At 2:30 pm AEST on Monday 16 June 2026, the Reserve Bank of Australia will almost certainly leave the cash rate unchanged at 4.35%. Markets already know this. ASX 30-day interbank cash rate futures imply approximately 0% probability of a move. The RBA rate decision itself is not the event. The event is what Governor Michele Bullock says afterwards, and how she frames a pause that sits between inflation still running at 4.2% and an unemployment rate that just hit a four-year high. That framing will determine whether bond yields firm or ease, whether the Australian dollar finds support or softens, and whether rate-sensitive equities face another day of pressure or catch a reprieve. What follows is a guide to the specific language signals investors should monitor tomorrow, the two scenarios those signals map to, and what each means for the RBA’s implied path toward 4.7% by end-2026.

Why a rate hold carries more information than the number itself

The rate announcement will land and, within seconds, be set aside. A hold at 4.35% is already fully discounted. The decision carries no information the market has not already absorbed.

The information arrives in the minutes that follow: in the written statement, in the press conference, in the specific adjectives Bullock attaches to inflation and the specific verbs she uses to describe the Board’s posture. That language will shift terminal rate pricing by as much as 25 basis points on the futures curve, a move with real consequences for borrowers, bond portfolios, and equity valuations, all without the cash rate changing by a single basis point.

A rate hold is not a neutral event when the forward guidance attached to it can shift terminal rate pricing by 25 basis points.

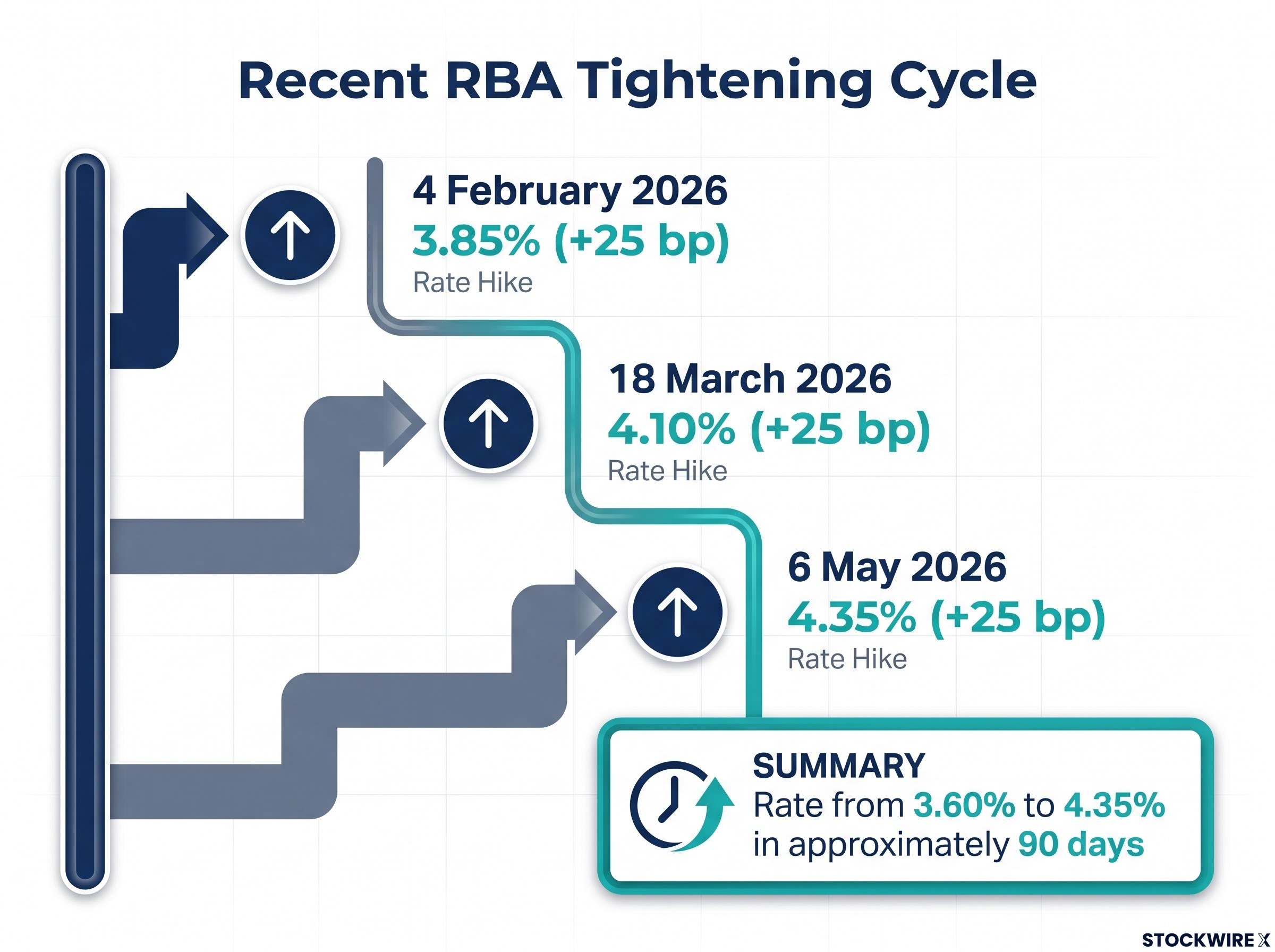

The context behind the pause matters. The RBA lifted rates three times in three months:

- 4 February 2026: Cash rate to 3.85% (+25 bp)

- 18 March 2026: Cash rate to 4.10% (+25 bp)

- 6 May 2026: Cash rate to 4.35% (+25 bp)

That sequence took the rate from 3.60% to 4.35% in approximately 90 days. June’s pause is tactical, not directional. The only question worth asking tomorrow is whether Bullock confirms that the tightening cycle still has further to run, or signals the Board is now inclined to sit and watch.

The Board’s decision to pause follows its third consecutive hike to 4.35%, a sequence in which eight of nine members voted for the May move, with the single dissent already signalling that the threshold between hiking and holding had narrowed considerably before June arrived.

When big ASX news breaks, our subscribers know first

Why the RBA is pausing now, and why it does not mean the job is done

Two data sets are pulling the RBA in opposite directions. Neither has won the argument, and the tension between them is the reason a pause makes sense without meaning the cycle is over.

Inflation still demands attention

April 2026 headline CPI sits at 4.2%, well above the RBA’s 2-3% target band. The May 2026 Statement on Monetary Policy projects trimmed mean inflation peaking near 3.8% in Q2 2026, with headline CPI still at 4.0% as late as December 2026. The RBA’s own projections do not show trimmed mean inflation returning to the 2.5% midpoint until 2027-2028.

The trimmed mean moving higher in April 2026, from 3.3% to 3.4%, is the data point the RBA will weigh most carefully, because it signals that underlying inflation is not retreating even as the headline CPI number appears to improve on fuel base effects.

Structural factors, particularly energy costs feeding through into goods and services prices, are contributing to the persistence. Rate hikes are a blunt instrument against supply-driven inflation, but they remain the RBA’s primary tool for anchoring expectations.

The labour market has changed the calculus

The April 2026 ABS Labour Force data, released on 21 May 2026, reported unemployment rising to 4.5%, up from 4.3% and its highest reading in over four years. Employment fell by 18,600 persons in the month.

The ABS Labour Force Survey is the primary source for Australian employment and unemployment statistics, and the April 2026 release placed unemployment at 4.5%, a reading that already exceeded the RBA’s own December 2026 projection by 20 basis points.

That unemployment figure already exceeds the RBA’s own December 2026 projection of 4.3%, meaning the labour market is weakening faster than the central bank anticipated just weeks ago. The RBA is also making this decision with one lagged data point; the next ABS Labour Force release is not due until 25 June 2026, nine days after the rate announcement.

| Signal | Inflation indicators | Labour market indicators |

|---|---|---|

| Latest reading | CPI at 4.2% (April 2026) | Unemployment at 4.5% (April 2026) |

| RBA forecast | CPI at 4.0% by December 2026 | Unemployment at 4.3% by December 2026 |

| Policy implication | Argues for maintaining tightening bias | Argues for pausing to assess transmission effects |

These conditions do not cancel each other out. They create a genuine policy dilemma. The RBA is pausing because the data is conflicted, not because it has won the inflation fight.

How to read central bank forward guidance as a retail investor

The rate decision moves markets once. Forward guidance, the language a central bank uses to shape expectations about where rates are heading, moves markets continuously between meetings. It is the mechanism through which monetary policy does most of its work, repricing bonds, currencies, and borrowing costs in real time based on what investors believe the next move will be.

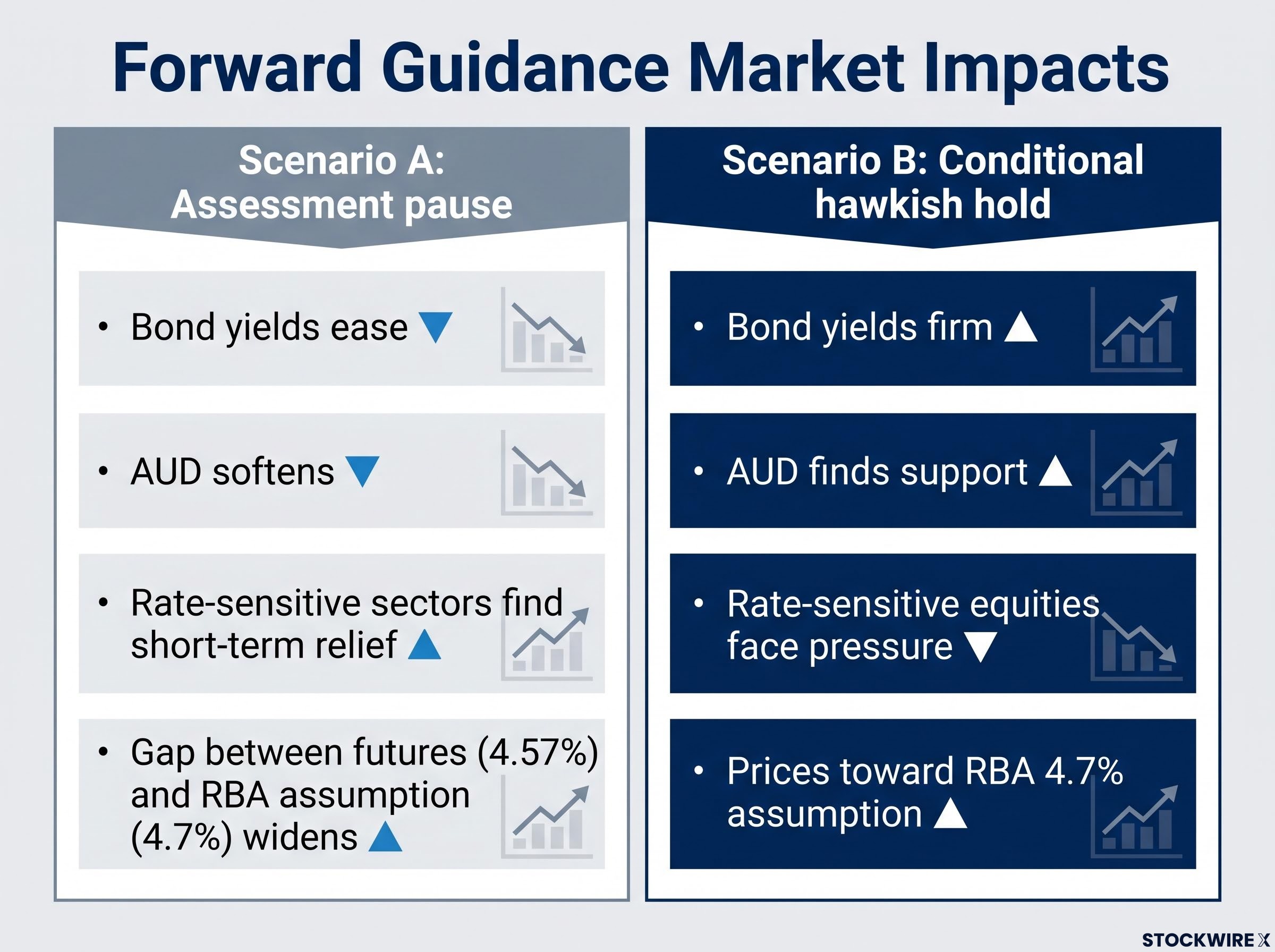

For tomorrow’s announcement, the distinction that matters is between two framings, both of which describe a hold at 4.35% but imply materially different rate paths:

- Assessment pause (Scenario A): The hold is about watching how the prior three hikes transmit through the economy. The hurdle for another hike has risen. Language emphasises lagged effects, data dependence, and acknowledgment of labour market softness.

- Conditional hawkish hold (Scenario B): The hold is about timing, not direction. The tightening bias remains explicitly intact, and the Board is ready to move again if inflation does not track back toward target. Language emphasises conditionality and inflation persistence.

After the May meeting, the RBA stated it was “well placed to respond to developments,” a phrase that signalled increased data dependence without abandoning the tightening bias.

The RBA’s own conditioning assumptions show the cash rate reaching approximately 4.7% by end-2026, consistent with at least one additional 25 basis point hike. ASX futures imply a rate near 4.57% by February 2027. How Bullock positions tomorrow’s hold relative to those expectations is what will determine whether markets reprice up or down.

The specific words that will tell you which scenario is playing out

The following table maps specific language signals to the scenario they imply and the rate path consequence. Investors can use this as a reference tool while following the 2:30 pm AEST statement and the subsequent press conference.

| Language signal | Scenario implied | What it means for the rate path |

|---|---|---|

| “Assess the impact of previous rate increases” | A (Assessment pause) | Hurdle for next hike has risen; hold likely extends |

| “Allow time for transmission to the economy” | A (Assessment pause) | Board waiting for lagged effects to appear in data |

| Unemployment cited as warranting “caution” or “balance” | A (Assessment pause) | Labour market softness is influencing policy posture |

| “The Board stands ready to tighten further if needed” | B (Conditional hawkish hold) | Tightening bias intact; one more hike remains live |

| Inflation described as “unacceptably high” or “more persistent than previously expected” | B (Conditional hawkish hold) | Board framing inflation as the dominant risk |

| Reference to second-round effects from energy prices | B (Conditional hawkish hold) | Structural inflation concerns keeping hawkish bias visible |

The single most telling dimension is how Bullock characterises inflation risk. If inflation is described as “easing as expected,” markets will read the statement as a genuine shift toward patience. If it is characterised as “more persistent than previously expected” or linked to second-round effects, the tightening bias is intact regardless of any softer language elsewhere.

Global context references also carry weight. Discussion of global headwinds provides cover for a longer domestic pause. Emphasis on global inflation persistence supports keeping the hawkish posture visible.

Global central bank divergence widened sharply around the May meeting, with the RBA raising to 4.35% while the Fed, ECB, and Bank of England all held, creating a rate differential of up to 235 basis points that continues to shape the AUD’s sensitivity to any shift in Bullock’s forward guidance tomorrow.

What each scenario means for your portfolio tomorrow

Because a hold is fully priced, the market reaction will be driven entirely by marginal repricing of the terminal rate expectation. The ASX futures curve currently implies a rate near 4.57% by February 2027, while the RBA’s own conditioning assumption sits at approximately 4.7% by end-2026. The gap between those two numbers is where tomorrow’s price action lives.

If Bullock signals the tightening bias is intact (Scenario B)

- Bond yields firm as markets reprice toward the RBA’s 4.7% conditioning assumption; duration underperforms

- AUD finds support on higher-for-longer rate expectations

- Rate-sensitive equities face pressure, particularly REITs, high-dividend defensives, and highly leveraged names

- Rate-cut pricing is pushed further out on the futures curve

Rate-sensitive sector losses can concentrate quickly when yield repricing accelerates: in the 20 May 2026 session, gold miners fell 5-6% in individual names and ASX 300 breadth showed 239 decliners against 42 advancers, illustrating how a single external yield shock can amplify into broad-based selling when domestic rates are already elevated.

If the tone is more cautious and data-dependent (Scenario A)

- Bond yields ease modestly, supporting a rally in duration

- AUD softens as markets bring forward the probability of a longer hold or an earlier start to cuts

- Rate-sensitive sectors find short-term relief as terminal rate expectations recede

- The gap between futures pricing (4.57%) and the RBA conditioning assumption (4.7%) widens, implying markets see the tightening cycle as closer to done

Forward guidance shifts create real same-day price movements even when the rate decision is unchanged. Knowing the directional implications in advance allows investors to respond with intention rather than react to headlines.

What Bullock’s language will confirm about the cycle by end of day

The hold at 4.35% will be announced and immediately filed as non-news. What remains after that headline fades is the durable signal: whether Bullock positions June as a conditional pause within an unfinished tightening cycle, or as a genuine inflection point toward a longer hold.

Neither scenario resolves the RBA’s core tension cleanly. The Board must acknowledge real economic softness without letting inflation expectations drift. How it threads that needle in real time, in specific word choices and specific emphasis, is the only thing that matters tomorrow.

The RBA’s own projections show trimmed mean inflation not returning to the 2.5% midpoint until 2027-2028. That timeline means the pause is tactical by definition, regardless of the tone Bullock adopts.

The investor who treats 16 June as a language event rather than a rate event is positioned to act on the signal while others are still waiting for the number. Read the statement language first. Listen to the press conference tone second. Score what you are hearing against the watchlist above before the market’s consensus interpretation forms around you.

This article is for informational purposes only and should not be considered financial advice. Investors should conduct their own research and consult with financial professionals before making investment decisions. Forward-looking statements regarding the RBA’s rate path are speculative and subject to change based on incoming economic data and Board deliberations.