How Hormuz Closure at $104 Oil Is Reshaping Every Asset Class

2 hrs ago

OpenAI quietly missed its target of one billion weekly active ChatGPT users by the end of 2025, and on 28 April 2026, Wall Street is paying the price. Reports from The Wall Street Journal, citing individuals with direct knowledge, revealed that the company fell short of both its user growth milestone and multiple monthly revenue targets earlier in 2026. Simultaneously, CFO Sarah Friar raised internal concerns about the company’s ability to fund future data centre contracts. The combined effect sent AI-linked equities into a sharp retreat on a morning already pressured by geopolitical turbulence and rising oil prices. What follows is a breakdown of exactly what OpenAI missed, which companies are absorbing the fallout and by how much, and what the episode reveals about the fragility of AI sector momentum for investors tracking publicly traded names.

The OpenAI selloff did not land in a vacuum; the broader market pressures this week include five Magnificent Seven earnings reports, a Federal Reserve rate decision, and residual Strait of Hormuz risk keeping WTI above $92 per barrel, a convergence that amplifies volatility for any sector already carrying elevated uncertainty.

OpenAI is not publicly traded. Retail investors cannot hold its shares directly. Yet its financial health is deeply embedded in the valuations of companies that are listed, and a single morning of bad news from inside the company can move billions in market capitalisation across multiple tickers.

The transmission works through three channels:

When a private anchor company misses benchmarks, it does not affect one stock. It reprices risk across the entire ecosystem simultaneously.

This is not theoretical. In January 2026, concerns about OpenAI’s debt load and Microsoft’s capital expenditure commitments to the partnership triggered a $440 billion market capitalisation wipeout for Microsoft. That episode established the template for what played out again on 28 April: OpenAI’s internal financial stress, surfaced through reporting, translating directly into public equity losses.

The headline miss was the user target. OpenAI set an internal goal of reaching one billion weekly active ChatGPT users by the end of 2025. It did not get there.

That alone would have drawn scrutiny. But it was not alone.

These were internal benchmarks, not external analyst projections. When a company misses targets it set for itself, the credibility damage runs deeper than a consensus miss because it suggests the company’s own leadership misjudged the trajectory.

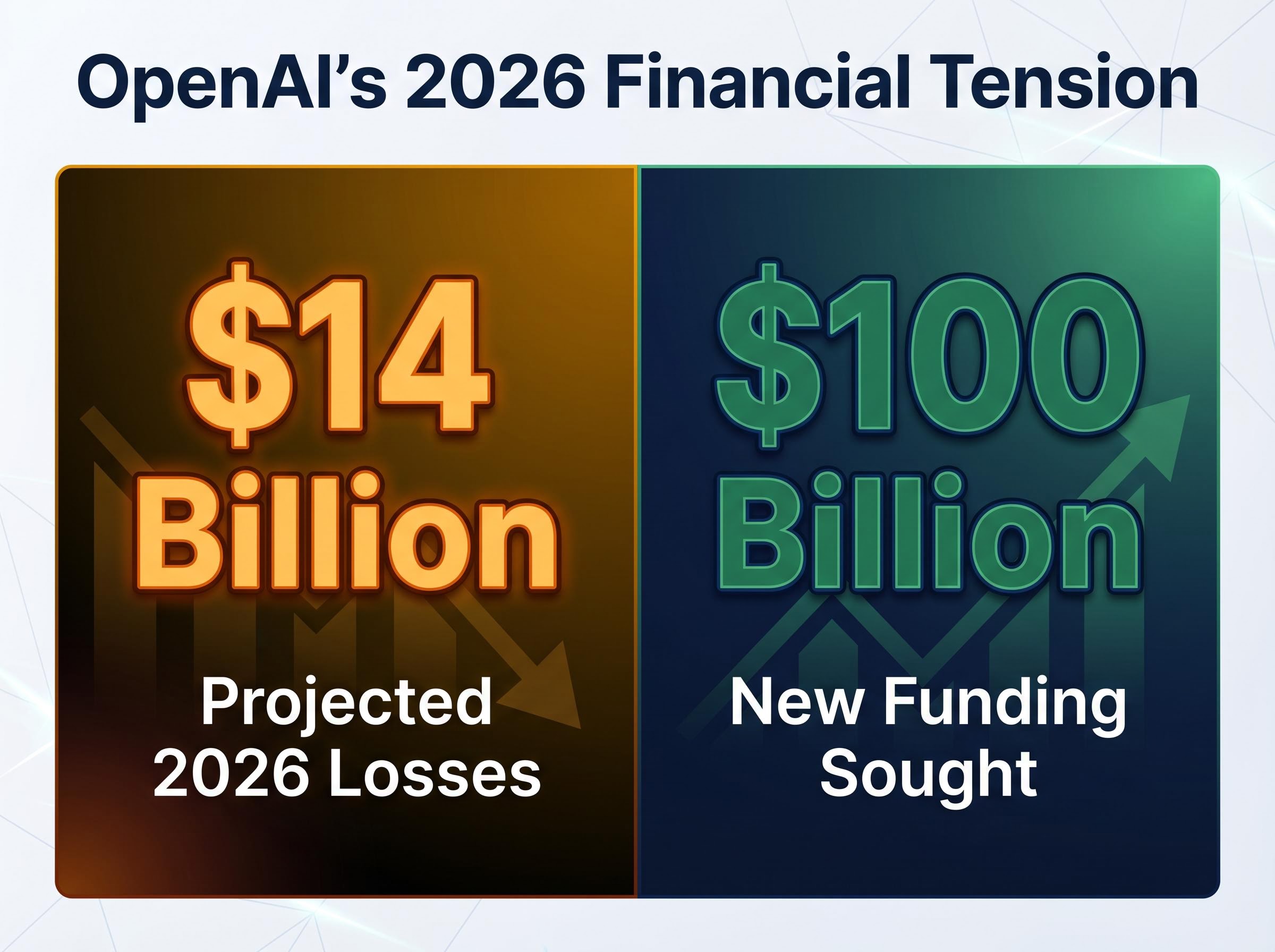

OpenAI is projected to incur approximately $14 billion in losses in 2026, according to reporting from R&D World, while simultaneously seeking $100 billion in new funding.

The board’s response was direct: scrutiny of existing data centre agreements and questions about whether OpenAI’s compute expansion plans remain financially viable. For investors in partner companies, this is the signal that matters. Internal confidence has cracked.

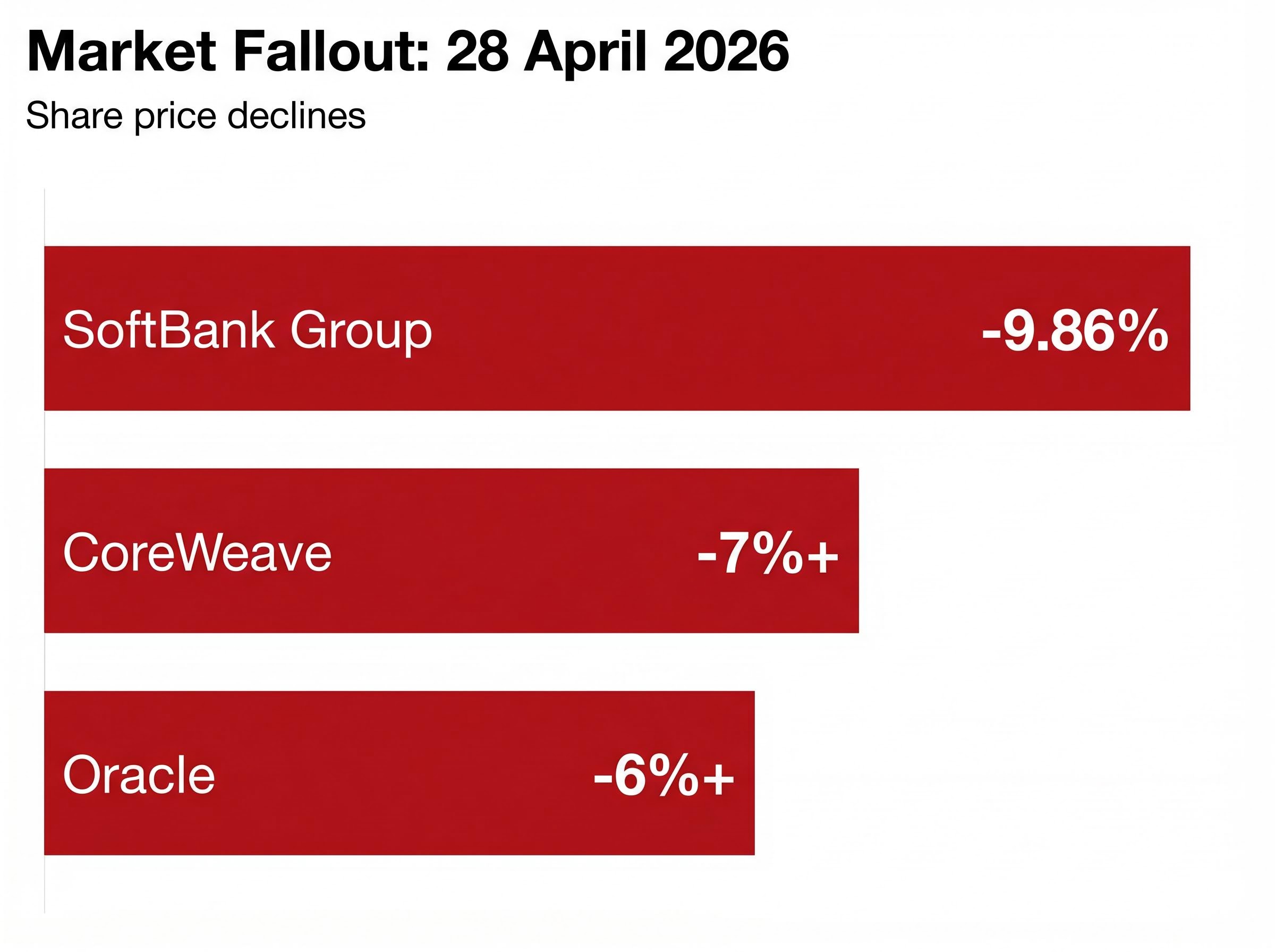

The selloff on 28 April 2026 did not land evenly. Each affected company carries a different type of OpenAI exposure, and the market priced those distinctions accordingly.

Oracle, as OpenAI’s primary cloud infrastructure provider, fell more than 6%. Its revenue dependency on OpenAI workloads made it the most directly exposed major name.

CoreWeave, a pure-play compute provider with a narrower business than Oracle, dropped over 7%. The amplified move reflected its concentrated exposure to AI infrastructure spending.

SoftBank Group suffered the steepest percentage decline, falling 9.86% in Tokyo trading. The conglomerate’s large pledged capital position in OpenAI made it the highest-beta name in the selloff.

Microsoft and Nvidia, the two headline names most commonly associated with AI, carry more qualified exposure. Microsoft closed at $424.82 on 27 April 2026, reflecting a year-to-date decline of approximately 11.96%. Nvidia’s market capitalisation sits at approximately $5.2 trillion. Specific 28 April percentage changes for both companies were not independently verified at time of writing.

| Company | Relationship to OpenAI | Reported 28 April Move |

|---|---|---|

| Oracle | Primary cloud infrastructure provider | Down more than 6% |

| CoreWeave | Pure-play compute provider | Down over 7% |

| SoftBank Group | Conglomerate investor, pledged capital | Down 9.86% (Tokyo) |

| Microsoft | Strategic partner, revenue sharing | Not independently verified |

| Nvidia | $100B infrastructure commitment | Not independently verified |

Note: Microsoft and Nvidia figures for 28 April 2026 were not independently verified at time of writing. Bloomberg Terminal remains the primary verification source for intraday and closing data.

When a CFO raises concerns internally about a company’s ability to meet its obligations, and those concerns subsequently surface in Wall Street Journal reporting, the signal carries more weight than any external analyst downgrade.

Sarah Friar warned that OpenAI may lack sufficient funds to honour future data centre agreements if revenue growth does not accelerate, according to reporting from The Wall Street Journal and the Economic Times. This is not abstract worry. It connects directly to the revenue streams of Oracle and CoreWeave, whose share price declines on 28 April reflect the market pricing precisely this risk.

Friar’s concern, as reported, centres on whether OpenAI can meet contracted compute obligations without a significant acceleration in revenue, a warning that triggered board-level scrutiny of existing data centre agreements.

Beyond the operational funding concern, Friar also flagged risks to OpenAI’s late 2026 IPO timeline. The company plans to allocate shares to retail investors as part of that offering. However, Friar cited heavy spending and internal rifts with CEO Sam Altman as factors that could derail the schedule.

That these concerns triggered board scrutiny means this is now a governance matter. For investors in partner companies, a CFO raising alarms that reach the board is a leading indicator, not a footnote.

On 27 April 2026, CNBC reported that OpenAI and Microsoft struck a revised agreement redrawing their once-exclusive partnership. Under the new terms, OpenAI can cap revenue sharing with Microsoft and sell its services across multiple clouds, no longer locked into Azure exclusivity.

The revision creates a genuinely ambiguous risk profile for Microsoft shareholders:

Scion Asset Management’s Michael Burry characterised the exclusivity breakup as “good for MSFT” on StockTwits. That read has merit: if OpenAI’s financial trajectory continues to deteriorate, Microsoft’s exposure is now structurally smaller than it was under the previous arrangement.

Microsoft closed at $424.82 on 27 April, carrying a year-to-date decline of approximately 11.96%. Analyst commentary suggests that if OpenAI were to fail, Microsoft would face a hit, though its diversification limits the severity. The revised partnership makes that hit smaller, at the cost of capping the upside.

The Microsoft analyst consensus heading into the 29 April earnings print sits at approximately $577-$583 across 45 covering analysts, with 42 maintaining buy-equivalent ratings despite the roughly 12% year-to-date decline, a disconnect between institutional conviction and recent price action that the partnership revision now makes harder to resolve cleanly.

OpenAI is targeting a late 2026 IPO with a planned retail investor share allocation, according to CNBC reporting from 8 April 2026. The listing, if it proceeds on schedule, would be one of the largest technology offerings in years.

The hurdles are now stacked. The company’s own CFO has publicly (through reported channels) questioned the timeline’s feasibility. The board is scrutinising data centre contracts. The $100 billion funding target and the $14 billion projected 2026 loss mean OpenAI must simultaneously raise enormous external capital and demonstrate an accelerating revenue trajectory, two demands that compete for management bandwidth.

OpenAI is seeking $100 billion in new funding while projecting approximately $14 billion in losses for 2026, a financial tension that complicates the institutional roadshow narrative for a late-2026 listing.

Institutional underwriters will need to see the credibility gap close between Friar’s stated concerns and the company’s stated ambitions before pricing a confident offering. That gap, as of today, is widening, not narrowing.

The IPO valuation math for high-profile tech listings under financial stress offers a useful frame for what OpenAI’s institutional roadshow would need to achieve; SpaceX’s $2 trillion filing illustrates how even bull-case projections can compress IPO-entry returns to roughly 5-6% annualised when the entry valuation already prices in years of assumed growth.

Past performance does not guarantee future results. Financial projections are subject to market conditions and various risk factors.

The 28 April selloff is a case study in systemic AI sector interdependency, not an isolated reaction to one company’s bad quarter. OpenAI’s internal benchmarks, funding needs, and leadership dynamics are now de facto market signals for anyone holding AI infrastructure, cloud, or conglomerate positions.

Three variables will determine whether today’s selloff is a correction or the start of a broader re-rating: OpenAI’s progress on its $100 billion fundraising round, the resolution (or escalation) of the CFO-CEO tension, and whether the late 2026 IPO timeline holds or slips.

Investors with exposure to any name in the OpenAI ecosystem, whether Oracle, Microsoft, Nvidia, SoftBank, or CoreWeave, may benefit from monitoring these milestones as the near-term triggers most likely to move partner stocks again.

Investors wanting to stress-test their AI sector exposure against the structural risks that predate today’s OpenAI news will find our deep-dive into AI investment risks for 2026 useful; it examines the $527 billion hyperscaler capex cycle, the early-2026 market divergence between individual AI business models, and Vanguard’s warning on US equity downside if AI capital expenditure fails to deliver proportionate returns.

This article is for informational purposes only and should not be considered financial advice. Investors should conduct their own research and consult with financial professionals before making investment decisions.

The Wall Street Journal reported that OpenAI missed its internal target of one billion weekly active ChatGPT users by end of 2025, fell short of multiple monthly revenue targets in early 2026, and had its CFO raise concerns about funding future data centre contracts, triggering a broad selloff in AI-linked stocks.

OpenAI's financial health is embedded in the valuations of listed partner companies through contracted revenue dependency, pledged capital exposure, and partnership-driven valuation premiums, meaning any deterioration in OpenAI's trajectory reprices risk across Oracle, Microsoft, Nvidia, CoreWeave, and SoftBank simultaneously.

SoftBank Group suffered the steepest decline at 9.86% in Tokyo trading, followed by CoreWeave which dropped over 7%, and Oracle which fell more than 6%, reflecting each company's degree of direct exposure to OpenAI infrastructure spending.

Sarah Friar warned that OpenAI may lack sufficient funds to honour future data centre agreements if revenue growth does not accelerate, and also flagged risks to the company's planned late 2026 IPO timeline, citing heavy spending and internal rifts with CEO Sam Altman.

The revised agreement caps the revenue Microsoft can share from OpenAI's commercial success while also reducing Microsoft's binary failure risk, since OpenAI is no longer locked into Azure exclusivity, meaning the potential upside is smaller but so is the downside exposure if OpenAI's financial trajectory worsens.