Goldman’s 3 Watchpoints for Europe’s Earnings Season

7 hrs ago

Uber has publicly offered €33 per share for Delivery Hero, valuing the Berlin-based food delivery operator at roughly €10 billion. The market has already priced the stock above €37. And Uber has spent the past several weeks buying up nearly 37% of the company’s shares.

Those three facts, taken together, tell you the two sides are still far apart on price, and that Uber is not walking away.

The disclosure of Uber’s indicative bid in late May 2026 transformed Delivery Hero from a struggling operator under new leadership into one of the most closely watched M&A situations in European tech. Uber’s simultaneous stake-building, including the purchase of Aspex Management’s block, means this is no longer a tentative approach. It is an active campaign with billions in irreversible financial commitment on the acquirer’s side. Here is what the price action, the stake mechanics, and the valuation gap actually tell you about where this deal is heading and what it means if you hold either stock.

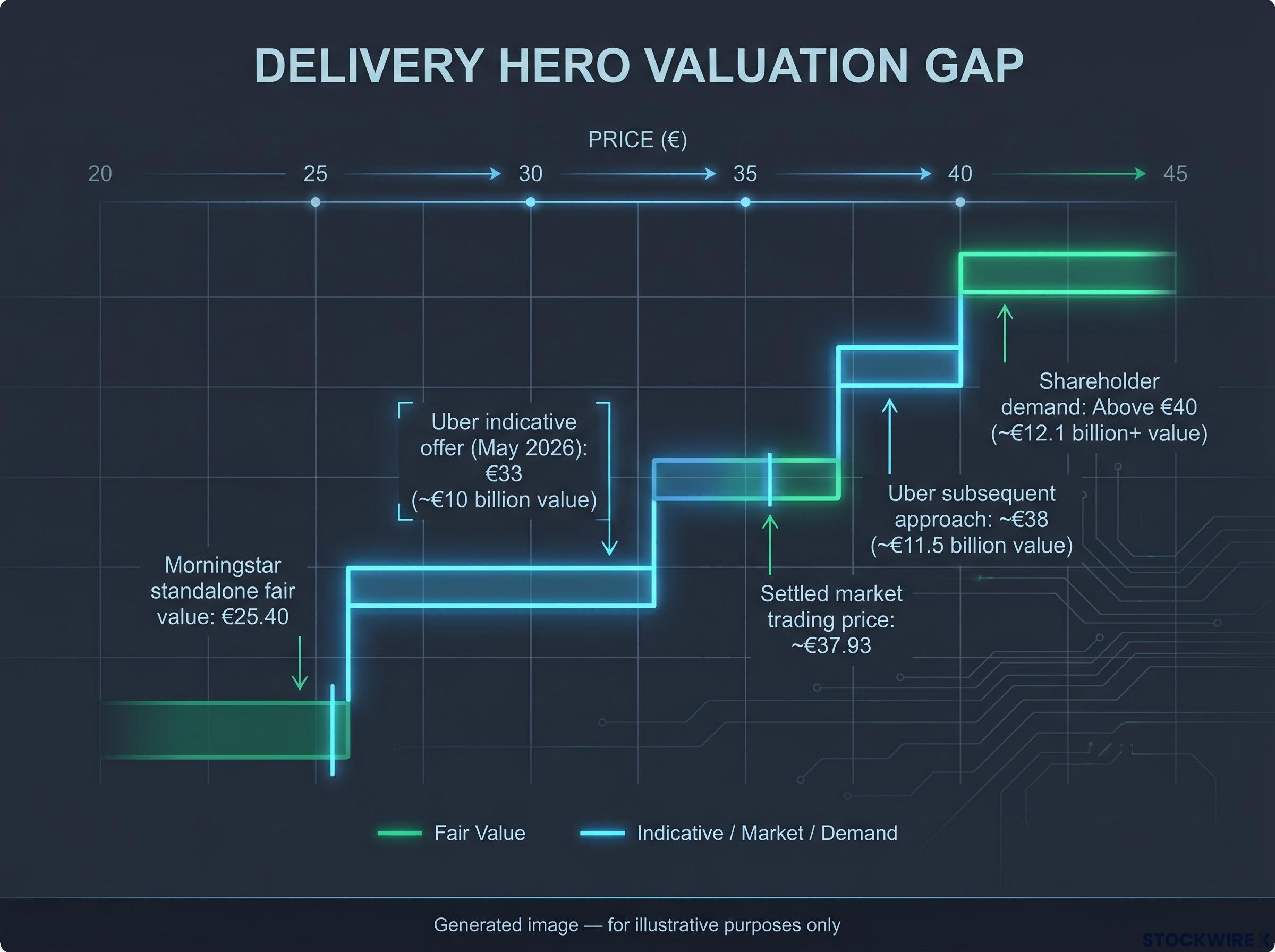

The €33-per-share indicative offer, disclosed by Delivery Hero in late May 2026, was the opening move. With the euro trading at €0.8745 to the dollar, each share equates to roughly $37.74, placing the implied equity value of the company at approximately €10 billion (or around $11.6 billion).

Scale of the deal: At €33 per share, Uber’s indicative offer values Delivery Hero at approximately €10 billion, making this one of the largest food delivery acquisitions ever attempted in Europe.

Delivery Hero’s board rejected it. Uber then approached at least one large shareholder at around €38 per share. That was rebuffed too. Key shareholders are now demanding a price above €40.

| Offer level | Status | Implied equity value |

|---|---|---|

| €33 per share | Rejected by DHER board | ~€10 billion (~$11.6 billion) |

| ~€38 per share | Rebuffed by large shareholder | ~€11.5 billion |

| Above €40 per share | Shareholder target; no offer at this level | ~€12.1 billion+ |

No binding agreement has been announced. The €2-plus gap between Uber’s last reported approach and what shareholders are demanding is the single most important number in this story right now, because it defines the probability-weighted range of outcomes for investors on both sides.

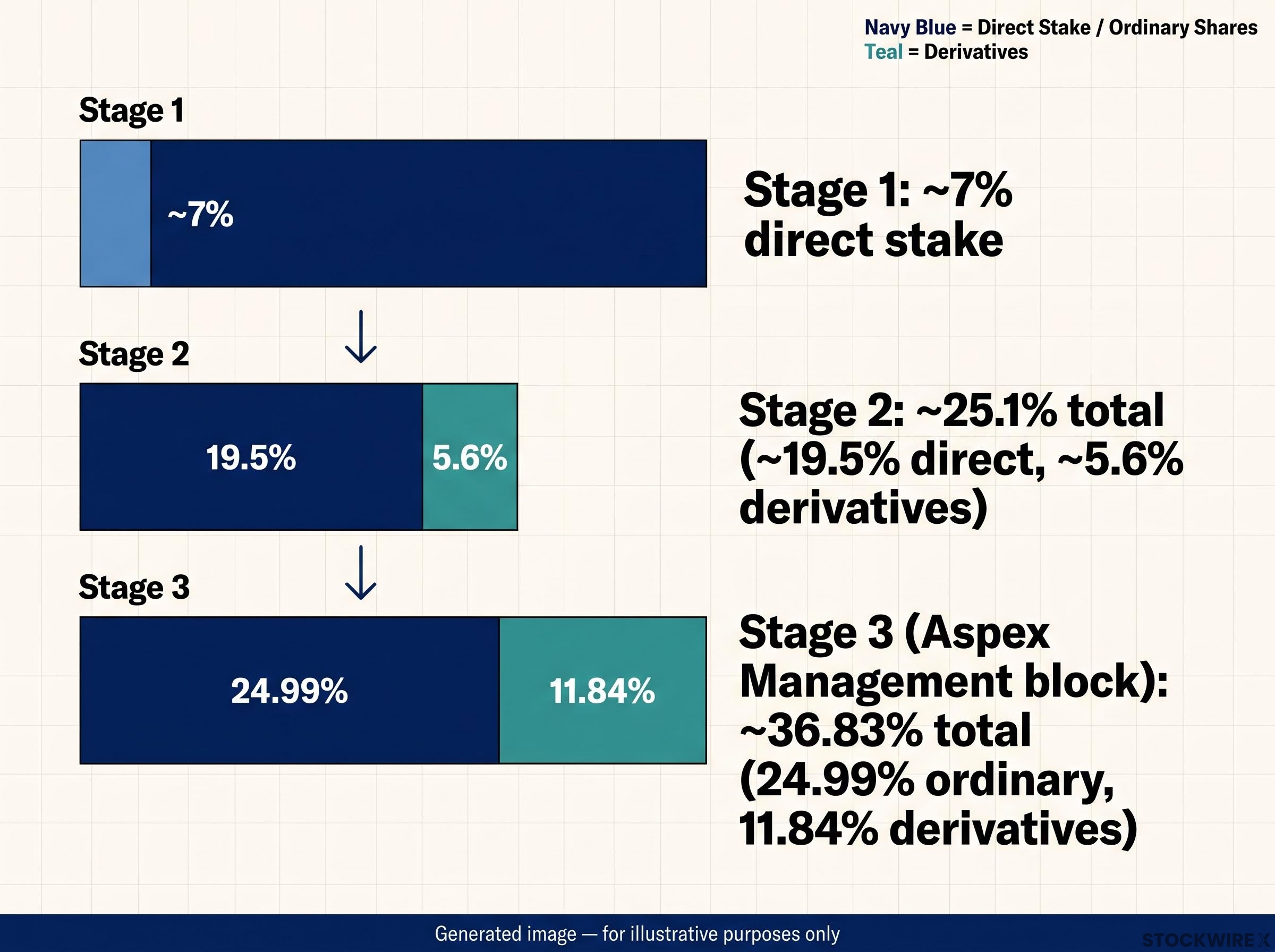

The stake build happened in three distinct stages, and each one raised the pressure.

The Aspex transaction is worth pausing on. At least one institutional shareholder was willing to sell around prevailing market prices rather than hold out for a higher bid. That sets a reference point for other holders weighing the same decision.

A nearly 37% stake means Uber has already committed billions to this campaign and now holds a position that makes a rival takeover structurally difficult. Any competing bidder would need to accumulate shares in a market where the largest holder is the other acquirer. That shifts negotiating power in ways that are not fully visible in the headline offer price, and it tells Delivery Hero investors that the most likely buyer is the one already at the table.

After the bid became public, Delivery Hero shares surged more than 10%, with intraday peaks around €37.16 to €37.85 in Frankfurt trading. Subsequent trading settled around €37.93, comfortably above Uber’s €33 indicative offer.

That would seem straightforward, except for one number that complicates the picture.

Morningstar estimates Delivery Hero’s standalone fair value at €25.40 per share, characterising the company as “no-moat,” suggesting structural competitive and profitability challenges absent a takeover.

The gap between €25.40 and €37-plus is roughly €12 per share. That is not fundamental value. It is deal premium and optionality. Investors buying or holding above €37 are placing a bet that Uber will raise its offer materially, not that Delivery Hero’s underlying business justifies the current price on its own.

Price-to-value gaps of this magnitude, roughly 50% between Morningstar’s standalone estimate and current trading levels, are a recurring feature of event-driven situations where deal optionality becomes the primary pricing input and fundamental analysis temporarily becomes secondary to bid probability assessments.

Uber shares retreated by roughly 2.4% when the disclosure hit markets.

The three scenarios investors are implicitly pricing:

If you are holding Delivery Hero above €37, you should be clear about which scenario you are betting on, because the gap between outcomes two and three is more than €12 per share.

Delivery Hero, headquartered in Berlin, operates food delivery platforms across Europe, the Middle East, and Asia. Those are precisely the geographies where Uber Eats has limited or no meaningful penetration, and where building from scratch would be slow and expensive.

The timing was not incidental. Co-founder and CEO Niklas Ostberg stepped down amid activist involvement, leaving the company mid-strategic review and creating a window that strategic buyers rarely get with operators of this scale.

Uber Eats commercial partnerships, including the exclusive multi-year arrangement locked in with Guzman y Gomez across Australia in early 2026, show the platform’s appetite for cementing delivery channel dominance through exclusive agreements rather than open-marketplace competition, a dynamic that gives the Delivery Hero acquisition a strategic logic extending beyond simple geographic expansion.

Uber’s strategic rationale comes down to four drivers:

This sits within a broader wave of food delivery consolidation. DoorDash acquired Deliveroo. Prosus bought Just Eat. The sector is restructuring around fewer, larger players, and Uber does not want to be the one left building while its competitors are buying.

For investors assessing whether Uber is overpaying, the question is not just the deal price in isolation. It is whether acquiring this footprint at a premium is more or less expensive than building comparable coverage from scratch across competitive European and Middle Eastern markets.

The split reaction on announcement day, Delivery Hero up more than 10% and Uber down approximately 2.4%, is the market’s clearest signal. It views this, at least initially, as a transfer of value from acquirer to target. The question is whether long-term synergies reverse that equation.

The split market verdict on announcement day follows a pattern seen in other contested cross-sector bids: the unsolicited bid mechanics that drove a 5.3% rise in eBay shares and a 7.5% fall in GameStop shares on the same day illustrate how acquirer and target shareholders routinely face opposite risk-reward profiles when deal terms remain unresolved.

The two shareholder groups face fundamentally different risk-reward profiles, and treating this as a single story leads to mispriced positions on both sides.

| Shareholder group | Key considerations |

|---|---|

| DHER | Upside depends on Uber raising bid toward €38-€40+ |

| DHER | Downside is reversion toward Morningstar’s €25.40 standalone estimate if deal collapses |

| DHER | Monitor M&A spread: gap between trading price and any revised offer level signals deal confidence |

| UBER | Acquisition price discipline is the primary risk; shareholder demands could push final price to levels where synergies cannot justify the premium |

| UBER | Financing structure (all-cash vs. cash plus stock) is undisclosed and will materially affect EPS, leverage, and balance sheet flexibility |

| UBER | Track management’s quantified synergy targets and ROIC framework once available |

DHER is now an event-driven position. UBER is a capital allocation question. Both require distinct frameworks, and investors holding either need to decide which scenario they are positioned for.

Three unresolved variables will determine whether this deal closes, and at what price.

The EU Merger Regulation establishes the mandatory notification thresholds and review powers that would apply to a combined Uber-Delivery Hero entity, with the European Commission holding authority to require divestitures in specific national markets as a condition of clearance.

Uber has made a credible, escalating financial commitment. Nearly 37% of Delivery Hero is already in its hands, multiple offers have been tabled, and the gap is narrowing. But the distance between what Uber has offered and what key shareholders demand means no outcome is certain.

Three variables will determine the next phase: a revised formal offer price above €38, the financing structure Uber discloses (all-cash versus cash plus stock), and any regulatory feedback from EU or national competition authorities. Those are the signals worth tracking; individual headlines between them are noise.

The broader signal is structural. Food delivery is consolidating globally, and Uber is betting that scale, not competition, is the path to profitability. Whether it pays the right price for that bet is the question that matters for both sets of shareholders.

This article is for informational purposes only and should not be considered financial advice. Investors should conduct their own research and consult with financial professionals before making investment decisions. These statements regarding potential deal outcomes are speculative and subject to change based on market developments and company performance.

Uber's indicative offer is €33 per share, valuing Delivery Hero at approximately €10 billion. The board rejected it, and Delivery Hero shares are trading above €37, reflecting market expectations that Uber will need to raise its bid significantly.

Uber holds approximately 36.83% of Delivery Hero, split between 24.99% in ordinary shares and 11.84% in derivatives, making it the company's largest shareholder after a three-stage accumulation campaign that included purchasing Aspex Management's block.

The market is pricing in the probability that Uber will raise its bid toward €38-€40 or higher; investors holding above €37 are betting on a revised deal rather than Delivery Hero's standalone value, which Morningstar estimates at just €25.40 per share.

If the deal collapses, Delivery Hero shares would likely revert toward Morningstar's standalone fair value estimate of €25.40 per share, representing a decline of more than €12 from current trading levels above €37.

Delivery Hero operates food delivery platforms across Europe, the Middle East, and Asia, precisely the geographies where Uber Eats has limited penetration; acquiring the company gives Uber instant geographic scale and removes a direct competitor, which Uber views as cheaper than building comparable coverage from scratch.