CURE and CLNE: the ASX ETFs Returning 25% in 2026

5 hrs ago

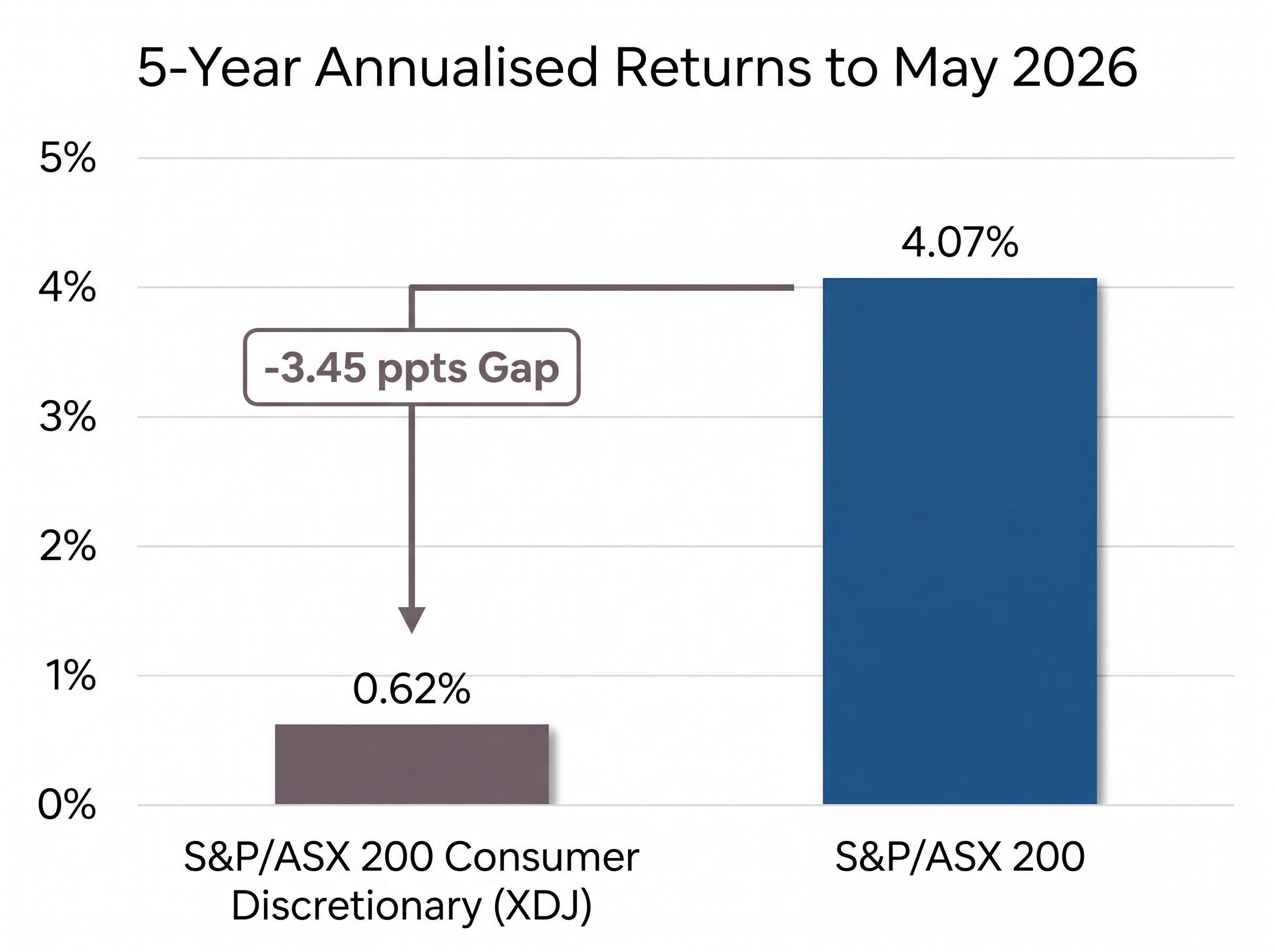

The ASX consumer discretionary sector has delivered an annualised return of just 0.62% over the past five years, compared with 4.07% for the broader S&P/ASX 200. That gap, roughly 3.45 percentage points per year, compounds into a material difference over any reasonable holding period. Yet the stocks that populate this sector are among the most recognised names on the exchange: retailers, travel companies, and leisure businesses that Australian investors interact with weekly. With the RBA holding the cash rate at 4.35% as of May 2026 and real per-capita household consumption broadly flat, the structural forces suppressing discretionary spending remain unresolved. This analysis explains why the sector has lagged, how interest rates transmit directly into discretionary revenues, where familiarity bias distorts investor decision-making, and what Flight Centre Travel Group (ASX: FLT) reveals as a real-world case study in valuation compression. It closes with a practical framework for monitoring forward-looking signals before reconsidering sector exposure.

The numbers are stark. Over the five years to May 2026, the S&P/ASX 200 Consumer Discretionary index (XDJ) returned an annualised 0.62%. The S&P/ASX 200, by contrast, delivered 4.07% annualised over the same period.

| Index | 1-Year Return | 5-Year Annualised Return | 5-Year Gap vs ASX 200 |

|---|---|---|---|

| S&P/ASX 200 Consumer Discretionary (XDJ) | Low single digits | 0.62% | -3.45 ppts |

| S&P/ASX 200 | Mid single digits | 4.07% | Benchmark |

A 3.45 percentage-point annual gap does not feel dramatic in any single year. Compounded over five, it represents a meaningful drag on portfolio returns. Morningstar noted in April 2026 that the sector has:

“materially underperformed the broader market over the past five years”

This is not a recent deterioration. BetaShares observed in the same period that “cyclical sectors such as consumer discretionary remain under pressure in a high-rate, low real-income growth environment.” VanEck’s Q1 2026 ETF flows data confirmed the institutional read: investors have been favouring “defensive quality and resources over rate-sensitive domestic cyclicals,” with limited net inflows into consumer discretionary funds. The broad market and resources products absorbed the capital instead.

Consider two purchases in a single week: groceries and a restaurant meal. The groceries happen regardless of the interest rate environment. The restaurant meal is the first thing cut when mortgage repayments rise by $400 a month. That distinction, between spending that cannot be deferred and spending that can, is the dividing line between consumer staples and consumer discretionary.

Consumer discretionary captures the non-essential, deferrable categories:

This classification matters because macro conditions affect the two sectors in opposite ways. When households tighten budgets, staples hold steady while discretionary revenues contract.

Consumer staples drawdown protection stands in direct contrast to the discretionary sector’s cyclical exposure: the XSJ recorded a maximum drawdown of approximately -9% in 2025 against the ASX 200’s -15%, while still delivering tax-advantaged franked income that discretionary names, with their variable dividend profiles, rarely match across a full rate cycle.

The composition of the ASX Consumer Discretionary sector amplifies this sensitivity. According to S&P Dow Jones Indices (January 2026), the Australian index comprises “traditional retail and domestic cyclicals,” predominantly bricks-and-mortar retailers, travel operators, and leisure businesses. The US equivalent is dominated by mega-cap e-commerce and global consumer platform companies with diversified revenue streams and structural growth profiles.

BetaShares identified two drivers behind the performance gap: composition and the greater sensitivity of Australian households to interest-rate changes. Investors who read global sector commentary and apply it to ASX names may be working from the wrong framework entirely.

The RBA’s cash rate does not affect discretionary revenues directly. It works through a causal chain, and each link amplifies the pressure:

The RBA’s May 2026 Statement on Monetary Policy confirmed that households with mortgages are constraining discretionary spending to service higher interest payments, with the document providing the official macroeconomic basis for the cash rate decision and its expected transmission into household consumption behaviour.

“Discretionary components of consumption continue to be particularly weak.” — RBA Statement on Monetary Policy, May 2026

This mechanism explains a subtlety that many investors miss. The sector does not recover when the RBA pauses. It needs actual rate cuts to translate into improved real household disposable income before spending lifts. The lag between peak rates and spending recovery means discretionary stocks typically bottom later than the rate-pause announcement.

Australian retail investors show a documented tendency to overweight companies whose products they use. The ASX/ASIC Australian Investor Study 2023 found that retail investors exhibit “home-bias within the home market,” favouring large, well-known consumer brands. Morningstar’s March 2024 analysis attributed this pattern to familiarity bias and brand recognition.

The investment consequence is more than an academic curiosity. Research from UNSW Business School (September 2024) found:

“Some evidence of higher valuation multiples for widely recognised consumer brands during boom periods,” described as “unstable and prone to reversal when macro conditions deteriorate.”

BetaShares labelled this the “brand halo effect,” where investors extrapolate personal product experience into an investment thesis. The dynamic can inflate valuations during optimistic periods and then amplify the de-rating when macro conditions shift, because crowded retail ownership means more sellers when sentiment turns.

Specific cognitive traps to monitor when evaluating a company as both a customer and a potential investor:

Recognising familiarity bias does not mean avoiding consumer stocks. It means applying greater discipline on entry price and separating the experience of using a product from the analysis of owning the equity.

Familiarity bias sits within a broader cluster of cognitive biases at market extremes, including loss aversion, anchoring, and herd behaviour, that interact to produce particularly costly outcomes when crowded retail ownership meets a deteriorating macro environment and sentiment turns sharply negative.

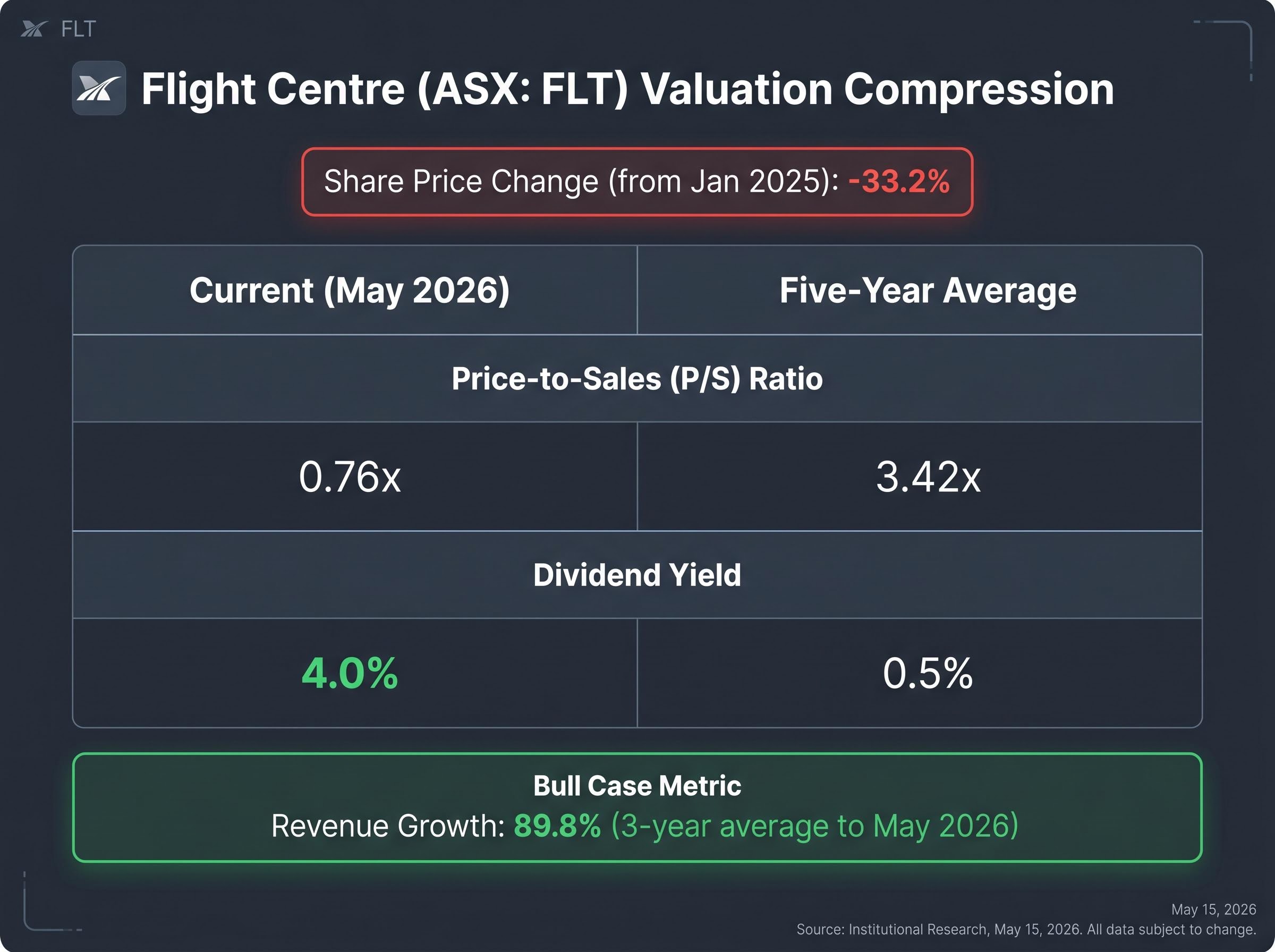

Flight Centre Travel Group (ASX: FLT) brings every preceding concept into focus. The share price has fallen 33.2% since January 2025. The current price-to-sales (P/S) ratio sits at 0.76x, against a five-year average of 3.42x. The dividend yield has risen to 4.0%, compared with a five-year average of 0.5%.

| Metric | Current (May 2026) | Five-Year Average |

|---|---|---|

| Price-to-Sales (P/S) Ratio | 0.76x | 3.42x |

| Dividend Yield | 4.0% | 0.5% |

| Share Price Change (from Jan 2025) | -33.2% | N/A |

Macquarie cut its price target following FLT’s FY25 results in August 2025, citing slower leisure margin recovery and:

“a more cautious consumer”

Revenue has grown at an average annual rate of 89.8% over three years to May 2026, driven substantially by post-COVID travel normalisation and a resilient corporate travel division. Management has highlighted ongoing investment in digital platforms. If the rate cycle turns and leisure demand recovers, the compressed P/S multiple offers significant re-rating potential. The dividend resumption, as noted by Intelligent Investor in September 2025, adds a yield floor that did not exist during the pandemic years.

The recovery thesis is real, but it is contingent on macro conditions the company does not control.

FLT’s FY25 full-year results showed net profit improvement, but margins remained below pre-COVID levels. Management acknowledged moderation in leisure travel growth as consumers adjust to cost-of-living pressures. A low P/S multiple is only attractive if earnings actually recover toward historical norms. If leisure demand stays weak and margins compress further, the stock’s valuation could remain depressed for an extended period. A compressed multiple reflects a market pricing in sustained earnings risk, not simply offering a discount.

FLT illustrates precisely where familiarity can create false confidence. Many investors have booked through Flight Centre. Fewer have modelled the margin trajectory required for the valuation to re-rate.

Investors who want to stress-test the recovery thesis against the bear case in quantitative detail will find our deep-dive into FLT’s value-trap risk, which examines the forward P/E of 8.76-9.26, the six-year negative free cash flow history, and the return-on-equity thresholds that separate genuine undervaluation from a structurally impaired business.

The sector’s recovery depends on rate cuts translating into improved real household disposable income, not merely on peak rates being confirmed. ANZ expects the first cut no earlier than early 2027. CBA forecasts easing “sometime in 2026-27” if inflation continues to track lower. Investors pricing in a near-term recovery may be early.

Sarah Hunter noted in her March 2026 speech that “gradual recovery in discretionary spending” is expected as real income growth improves, but that “timing is uncertain.” Morningstar’s April 2026 assessment was direct: the sector is “not yet priced for a return to trend spending,” and fund managers remain “neutral to underweight” on XDJ.

Rather than waiting passively for a rate cut announcement, investors can monitor specific forward-looking signals before increasing discretionary sector exposure:

These indicators convert a vague “wait for rates to fall” thesis into a monitoring framework with observable triggers.

The structural challenges are real and unresolved. The macro headwinds documented throughout this analysis persist as of May 2026. Yet the response from professional allocators is not blanket avoidance. Morningstar noted “modest but selective inflows into high-quality discretionary names” in April 2026, even as BetaShares confirmed that broad ETF flows continued to favour market-wide and resources products over consumer sector funds.

Contrarian rotation into consumer defensives has been gaining institutional traction precisely because the conditions the current article describes, compressed discretionary valuations alongside a high-rate environment, are the same conditions that historically preceded defensive sector outperformance across the dot-com and GFC recovery periods.

The analysis distils into three principles. First, macro sensitivity is the primary risk driver for this sector, and the interest-rate transmission mechanism makes Australian discretionary stocks more exposed than their global peers. Second, familiarity bias is the primary cognitive risk, inflating perceived safety in names investors know as customers. Third, valuation compression is a feature of the cycle rather than a permanent state.

“We expect a gradual recovery in discretionary spending [as conditions improve], though timing is uncertain.” — Sarah Hunter, RBA Assistant Governor, March 2026

Familiarity with a business is a starting point for research, not a substitute for it. For the ASX consumer discretionary sector specifically, the macro timing layer is non-negotiable, and the data signals worth monitoring are now clearly defined.

This article is for informational purposes only and should not be considered financial advice. Investors should conduct their own research and consult with financial professionals before making investment decisions. Past performance does not guarantee future results. Financial projections are subject to market conditions and various risk factors.

The ASX consumer discretionary sector covers non-essential, deferrable spending categories such as travel, dining, apparel, electronics, and leisure businesses. It includes well-known ASX-listed companies like Flight Centre Travel Group, bricks-and-mortar retailers, and leisure operators.

The sector returned just 0.62% annualised over the five years to May 2026, compared with 4.07% for the S&P/ASX 200, primarily because high interest rates have reduced household disposable income, causing consumers to cut deferrable spending on travel, dining, and retail first.

When the RBA raises the cash rate, variable mortgage repayments increase immediately, reducing household disposable income and causing consumers to cut discretionary spending before essentials. The sector typically does not recover until actual rate cuts translate into improved real household disposable income, meaning the lag can extend well beyond the rate-pause announcement.

Investors should watch for sustained real wage growth outpacing inflation, an uptick in discretionary categories within CBA and ANZ card-spending data, forward earnings estimate upgrades across discretionary names, and a shift in RBA language away from describing discretionary consumption as particularly weak.

Familiarity bias occurs when investors overweight companies whose products they personally use, confusing product satisfaction with earnings quality or competitive advantage. Research from UNSW Business School found this can inflate valuation multiples during optimistic periods, with those premiums prone to sharp reversal when macro conditions deteriorate.