How Hormuz Closure at $104 Oil Is Reshaping Every Asset Class

9 hrs ago

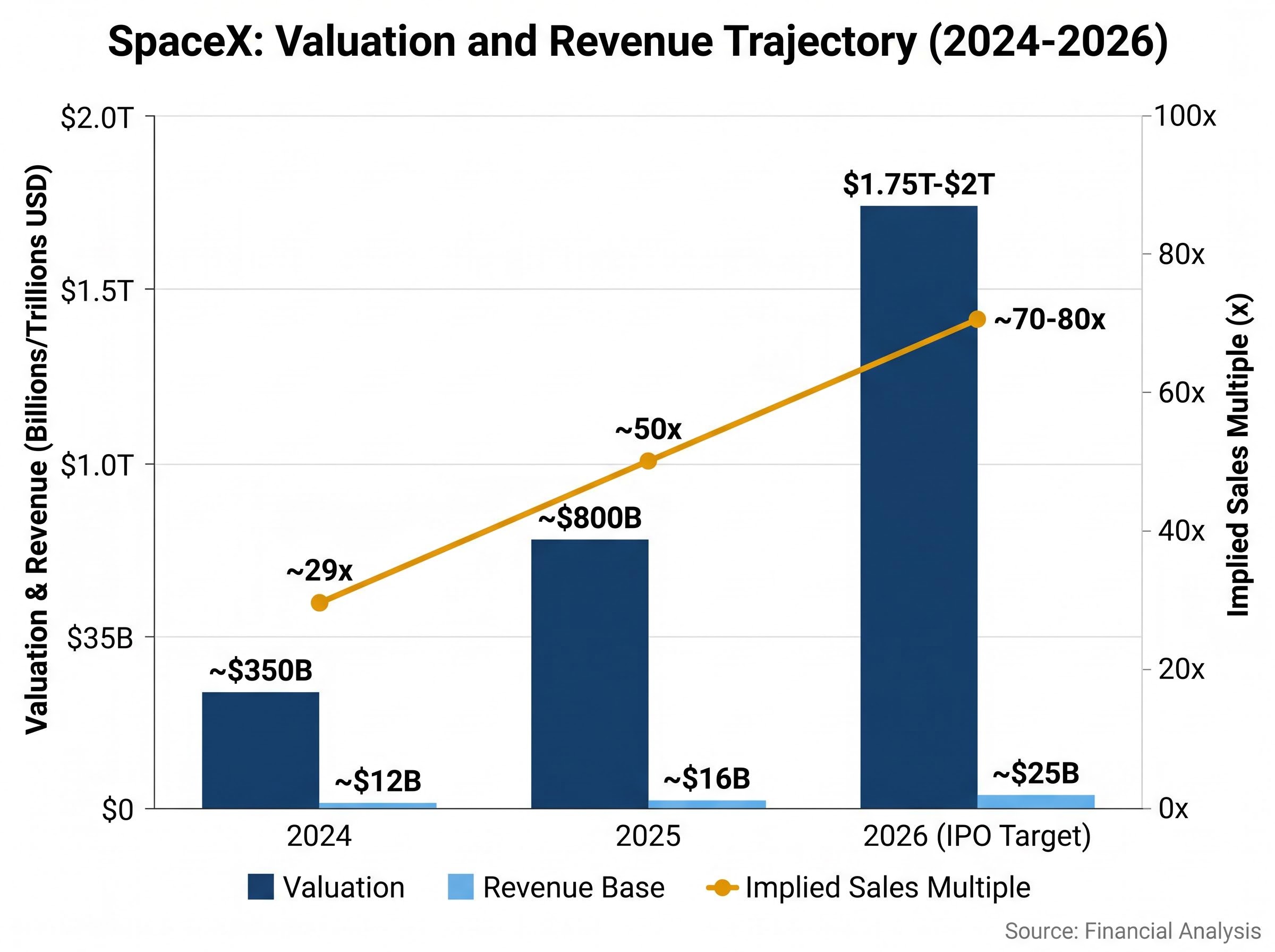

“`json { “fact_checked_full_article”: “SpaceX confidentially filed for an initial public offering on 1 April 2026, targeting a June listing on Nasdaq at a valuation of up to $1.75 trillion. Some analyst estimates place the market price closer to $2 trillion by the time shares begin trading, a figure that would make SpaceX more valuable than every publicly traded aerospace company combined and roughly 75 times its projected 2026 sales.\n\nThe S-1 filing is expected in late April or May 2026, marking the first time retail investors will see audited financials for a company that has operated in deliberate opacity for more than two decades. That transparency gap makes the current moment unusually consequential: valuations are being set before the numbers are confirmed.\n\nWhat follows is an analysis of the mathematics behind the $1.75 trillion to $2 trillion price tag, an assessment of ARK Invest’s $2.5 trillion target for 2030, and an answer to the question finance-literate readers are actually asking: even if the bulls are right about SpaceX’s future, does buying at IPO leave any meaningful return on the table?\n\n## What a $2 trillion valuation actually means in numbers\n\nThe headline range is $1.75 trillion to $2 trillion. Translated into the multiples that determine whether a price is defensible, that implies approximately 75 times forward sales on an estimated $25 billion in 2026 revenue, and approximately 160 times projected EBITDA based on the $8 billion EBITDA reported for 2025.\n\n> At roughly 75x forward sales, SpaceX would list at a multiple that exceeds the vast majority of high-growth technology IPOs of the past decade, including those with faster near-term revenue acceleration.\n\nThose multiples are grounded in concrete estimates, not abstraction. SpaceX generated approximately $16 billion in revenue and $8 billion in EBITDA in 2025, and 2026 revenue is projected at approximately $25 billion. The question is not whether the business is real. It is whether the price already reflects the reality.\n\nThe private market trajectory tells part of that story. SpaceX’s valuation has moved with unusual velocity over the past two years, compressing what might have been a decade of price discovery into 24 months.\n\n

| Year | Valuation | Revenue Base | Implied Sales Multiple |

|---|---|---|---|

| 2024 (private) | ~$350 billion | ~$12 billion | ~29x |

| 2025 (private) | ~$800 billion | ~$16 billion | ~50x |

| 2026 (IPO target) | $1.75T-$2T | ~$25 billion | ~70-80x |

\n

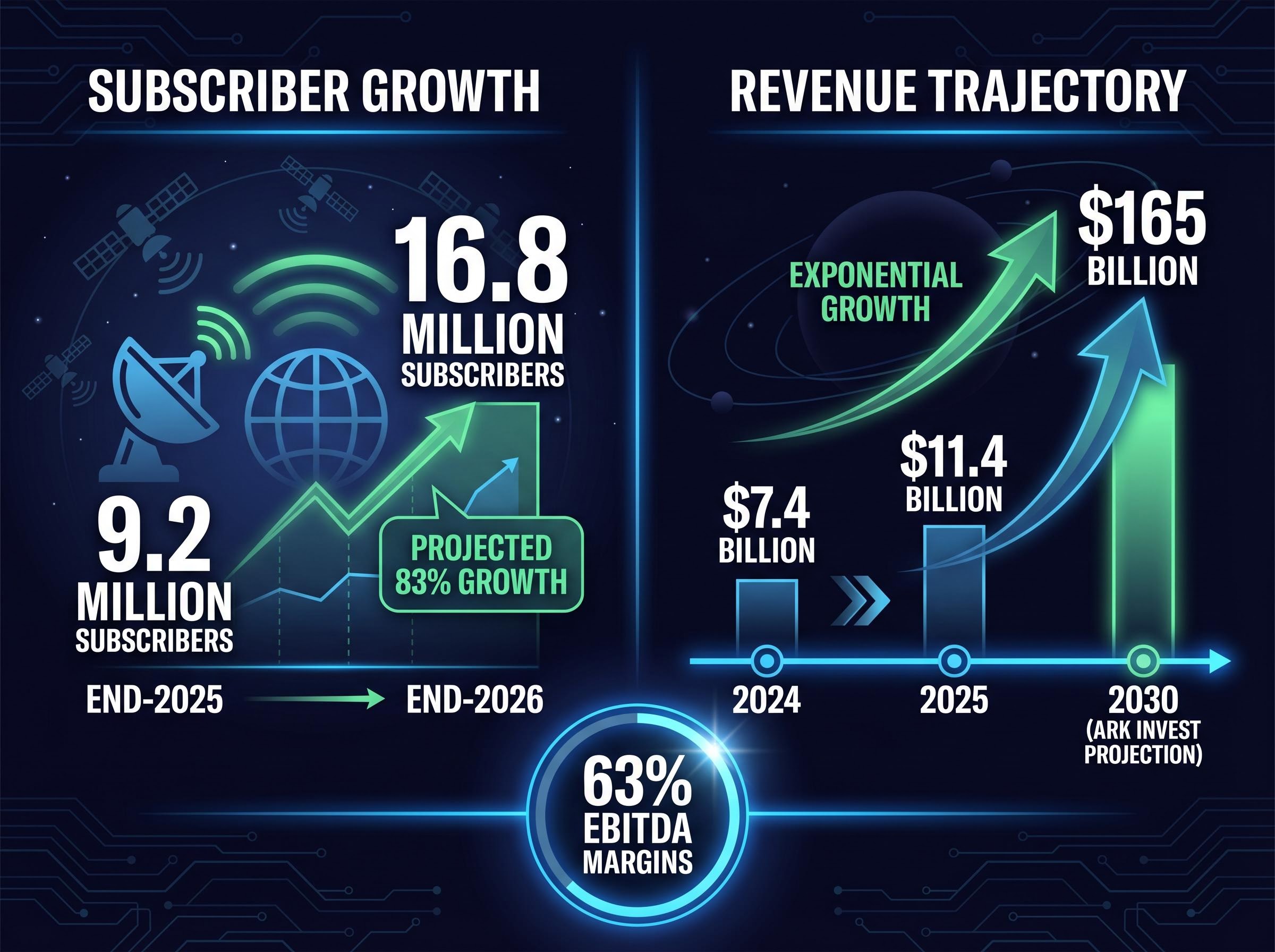

\n\nEach step-up has required investors to accept a higher multiple for the same underlying business, a pattern that works only as long as the growth rate justifies it.\n\n## Starlink is the engine, and its numbers are genuinely impressive\n\nThe bull case starts with Starlink, and it starts there for a reason. The satellite internet division’s 2025 operating metrics represent one of the strongest subscription-revenue profiles in any pre-IPO company in recent memory:\n\n- 9.2 million subscribers at end-2025\n- $11.4 billion in Starlink and Starshield revenue\n- 63% EBITDA margins\n\nThat margin profile is what separates Starlink from the rest of SpaceX’s revenue base. Launch services are high-profile but operationally lumpy. Starlink generates recurring, high-margin subscription income with a growth trajectory that analysts project will reach 16.8 million subscribers by end-2026. The comparison point is not other aerospace businesses; it is high-margin software platforms, and Starlink earns a premium multiple on that basis.\n\nARK Invest projects $165 billion in combined Starlink and Starshield revenue by 2030. That figure represents more than a fourteen-fold increase from the $11.4 billion generated in 2025 (itself up from $7.4 billion in 2024). The growth rate implied is aggressive, but it is not without a foundation: subscriber additions accelerated through 2025, and the addressable market is expanding.\n\nIt is worth noting that all Starlink subscriber and revenue figures cited here are analyst estimates from sources including Quilty Space, not official SpaceX disclosures. The S-1 will be the first opportunity to verify them against audited data.\n\n### What “Direct to Cell” adds to the subscriber thesis\n\nStarlink’s Direct to Cell initiative, which enables satellite connectivity directly to standard mobile handsets, expands the total addressable market beyond traditional broadband consumers. It opens a subscriber base that includes users in regions without terrestrial mobile coverage and adds an entirely new service tier to Starlink’s revenue model. Bulls cite it as a near-term growth vector, though material revenue from the programme is not yet reflected in current analyst estimates.\n\n## Understanding the valuation math: why growth multiples work the way they do\n\nA company priced at 75x forward sales is not automatically overpriced. High-multiple valuations are a bet on compounding: if revenue grows fast enough and margins expand, the entry multiple compresses over time and the valuation \”grows into\” the price the market assigned in advance.\n\nThe logic works in three steps when applied to SpaceX at IPO:\n\n1. ARK’s target: ARK Invest projects a $2.5 trillion enterprise value for SpaceX by 2030, based on its venture fund analysis (updated summer 2025), underpinned by the $165 billion combined revenue projection.\n2. Implied price appreciation: If an investor enters at a $2 trillion IPO valuation and ARK’s $2.5 trillion target is reached by 2030, the total return is approximately 25% over four years.\n3. Annualised return vs. benchmark: That 25% total return annualises to roughly 5-6% per year, a figure that falls below historical equity market averages when adjusted for the concentration risk and uncertainty profile of a single-stock position in a company that has never reported public financials.\n\n> Even if every major bull projection proves correct, the return available to IPO-entry investors may not compensate adequately for the risk premium being accepted.\n\nThis is the central tension of the SpaceX IPO valuation. The business may be extraordinary. The question is whether the price already reflects that.\n\nThese statements are speculative and subject to change based on market developments and company performance.\n\n## The xAI merger introduces upside and a meaningful new risk\n\nIn February 2026, SpaceX (valued at approximately $1 trillion at the time) merged with xAI (valued at approximately $250 billion), creating a combined entity with a stated valuation of $1.25 trillion at announcement. The merger broadened SpaceX’s investment thesis from space infrastructure into artificial intelligence, and contributed to subsequent upward IPO valuation revisions.\n\nThe implications split cleanly:\n\nBull case:\n- AI infrastructure exposure adds a second long-duration growth vertical alongside Starlink\n- The orbital data centre opportunity, powered by SpaceX launch economics, could represent a large addressable market if costs continue to decline\n\nBear case:\n- xAI is currently operating at a loss, with its AI models described as trailing leading competitors including OpenAI\n- There is genuine analytical concern that Starlink’s 63% EBITDA margins may effectively subsidise xAI ventures, diluting the profitability of SpaceX’s most proven business line\n\nThe combined entity also includes X (formerly Twitter), adding a social media platform to a conglomerate already spanning rockets, satellites, and AI. Whether that breadth represents strategic optionality or structural complexity is a question reasonable investors can disagree on.\n\n### The orbital data centre thesis: genuine opportunity or narrative inflation?\n\nThe concept is straightforward: drastically reduced launch costs could enable data centres deployed in orbit, powered by solar energy, and potentially cheaper than ground-based equivalents given the scale of projected AI infrastructure spending. The opportunity is real in concept, but it is contingent on further cost reductions and unresolved technical challenges that place it firmly in the category of long-duration speculation rather than near-term revenue driver.\n\n## Post-IPO monitoring: two variables that matter most\n\nTwo specific, trackable variables will determine whether the IPO valuation proves defensible:\n\n1. Starlink subscriber growth. The gap between the 9.2 million end-2025 estimate and the 16.8 million end-2026 analyst forecast is the single most market-moving disclosure investors should expect from the S-1 and subsequent earnings. If actual subscriber figures confirm the trajectory, the revenue projections hold. If they fall short, the 75x forward multiple loses its foundation.\n\n2. Rocket launch cost trajectory. ARK’s $165 billion 2030 revenue projection and the orbital data centre thesis both depend on launch costs continuing to decline at historically observed rates. That trajectory is not guaranteed. Any plateau in cost reduction compresses the upside case materially.\n\nSecondary risk factors that merit ongoing monitoring include:\n\n- Regulatory risk and government contracting dependencies, particularly given Elon Musk’s public profile and political exposure\n- xAI cash burn and its impact on consolidated margins\n- Competitive developments from Blue Origin and other launch providers, though the gap remains wide\n\nThe S-1, expected in late April or May 2026, will be the first audited disclosure event. Every figure cited in this analysis is analyst-sourced pending that filing. Readers should treat current estimates as directional rather than definitive.\n\n## Where that leaves IPO investors\n\nAt $1.75 trillion to $2 trillion, SpaceX is priced for a future that may well arrive, but the return available to IPO-entry investors if that future arrives on schedule is modest relative to the risk being accepted. Even ARK Invest’s own $2.5 trillion 2030 target implies roughly 25% total appreciation from a $2 trillion entry, a figure that underperforms broad equity indices on a risk-adjusted basis.\n\nThe bull case is not hollow. Starlink’s margins, subscriber trajectory, and SpaceX’s near-monopoly position in commercial launch represent real competitive advantages that justify a substantial premium over traditional aerospace valuations.\n\nThe S-1 filing is the inflection point. Investors considering participation should monitor Starlink subscriber disclosures as the primary valuation anchor, assess whether the IPO pricing leaves sufficient return given the risks the xAI merger has introduced, and recognise that the difference between a good company and a good investment often comes down to the price paid at entry.\n\nThis article is for informational purposes only and should not be considered financial advice. Investors should conduct their own research and consult with financial professionals before making investment decisions.” } “`

Investors wanting to evaluate the specific mechanics, fees, and redemption terms before committing capital will find our comprehensive walkthrough of SpaceX proxy investment vehicles covers the ARKVX quarterly redemption restriction, BPTRX concentration risk across Musk-led positions, and the practical limitations of GOOGL as a SpaceX proxy given its roughly 2.5% implied exposure.

The orbital data centre thesis assumes AI infrastructure spending continues at pace, but physical constraints on AI infrastructure buildout, including grid interconnection queues exceeding 2,100 GW and HBM3e memory shortages forecast to persist beyond 2026, suggest that the timeline for deploying space-based compute at meaningful scale faces compounding headwinds beyond launch cost economics alone.

One dimension the valuation multiples alone do not capture is the governance structure of the SpaceX IPO: Elon Musk is expected to retain approximately 79% of voting control through a permanent dual-class share structure, meaning public shareholders will hold economic exposure with minimal influence over capital allocation decisions.

Peer-reviewed research on long-run IPO performance and risk-adjusted returns from Prof. Jay Ritter, whose analysis of post-IPO equity markets across multiple cycles shows that newly public companies historically underperform seasoned stocks on a risk-adjusted basis, a pattern that frames the SpaceX return math in its proper historical context.

Quilty Space’s Starlink financial overview and 2026 subscriber forecast, the primary research underpinning the 16.8 million subscriber projection and the $11.4 billion revenue figure cited here, represents the most granular independent dataset available on Starlink’s commercial trajectory ahead of the S-1.

SpaceX is targeting a valuation of $1.75 trillion to $2 trillion at its planned June 2026 Nasdaq listing, implying roughly 75 times forward 2026 sales and approximately 160 times projected EBITDA, multiples that exceed the vast majority of high-growth technology IPOs from the past decade.

If an investor enters at a $2 trillion IPO valuation and ARK Invest's $2.5 trillion target for 2030 is reached on schedule, the total return would be approximately 25% over four years, which annualises to roughly 5-6% per year, below historical broad equity market averages on a risk-adjusted basis.

Starlink is the primary engine of the bull case, generating an estimated $11.4 billion in revenue at 63% EBITDA margins in 2025, with analysts projecting subscriber growth from 9.2 million to 16.8 million by end-2026 and ARK Invest forecasting $165 billion in combined Starlink and Starshield revenue by 2030.

The February 2026 merger with xAI adds an AI business that is currently operating at a loss with models described as trailing leading competitors, raising concerns that Starlink's 63% EBITDA margins could effectively subsidise xAI ventures and dilute the profitability of SpaceX's most proven business line.

SpaceX's S-1 filing is expected in late April or May 2026, representing the first public audited financials in the company's history; investors should pay closest attention to actual Starlink subscriber counts and launch cost trends, as these two variables underpin nearly every major valuation projection.