What JB Hi-Fi’s Sales Data Says About ASX Discretionary Stocks

27 mins ago

Flight Centre cut its earnings guidance on 17 June 2026, and its share price went up. For any investor who absorbed the lesson that bad news sends stocks lower, that outcome feels like a malfunction. It is not.

The gap between what the market expected and what was actually announced is where price moves originate, not the headline number itself. Understanding how that mechanism works is one of the most practically useful things you can develop as an ASX investor, and the Flight Centre (ASX: FLT) move from last week is a clean, current illustration of it in action.

By the end of this piece, you will understand why rallies on bad news happen, how to read them correctly, and what the FLT move specifically signals about investor positioning in the travel sector right now.

Share prices do not move on outcomes. They move on the gap between outcomes and expectations.

By the time a company formally revises its guidance, most institutional investors and analysts have already adjusted their models. They have watched industry data, management commentary, and peer results for weeks or months. Their positions reflect what they believe is coming, not what the company has officially told them.

The mechanics of why stock prices move are more nuanced than headlines suggest: prices shift when new information changes the gap between what participants expected and what is actually confirmed, which is why the same earnings number can produce opposite reactions in two different stocks depending on where sentiment sat going in.

Markets price the gap between reality and expectations, not reality alone.

That is exactly what played out with FLT. As reported by Joseph Lyons at MarketIndex.com.au on 17 June 2026, the share price advanced directly in the context of a downward revision to earnings guidance. The downgrade was real. But sentiment around the stock was already weak enough that the actual number landed as less severe than many participants had priced in. The reaction was relief, not punishment.

Every time a market reaction confuses you, the first question worth asking is not “what was the number?” It is “what was the number relative to what the market already believed?”

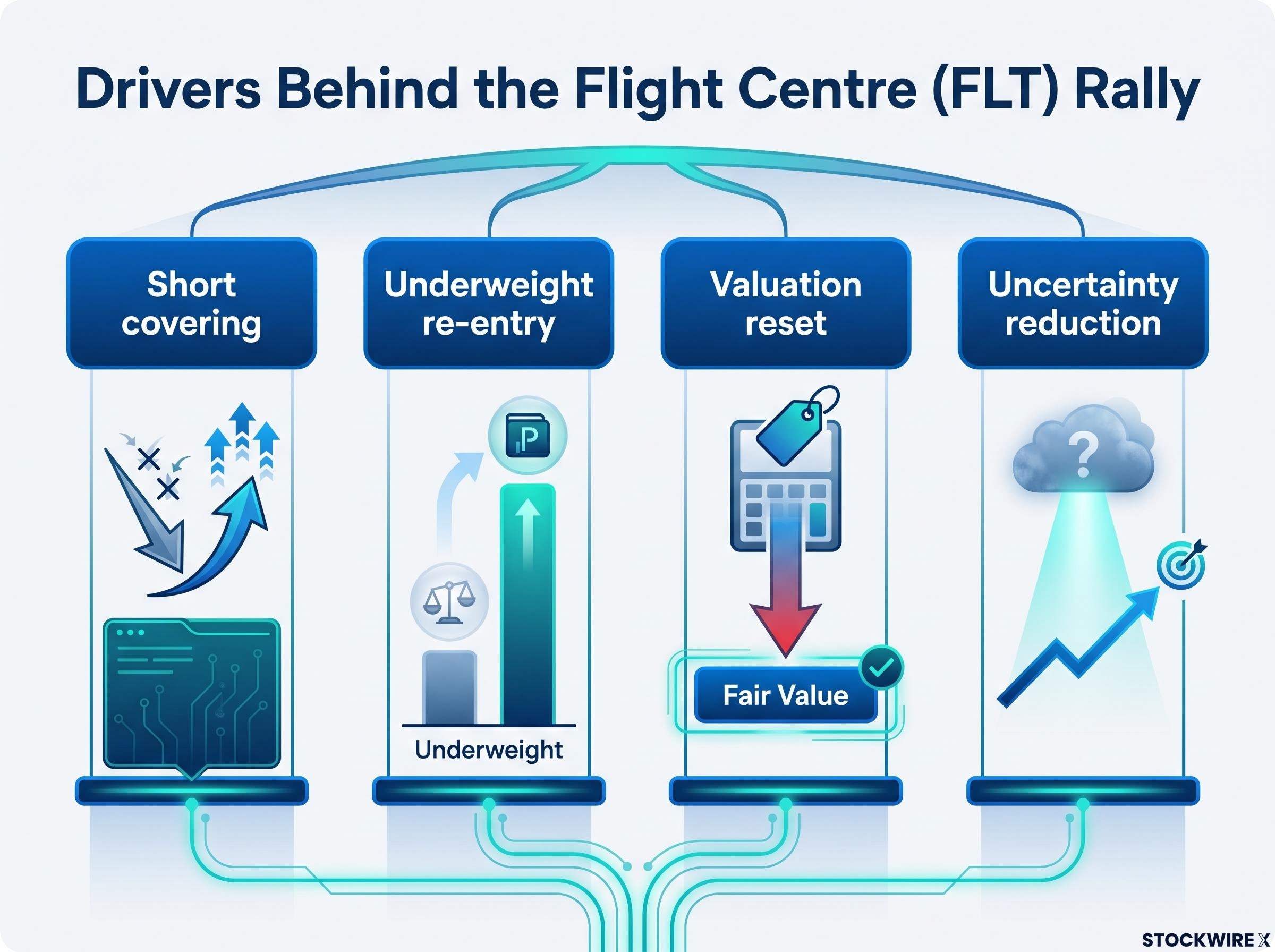

Reconstructing the logic behind a post-downgrade rally means looking at who was positioned where before the announcement hit. The FLT move carries several positioning fingerprints, each reinforcing the others.

Travel has been a volatile sector since the pandemic, and FLT has navigated shifting travel patterns, cost pressures, and earnings volatility across multiple reporting periods. That backdrop tends to attract short sellers and make long-only funds cautious or outright underweight the stock. When bearish positioning becomes crowded, even modestly less-bad news can trigger a mechanical unwind.

Post-downgrade short strategies on the ASX succeed roughly 50-60% of the time when accounting for forced covers, which means the short-covering dynamic visible in the FLT move is not an isolated quirk but a recurring institutional behaviour pattern documented across multiple ASX earnings cycles.

Four mechanisms tend to operate in situations like this:

What the FLT rally tells you about professional money is as important as what it tells you about the earnings number. The move reveals where institutional investors were sitting before the announcement, not just what the company reported.

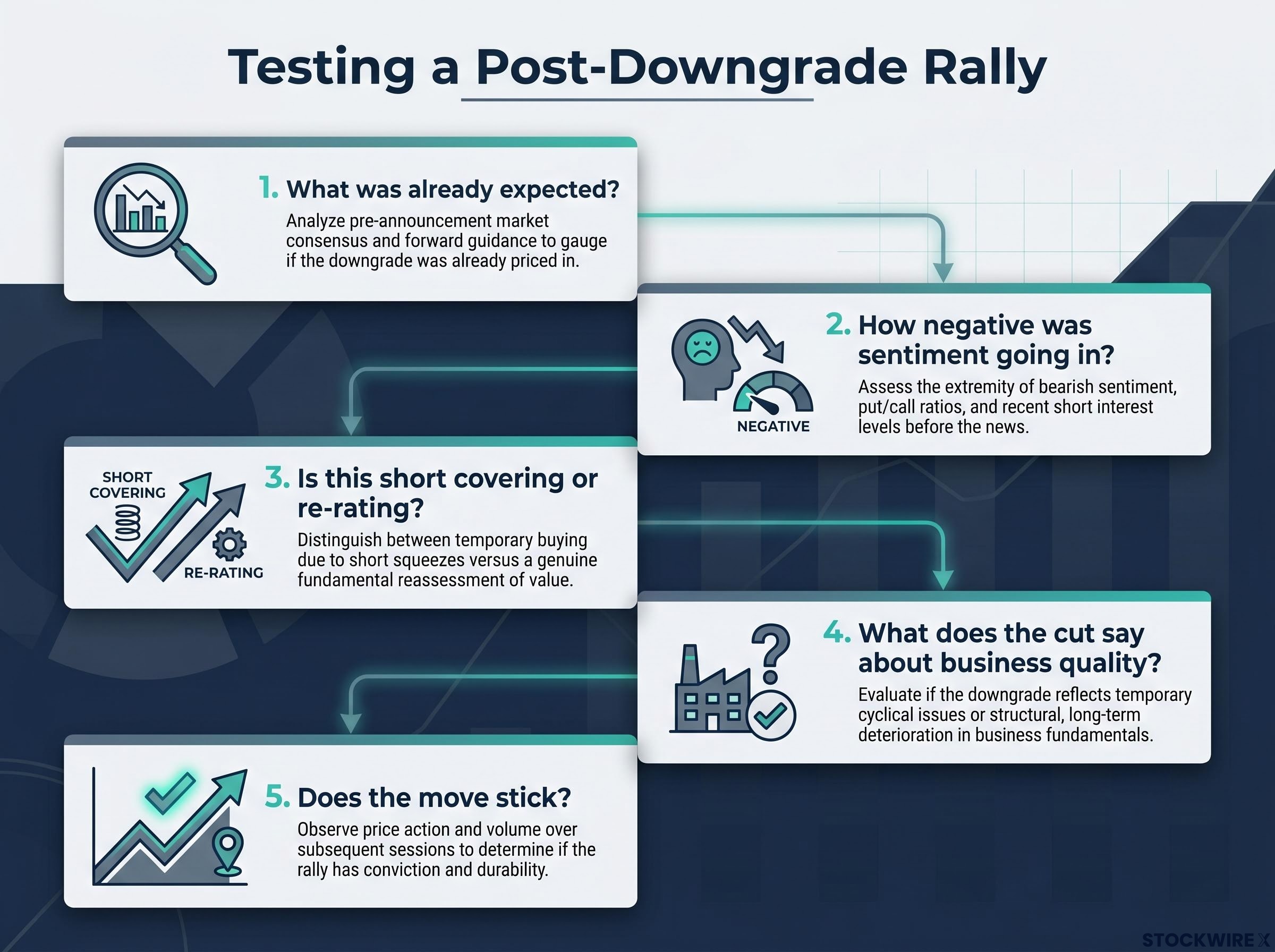

The honest answer, five days after the announcement, is that it is too early to be certain. And that uncertainty is itself the most useful thing to acknowledge.

A short-covering spike and a genuine re-rating look identical on day one. Both produce a rising share price on higher volume. The difference shows up in what happens next. A spike driven primarily by short covering tends to fade within a few sessions as the mechanical buying pressure exhausts itself. A genuine re-rating holds, grinds higher, and is usually accompanied by improving broker sentiment and multiple expansion over days or weeks.

The quality of the earnings cut matters too. If the downgrade reflects a one-off disruption, the market can digest it and move on. If it points to structural deterioration in corporate travel volumes, rising distribution costs, or competitive pressure from online travel platforms, the implications are more serious and the rally is more likely to prove fragile.

The initial pop tells you a floor may have been found. Only the subsequent price behaviour will confirm whether the market has genuinely changed its view of FLT’s earnings trajectory.

If FLT’s rally illustrates what happens when a stock reaches the end of its bad-news cycle, Webjet (ASX: WJL) illustrates what happens when the market suspects the cycle still has further to run.

As reported by Kerry Sun at MarketIndex.com.au on 21 May 2026, Webjet’s share price appeared inexpensive on valuation metrics, but analysts cautioned that adverse news flow may not have fully concluded and that further negative developments remained possible.

That distinction is the point. Valuation alone is not a catalyst. A stock can be statistically cheap on earnings or cash flow multiples and still keep falling if the market believes estimates will be cut again. A low price-to-earnings ratio tells you where the stock sits on the valuation spectrum. It does not tell you where the company sits in the bad-news cycle.

| Variable | Flight Centre (FLT) | Webjet (WJL) |

|---|---|---|

| Valuation signal | Reset lower after guidance cut | Appears inexpensive on metrics |

| Recent analyst tone | Relief that downgrade was manageable | Caution that further negatives possible |

| Position in negative news cycle | Closer to the end (floor potentially found) | Potentially mid-cycle (further cuts feared) |

| Market interpretation | Rally on downgrade (relief) | Cheap but not yet catalysed |

For any investor eyeing cheap travel stocks right now, the Webjet comparison forces a specific question: is this company pricing in a floor, or is the market still waiting to find out how bad the final number will be?

The FLT event is specific, but the analytical framework it illustrates applies across the travel sector.

Travel stocks carry a structural tension that makes positioning analysis especially valuable:

The ASX consumer discretionary sector delivered just 0.62% annualised over the five years to May 2026, lagging the broader ASX 200 by 3.45 percentage points per year, a structural underperformance that helps explain why institutional positioning in travel names like FLT had already shifted defensively well before the June guidance cut.

For a retail investor holding or considering FLT or other ASX travel names, the practical takeaway is straightforward. Before a major announcement, checking where positioning sits is as important as reading the announcement itself. If professional money is already braced for disappointment, even a modest beat can trigger a relief rally. If positioning is still optimistic, even a solid result can disappoint.

The FLT rally on an earnings downgrade is not an anomaly. It is the expectations gap doing exactly what it always does: pricing the distance between what was believed and what was confirmed.

The same mechanism works in reverse. A company reporting strong earnings can still see its share price fall if the result merely meets, rather than exceeds, elevated expectations. The gap works in both directions, and understanding that prevents both panic on bad headlines and euphoria on good ones.

FLT and Webjet sit on opposite sides of that gap right now: one where the market judges the worst to be priced in, and one where uncertainty about further downgrades keeps the gap open. Neither verdict is permanent.

What did the market already believe before this announcement?

That single question, applied to any future earnings event or guidance update, will make more market reactions interpretable than any price target or broker note. It is the portable version of everything the FLT move just demonstrated.

For investors wanting to apply the expectations gap framework systematically beyond single-stock earnings events, our full explainer on contrarian positioning across crowded consensus trades examines how the same mechanism that drove the FLT relief rally operates at the sector and asset class level, with case studies covering European banks, Japanese equities, and the current AI consensus trade.

This article is for informational purposes only and should not be considered financial advice. Investors should conduct their own research and consult with financial professionals before making investment decisions. Past performance does not guarantee future results.

Flight Centre's share price rose because the downgrade was less severe than many investors had already priced in. When bearish positioning becomes crowded, even modestly less-bad news can trigger short covering and relief buying, pushing the price higher despite the negative headline.

The expectations gap is the difference between what the market already believes about a company's earnings and what is actually announced. Stock prices move on this gap, not the headline number alone, which is why the same earnings result can cause opposite price reactions in different stocks depending on prior sentiment.

Short covering occurs when traders who have borrowed and sold shares to profit from a price fall buy those shares back to close their positions. When a bad-news announcement is less severe than feared, short sellers rush to cover simultaneously, creating real buying pressure that pushes the price up independent of any change in the company's fundamentals.

A genuine re-rating typically holds or grinds higher over several sessions with broadening participation and improving broker sentiment, while a short-covering spike tends to fade within a few days as mechanical buying pressure exhausts itself. Monitoring whether the initial volume spike continues across multiple sessions is the key practical test.

As of mid-2026, Flight Centre appears closer to the end of its negative news cycle, with the market interpreting its guidance cut as a manageable floor, while Webjet was flagged by analysts as potentially mid-cycle with further negative developments still possible despite appearing inexpensive on valuation metrics.