How the Hormuz Closure Drives Oil Prices and Inflation

2 mins ago

Commonwealth Bank of Australia shares suffered their steepest single-session decline since the bank’s 1991 ASX debut on 13 May 2026, falling more than 10% in a sell-off that surpassed drawdowns from the Global Financial Crisis, the dot-com collapse, and the COVID-19 pandemic. Two distinct catalysts converged on the same morning: a Q3 FY2026 earnings result that missed Citi’s forecast by 2%, and a Federal Budget announced the previous night introducing the most far-reaching property tax changes in approximately 26 years. Neither catalyst alone would likely have driven a decline of this magnitude. Together, they exposed a premium valuation that had left no margin for bad news. This analysis unpacks what the budget reforms actually change, why CBA is structurally more exposed than its peers, what a projected 25% reduction in housing credit growth means for the bank’s earnings trajectory, and how the structural character of this sell-off distinguishes it from almost every comparable drawdown in the bank’s history.

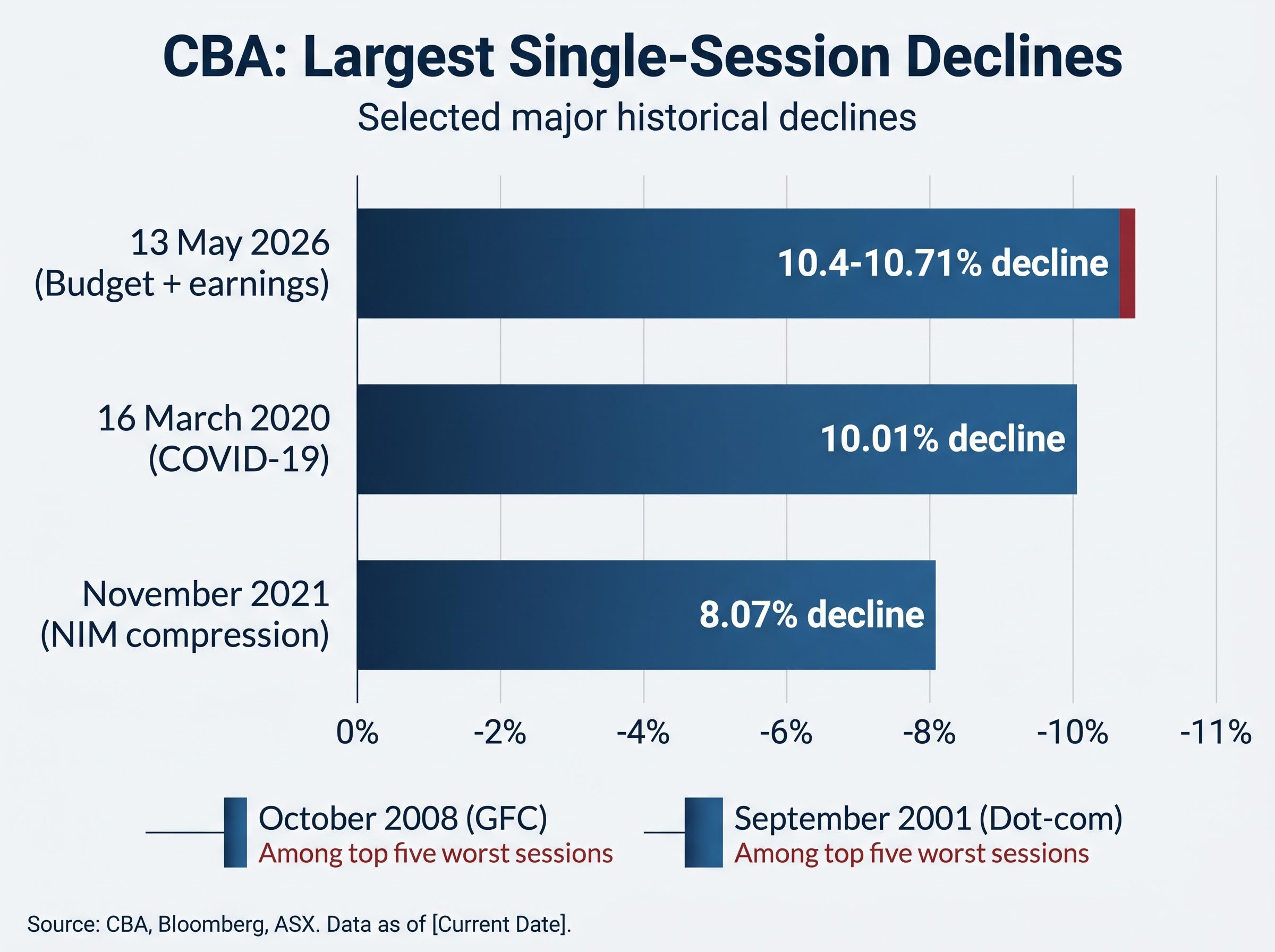

CBA closed at approximately $153.19-$153.67 on 13 May, a decline of roughly 10.4-10.71%. That figure places it above the 10.01% loss recorded on 16 March 2020 during the pandemic’s initial market rout, and above every other single-session decline in the bank’s listed history.

CBA’s steepest single-session loss since its 1991 ASX debut, surpassing GFC and pandemic drawdowns.

The scale surprised even seasoned observers because the damage was overdetermined. Two independent triggers arrived simultaneously, each compounding the other before the market opened.

The quarterly result was disappointing without being alarming. Unaudited cash net profit after tax came in at approximately $2.7 billion, 2% below Citi’s forecast and 1% below the H1 FY2026 quarterly average, though 4% higher year-on-year. Net interest margins appeared stable once one-off items were excluded. Home loan arrears rose 6 basis points and credit card arrears rose 2 basis points, attributed to seasonal patterns.

Loan impairment expense reached $316 million, including a $200 million addition to forward-looking collective provisions. Personal loan arrears over 90 days hit 1.71%, the highest level since before the pandemic.

CBA’s rising arrears tell a more specific story than the headline profit figure: personal loan arrears spiked 30 basis points in a single quarter, home loan arrears climbed to 1.12% above the sector average, and the $200 million provision top-up signals that the bank’s own internal risk modelling expects credit conditions to worsen before they stabilise.

A 2% miss on a single quarter does not, on its own, justify a 10% share price decline.

The budget was announced on the night of 12 May, giving institutional investors hours to model implications before the open. When trading began, CBA opened approximately 5% lower and continued deteriorating through the session with no meaningful recovery. That pattern is consistent with repricing of a structural shift rather than panic selling, which typically produces sharp intraday reversals.

The budget contained two headline property tax reforms. Both are significant, but the grandfathering provisions attached to each make the timeline of their market impact slower and more complex than a binary “negative gearing is gone” reading suggests.

Treasurer Chalmers’ 2026-27 Budget speech confirmed both the negative gearing restriction to new builds only and the CGT discount replacement, with effective dates and grandfathering provisions outlined in detail, giving institutional investors the precise policy parameters they needed to model earnings implications before the market opened on 13 May.

Negative gearing concessions are now available only for new builds, effective from the night of 12 May 2026 for properties newly acquired from that date. Investors who lose eligibility can only apply rental losses against residential rental income or future capital gains, not wages or other personal income.

The negative gearing restriction to new builds applies immediately to properties acquired after budget night, meaning investors who purchased established dwellings from 12 May 2026 onward can only offset rental losses against rental income rather than wages, a structural change to investor economics that took effect before most market participants had finished reading the budget papers.

The 50% CGT discount for assets held over 12 months is abolished from 1 July 2027, replaced by cost-base indexation with a minimum 30% effective tax rate. Grandfathering applies to unrealised gains already accrued. As ABC Economics Reporter Tom Crowley summarised: “Any capital gains you’ve already made keep the old discount.”

| Reform | Previous Rule | New Rule | Effective Date | Grandfathering |

|---|---|---|---|---|

| Negative Gearing | Available on all investment properties | Restricted to new builds only | 12 May 2026 | Existing holdings retain current treatment |

| CGT Discount | 50% discount for assets held 12+ months | Cost-base indexation; minimum 30% effective rate | 1 July 2027 | Unrealised gains accrued before commencement retain old discount |

The reforms extend beyond residential property. Asset classes affected include:

For property investors and mortgage holders, the grandfathering detail is material. The policy’s effect on existing holders operates through changed incentives for future decisions, not through immediate tax reclassification.

The general policy change is one thing. The reason CBA fell harder than its peers is specific: the bank holds the largest investor mortgage portfolio among Australia’s major banks, placing it directly in the path of reduced investor credit demand.

CBA entered the session trading at approximately 28 times earnings, versus high-teens P/E multiples for ANZ, NAB, and Westpac.

Investor loans are a high-margin segment for Australian banks. Interest-only products carry wider spreads, tend to demonstrate superior asset quality, and generate stronger returns on equity than standard owner-occupier loans. A structural reduction in investor lending volumes therefore hits the most profitable part of the mortgage book.

The broader sector was already showing softness heading into budget night. ANZ reported on 3 May with disappointing revenue momentum. NAB followed on 4 May with revenues below expectations and weak deposit balances. Westpac reported on 6 May with solid volumes offset by net interest margin pressure. CBA’s vulnerability was more visible, not less, against that backdrop.

| Bank | Approximate P/E | Dividend Yield Context | Recent Result Concern |

|---|---|---|---|

| CBA | ~28x | ~3%, low relative to multiple | Q3 cash NPAT 2% below Citi forecast |

| ANZ | High teens | Higher yield than CBA | Disappointing revenue momentum (3 May) |

| NAB | High teens | Higher yield than CBA | Revenues below expectations, weak deposits (4 May) |

| Westpac | High teens | Higher yield than CBA | NIM pressure despite solid volumes (6 May) |

A historical parallel exists. In November 2021, CBA fell 8.07% in a single session when trading at 18 times earnings, driven by NIM compression from fixed-rate loan migration (which had risen from 15% historical origination share to approximately 40-45% by late 2021). That episode was also company-specific rather than crisis-driven.

The pathway from a budget announcement to a bank’s earnings line runs through several intermediate steps. Understanding the transmission mechanism is what separates a headline reaction from an informed assessment.

Jarden analyst Matthew Wilson projects up to a 25% reduction in housing credit growth as a result of the reforms.

That projection is the most specific quantitative benchmark available as of budget night. Industry body responses, RBA financial stability commentary, and APRA stress-test data had not been published, meaning the Jarden figure is the leading available estimate but should be held with appropriate uncertainty.

The budget’s combined reforms produce a clear hierarchy of asset class winners and losers: passive ETFs, dividend-paying blue-chip equities, and superannuation are structurally better positioned under the new settings, while leveraged residential property and discretionary trusts face the sharpest after-tax deterioration, a realignment that could accelerate capital flows away from investment property toward listed markets.

As Tom Crowley observed: “Every one of those new home owners buys from an investor that has been chased out of the market by higher taxes.” The government itself acknowledges approximately 35,000 interim contraction in homeownership during the transition period, even as it projects 75,000 net new homeowners over a decade.

Housing credit growth is a primary driver of bank net interest income. A structural reduction of 25%, if it materialises, would require downward earnings revisions across the sector, with CBA most exposed given its portfolio concentration.

Nearly every comparable CBA single-day loss in the bank’s listed history was triggered by a global crisis, and most subsequently represented medium-term buying opportunities, according to Market Index analysis. The historical pattern is real and honestly acknowledged.

The question is whether it applies here.

| Event | Catalyst Type | CBA P/E at Time | Decline | Subsequent Trajectory |

|---|---|---|---|---|

| GFC (2008) | Global crisis (cyclical) | Below long-run average | Among top five worst sessions | Medium-term buying opportunity |

| COVID-19 (March 2020) | Global crisis (cyclical) | Below long-run average | 10.01% | Strong recovery within 12 months |

| November 2021 | Domestic, company-specific | ~18x | 8.07% | Uncertain forward returns |

| May 2026 | Domestic, structural policy | ~28x | ~10.4-10.71% | Pending; no broker revisions yet |

Cyclical shocks are temporary. Structural policy changes redefine the earnings architecture permanently. The relevant analytical question is not “when will sentiment recover” but “what is the correct earnings multiple for a bank with structurally reduced investor mortgage growth.”

The November 2021 episode is the closest precedent, and forward returns from that period were described as uncertain, providing a relevant comparison for domestically driven structural repricing.

For investors wanting to apply a rigorous framework to CBA’s post-sell-off price, our comprehensive walkthrough of ASX bank valuation uses Westpac’s live H1 2026 data to demonstrate how NIM, return on equity, and CET1 ratios combine across the dividend discount model and price-to-book approaches, with worked examples showing how input assumptions shift fair value estimates by as much as $15 per share.

Mining majors reached all-time highs on the same session, raising the possibility of capital rotating out of financials and into resources, which could extend the recovery timeline. Evan Lucas observed that “bracket creep is still the biggest problem” for housing affordability, suggesting the reforms do not resolve all structural headwinds.

Pending data points that will shape the repricing narrative:

The analytical framework is established. What follows is the specific monitoring agenda.

Treasurer Jim Chalmers: “The reforms in this Budget will lift our total investment in housing to a record $47 billion.”

That $47 billion housing investment package is the stated offsetting force. The new-build incentive is designed to redirect investor activity rather than eliminate it entirely, and the extent to which this redirection occurs will shape actual credit outcomes.

Property investors face distinct watchpoints. CGT changes do not commence until 1 July 2027, providing a defined window before the new regime takes effect. Negative gearing restrictions are already operative for new acquisitions as of 12 May 2026. Shadow Treasurer Tim Wilson has argued the reforms “won’t increase the number of homes being built or help renters,” signalling the opposition’s likely policy reversal platform.

The Q3 earnings miss confirmed cyclical softness. The budget reforms reframed the earnings outlook as structurally impaired. CBA’s premium valuation at approximately 28 times earnings left no buffer for either development.

The recovery thesis depends on how investors categorise this event: as a structural repricing requiring a new, lower earnings multiple, or as an overreaction to policy uncertainty that resolves as implementation detail clarifies. Historical precedent favours buying the dip after crisis-driven sell-offs. This event is policy-driven, and the closest domestic precedent (November 2021) produced uncertain, not strong, forward returns.

The government’s $47 billion housing package and new-build incentive could partially redirect investor activity. The lock-in effect, credit growth headwinds, and potential sector rotation into resources all argue for patience before assuming historical patterns apply.

This article is for informational purposes only and should not be considered financial advice. Investors should conduct their own research and consult with financial professionals before making investment decisions. These statements regarding future credit growth, earnings impacts, and policy outcomes are speculative and subject to change based on market developments and regulatory responses.

Two catalysts hit simultaneously: a Q3 FY2026 cash profit that came in 2% below Citi's forecast, and a Federal Budget announced the previous night that restricted negative gearing to new builds only and replaced the 50% CGT discount with cost-base indexation. Neither event alone would likely have caused a decline of this magnitude, but together they struck a stock trading at approximately 28 times earnings with no valuation buffer.

From 12 May 2026, negative gearing concessions are available only on newly built properties. Investors who purchased established dwellings from that date onward can only offset rental losses against rental income or future capital gains, not against wages or other personal income. Existing holdings acquired before budget night retain their current tax treatment.

Jarden analyst Matthew Wilson projected that the combined budget reforms could reduce housing credit growth by up to 25%. Housing credit growth is a primary driver of bank net interest income, and CBA is considered the most exposed of the major banks given its concentration in investor mortgages.

The 13 May 2026 decline of approximately 10.4-10.71% surpassed the 10.01% fall recorded on 16 March 2020 during the COVID-19 sell-off and exceeded every other single-session decline in CBA's listed history, including drawdowns during the Global Financial Crisis and the dot-com collapse.

Key items to watch include broker EPS and price target revisions from Morgan Stanley, Goldman Sachs, Citi, UBS, and Macquarie; RBA financial stability commentary; APRA stress-test updates on bank capital under a housing credit contraction; and the first post-announcement RBA Credit Aggregates data showing actual lending patterns.