What Domino’s Q1 Results Reveal About the Consumer Spending Slowdown

15 hrs ago

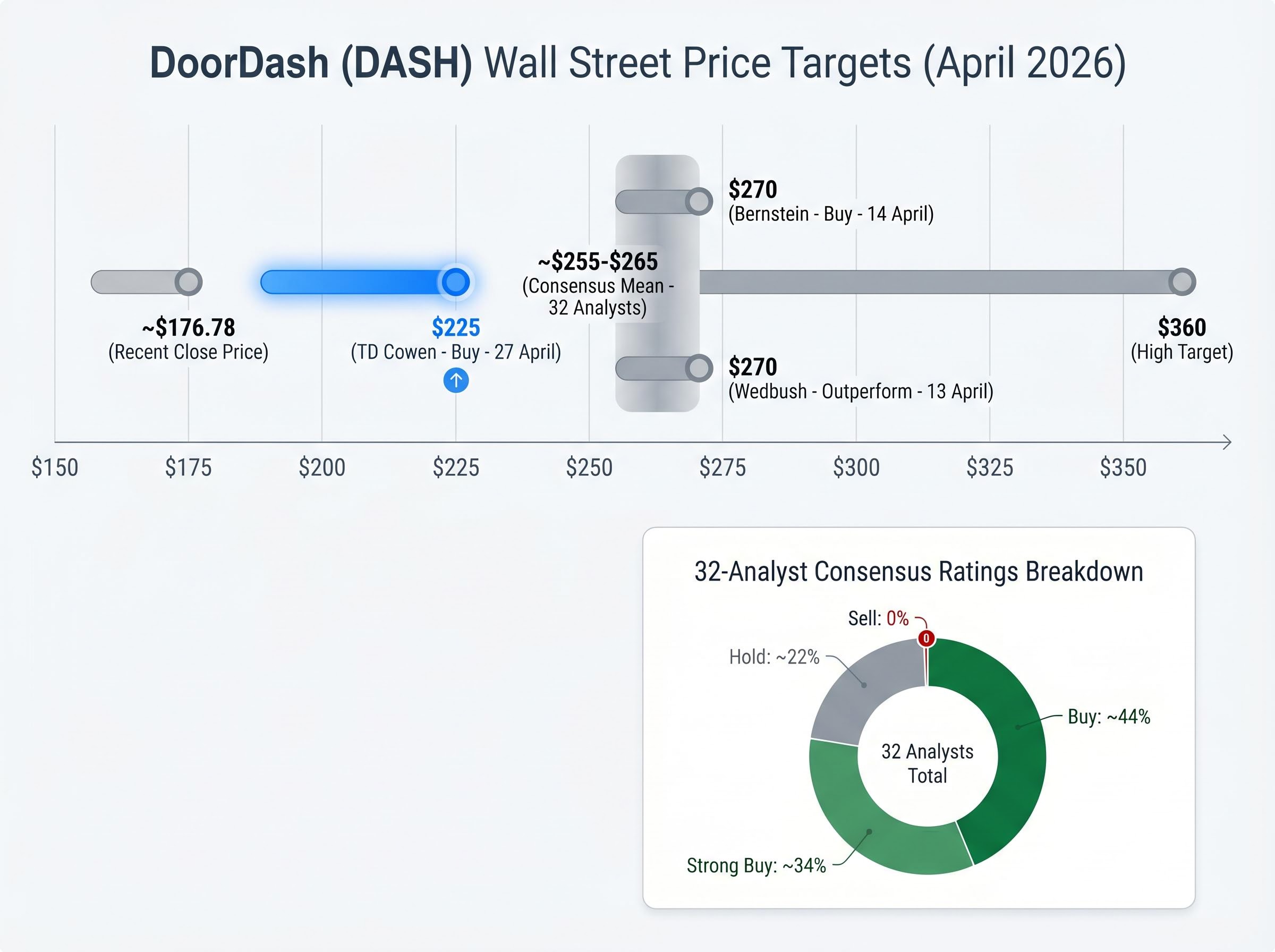

TD Cowen initiated coverage of DoorDash (DASH) on 27 April 2026 with a Buy rating and a $225 price target, implying approximately 27% upside from the stock’s recent close near $176.78. The initiation lands while DoorDash trades well below the Wall Street consensus target of roughly $255-$265, and follows a February round in which several analysts trimmed targets after Q4 2025 earnings while maintaining bullish ratings. What follows is a breakdown of TD Cowen’s specific investment case, the financial forecasts underpinning the $225 target, where that figure sits relative to broader analyst opinion, and the risks that could challenge the thesis.

TD Cowen’s initiation prices DoorDash at $225, a level that would represent roughly 27% upside from the current share price of approximately $176.78. The firm projects 18% annual revenue growth through 2030, driven by global expansion, category diversification beyond food delivery, and accelerating earnings power.

TD Cowen’s core projection: 18% annual revenue growth through 2030, underpinned by international scale, category expansion, and margin improvement.

The business being evaluated is substantial. TD Cowen’s thesis rests on a platform with:

That 18% revenue growth figure through the end of the decade is the load-bearing number in the entire investment case. It assumes DoorDash can sustain top-line momentum well beyond the current delivery boom, a claim that the remaining sections of this article will stress-test against the company’s most recent financials, its competitive environment, and the wider Wall Street consensus.

No analyst initiation exists in a vacuum, and the risks to DoorDash are neither theoretical nor distant.

The three categories investors should weigh:

The U.S. Department of Labor independent contractor classification rules under the Fair Labor Standards Act apply a multi-factor economic reality test to determine worker status, meaning that any regulatory tightening of that standard could compel platforms like DoorDash to reclassify a portion of their driver network and absorb the associated payroll cost increases.

The margin compression concern is not a distant scenario. It is already built into guidance, and Q1 results will determine whether it stabilises or deepens.

TD Cowen’s bull case is not a single-catalyst story. It is built on four reinforcing pillars:

Business of Apps 2026 food delivery market share data places DoorDash above 65% of the U.S. market, a dominance that underpins TD Cowen’s expectation of continued domestic share gains but also raises the question of how much incremental share remains available to capture from Uber Eats and smaller rivals.

The domestic story is the most immediate. TD Cowen sees DoorDash maintaining a competitive advantage through category breadth and user frequency, with grocery and retail orders increasing average transaction values alongside traditional restaurant delivery.

Wolt provides DoorDash’s footprint across European and select Asian markets, while the Deliveroo acquisition extends reach into the United Kingdom and additional territories. Together, international revenue is expected to account for a meaningfully larger share of total revenue over the medium to long term, though specific integration updates beyond January 2026 remain limited.

The advertising business may prove equally significant to the margin story. The model is straightforward: brands pay DoorDash for promoted listings and targeted placement within a platform where users are already in a purchasing mindset. TD Cowen identifies this as a high-margin growth driver that lifts order frequency, average transaction value, and overall profitability without requiring proportional increases in delivery costs.

The forward-looking analyst thesis needs to be measured against what DoorDash has already delivered. The most recent verified data point is the Q4 2025 earnings report.

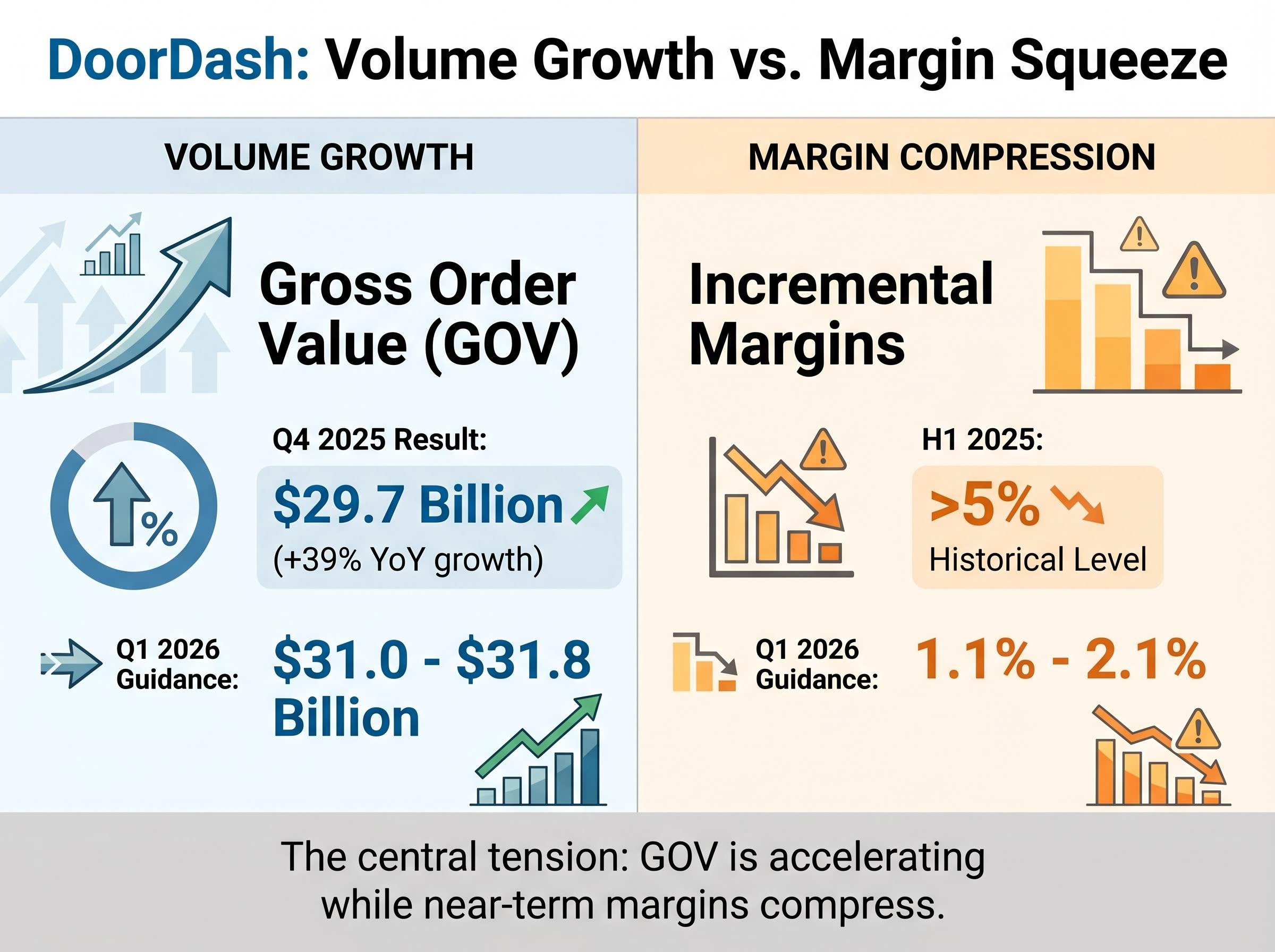

Q4 2025 headline: Gross Order Value (GOV), the total dollar value of all orders processed through the platform, reached $29.7 billion, representing 39% year-over-year growth.

That 39% GOV growth rate is the clearest signal of underlying business momentum. Adjusted earnings per share, however, missed consensus estimates, triggering an initial post-earnings stock decline before a subsequent rally of approximately 14% in extended hours as investors digested the full results.

| Metric | Q4 2025 Result | Q1 2026 Guidance | Significance |

|---|---|---|---|

| Gross Order Value | $29.7B (+39% YoY) | $31.0-$31.8B | Signals continued volume acceleration |

| Incremental Margin | >5% (H1 2025) | 1.1-2.1% | Near-term profitability pressure; source of analyst caution |

The gap between strong top-line volume growth and compressed near-term margins is the central tension in the DoorDash investment case right now. GOV, which measures the total dollar value of orders flowing through the platform, is accelerating. Margins are not keeping pace. For investors assessing whether TD Cowen’s initiation is well-timed, the Q1 2026 results against the $31.0-$31.8 billion GOV guidance range and the 1.1-2.1% margin trajectory will be the next checkpoint.

The $225 figure may sound bullish in isolation. Within the context of where Wall Street sits on DoorDash, it is actually the most conservative of recent initiations and reaffirmations.

| Analyst Firm | Price Target | Rating | Date |

|---|---|---|---|

| TD Cowen | $225 | Buy | 27 April 2026 |

| Bernstein | $270 | Buy | 14 April 2026 |

| Wedbush | $270 | Outperform | 13 April 2026 |

| Consensus Mean | ~$255-$265 | Buy | 32-analyst aggregation |

| High Target | $360 | — | — |

The consensus mean across 32 tracked analysts implies approximately 44-50% upside from the current price, placing TD Cowen’s $225 target meaningfully below the Street average. The highest target on record is $360, more than double the current share price.

The rating distribution reflects near-unanimous bullishness:

No analyst in the primary sample carries a Sell rating on DoorDash. Multiple firms, including Guggenheim, BofA Securities, and Needham, trimmed targets in February 2026 following the Q4 earnings margin guidance, but none downgraded. The question this framing raises is not whether TD Cowen is bullish, but why the stock remains roughly $80-$90 below the consensus target despite nearly universal Buy ratings.

DoorDash is not the only major US tech name where stocks trading well below unanimous buy-rated analyst consensus have become the defining puzzle for investors; Nvidia sits roughly 33% below its median Wall Street target despite 93% of covering analysts carrying a buy rating, suggesting the gap between Street optimism and market pricing reflects broader uncertainty about execution timelines rather than fundamental disagreement on long-term value.

TD Cowen’s Buy initiation with a $225 price target adds another bullish voice to an already broadly constructive analyst consensus on DoorDash. The 18% annual revenue growth projection through 2030, combined with a platform serving 56 million monthly active users across more than 40 countries, forms the foundation of a multi-year investment case built on domestic market share gains, international scale, and advertising margin expansion.

Retail investors should weigh the $225 target in the context of a consensus mean closer to $255-$265, while keeping the near-term margin compression (incremental margins guided at 1.1-2.1% for Q1 2026) and competitive risks clearly in view. The next execution checkpoint arrives with Q1 2026 earnings, where GOV performance against the $31.0-$31.8 billion guidance range and margin trajectory will determine whether the analyst optimism translates into stock price recovery.

Investors applying analyst frameworks for identifying high-upside US tech and platform stocks ahead of Q2 2026 earnings will find that Morgan Stanley’s quantitative screen flagged Datadog and DraftKings for 45% and 75% implied upside respectively from April 2026 levels, with DraftKings delivering its first GAAP profitable year in FY2025 while trading 58% below its February 2025 high, a contrarian setup that parallels DoorDash’s own positioning relative to the broader analyst consensus.

This article is for informational purposes only and should not be considered financial advice. Investors should conduct their own research and consult with financial professionals before making investment decisions. Forward-looking statements, including analyst price targets and revenue projections, are subject to change based on market developments and company performance.

TD Cowen initiated coverage of DoorDash on 27 April 2026 with a Buy rating and a $225 price target, implying approximately 27% upside from the stock's then-current price near $176.78.

TD Cowen's $225 target is actually the most conservative among recent analyst initiations and reaffirmations; the consensus mean across 32 tracked analysts sits closer to $255-$265, implying 44-50% upside from current levels.

Several analysts lowered their DoorDash price targets in February 2026 following Q4 2025 earnings guidance, which revealed that Q1 2026 incremental margins were expected to fall sharply to 1.1-2.1%, down from over 5% in the first half of 2025, though all maintained bullish ratings.

TD Cowen's bull case rests on four pillars: domestic market share expansion over Uber Eats and Instacart, international growth via the Wolt and Deliveroo acquisitions, a high-margin advertising revenue stream, and AI-driven technology investment expected to improve unit economics through 2030.

The most immediate risk is near-term margin compression: DoorDash guided Q1 2026 incremental margins at just 1.1-2.1%, a steep decline from over 5% in H1 2025, making the upcoming Q1 2026 earnings report the next critical checkpoint for investors.