AI Investment Risks: Why $6 Trillion May Not Pay Off

Key Takeaways

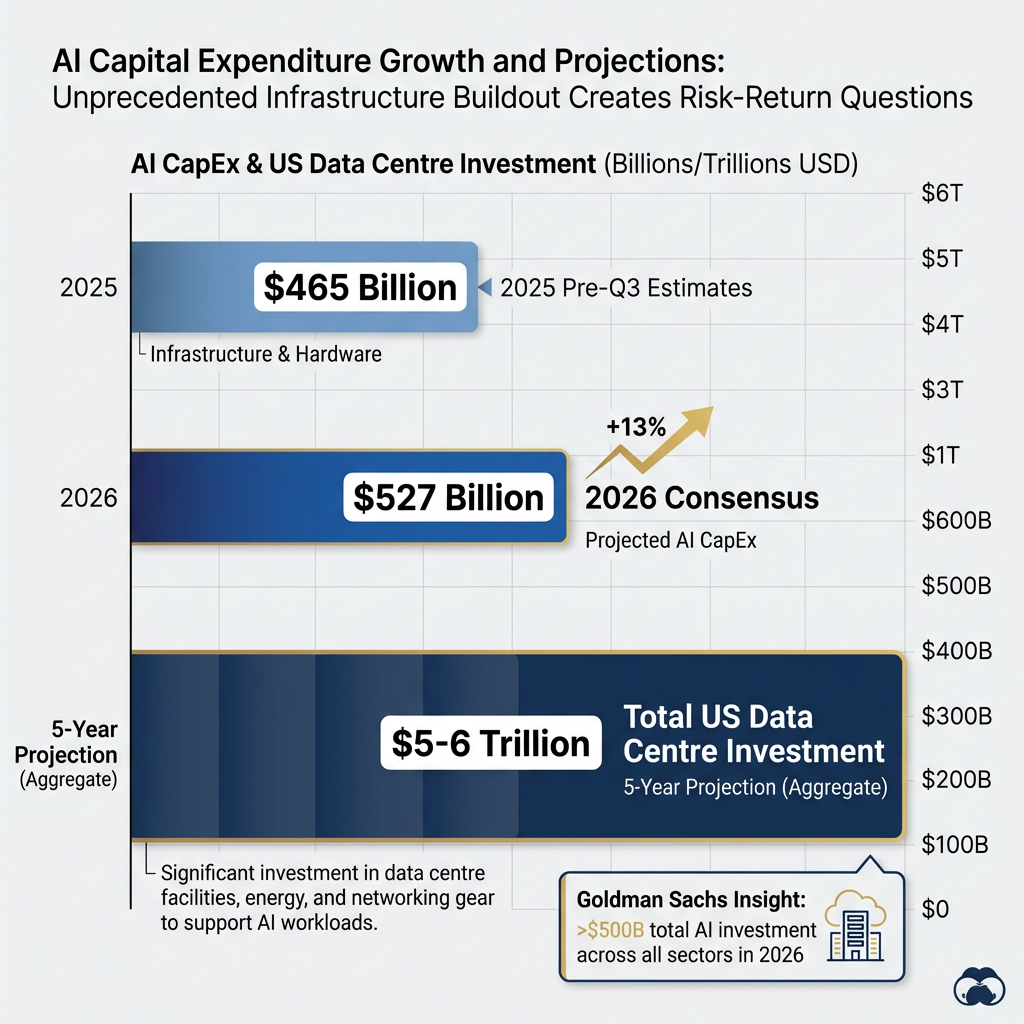

- Consensus hyperscaler capital expenditure for 2026 has reached $527 billion, yet no major provider has announced a path to proportionate returns, raising serious ROI sustainability concerns.

- Early 2026 market divergence — with Google gaining 30% while Oracle fell 30% — signals investors are now evaluating individual AI business models rather than treating AI as a single investable theme.

- A KPMG survey found 75% of large-company CEOs believe generative AI has been overhyped, yet nearly 80% still plan to allocate at least 5% of capital budgets to AI initiatives in a telling paradox.

- Vanguard warns of material US equity downside risk if AI capital expenditure fails to deliver proportionate returns, particularly given the debt financing structures underpinning much of the buildout.

- Institutional consensus favours diversification and rigorous fundamental analysis over momentum-driven AI exposure, with Vanguard estimating AI could contribute 1.2% to GDP growth but urging against concentrated sector bets.

The artificial intelligence investment landscape is undergoing a profound transformation in 2026. After years of surging capital flows that propelled AI stocks to record valuations, institutional investors are now stress-testing which companies will actually deliver returns versus which will be disrupted by the very technology they helped fund. Apollo Global Management president Jim Zelter’s pointed question captures the moment: with an estimated $5 trillion to $6 trillion in US data centre investment projected over the next five years, will those funding the buildout reap proportionate financial rewards?

The era of blanket AI optimism is giving way to rigorous scrutiny. Hedge funds, Morgan Stanley, and Goldman Sachs are distinguishing between AI beneficiaries and those vulnerable to displacement. Early 2026 market volatility punished knowledge-sector services including finance, media, and software, whilst hyperscalers demonstrated resilience amid selective rotation. Google climbed 30% in late 2025 with momentum extending into the new year, whilst Oracle dropped 30% on execution concerns and Meta declined 10%. This divergence signals that investors are no longer treating AI as a monolithic theme but rather evaluating which specific business models will thrive.

> Industry Sentiment

> A KPMG survey revealed that approximately 75% of large-company chief executives believed generative AI had been overhyped during the preceding year, yet nearly 80% still plan to direct at least 5% of capital budgets towards AI initiatives. This paradox frames the complexity confronting investors in 2026.

Understanding AI Investment Cycles and Why Returns Are Uncertain

Artificial intelligence is fundamentally converting the technology sector from capital-light to capital-intensive, altering its investment profile in ways that matter deeply for return expectations. Historically, software companies operated with minimal physical infrastructure, delivering high margins and requiring little capital expenditure. AI demands massive data centres, specialised chips, and energy infrastructure. This structural shift changes risk-return dynamics in ways many investors may not fully appreciate.

The concept that transformative technology utility doesn’t guarantee investor returns has historical precedent. Zelter draws parallels to mobile phone adoption, which transformed daily life globally yet delivered modest returns for many industry investors. Railroads, airlines, and early internet companies offer similar patterns: societally transformative but often value-destructive for equity holders. Apollo’s three decades observing technology investment cycles inform this caution.

NBER research on technology productivity J-curves demonstrates that transformative technologies historically require years of capital investment before measurable productivity gains appear, providing an analytical framework that explains the lag between AI infrastructure spending and observable economic returns.

Several structural factors create AI return uncertainty. Unprecedented capital requirements introduce execution risk at scales previously unseen in technology. Competitive dynamics drive spending regardless of clear return on investment pathways, as companies fear being left behind. The timeline for enterprise adoption to match infrastructure investment remains uncertain. Perhaps most critically, value may accrue to AI users rather than AI builders, a distribution that would disappoint those funding the buildout.

When big ASX news breaks, our subscribers know first

Valuation and ROI Risks: The Capex Sustainability Question

The 2026 AI capital expenditure boom continues at staggering scale. Consensus estimates for hyperscaler capex reached $527 billion for the year, up from $465 billion in pre-Q3 2025 estimates. Goldman Sachs projects over $500 billion in total AI investment across all sectors. Notably, no major hyperscaler has announced scaling back. These figures have been consistently revised upward as actual spending repeatedly exceeds projections.

Whilst hyperscaler spending dominates headlines, regional data centre infrastructure demand demonstrating tangible contract wins is accelerating globally, with companies like NEXTDC reporting record orders that show enterprise appetite for AI-ready facilities extends well beyond the major cloud providers.

Much of this investment is debt-financed, creating pressure for near-term returns that may not materialise at expected timescales. Credit stress is rising among lower-rated issuers funding AI initiatives. Vanguard warns of material US equity downside risk if capital expenditure fails to deliver proportionate returns. The combination of elevated valuations and debt financing creates vulnerability to sentiment shifts that could trigger rapid revaluations.

The financing mechanisms supporting AI infrastructure vary significantly, with debt-financed infrastructure projects with institutional capital commitments attracting billions in backing that provides stability but also creates fixed return expectations that may constrain operational flexibility during market volatility.

Bear case concerns centre on several specific mechanisms. Circular investing patterns, where AI companies invest in each other’s services, may artificially inflate valuations without creating sustainable external demand. Aggressive accounting practices around chip depreciation risk future earnings surprises as assets age faster than balance sheets reflect. Current productivity gains remain modest relative to investment levels. Enterprise demand hasn’t matched infrastructure buildout pace, raising questions about whether customer willingness to pay will justify the spending.

> Investment Caution

> “The need for capital does not inherently make every opportunity an attractive investment,” warned Jim Zelter, president of Apollo Global Management, speaking on Goldman Sachs’ ‘Exchanges’ podcast in April 2026. He stressed that elevated-risk equity-style exposure shouldn’t be treated as though it carried fixed-income safety profiles.

Market Volatility and Disruption: Winners Versus Losers

The early 2026 selloff reveals that markets are stress-testing which sectors AI will enhance versus replace. Knowledge sectors including software, finance, and media face disruption fears as AI demonstrates capability to automate tasks previously requiring human expertise. Infrastructure and platform plays show resilience as they provide the picks and shovels for AI deployment. Stock selection matters more than sector exposure in this environment.

| Company/Sector | Recent Performance | Primary Driver |

|---|---|---|

| +30% (late 2025 into 2026) | AI integration momentum and search dominance | |

| Oracle | -30% | Execution concerns and cloud competition |

| Meta | -10% | Execution issues and capex concerns |

| Software/Data Stocks | Broad selloff | GenAI replacement fears |

| Hyperscalers | Resilient | Infrastructure demand fundamentals |

Goldman Sachs identifies a strategic shift: rotation from debt-funded AI infrastructure towards platforms and productivity plays. Investors are penalising capex-heavy positions lacking demonstrable earnings growth whilst favouring companies showing actual AI-driven productivity gains. Morgan Stanley flags capital expenditure as creating both winners and losers, suggesting some software and data stock selloffs don’t match underlying fundamentals. This divergence may represent opportunity for selective investors willing to distinguish between disruption narratives and business reality.

Regulatory, Geopolitical, and Economic Risks

AI investment risks extend beyond company fundamentals into external factors affecting all positions regardless of individual company strength. US-China chip competition fragments supply chains and raises costs for AI hardware. Export controls and tariffs create uncertainty around component access and market reach. The potential for escalation could disrupt investment timelines and profitability projections regardless of company-specific execution.

Economic and inflation risks compound these concerns. AI-driven inflation from data centre energy demand represents an underestimated threat, with PCE inflation sticky at 2.8%. Yield curve implications affect financing costs for technology companies, particularly those relying on debt to fund AI investments. Vanguard points to AI exuberance creating stock downside despite potential economic upside, suggesting valuations have outpaced fundamental support.

IEA projections for data centre electricity consumption forecast substantial increases in power demand through 2026 and beyond, quantifying the infrastructure challenges that underpin inflation concerns about AI-driven energy costs affecting both operating expenses and broader economic price stability.

External risk factors requiring investor monitoring include:

- US-China chip access and supply chain stability affecting hardware availability and costs

- Data centre energy costs and inflation pressures that may exceed current projections

- Employment policy responses to AI-driven job displacement that could shift regulatory landscapes

- Interest rate environment affecting debt-financed AI capital expenditure sustainability

- Regulatory frameworks still forming globally, creating legal and compliance uncertainty

Contrarian Views: Where Opportunity May Exist

Not all experts share bearish perspectives on AI investments. Morgan Stanley argues that AI disruption fears overreact in certain cases. Software and data stock selloffs may not match underlying fundamentals, potentially representing opportunity for investors willing to look past near-term volatility. Historical precedent shows technology cycles are volatile but ultimately opportunity-rich for well-positioned players who survive the shakeout.

Goldman Sachs sees AI’s next phases boosting platforms and productivity stocks. Adoption will eventually lift broader productivity and economic growth, benefiting companies that successfully integrate AI into existing operations. LSEG notes the AI tide creates differentiated returns, favouring adaptors over disruptors. Success depends on distinguishing sustainable business models from speculative plays.

Some data centre operators reporting stronger-than-expected demand are upgrading earnings guidance, suggesting enterprise adoption may be accelerating faster than bears anticipate, though whether this translates to sustainable returns matching the infrastructure investment scale remains the critical question.

> Balanced Perspective

> Vanguard acknowledges “rational” exuberance with economic upside potential, estimating AI could contribute 1.2% to GDP growth. However, the firm urges diversification rather than concentrated AI bets. The takeaway is not blanket avoidance but rather sophisticated selection and risk management.

Warren Street views US equities as favourable into 2026 despite AI investment risks, contingent on inflation cooling with monetary easing. This suggests the current environment may favour selective stock-pickers over wholesale sector avoidance, with opportunity existing alongside elevated risks.

The next major ASX story will hit our subscribers first

Navigating AI Investment Risks: Key Takeaways for 2026

AI’s transformative potential doesn’t guarantee investor returns. The 2026 landscape requires distinguishing between companies positioned to benefit and those vulnerable to disruption. Zelter’s central question remains unanswered: will those funding the buildout reap proportionate rewards? The scale of investment creates both opportunity and risk, with outcomes likely varying dramatically across individual positions.

Key evaluation considerations for AI investments in 2026:

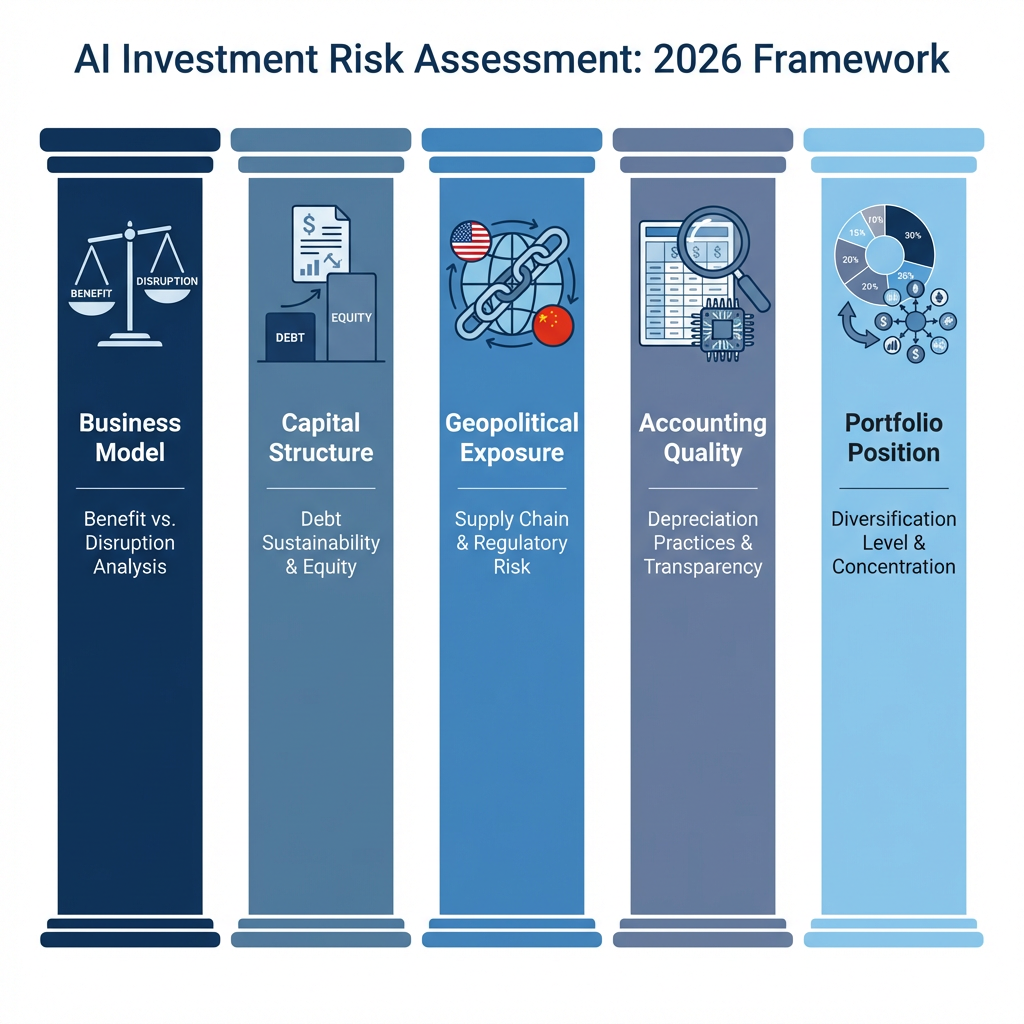

- Assess whether a company benefits from AI adoption or faces disruption from AI capabilities replacing its business model

- Evaluate debt levels and capital expenditure sustainability relative to demonstrable revenue growth and margins

- Consider exposure to US-China supply chain risks that could disrupt operations or increase costs

- Monitor accounting practices around chip depreciation and revenue recognition that may flatter near-term earnings

- Maintain diversification rather than concentrated AI bets, given the uncertain distribution of returns across the sector

The opportunity is real, but so are the AI investment risks. Institutional investors are shifting from momentum-chasing to rigorous fundamental analysis. Those who navigate carefully, distinguishing sustainable business models from speculative narratives, may find the current volatility creates entry points. Those who fail to assess these specific risk factors may discover that transformative technology doesn’t automatically translate to portfolio gains.

This article is for informational purposes only and should not be considered financial advice. Investors should conduct their own research and consult with financial professionals before making investment decisions.

Frequently Asked Questions About AI Investment Risks

Is AI a bubble in 2026?

The question of whether AI represents a bubble is nuanced. A KPMG survey found 75% of chief executives see overhype, and Howard Marks of Oaktree Capital warned about lottery-style speculation in December 2025. However, institutional views vary considerably. Vanguard sees “rational” exuberance with real economic potential, estimating 1.2% GDP growth contribution. The concern isn’t whether AI is valuable (it demonstrably is) but whether current valuations reflect realistic return expectations given the capital requirements and uncertain timeline to profitability. The situation is better characterised as elevated risk requiring appropriate compensation rather than a definitive bubble.

How much are companies spending on AI in 2026?

Consensus estimates for hyperscaler capital expenditure reached $527 billion in 2026, up from $465 billion in pre-Q3 2025 projections. Goldman Sachs projects over $500 billion in total AI investment across all sectors for the year. Apollo estimates $5 trillion to $6 trillion in US data centre investment over the next five years. These figures have been consistently revised upward as actual spending exceeds forecasts, and no major scaling back has been announced by leading technology companies.

Which AI stocks are performing well in 2026?

Performance has diverged significantly across AI-related equities. Google showed 30% gains in late 2025 with momentum extending into 2026, whilst Oracle dropped 30% and Meta declined 10% on execution concerns. Hyperscalers generally held gains whilst software and data stocks faced selloffs on disruption fears. Morgan Stanley suggests some selloffs may not match fundamentals, potentially creating opportunity. However, specific investment recommendations fall outside the scope of informational analysis.

What are the biggest risks to AI investments right now?

Key risk categories include ROI uncertainty, with spending outpacing revenue and debt financing adding pressure for near-term returns. Disruption risk affects some sectors facing replacement rather than enhancement from AI capabilities. Geopolitical risks centre on US-China chip competition fragmenting supply chains and raising costs. Economic risks include inflation from data centre energy demand and employment policy concerns. Vanguard warns of material equity downside if capital expenditure fails to deliver proportionate returns, whilst elevated valuations combined with debt create vulnerability to sentiment shifts.

Should I avoid AI investments entirely?

Most experts don’t advocate complete avoidance but rather sophisticated selection. Goldman Sachs sees opportunity in platforms and productivity stocks as adoption progresses. LSEG notes AI favours adaptors over disruptors, suggesting opportunity for companies successfully integrating the technology. Vanguard urges diversification rather than dismissal of AI themes entirely. The key is distinguishing sustainable business models from speculative plays and maintaining appropriate position sizing relative to overall portfolio risk. Specific investment decisions should be made in consultation with financial professionals based on individual circumstances and risk tolerance.

Frequently Asked Questions

What are the biggest AI investment risks in 2026?

The biggest AI investment risks in 2026 include ROI uncertainty from debt-financed capex outpacing revenue growth, disruption risk to knowledge sectors like software and finance, US-China chip supply chain fragmentation, and inflation pressures from data centre energy demand. Vanguard warns of material equity downside if the $527 billion in hyperscaler capital expenditure fails to deliver proportionate returns.

Is AI a bubble in 2026?

Most institutional analysts characterise AI in 2026 not as a definitive bubble but as elevated risk requiring appropriate compensation, with 75% of CEOs surveyed by KPMG seeing overhype yet Vanguard estimating AI could contribute 1.2% to GDP growth. The core concern is whether current valuations reflect realistic return expectations given the massive capital requirements and uncertain timeline to profitability.

How much are companies spending on AI infrastructure in 2026?

Consensus estimates for hyperscaler capital expenditure reached $527 billion in 2026, up from $465 billion in pre-Q3 2025 projections, with Goldman Sachs projecting over $500 billion in total AI investment across all sectors. Apollo Global Management estimates $5 trillion to $6 trillion in US data centre investment over the next five years.

Which sectors are most vulnerable to AI disruption risk?

Knowledge sectors including software, finance, and media face the greatest disruption risk in 2026 as AI demonstrates the ability to automate tasks previously requiring human expertise, driving broad selloffs in software and data stocks. Infrastructure and hyperscaler plays have shown resilience as providers of the underlying AI deployment stack.

Should investors avoid AI stocks entirely due to these risks?

Most leading institutions including Goldman Sachs, Morgan Stanley, and Vanguard do not advocate complete avoidance but instead urge sophisticated selection, focusing on platforms and productivity beneficiaries over speculative capex-heavy plays. The key is distinguishing sustainable business models from speculative narratives and maintaining diversified exposure rather than concentrated AI bets.