

The FDA approval for EYLEA HD validates the clinical efficacy demonstrated in these late-stage trials, cementing the treatment as the only injectable anti-VEGF option capable of maintaining such prolonged maintenance schedules.

This shift means the company is intentionally cannibalising its own legacy sales. Transitioning patients to the new formulation before competitors can capture them is a deliberate corporate strategy. It is a commercial necessity to protect long-term revenue streams from generic erosion.

The quarterly print was not entirely flawless. A mechanical failure at the company’s international manufacturing plant translated directly into a tightened margin outlook. This unexpected production halt at the Limerick, Ireland facility required immediate, unanticipated repairs.

The disruption caused operational costs to spike significantly. Cost of Goods Sold rose 40% to $373 million, pushing the gross margin on product sales down to 76% from 81% the previous year. Consequently, management lowered full-year 2026 GAAP gross margin guidance to 77-78%, down from the previous 79-80% projection.

To mitigate similar single-source vulnerabilities during critical phases, many pharmaceutical companies establish alternate commercial supplier arrangements that can meaningfully reduce the cost of goods sold and protect gross margins.

Despite the financial hit, the supply chain held firm.

Management Commentary “While the temporary interruption at our Limerick facility negatively impacted GAAP gross margins this quarter, operations have resumed and the disruption caused zero impact on actual product availability for patients.”

Understanding exactly why margins are compressing allows investors to judge the situation accurately. The data indicates this is a temporary facility issue rather than a structural flaw in the underlying business.

Markets operate as forward-looking mechanisms. Looking beyond the immediate quarterly noise reveals a company aggressively funding its next growth phase. Internal R&D investment increased 16% to $1.544 billion, supporting a pipeline of over 50 experimental therapeutics.

Beyond internal development, the company is expanding into radiopharmaceutical partnerships that provide strategic optionality across multiple solid tumour programmes, reducing reliance on traditional biologics.

Recent regulatory victories have expanded the addressable market for existing drugs. The FDA and European Commission secured new approvals for Dupixent expansions. Additionally, regulators granted accelerated approval for the Otarmeni gene therapy.

The company also announced that the Biologics License Application for garetosmab was accepted. This places the FDA action date firmly in August 2026.

Several major Phase 3 trial advancements are expected to materialise later this year. Phase 3 results for the fianlimab and cemiplimab combination therapy in metastatic melanoma are on track for the second quarter of 2026.

The company is also broadening its late-stage clinical targets. New Phase 3 trials have been initiated evaluating mibavademab for monogenic obesity. Separate trials are now assessing a new compound for thrombosis and stroke prevention.

Wall Street reacted positively to the earnings disclosure. The stock opened at $751.37 on 29 April 2026. Intraday trading showed steady volume as the market digested the news.

Heading into the print, analysts maintained a bullish stance. Piper Sandler initiated coverage with an Overweight rating, while Raymond James reiterated an Outperform rating. Both firms highlighted the successful transition to the high-dose vision care formulation as a key valuation driver.

The aggressive capital return strategy appears to have successfully balanced the temporary manufacturing headwinds. By repurchasing shares at current levels, management has signaled that the long-term pipeline value far outweighs near-term margin compression.

For investors wanting to explore the underlying cost dynamics, our detailed coverage of Regeneron’s first-quarter profitability unpacks the specific gross product margin declines and how the ongoing Dupixent joint venture continues to support the broader balance sheet.

This article is for informational purposes only and should not be considered financial advice. Investors should conduct their own research and consult with financial professionals before making investment decisions. Past performance does not guarantee future results. Financial projections and forward-looking statements are speculative and subject to market conditions and company performance.

Regeneron reported Q1 2026 revenues of $3.6 billion, a 19% year-over-year increase, and non-GAAP earnings per share of $9.47, exceeding Wall Street estimates. The company also authorized a new $3.0 billion stock repurchase program.

Regeneron is successfully transitioning patients from its legacy EYLEA to the newer EYLEA HD formulation, which offers extended dosing intervals and better protects market share against biosimilar competition. EYLEA HD US net sales increased 52% while legacy EYLEA sales declined 10%.

A mechanical failure at Regeneron's Limerick facility caused a 40% increase in Cost of Goods Sold, leading to a temporary decline in gross margin on product sales and a lowered full-year 2026 gross margin guidance. However, product availability was unaffected.

Regeneron is aggressively funding over 50 experimental therapeutics, with key catalysts including late-stage clinical trial results for fianlimab and cemiplimab in Q2 2026, new Phase 3 trials for mibavademab, and an FDA action date for garetosmab in August 2026.