Global X Releases 26 ASX ETF Distribution Estimates Ahead of 3 July

1 hr ago

Meta shares climbed approximately 8% on 1 July 2026 after Bloomberg reported that the company is constructing a cloud division to sell spare AI computing capacity to outside buyers. The move, if executed, would position Meta as a fourth major American hyperscaler alongside Amazon, Microsoft, and Google, and the market’s reaction suggests investors are treating the possibility with real conviction.

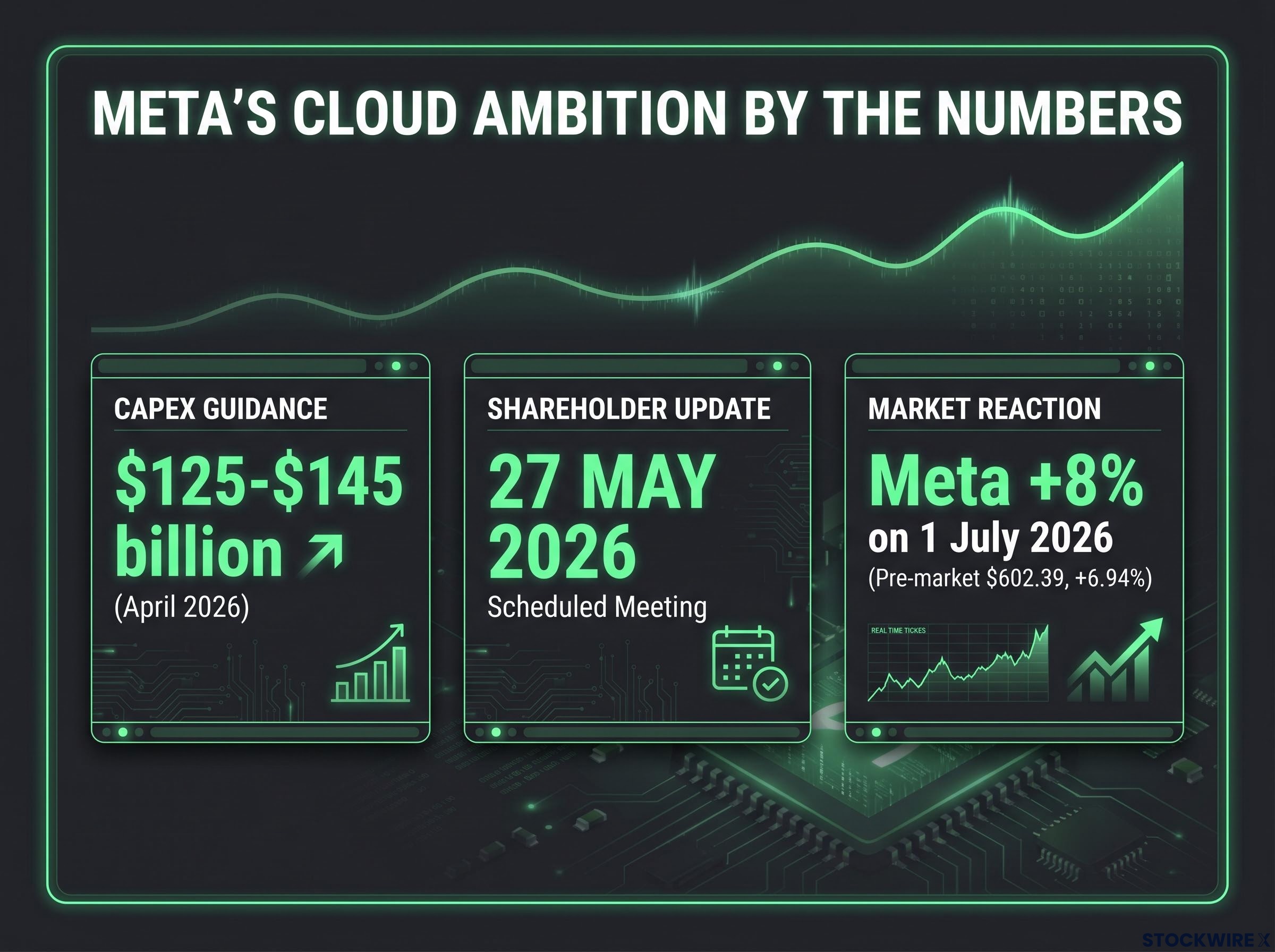

This is not a speculative rumour. Mark Zuckerberg told shareholders on 27 May 2026 that a cloud business is “definitely on the table,” and the company has a $125-$145 billion capital expenditure programme already under construction to back it up. The story sits precisely where Meta’s AI ambitions meet its concentration risk in advertising revenue.

Here is what Meta is actually planning, how seriously the initiative should be taken at this stage, and what the announcement means for the hyperscaler stocks that sold off today.

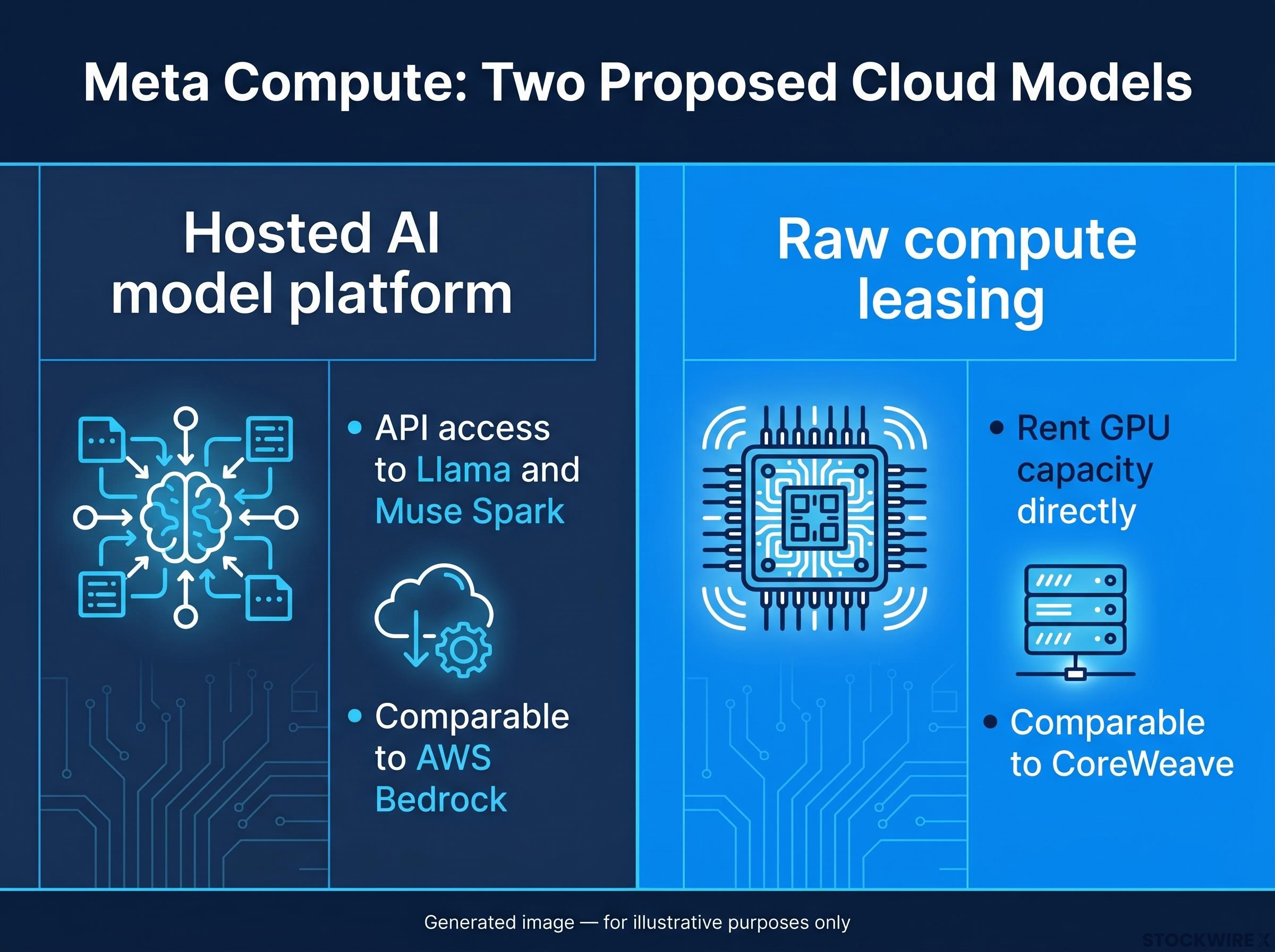

According to Bloomberg, citing individuals with knowledge of the matter, Meta is developing two distinct cloud revenue models under an internal initiative called Meta Compute. Neither has a confirmed launch date, pricing structure, or disclosed customer pipeline as of 1 July 2026. The distinction between them matters because they target very different buyers and carry different margin profiles, and which path Meta pursues will shape how disruptive it can be to incumbents.

Hosted AI model platform:

Raw compute leasing:

| Model | How it works | Comparable product | Primary customer type |

|---|---|---|---|

| Hosted AI model platform | Meta runs infrastructure; customers access models via APIs | AWS Bedrock | AI developers, startups, enterprises |

| Raw compute leasing | Customers rent GPU capacity and run own workloads | CoreWeave | Sophisticated enterprises, AI startups |

Which model Meta ultimately leads with will determine whether it competes primarily on AI model quality or on infrastructure price and availability. Those are very different competitive positions, and investors should watch for which one gets a formal product announcement first.

Start with the spending. Meta raised its 2026 capital expenditure guidance to $125-$145 billion at its April 2026 earnings release, directed primarily at AI data centres and related infrastructure. That figure alone places Meta’s infrastructure investment in the same tier as the established hyperscalers, and it was committed before the cloud business was formally reported.

Meta’s $125-$145 billion buildout is running directly into AI infrastructure binding constraints, particularly power availability and cooling density, where multi-year grid interconnection delays mean physical capacity may prove harder to scale than the company’s spending commitment suggests.

Then came the public signal. At Meta’s annual shareholder meeting on 27 May 2026, Zuckerberg made the strategic logic explicit.

“A Meta-owned cloud business is definitely on the table. If we overbuild compute, we can sell or rent that extra capacity rather than leave it idle.”

Mark Zuckerberg, Meta Annual Shareholder Meeting, 27 May 2026

Zuckerberg also noted that external companies are already approaching Meta asking for API services or compute they could purchase at a premium. That detail is significant: demand is pulling this initiative forward, not just internal supply-side logic. Companies are seeking access to Meta’s infrastructure before a formal product exists.

The strategic parallel is direct. Amazon built AWS by commercialising internal infrastructure. Microsoft and Google followed the same path. Meta is not making a cold start into cloud; it is considering whether to monetise capacity it is already building at hyperscaler scale. That reframes the announcement from a surprising pivot to something closer to a logical next step, and it matters for how investors should weight the probability of execution.

The market Meta is considering entering is not fragmented. It is concentrated, mature, and defended by players with decade-long enterprise trust relationships.

AWS holds approximately 28-31% of global cloud infrastructure market share as of Q1 2026, according to Synergy Research Group. Microsoft Azure and Google Cloud together control another significant portion of the remainder. The three incumbents collectively dominate enterprise cloud spending worldwide.

Their structural advantages are specific and hard to replicate quickly:

The competitive context sharpened considerably in Q1 2026, when hyperscaler earnings revealed AWS carrying a $364 billion backlog and Google Cloud posting 63% year-over-year growth, figures that illustrate precisely the entrenched demand relationships Meta would need to compete against.

Shares of Amazon, Microsoft, and Google experienced downward pressure on 1 July 2026 following the Bloomberg report, reflecting immediate competitive concern.

One detail worth noting: Meta is itself a major cloud customer. The company has signed multi-billion-dollar deals with cloud providers to access TPUs and GPUs for its own AI workloads. It understands the buyer experience, the pricing dynamics, and the service gaps from the customer side. That perspective is an asset few new entrants bring.

Still, the competitive threat Meta poses is measured over years, not quarters. Winning enterprise contracts requires trust, compliance infrastructure, and support capabilities that take time to build. Investors in hyperscaler stocks should calibrate whether today’s sell-off reflects justified incremental concern or an overreaction to an early-stage announcement with no confirmed launch date.

META gained approximately 8% on 1 July 2026, with pre-market trading showing a price of approximately $602.39 (+$39.10, +6.94%) as of 08:47 AM.

The size of that move tells you something. The market is pricing in significant long-term optionality, not near-term revenue. A high-margin, recurring infrastructure revenue stream would reduce Meta’s near-total dependence on advertising cycles, a vulnerability that has weighed on the stock during every ad spending downturn of the past decade. Recurring cloud revenue could justify higher long-term valuation multiples closer to infrastructure and platform peers.

The investor anxiety around Meta’s capex build is partly rooted in advertising revenue concentration: unlike AWS and Google Cloud, Meta historically generated zero direct revenue from its compute infrastructure, making the entire return on investment dependent on ad yield improvements and platform engagement gains.

The capex validation angle is equally important. Meta’s $125-$145 billion spending programme has been a point of investor anxiety: is the company overbuilding? The cloud plan provides a commercial rationale for that investment, turning what looked like a cost risk into a potential revenue engine. If surplus compute can be monetised externally, the return on capital calculation changes materially.

But the execution risks are real and should be stated plainly:

The enthusiasm is justified in principle. A cloud division is strategically coherent and financially attractive. But the timeline to material cloud revenue is long, and the path runs through enterprise trust-building that Meta has not had to do before. This is best characterised as an early-stage strategic catalyst rather than a near-term earnings driver.

For investors trying to translate today’s 8% move into a position sizing decision, our deep-dive into Meta’s valuation framework examines the sum-of-parts methodology that separates Reality Labs losses from the Family of Apps multiple, giving a more precise picture of what the cloud optionality is actually worth at current prices.

This article is for informational purposes only and should not be considered financial advice. Investors should conduct their own research and consult with financial professionals before making investment decisions.

Rather than summarising what happened today, here is what to watch over the coming months to evaluate whether Meta Compute matures into a genuine business or remains an aspirational talking point.

Until at least two of these three signals materialise, Meta’s cloud ambition is a high-conviction strategic thesis with an unresolved execution question. That distinction should sit at the centre of any investment decision involving META or its hyperscaler peers in the months ahead.

These statements regarding Meta’s cloud business plans are speculative and subject to change based on market developments and company performance.

Meta Compute is an internal initiative at Meta to commercialise surplus AI infrastructure by selling cloud services to external buyers through two models: a hosted AI model platform giving API access to models like Llama, and raw compute leasing where customers rent GPU capacity directly to run their own workloads.

Meta shares climbed approximately 8% after Bloomberg reported the company is developing a cloud division called Meta Compute, with investors pricing in long-term optionality from a high-margin recurring revenue stream that would reduce Meta's near-total dependence on advertising income.

Meta is following the same path Amazon, Microsoft, and Google took by commercialising internally built infrastructure at hyperscaler scale, but unlike those incumbents, Meta currently lacks enterprise sales capabilities, compliance certifications, and the decade-long customer trust relationships that underpin cloud market dominance.

Meta has no history selling managed services to enterprise buyers, lacks an established enterprise sales force, must build compliance certifications from a low base, and as of 1 July 2026 has confirmed no launch timeline, pricing structure, or target customer segments for Meta Compute.

The three key signals are a formal product announcement with pricing and launch details, enterprise partnerships or early customer contracts converting Zuckerberg's claimed inbound demand into signed agreements, and senior hiring from AWS, Azure, or Google Cloud into enterprise sales and compliance roles.