Record Highs Are Not the Risk Most Investors Think They Are

2 hrs ago

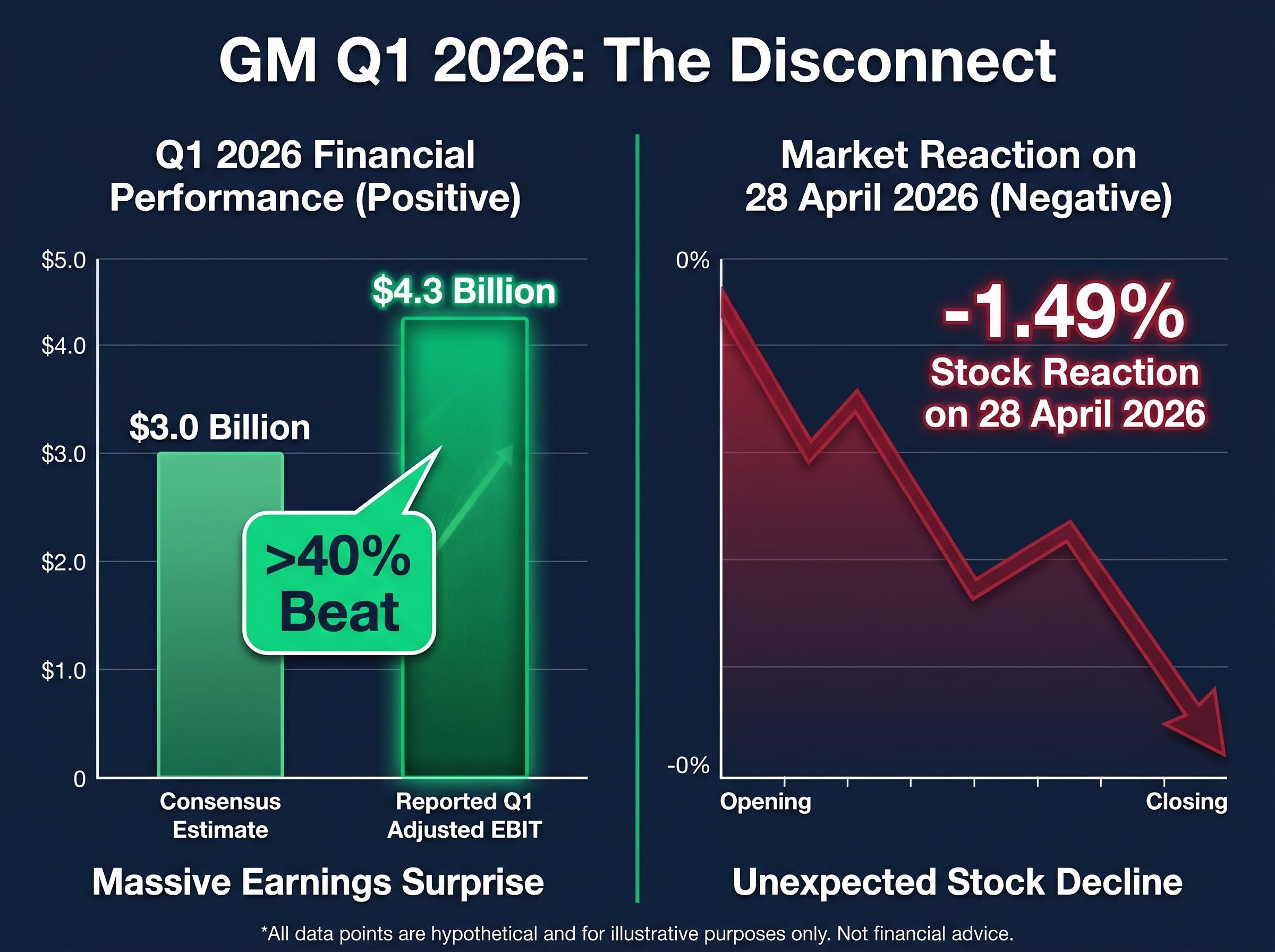

General Motors beat Wall Street on every headline metric in Q1 2026 and lifted full-year guidance, and the stock fell 1.49% on the day of the announcement. That gap between the numbers and the market’s response is where the real story sits.

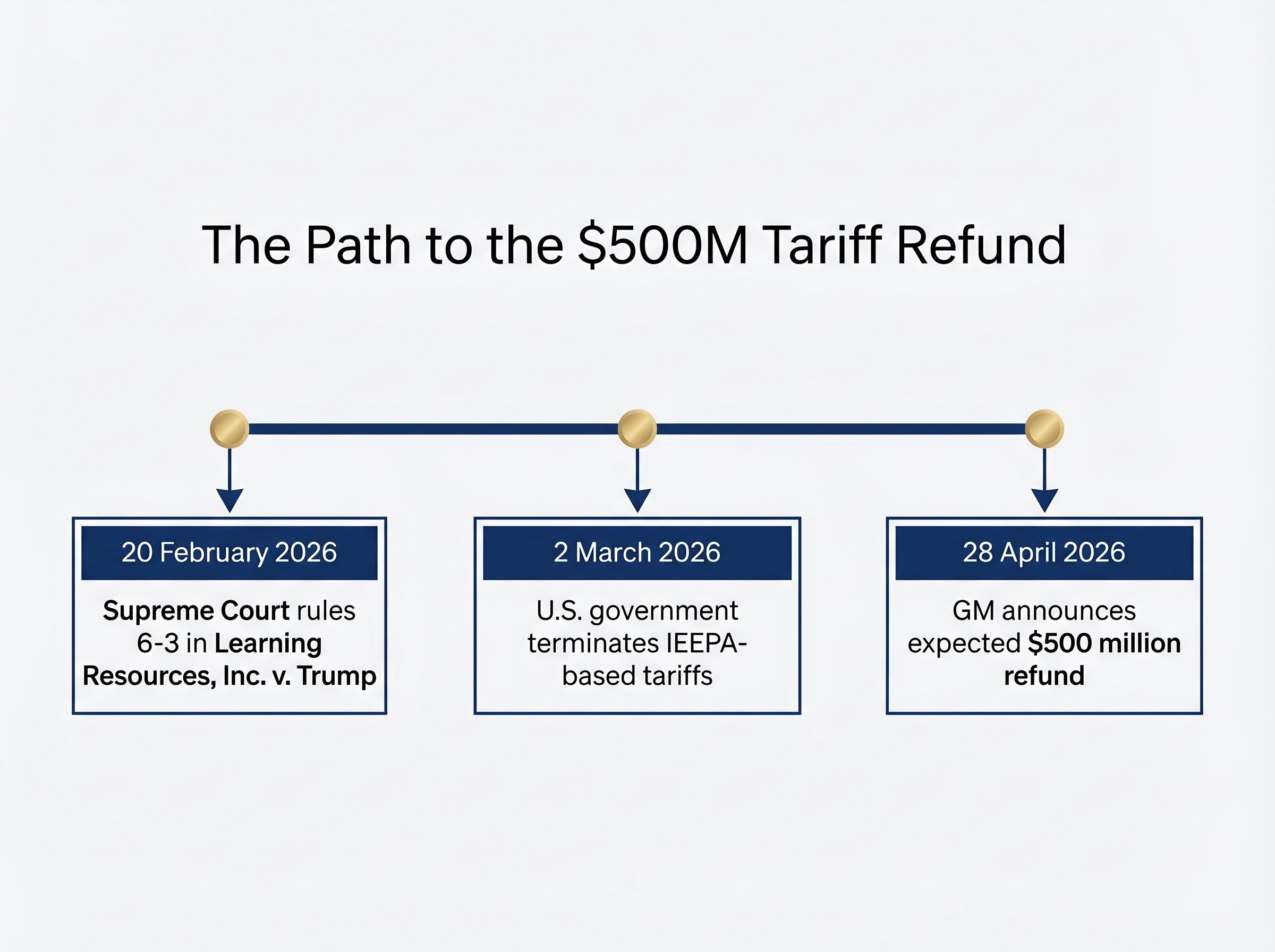

On 28 April 2026, GM reported Q1 adjusted EBIT of $4.3 billion against a consensus expectation of $3.0 billion, a beat of more than 40%. GM’s full-year adjusted EBIT guidance was revised upward to $13.5-$15.5 billion, compared with the previous range of $13.0-$15.0 billion. But GM’s own disclosures made clear that the entire guidance upgrade was attributable to a single one-time benefit: a $500 million tariff refund tied to a February 2026 Supreme Court ruling. No improvement in the underlying operational outlook was cited.

What follows is an analysis of what the GM earnings beat and guidance revision actually signal, where the $500 million came from, why rising commodity and freight headwinds of up to $2 billion complicate the second half, and how investors can distinguish windfall-driven guidance upgrades from structural earnings improvement.

The headline figures were unambiguous. GM delivered Q1 adjusted EBIT of $4.3 billion, a 9.7% margin, against a consensus estimate of $3.0 billion. The company returned $800 million to shareholders through buybacks in the quarter, with approximately $5.5 billion remaining under its repurchase authorisation.

Q1 2026 adjusted EBIT: $4.3 billion versus a $3.0 billion consensus estimate, a beat exceeding 40%.

GM attributed the outperformance to three drivers:

Then the market spoke. GM shares, which closed at $77.96 on 27 April 2026 against an average analyst price target of $94.24, declined 1.49% on 28 April. The beat was large enough to be impossible to ignore. The sell-off was small enough to suggest not panic, but doubt. Investors looked past the headline and found a question they could not resolve from one quarter’s data alone: how much of this is repeatable?

The one-time item at the centre of the guidance revision has a specific origin, and understanding the sequence matters.

The IEEPA, a law originally designed to grant the president emergency powers over international economic transactions, had been used as the legal basis for certain tariff actions. The Supreme Court’s ruling removed that authority, triggering refund claims from companies that had paid tariffs under the now-invalidated framework.

IEEPA refund claims are not unique to GM: Reliance Worldwide lodged its own claim following the same 20 February 2026 Supreme Court ruling, with the company reporting its FY26 net tariff impact tracking at the lower end of its previously flagged range, a parallel that illustrates how the ruling is flowing through corporate guidance across multiple industries simultaneously.

GM held its automotive free cash flow guidance at $9.0-$11.0 billion for full-year 2026, unchanged from the prior forecast. The reason is straightforward: GM does not yet know when the $500 million cash will actually arrive. The refund is expected, not received. By keeping cash flow guidance static, GM signalled that it is not treating the windfall as certain in its liquidity planning, a meaningful distinction for investors tracking the company’s actual cash generation capacity.

The backward-looking windfall is one side of the equation. The forward-looking cost picture is the other, and it has deteriorated since GM last issued guidance.

GM revised its commodity and freight cost headwind estimate to $1.5-$2.0 billion for full-year 2026, up from a prior projection of $1.0-$1.5 billion. The increase reflects higher raw material input costs and elevated logistics expenses that have persisted longer than anticipated.

The Strait of Hormuz blockade, which has kept Brent crude above $100 a barrel since early March 2026 despite a new Iranian diplomatic proposal delivered on 27 April, is the upstream origin of the elevated raw material and logistics costs now embedded in GM’s revised $1.5-$2.0 billion commodity and freight headwind estimate.

Revised commodity and freight headwind: $1.5-$2.0 billion, up from a prior estimate of $1.0-$1.5 billion.

Three distinct cost categories are pressuring margins:

That last figure puts the $500 million refund in proportion. It offsets roughly 12-17% of GM’s total tariff cost base for the year. GM’s stated expectation is that Q1 operational outperformance will counterbalance the rising second-half cost pressures, but that assumption places considerable weight on sustained North American margin performance through Q2 and Q3 without the assistance of another one-time item.

The arithmetic of the guidance revision is unusually transparent.

| Metric | Prior guidance | Revised guidance |

|---|---|---|

| Adjusted EBIT | $13.0-$15.0 billion | $13.5-$15.5 billion |

| Automotive free cash flow | $9.0-$11.0 billion | $9.0-$11.0 billion (unchanged) |

The midpoint of adjusted EBIT guidance rose by exactly $500 million, the same figure as the IEEPA tariff refund. GM’s own disclosure stated that the guidance upgrade was entirely attributable to the one-time benefit, with no contribution from an improved operational outlook.

GM attributed 100% of the guidance upgrade to the IEEPA tariff benefit. No operational improvement was cited.

For forward context, Wolfe Research upgraded GM to Outperform with a $96 price target on 25 March 2026, citing a 2026 EPS estimate of $12.37 and a 2027 estimate of $16.03. That trajectory assumes operational execution beyond the windfall, a path that depends entirely on the second-half cost picture GM has yet to navigate.

The GM situation offers a useful framework for evaluating any guidance revision that arrives alongside a windfall.

Operational earnings improvement is driven by volume growth, pricing power, cost efficiency, or product mix. These are recurring forces that affect future quarters. One-time regulatory or legal windfalls, by contrast, add to the current period’s reported figures without changing the company’s production capacity, competitive position, or cost structure going forward. Analysts and institutional investors typically strip out one-time items when assessing whether an earnings beat or guidance revision reflects genuine business momentum.

KPI-based earnings screening separates companies where headline beats reflect genuine operational momentum from those where a single non-recurring item is carrying the number; Morgan Stanley’s approach, which targets the single metric most likely to drive a surprise rather than accepting reported EPS at face value, is exactly the discipline the GM result rewards.

A three-step framework applies:

Step one: the $500 million midpoint increase maps directly onto the IEEPA refund. One-time, not recurring. Step two: free cash flow guidance held at $9.0-$11.0 billion, unchanged. Step three: Q1 operational performance was genuinely strong (the beat against consensus was real), but the guidance revision itself rests entirely on the windfall.

The takeaway is not that GM had a bad quarter. The Q1 beat was real. The takeaway is that the guidance upgrade was a windfall story, and investors should evaluate GM’s forward value on the operational baseline rather than the revised headline.

The Q1 results delivered genuine positives. North American margins held at 9.7%, the operational beat against a $3.0 billion consensus was substantial, and $800 million in buybacks signalled management confidence in the company’s cash generation.

Q1 adjusted EBIT margin: 9.7%. This is the operational benchmark the market will hold GM to in subsequent quarters.

Three variables will determine whether full-year guidance is achievable:

At $77.96 versus an average analyst target of $94.24, the market is pricing approximately 21% implied upside, contingent on execution. Wolfe Research’s 2027 EPS estimate of $16.03 represents the bull-case scenario, but reaching it depends on GM navigating the second-half cost pressures that the first quarter’s headline numbers did not have to face.

The asymmetric equity market risk framing that analysts applied to the Hormuz standoff, where a confirmed deal could drive a broad rally while further escalation could trigger a sharp repricing, applies with equal force to GM’s second-half outlook: a resolution that brings Brent below $90 substantially changes the commodity cost trajectory, while continued disruption entrenches the upward pressure on the freight and materials line.

The Q1 beat and the guidance upgrade are already in the rearview mirror. What matters from here is whether GM’s operational engine can sustain the margins that made the quarter genuinely strong, without the help of a one-time legal windfall to carry the numbers.

This article is for informational purposes only and should not be considered financial advice. Investors should conduct their own research and consult with financial professionals before making investment decisions. Past performance does not guarantee future results. Financial projections are subject to market conditions and various risk factors.

GM reported Q1 2026 adjusted EBIT of $4.3 billion, beating the Wall Street consensus estimate of $3.0 billion by more than 40%, with an adjusted EBIT margin of 9.7%.

GM lifted its full-year adjusted EBIT guidance to $13.5-$15.5 billion from $13.0-$15.0 billion, but the company stated the entire upgrade was attributable to a one-time $500 million IEEPA tariff refund, with no improvement in the underlying operational outlook cited.

The IEEPA tariff refund stems from a February 2026 U.S. Supreme Court ruling that found the International Emergency Economic Powers Act does not authorise presidential tariffs; GM expects to receive $500 million as a result, which accounts for the full midpoint increase in its revised earnings guidance.

Despite a substantial earnings beat, GM shares declined 1.49% on 28 April 2026 because investors recognised that the guidance upgrade was driven entirely by a one-time legal windfall rather than improved operational performance, and the company faces rising commodity and freight cost headwinds of $1.5-$2.0 billion in the second half of 2026.

Investors can apply a three-step check: confirm whether the guidance driver is one-time or recurring, compare whether cash flow guidance moved in line with earnings guidance, and assess whether volume, margin, or pricing metrics improved independently of the windfall; in GM's case, free cash flow guidance was left unchanged while earnings guidance rose by exactly the amount of the tariff refund.