Delivery Hero Shareholders Reject Uber’s €33 Bid, Demand €40+

4 hrs ago

Morgan Stanley has kept Meta on its top picks list with a $775 price target, but the reasoning behind that call has almost nothing to do with the cloud announcement dominating headlines this week.

On 5 July 2026, Meta disclosed plans to enter the cloud computing market, positioning itself as a potential rival to AWS, Azure, and Google Cloud. The announcement captured investor attention and generated considerable noise. Morgan Stanley’s analyst team looked at the same news and reached a pointed conclusion: cloud is a sideshow. The real bull case rests on a different set of products entirely, and whether you should be positioned in Meta depends on understanding that distinction clearly.

Here is the actual architecture of Morgan Stanley’s investment thesis, what separates the durable drivers from the secondary ones, and the specific milestones that would signal whether the thesis is tracking. This is the framework for evaluating Meta stock on its own terms, not through the lens of whatever headline happens to be loudest.

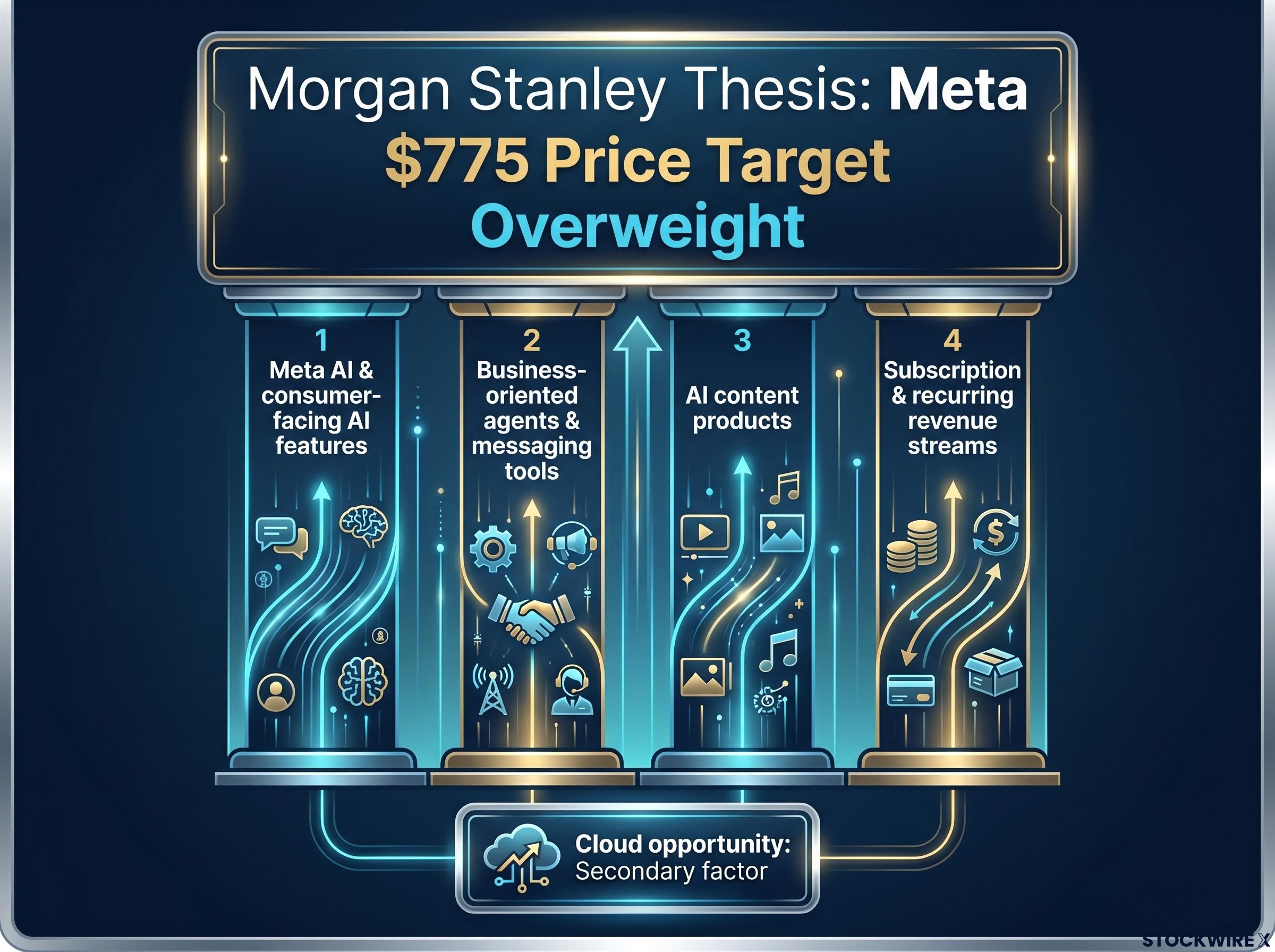

Morgan Stanley rates Meta Overweight, designates it a top pick, and sets a $775 price target. None of those calls rest on cloud infrastructure. The rating’s foundation is a multi-year product-scaling story across four specific categories, and each one ties back to Meta’s existing user base and app ecosystem rather than to competing with hyperscalers.

Morgan Stanley’s research rating methodology uses a three-tier system of Overweight, Equal-weight, and Underweight rather than conventional Buy, Hold, or Sell designations, a distinction that matters when interpreting the firm’s conviction level behind its Meta top-pick designation.

The four product pillars driving the thesis:

Morgan Stanley characterises the cloud opportunity as a “secondary factor,” a temporary earnings cushion while these core products scale. That distinction between what is driving the rating and what is generating headlines is the first thing you need to internalise before making any position decision. If you anchor your conviction to cloud market share, you are watching the wrong variable.

A list of product categories only becomes investable when you can see how each one converts users into revenue. Morgan Stanley tracks specific progress metrics here: active users, engagement, monetisation per user, and subscription attach rates. Evidence of scaling across these categories is, in the firm’s framework, the primary driver of outperformance and multiple expansion.

Meta AI functions as both an engagement deepener and an ad effectiveness amplifier. The more time users spend inside Meta’s apps interacting with AI features, the more targeting data the ad platform collects and the more ad inventory it creates.

Business agents and messaging tools represent an expansion of an existing customer relationship rather than a cold start. Small and medium-sized businesses already spend on Meta for marketing. Agents give them a reason to spend more, handling customer interactions directly inside the platforms they already use.

That subscription and agent-monetisation layer is not just a growth story. It is a multiple story. A meaningful revenue mix shift toward recurring streams would likely re-rate the stock even before earnings per share move materially, because the market assigns higher multiples to predictable revenue. If you are tracking quarterly results, these are the lines that tell you whether the thesis is progressing.

Meta’s cloud announcement deserves a fair hearing. The company plans to leverage excess data centre capacity to sell AI computing power, and two distinct models are under consideration. Morgan Stanley treats them very differently.

| Cloud model | Market comparison | Incremental risk | Upside potential | Relevance to MS thesis |

|---|---|---|---|---|

| Neocloud (raw GPU compute) | CoreWeave and similar providers | Lower: leverages existing infrastructure | Moderate: earnings cushion | Secondary; supports capex absorption |

| Full-stack hosted API service | AWS Bedrock, Azure, Google Cloud | Higher: competes with mature ecosystems | Large if successful | Not required for bull case |

The neocloud option is lower incremental risk because it builds on infrastructure Meta is already deploying for its own AI workloads. The full-stack platform would mean competing head-on with AWS, Azure, and Google Cloud, each with years of enterprise reliability track records and developer ecosystems.

The Meta Compute announcement, confirmed by Zuckerberg at the May 2026 shareholder meeting, describes two structurally different revenue models: a hosted AI platform comparable to AWS Bedrock and raw GPU compute leasing comparable to CoreWeave, each carrying distinct margin profiles and competitive implications for the existing hyperscaler ecosystem.

Morgan Stanley views cloud as a secondary, attention-grabbing development rather than the core of the investment story. The firm’s Overweight rating is built on Meta’s first-party product roadmap, not on whether the company can establish itself as a hyperscale cloud rival.

If you are watching Meta’s cloud progress, track it as an optionality layer on top of the core thesis. It is not the variable that determines whether the Overweight rating is right or wrong. That separation prevents a specific cognitive error: abandoning a sound investment case if the cloud buildout encounters early friction that has no bearing on the actual drivers of the stock.

The numbers are large. The question is whether they are alarming or logical.

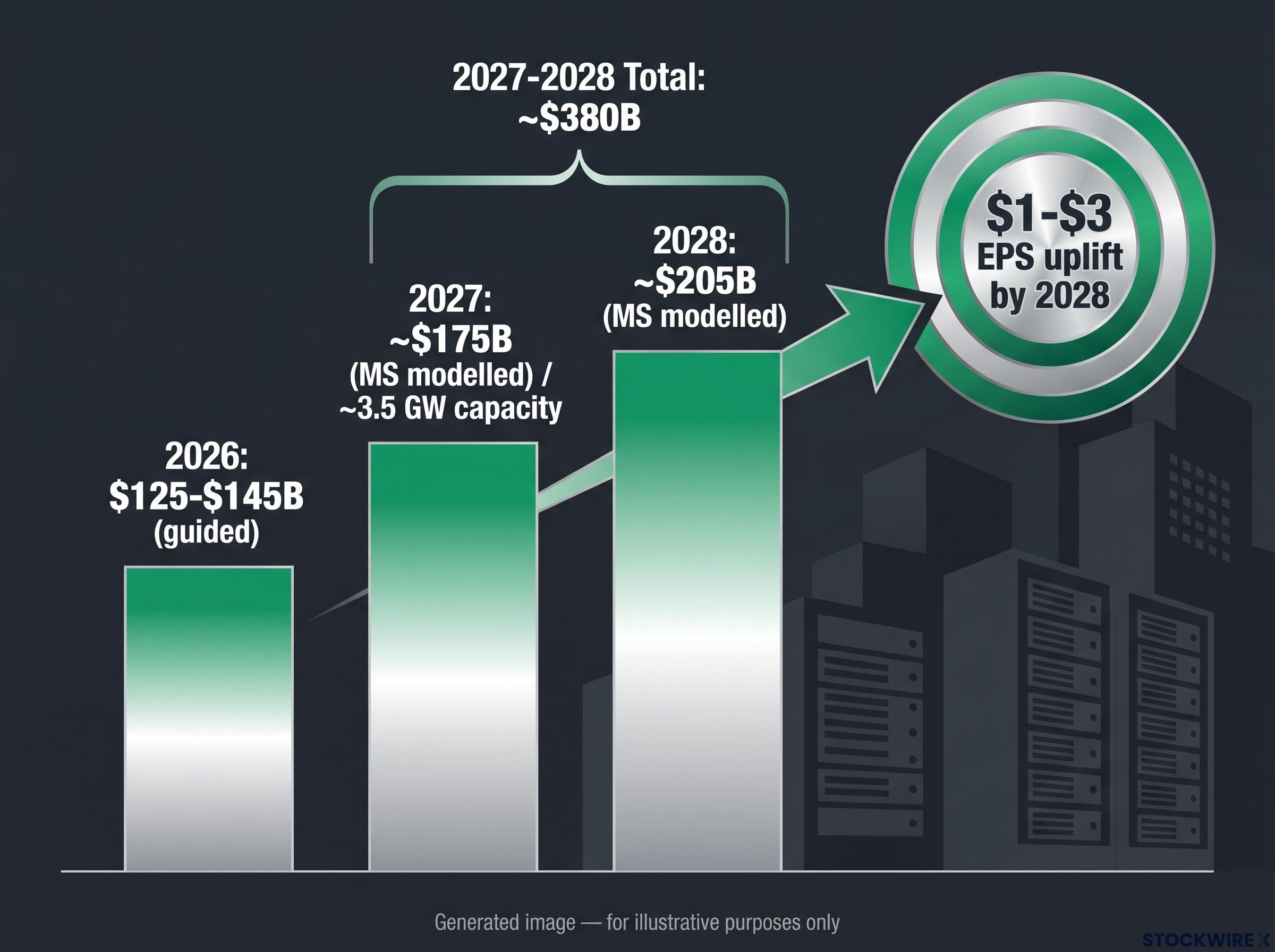

Meta guided 2026 capital expenditure (the money a company spends on physical assets like data centres and servers) at $125-$145 billion, raised during the year from an initial $115-$135 billion range. In Morgan Stanley’s model, spending climbs to around $175 billion in 2027 and roughly $205 billion in 2028, with 2027 capacity additions of approximately 3.5 GW, bringing the combined 2027-2028 total to around $380 billion.

| Year | Capex figure | Key assumption | EPS impact |

|---|---|---|---|

| 2026 | $125-$145B (guided) | First-party AI product infrastructure | Foundation year |

| 2027 | ~$175B (MS modelled) | ~3.5 GW capacity addition; AI scaling | EPS trajectory building |

| 2028 | ~$205B (MS modelled) | Full-scale AI product monetisation | $1-$3 EPS uplift |

Morgan Stanley projects that this spending could translate into a $1-$3 earnings per share uplift by 2028, on the condition that the capital is directed at scaling Meta’s own AI products rather than building out a full hyperscale cloud platform for third-party use.

The assumption underpinning these figures matters. Morgan Stanley models this capex as primarily supporting Meta AI, business agents, messaging workloads, and internal AI development. If Meta pursues a full Bedrock-style cloud offering at scale, the 2027-2028 figures would likely need to be revised higher, amplifying both upside and execution risk.

The $380 billion is large enough to be alarming in isolation. In Morgan Stanley’s framework, it is the precondition for the EPS uplift that would justify the current valuation. Investors who treat capex purely as a liability column without modelling the corresponding earnings contribution will systematically undervalue Meta under this thesis.

The capex-driven free cash flow repricing that followed Meta’s Q1 2026 earnings call cut analyst free cash flow estimates from approximately $35 billion to $25 billion, illustrating precisely the cost-lens framing Morgan Stanley argues investors must move beyond if the 2027-2028 EPS uplift is to be recognised in the multiple.

Understanding the thesis is one step. Monitoring whether it is tracking is the step that actually protects your capital. Morgan Stanley identifies five stock drivers that convert directly into observable milestones you can check quarter by quarter:

Morgan Stanley sees a necessary narrative shift here. The market currently frames Meta’s spending through a cost lens. The thesis works when that frame flips to an asset lens. If quarterly disclosures are not showing movement on engagement, agent monetisation, or subscription adoption, the thesis is not tracking, regardless of how the cloud narrative develops.

The Morgan Stanley bull case is a product-execution bet. It stands or falls on Meta AI, agents, messaging tools, and subscriptions scaling into meaningful revenue lines, not on whether Meta can compete with AWS for enterprise cloud contracts.

The $775 price target and the $1-$3 EPS uplift by 2028 are the quantitative anchors. The $380 billion in projected 2027-2028 capex is the scale of the bet you are implicitly endorsing by holding the stock.

A sum-of-parts valuation matters here because the widely cited consolidated price-to-earnings multiple is inflated by Reality Labs losses, making the Family of Apps segment’s standalone multiple substantially lower and more directly comparable to the AI-driven earnings trajectory Morgan Stanley is modelling for 2027-2028.

The $775 target and the projected $1-$3 EPS uplift by 2028 function as linked benchmarks in Morgan Stanley’s framework: the capex cycle must deliver that earnings improvement to validate the price target. A spending programme that fails to produce corresponding earnings growth would indicate the investment was sized too aggressively.

What would functionally challenge the thesis: sustained failure to scale Meta AI engagement, absence of agent monetisation evidence through 2027, or capex escalating without corresponding EPS trajectory improvement. The cloud announcement, if it progresses toward a full platform, represents optionality that could provide upside beyond the $775 target, but also requires monitoring for capex revision risk.

If you understand which variables actually govern the thesis outcome, you can hold through cloud-related volatility with conviction, or exit early if the product milestones stop arriving. That is the difference between a positioned investor and one reacting to noise.

For investors wanting to stress-test the capex-as-asset argument against historical precedent, our deep-dive into Meta’s AWS investment cycle comparison examines whether the current infrastructure build more closely mirrors Amazon’s early AWS runway or the 2021-2022 metaverse overbuild, including the five-year return range modelled across conservative and base-case scenarios.

This article is for informational purposes only and should not be considered financial advice. Investors should conduct their own research and consult with financial professionals before making investment decisions. Financial projections are subject to market conditions and various risk factors.

Morgan Stanley has set a $775 price target on Meta, rating it Overweight and designating it a top pick, with the bull case built on Meta AI, business agents, messaging tools, and subscription revenue rather than the company's cloud computing entry.

Morgan Stanley views Meta's cloud entry as an earnings cushion that absorbs excess data centre capacity, not a structural driver of the Overweight rating; the firm's thesis stands or falls on first-party AI products scaling into meaningful revenue, not on Meta winning enterprise cloud contracts from AWS or Azure.

Morgan Stanley models Meta's capex at approximately $175 billion in 2027 and $205 billion in 2028, a combined $380 billion over two years, with the firm projecting that spending translates into a $1-$3 earnings per share uplift by 2028 if directed at first-party AI product scaling.

The five key indicators are: Meta AI engagement growth, business agent adoption and monetisation per advertiser, subscription attach rates as a share of total revenue, quarterly EPS trajectory improvement, and analyst commentary signalling a shift from capex-as-cost to capex-as-asset framing.

The neocloud model leases raw GPU compute (comparable to CoreWeave) using existing infrastructure, carrying lower incremental risk; the full-stack hosted API service would compete directly with AWS Bedrock, Azure, and Google Cloud, carrying higher execution risk and requiring substantially greater investment.