Finfluencer Rules Won’t Work Until the Penalty Beats the Profit

2 hrs ago

Pro Medicus has shed more than half its value from its 2025 highs, yet the trailing price-to-earnings ratio still sits at approximately 55-58x. For retail investors watching the ASX’s most scrutinised growth stock, that combination raises an immediate question: is this a discount or a trap? The pullback brings the Pro Medicus share price to valuation territory it has not occupied in years, and it coincides with a string of significant North American contract wins through April and May 2026. The tension between a compressed (but still elevated) multiple and accelerating contract momentum is precisely what makes this a live investment decision. What follows is a structured assessment of whether the current price represents a genuine re-entry point, using the company’s own financials, recent contract data, the competitive environment, and a valuation framework designed to help investors reach their own conclusions.

The scale of the repricing is worth sitting with. Pro Medicus traded as high as A$336 over the past 52 weeks. As of 15 May 2026, the stock changed hands at A$122.11, an intraday range of A$121.22 to A$123.38. That represents a decline of roughly 44-58% depending on the reference point.

Valuation snapshot: Pro Medicus’s trailing P/E has compressed from above 100x at earlier peaks, through the high-70s to low-80s as recently as March 2026, to approximately 55-58x today.

The multiple contraction is real. It is also relative. A trailing P/E of 55-58x remains historically elevated for an ASX-listed company by any standard measure.

“Cheaper than before” and “cheap” are not the same thing. That distinction runs through every section of this analysis.

For investors wanting to track how broker consensus has evolved through the decline, our full explainer on PME valuation de-rating covers the May 2026 analyst price target range, the zero-sell-rating broker consensus, and the specific AI disruption fears that triggered multiple compression without any corresponding change in earnings forecasts.

A falling share price only creates a buying opportunity if the business behind it remains sound. Pro Medicus’s most recent confirmed full-year results, for FY25 (the year ended 30 June 2025), provide the baseline.

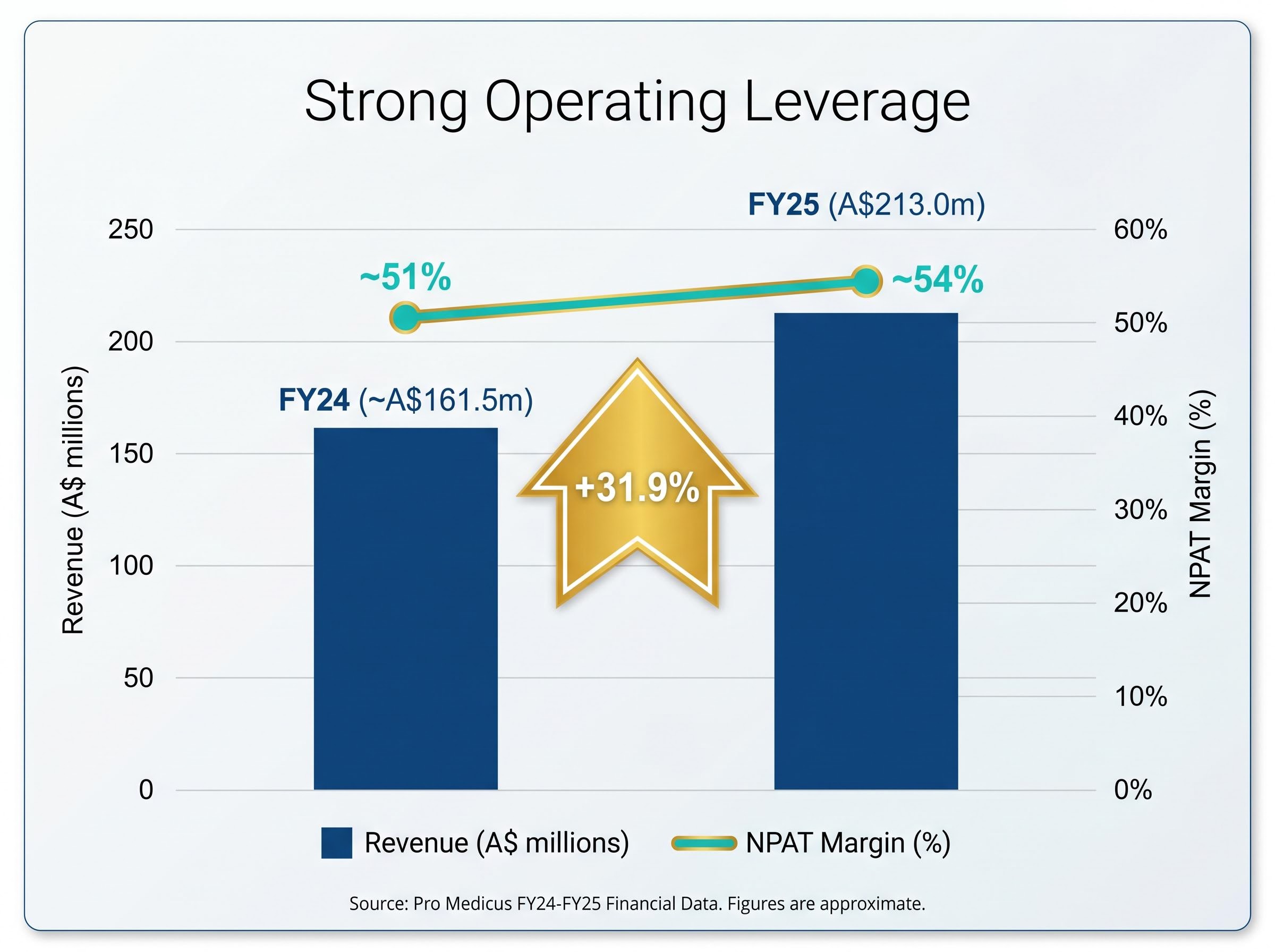

Revenue came in at A$213.0 million, up 31.9% year-on-year. Net profit after tax (NPAT) reached A$115.2 million, up 39.2%. Both figures confirm the company is growing revenue and profit at above-30% rates, a pace that places it among the fastest-growing technology companies on the ASX.

| Metric | FY24 | FY25 | Change |

|---|---|---|---|

| Revenue | ~A$161.5m | A$213.0m | +31.9% |

| NPAT | ~A$82.8m | A$115.2m | +39.2% |

| NPAT Margin | ~51% | ~54% | +3 ppts |

The pullback, then, is a valuation compression story rather than a deterioration story. That is a distinction worth making explicit.

A 54% NPAT margin means that for every dollar of revenue Pro Medicus earns, it keeps 54 cents as profit after tax. That figure expanded from approximately 51% in FY24, evidence of operating leverage as the platform scales rather than revenue growth alone.

High margins matter particularly for a stock trading at an elevated P/E. They reduce the earnings risk that typically punishes expensive stocks when costs blow out. A capital-light, high-margin business model is the core reason the market has historically been willing to pay a premium multiple for Pro Medicus, and the FY25 results confirm that model remains intact.

The share price has been falling. The contract announcements have not stopped.

On approximately 8 April 2026, Pro Medicus announced a A$23 million, five-year deal with the University of Maryland Medical System for its Visage 7 Enterprise Imaging platform. Five days later, on approximately 13 April 2026, a A$37 million, five-year renewal with Northwestern Medicine followed. Together, those two wins represent more than A$60 million in contracted revenue in a single month.

A further contract with Beth Israel Lahey Health, referenced as A$90 million over seven years and announced on 18 May 2026, has been reported but should be verified directly via the ASX announcement before being relied upon for investment decisions.

The Northwestern Medicine deal is particularly relevant to the competitive risk assessment: it demonstrates pricing power on renewal, with higher per-transaction fees and increased minimum volume commitments negotiated at contract extension rather than conceded, which is the opposite of what margin compression from competitive pressure would look like.

| Client | Value | Term | Platform | Announced |

|---|---|---|---|---|

| University of Maryland Medical System | A$23m | 5 years | Visage 7 | ~8 April 2026 |

| Northwestern Medicine | A$37m | 5 years | Visage 7 | ~13 April 2026 |

| Beth Israel Lahey Health | A$90m* | 7 years | Visage 7 | 18 May 2026 |

*Readers should verify this contract via the ASX announcement directly.

CEO Dr Sam Hupert has characterised the cloud-hosted platform as increasingly becoming the benchmark in North American healthcare IT, with the pipeline described as strong across all market segments including Europe and ANZ.

Multi-year contract structures provide the earnings visibility that subscription-style software businesses are valued on. A run of large wins in the months following a share price decline materially strengthens the bull case for investors considering entry.

A P/E ratio of 55-58x can look alarming in isolation. What it actually encodes is the market’s expectation of future earnings growth, not a reflection of current earnings alone. When investors pay 55x trailing earnings, they are betting that those earnings will grow rapidly enough over the next several years to bring the effective multiple down to a reasonable level.

The challenge of valuing growth stocks on the ASX is that trailing P/E ratios are structurally backward-looking; a company compounding earnings at 30-40% annually will always look expensive on last year’s numbers, which is precisely why the multiple compresses faster than the headline figure suggests when growth accelerates.

The risk is captured in a phrase that appears repeatedly in broker commentary on Pro Medicus: “priced for perfection.” A high multiple leaves no buffer for execution errors, growth deceleration, or competitive setbacks. The three conditions under which a high-P/E growth stock typically de-rates are:

Damodaran’s PEG ratio framework, which relates a stock’s P/E multiple directly to its expected earnings growth rate, provides a useful lens here: a trailing P/E of 55-58x is arithmetically supportable only if the market expects earnings to compound at rates that bring the effective forward multiple down to a reasonable level within a defined investment horizon.

Morgans noted in 2026 commentary that the premium is partly justified by strong earnings visibility, very high margins, and a deep pipeline, while simultaneously flagging de-rating risk if contract momentum slows.

At 55-58x trailing earnings, the market is embedding an expectation of sustained high growth for multiple years ahead. Even after a 44-58% share price fall, the multiple remains elevated by historical ASX standards. The “discount” is relative rather than absolute.

An investor buying at A$122 is still paying a premium. The investment case rests on Pro Medicus continuing to execute at a high level. That is the trade.

The competitive environment in North American enterprise imaging IT has intensified. GE HealthCare, Philips, Siemens Healthineers, Sectra, and IBM/Change Healthcare are all accelerating cloud and enterprise imaging offerings, increasingly marketing end-to-end platforms that integrate radiology, cardiology, and other specialties under multi-modality deals. This approach could pressure Pro Medicus’s win-rates or pricing in North American requests for proposals.

The procurement environment adds a second layer of risk. US hospital systems face margin pressure from labour costs and reimbursement dynamics, and industry reporting through 2025-2026 describes longer procurement cycles for large enterprise IT projects. Contracts can still be won, but revenue ramp may be delayed.

AHA research on hospital financial pressures published in March 2026 quantifies the scale of this challenge: US hospital expenses grew faster than prices throughout 2025, creating capital allocation stress that directly affects the timeline and appetite for large enterprise IT commitments.

Broker commentary consistently describes Pro Medicus as “priced for perfection,” flagging that even minor earnings disappointments could cause outsized share price declines at these multiples.

A high-quality business with a falling share price can still be a poor investment if the multiple remains demanding and the competitive environment shifts. These risks need to be priced explicitly, not assumed away.

For investors wanting to assess the competitive threat from below as well as from incumbents, our deep-dive into enterprise imaging competition via Mach7’s Flamingo Architecture launch examines how smaller ASX-listed rivals are rebuilding go-to-market strategies targeting the same North American health system segment, in a market forecast to reach US$4.1 billion by 2030.

The bull and bear cases are both grounded in verifiable data. The question is which set of conditions an investor expects to prevail.

| Dimension | Bull Case | Bear Case |

|---|---|---|

| Earnings Growth | +31.9% revenue, +39.2% NPAT in FY25 | Growth must sustain for years to justify 55-58x |

| Margins | ~54% NPAT margin, expanding | Competitive pricing could compress margins |

| Contract Momentum | A$60m+ in verified April 2026 wins | Longer procurement cycles may slow pipeline |

| Valuation | 44-58% pullback from highs | 55-58x trailing P/E remains elevated by ASX standards |

| Competitive Risk | Cloud platform adoption accelerating | GE, Philips, Siemens, Sectra intensifying |

The investment case is not about whether Pro Medicus is a good business. The FY25 results and contract pipeline confirm that it is. The question is whether the current multiple adequately prices the risks alongside the earnings visibility. Investors who work through this framework will have a clearer sense of what conditions need to hold for the stock to justify its current price, and what would need to change to prompt a reassessment.

Pro Medicus has repriced materially. A 44-58% decline from the highs is not a rounding error. But the trailing P/E of 55-58x means the stock is still priced for sustained, high-level execution over multiple years. The two questions that matter most before taking a position: what growth rate does 55-58x embed, and is that rate achievable given the competitive dynamics outlined above?

The answer depends on an investor’s own assessment of sustainable growth rates and risk tolerance. The data presented here is designed to inform that assessment, not to replace it.

This article is for informational purposes only and should not be considered financial advice. Investors should conduct their own research and consult with financial professionals before making investment decisions. Past performance does not guarantee future results. Financial projections are subject to market conditions and various risk factors.

A trailing P/E ratio measures a company's share price relative to its earnings over the past 12 months, indicating how much investors are paying per dollar of profit. For Pro Medicus, a trailing P/E of 55-58x means investors are paying a significant premium, reflecting expectations of sustained high earnings growth rather than current profitability alone.

Pro Medicus traded as high as A$336 over the past 52 weeks and was changing hands at A$122.11 as of 15 May 2026, representing a decline of approximately 44-58% depending on the reference point used.

Pro Medicus announced a A$23 million five-year deal with the University of Maryland Medical System in April 2026, followed by a A$37 million five-year renewal with Northwestern Medicine, representing more than A$60 million in contracted revenue within a single month.

The key risks include competitive pressure from large incumbents such as GE HealthCare, Philips, and Siemens Healthineers, longer procurement cycles caused by US hospital budget constraints, and the fact that an elevated 55-58x trailing P/E amplifies the share price impact of any earnings miss or growth deceleration.

Pro Medicus reported an NPAT margin of approximately 54% in FY25, meaning it retained 54 cents of profit after tax for every dollar of revenue earned, a figure that expanded from around 51% in FY24 and places it among the most profitable technology companies listed on the ASX.