How Hormuz Closure at $104 Oil Is Reshaping Every Asset Class

5 hrs ago

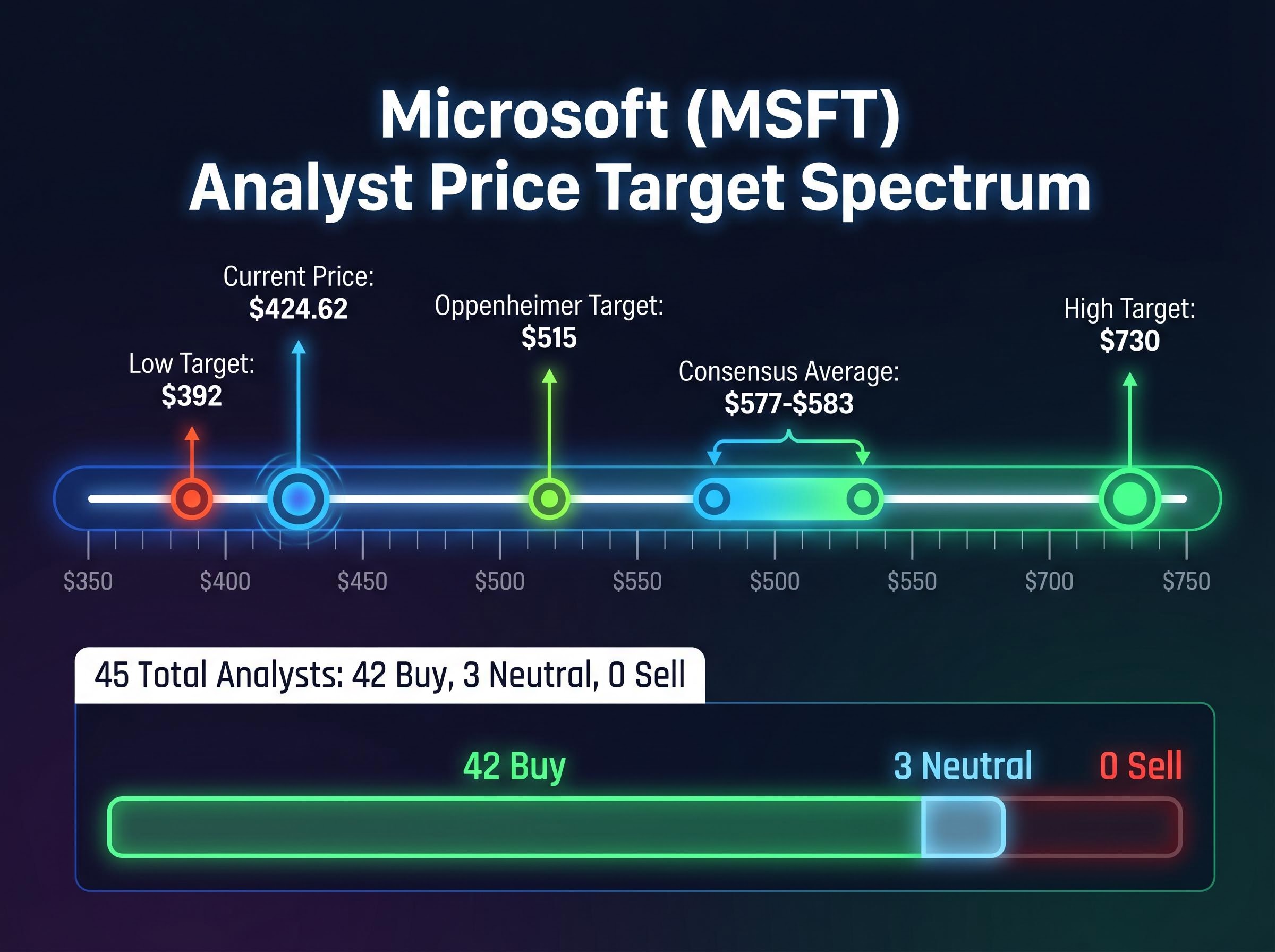

Oppenheimer slashed its Microsoft price target by $115 on 27 April 2026, cutting from $630 to $515, yet the firm kept its Outperform rating in place. That contradiction sits at the centre of a broader fracture in analyst sentiment on one of the world’s most widely held stocks. With MSFT down roughly 12% year-to-date and trading at $424.62, the consensus average target of approximately $577-$583 implies more than 36% upside from current levels. Two days before fiscal Q3 2026 earnings land after market close on 29 April, this analysis maps the full analyst divergence, examines the specific AI concerns driving the bear case, lays out the competing bull arguments, and identifies the numbers that will determine which side of the debate strengthens after the print.

Oppenheimer’s revised $515 target, down from $630, represents one of the steepest single-revision reductions on Microsoft this year. The firm published the cut on 27 April 2026, just two sessions before fiscal Q3 earnings, a timing choice that signals urgency rather than routine model maintenance.

The retention of the Outperform rating is the detail that reframes the move. At $424.62, MSFT trades roughly 21% below the new $515 target. Oppenheimer is not walking away from the stock; the firm is resetting where it believes the ceiling sits while maintaining the view that the floor is well above the current price.

InvestingPro data adds a layer to that view. Microsoft carries a trailing P/E of 26.6, a PEG ratio of 0.92, and a “GREAT” financial health score.

A PEG ratio of 0.92 suggests the market may be pricing Microsoft’s earnings growth at a discount to its actual trajectory, a signal that typically attracts value-oriented institutional buyers in large-cap tech.

Oppenheimer cited four named concerns: the risk that AI-powered tools disrupt Microsoft 365 revenue rather than expand it, an elevated capital expenditure trajectory tied to data centre buildouts, competitive pressure from rivals advancing their own AI platforms, and a perception that Microsoft lags peers in certain areas of AI development.

Microsoft’s voluntary retirement programme, targeting approximately 8,750 U.S. employees through a rule-of-70 eligibility threshold, forms part of the same organisational pivot that includes the return-to-office mandate and compensation structure overhaul, signalling a deliberate effort to manage costs alongside the elevated capital expenditure tied to AI infrastructure.

The firm explicitly noted that these concerns are unlikely to be resolved by the Q3 earnings release alone. Oppenheimer also flagged that depressed expectations, partly driven by ServiceNow’s weaker Q1 results, could create a setup for a positive revision cycle if Microsoft delivers an upside surprise.

The AI disruption narrative is real as a concern. The adoption numbers, however, tell a more specific story.

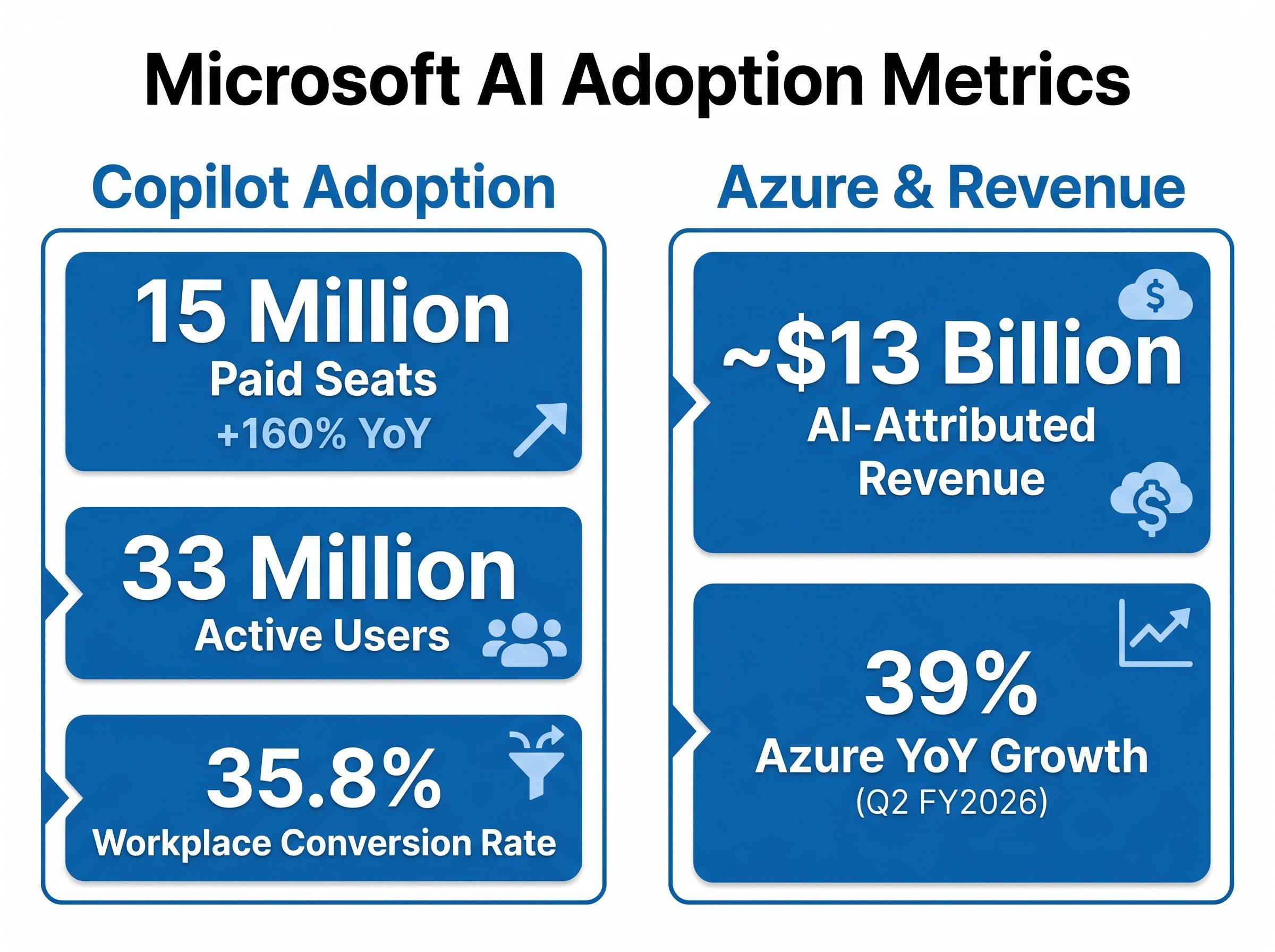

Microsoft 365 Copilot has reached 15 million paid seats, up 160% year-over-year. Active users stand at 33 million, with a workplace conversion rate of 35.8%. AI-attributed revenue has reached approximately $13 billion across the business.

| Metric | Current | Year-over-Year Change |

|---|---|---|

| Copilot paid seats | 15 million | +160% |

| Active Copilot users | 33 million | — |

| Workplace conversion rate | 35.8% | — |

The product that investors fear is cannibalising M365 is simultaneously driving M365 adoption at commercial scale. That distinction matters.

Jefferies enterprise survey data showing M365 Copilot penetration at 82% of surveyed firms, with projected revenue reaching up to $11.4 billion by CY2026, reinforces the commercial adoption trajectory implied by the 15 million paid seat figure and provides a demand-side anchor for the bull case on M365 monetisation.

Azure revenue grew 39% year-over-year in Q2 FY2026, with AI workload demand cited as the primary driver. Several forward-looking structural tailwinds remain in motion:

Oppenheimer itself acknowledged these tailwinds even as it cut the target, a tension that underscores the complexity of the current investment debate.

A price target is a 12-month fair value estimate based on a specific set of assumptions about revenue growth, margins, competitive positioning, and macroeconomic conditions. When two analysts cover the same stock and arrive at targets $338 apart (the distance between the low of $392 and the high of $730), it does not mean one is right and the other wrong. It means they are modelling different scenarios.

The useful signal sits in the distribution pattern, not any single number. Of the 45 analysts covering Microsoft, approximately 42 maintain Buy or equivalent ratings. Only 3 hold neutral positions. Zero recommend selling.

Over the past 90 days, the consensus average has drifted lower by approximately 5%, with notable downward revisions from TD Cowen (from $610 to $540) and Baird (from $540 to $500). The direction is down, but the conviction structure remains overwhelmingly bullish.

| Firm (Analyst) | Price Target | Rating | Most Recent Action |

|---|---|---|---|

| Oppenheimer | $515 | Outperform | 27 April 2026 |

| TD Cowen (Derrick Wood) | $540 | Buy | 16 April 2026 |

| Guggenheim (John DiFucci) | $586 | Buy | 23 April 2026 |

| Citigroup (Tyler Radke) | $600 | Buy | 22 April 2026 |

| Goldman Sachs | $600 | Buy | April 2026 |

TD Cowen’s Derrick Wood anchors his $540 target on improved Office 365 Commercial Cloud revenue projections, estimating 15% annual growth through FY2030. Guggenheim’s John DiFucci at $586 has expressed confidence in a Q3 revenue beat but flagged specific Q4 downside risk for Azure. The major Wall Street cluster sits between $575 and $610, with Morgan Stanley at $580, Goldman Sachs at $600, and Jefferies at $610.

Microsoft reports fiscal Q3 2026 earnings after market close on 29 April 2026.

With MSFT trading at a 36% discount to consensus fair value, this release functions as a binary catalyst. Four specific metrics will determine whether the bull or bear case gains the upper hand:

Bank of America’s pre-earnings Azure growth estimate of 37.5% sits just below the Q2 FY2026 baseline of 39%, illustrating how closely institutional models are clustered around a narrow band of outcomes and why even a modest beat or miss on that single metric could drive outsized target revisions.

A strong Azure print paired with bullish forward guidance could compress the gap between the current price and consensus targets. A miss risks extending the 12% year-to-date drawdown.

Microsoft’s 12% drawdown has brought its forward P/E to approximately 22x, below Apple’s 28x but slightly above Alphabet’s 21x. On an EV/Sales basis, the stock trades at 10.4x versus a sector average of 8x, indicating that a meaningful premium persists even after the selloff.

| Factor | Bull Case | Bear Case |

|---|---|---|

| Azure growth | 39% baseline with AI demand accelerating | Capex returns unproven; Q4 risk flagged |

| Copilot adoption | 15M paid seats, up 160% YoY | M365 cannibalisation risk unresolved |

| Valuation | Forward P/E of 22x, PEG of 0.92 | EV/Sales premium of 10.4x vs 8x sector avg |

| Macro and sector backdrop | 42 of 45 analysts at Buy; 36%+ implied upside | AI capex skepticism; sector volatility; IP theft allegations |

The forward P/E comparison shows MSFT is not obviously cheap relative to Alphabet at 21x, but the 160% Copilot seat growth and 39% Azure trajectory offer a growth premium justification that peers cannot currently match at the same scale.

Background risks remain real but are not company-specific:

These factors weigh on sentiment across the sector rather than singling out Microsoft, but they provide the backdrop against which the Q3 print will be interpreted.

Oppenheimer’s $115 cut is the most visible signal of a broader recalibration in Microsoft expectations, yet the analyst community as a whole remains firmly in the Buy camp. The consensus target of approximately $577-$583 implies more than 36% upside from current levels, a gap that the 29 April earnings release will either begin to close or widen.

Azure growth and Copilot commentary are the two numbers that matter most. Oppenheimer itself projects H2 2026 as the period when data centre capacity expansion unlocks booking acceleration, meaning the longer investment thesis extends well beyond a single quarter’s print. The scorecard is set. The earnings call will update it.

This article is for informational purposes only and should not be considered financial advice. Investors should conduct their own research and consult with financial professionals before making investment decisions. Past performance does not guarantee future results. Financial projections are subject to market conditions and various risk factors.

The consensus analyst price target for Microsoft sits between approximately $577 and $583, implying more than 36% upside from the current trading price of $424.62. Individual targets range from a low of $392 to a high of $730 across the 45 analysts covering the stock.

Oppenheimer reduced its Microsoft price target from $630 to $515 on 27 April 2026, citing four concerns: the risk that AI tools could disrupt Microsoft 365 revenue, elevated capital expenditure on data centres, competitive pressure from rival AI platforms, and a perception that Microsoft lags peers in certain areas of AI development.

The four key metrics to monitor are Azure revenue growth rate relative to the Q2 baseline of 39% year-over-year, Copilot paid seat expansion beyond 15 million, management commentary on Microsoft 365 monetisation and pricing, and forward guidance on Q4 Azure outlook and H2 2026 data centre capacity.

Of the 45 analysts covering Microsoft, approximately 42 maintain Buy or equivalent ratings, 3 hold neutral positions, and zero recommend selling, making the conviction structure overwhelmingly bullish despite recent downward target revisions.

Microsoft 365 Copilot has reached 15 million paid seats, up 160% year-over-year, with 33 million active users and a workplace conversion rate of 35.8%, suggesting the product is driving Microsoft 365 adoption at commercial scale rather than simply cannibalising it.