Nvidia’s Computex Keynote Must Answer 3 Questions to Hit $250

24 mins ago

Markets have spent two months trading headlines about the Strait of Hormuz reopening and a potential US-Iran nuclear deal, yet neither the Federal Reserve nor the European Central Bank has moved a single basis point in response. The Fed rate cut outlook has not shifted. The ECB’s rate path has not shifted. Crude oil risk premia have faded, tanker traffic has normalised, and swap rates have repriced, but the policy rate in Washington sits exactly where it sat in March, and the deposit facility rate in Frankfurt has not budged either. The disconnect between the geopolitical narrative and the central bank reality is the story worth examining, because the gap reveals which signals actually matter for rate-sensitive positioning and which ones amount to noise.

A plausible-sounding trade formed in the spring of 2026: US-Iran talks produce a deal, Hormuz risk evaporates, oil prices fall, headline inflation drops, and central banks cut sooner. Each link in that chain sounds reasonable in isolation. The problem is that the first link never materialised, and the remaining links would not have triggered the conclusion even if it had.

Three facts anchor the actual situation:

Reporting on the US-Iran negotiation status as of late May 2026 confirms that President Trump rejected a draft framework described by Iranian state media, with sanctions relief explicitly excluded from active discussions, leaving the foundational premise of the geopolitical rate-cut trade without a factual anchor.

Yet despite the absence of an actual deal, markets kept trading the expectation of one. ING analysts characterised the pattern bluntly.

ING described the Strait of Hormuz reopening headlines as “repetitive,” noting such reports had circulated persistently over the approximately two months prior to late May 2026, with markets trading speculation rather than confirmed developments.

The Hormuz blockade transmission mechanics across crude, shipping insurance, and inflation expectations unfolded in a specific sequence during April and May 2026, and tracking that sequence is what allows investors to distinguish which asset class moves reflected genuine supply risk and which reflected narrative momentum that ran ahead of confirmed developments.

The result was a series of asset price moves built on a narrative that lacked a factual anchor. Understanding why those moves failed to produce a policy response requires examining what central banks actually respond to.

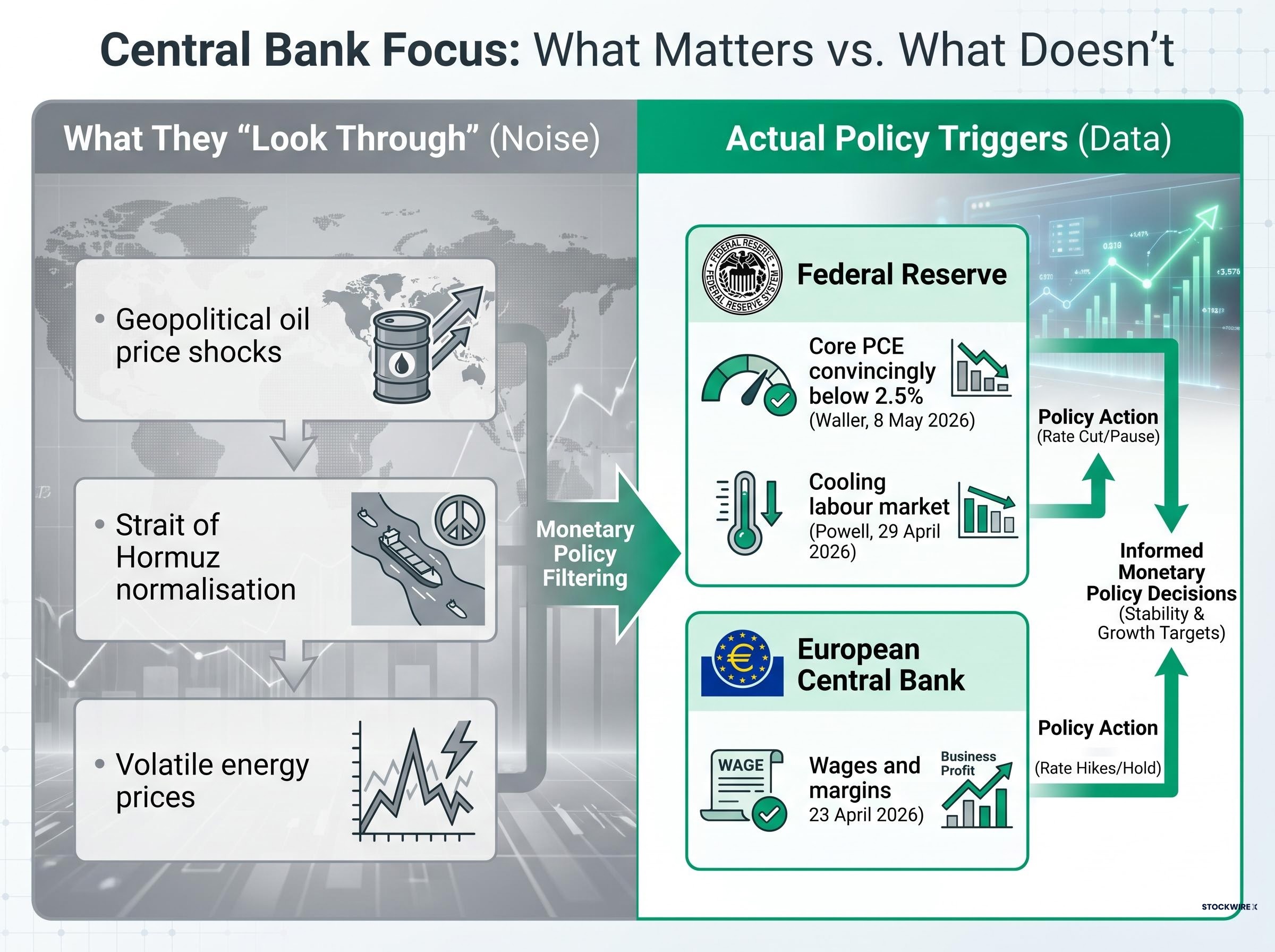

Both the Fed and ECB operate under a framework that explicitly separates the kind of oil price move produced by a geopolitical event from the kind of data that shifts their rate decisions. The distinction is straightforward: central banks “look through” temporary, geopolitically driven oil price shocks unless those shocks produce second-round effects on wages, core inflation, and inflation expectations.

The mechanism matters. A drop in crude prices reduces headline inflation directly because energy is a large component of consumer price indices. But headline inflation is not what either central bank targets when setting policy. The Fed watches core PCE (which strips out food and energy). The ECB watches core services inflation and wage settlements. A crude price decline that does not feed through to those measures does not, by design, alter the policy path.

The cost-push inflation dilemma facing central banks when supply shocks drive headline prices is structurally different from demand-driven inflation: tightening into a supply shock risks deepening any growth slowdown, while holding risks appearing to accommodate above-target prices, which is precisely why the look-through framework exists as a standing policy tool rather than an improvised response.

The Fed’s stated prerequisites for cutting are specific. Governor Christopher Waller said on 8 May 2026 that the bar requires core PCE falling “convincingly below 2.5% on a 6-month annualised basis.” Chair Jerome Powell, at the 29 April 2026 FOMC press conference, added that the Committee needs “several more good inflation readings” and evidence that labour market conditions are cooling without collapsing. A San Francisco Fed Economic Letter published on 3 March 2025 formalised the principle: central banks should react to geopolitical oil shocks only if second-round effects on inflation expectations and wages become evident, not to the shock itself.

The FOMC minutes from April 2026 record core PCE price inflation running at 3.2 percent in March, with the Committee explicitly noting elevated inflation driven in part by global energy prices while maintaining its federal funds rate target, a combination that underscores how far the data still sits from the threshold officials have set for easing.

Powell stated that the Fed “takes commodity prices into account as they affect the outlook” but stressed that policy focuses on “the medium-term inflation path, not short-term oil fluctuations.”

ECB President Christine Lagarde stated at the 23 April 2026 press conference that ECB decisions “depend more on wages and margins than on short-term energy price swings.” Executive Board member Isabel Schnabel went further on 16 May 2026, warning that cutting too early on the basis of volatile energy prices “could entrench underlying inflation.” The ECB’s own Economic Bulletin (Issue 2/2025, 28 March 2025) concluded that policy should “look through” temporary energy price shocks and adjust only if second-round effects threaten to de-anchor inflation expectations.

None of these conditions are met by a Hormuz headline or a crude price dip driven by easing geopolitical risk.

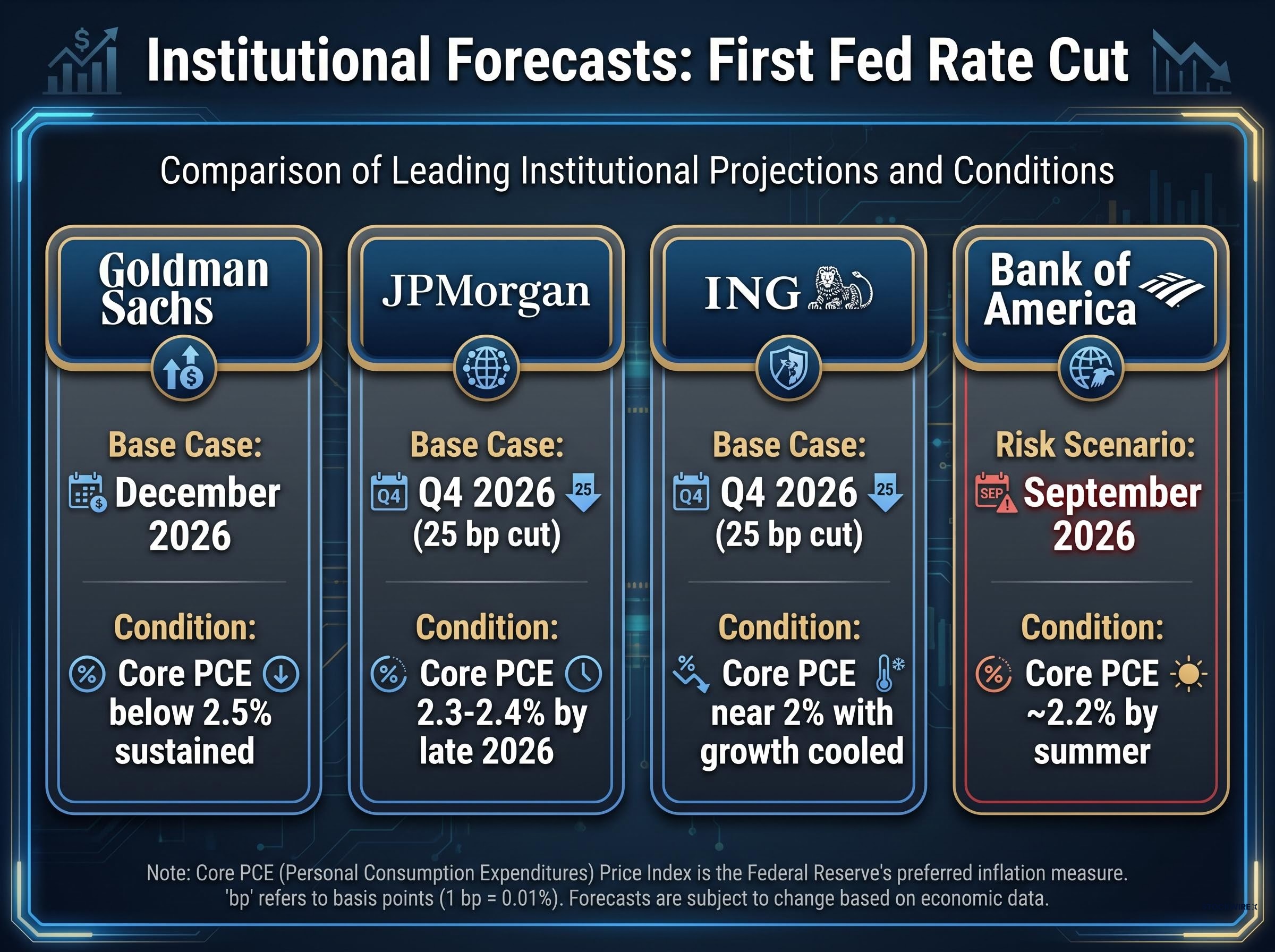

The consensus among major institutions has converged on late 2026 as the earliest realistic window for a first Fed cut, and even that is conditional. The timeline has lengthened, not shortened, in recent months.

Goldman Sachs shifted its first-cut call to December 2026 from a prior September forecast, citing stickier core services inflation and resilient US growth. JPMorgan projects one 25 bp cut in Q4 2026, with core PCE drifting only to 2.3-2.4% by late 2026. ING pencils in a first 25 bp cut in Q4 2026, contingent on core inflation clearly approaching 2% and growth cooling materially. Bank of America retains a lower-conviction risk scenario of a September cut if core PCE reaches approximately 2.2% by summer, but labels this explicitly as a tail possibility.

| Institution | First Cut Forecast | Core PCE Condition | Conviction Level |

|---|---|---|---|

| Goldman Sachs | December 2026 | Below 2.5% sustained | High (base case) |

| JPMorgan | Q4 2026 | 2.3-2.4% by late 2026 | High (base case) |

| ING | Q4 2026 | Near 2%, growth cooled | High (base case) |

| Bank of America | September 2026 (risk scenario) | ~2.2% by summer | Low |

Fed officials have reinforced this framing directly. New York Fed President John Williams said on 15 May 2026 that there is “no urgency” to cut and that cuts are “not imminent.” Waller described the bar for cuts as “higher than markets had priced earlier this year.”

Williams told Reuters on 15 May 2026 that policy is “well positioned” and there is “no urgency” to cut rates in the near term.

The picture is consistent: late 2026 at the earliest, and only if the data cooperate. A geopolitical oil price dip does not accelerate any of these conditions.

If the Fed’s path to a cut is narrow, the ECB’s is narrower still. The constraints are structural as well as cyclical, and the two central banks are arriving at restraint from different directions but reaching the same destination.

The institutional forecasts are stark:

Schnabel’s 16 May 2026 interview crystallised the ECB’s position. She said markets had moved “too aggressively” in pricing multiple cuts and that geopolitically driven energy price declines are “unlikely to alter the ECB’s medium-term assessment.”

Schnabel warned that loosening policy too early on the basis of volatile energy prices “could entrench underlying inflation.”

Bundesbank President Joachim Nagel reinforced the message on 9 May 2026, stating that “the bar for rate cuts is high.” And ING flagged a complicating factor that receives too little attention: European natural gas supply tightness is anticipated later in 2026, meaning any energy price relief from easing geopolitical tensions may not persist even at the headline level.

The ECB is not merely waiting for better data. It faces a structural tension between sticky wage growth and potentially transitory energy relief, a combination that makes early easing riskier than patience.

ECB structural balance sheet risks from approximately 425 billion euros in private credit exposure across European insurers, banks, and pension funds add a layer of financial stability constraint to the rate decision framework that operates entirely separately from the energy price dynamics the current policy debate is focused on.

Two-year interest rate swaps are among the cleanest real-time indicators of where the market believes policy rates will be over the next 24 months. Their current signal confirms the higher-for-longer narrative, but with a nuance worth tracking.

| Rate | Current Level | Recent Peak | Move | Market Interpretation |

|---|---|---|---|---|

| US 2-year swap | ~4.10% | ~4.35% (early May) | -25 bps | Modest easing priced; no rapid cuts expected |

| Euro 2-year swap | ~2.55% | ~2.80% (late April) | -25 bps | Token easing only; full cycle abandoned |

Both rates have pulled back from their spring peaks, and ING attributes the move to falling crude prices, improved risk sentiment, and repricing away from near-term cuts. The pullback might look like the market pricing in easing. It is not. ING emphasises that “the level of the 2-year still implies only very modest easing priced in, with markets converging to the Fed and ECB’s higher-for-longer narrative.”

Morgan Stanley’s interpretation is more pointed.

Morgan Stanley strategists said the euro swap move “signals markets have given up on a full easing cycle and now price only a token amount of ECB cuts over the next two years.”

The swap market, in other words, has caught up to what officials have been saying. The trade that assumed geopolitical relief would compress the rate timeline has been largely unwound in the pricing.

The analytical framework above carries three specific implications for portfolio positioning, ranked by immediacy.

Geopolitical agreements, Strait of Hormuz normalisation, and crude oil price declines driven by supply events rather than demand or core inflation dynamics all sit within the “look-through” category for both the Fed and ECB. The IMF has stated that central banks should avoid over-reacting to commodity-price-driven disinflation and focus on core inflation and expectations. The OECD concluded that major central banks “are likely to maintain restrictive stances until core inflation is convincingly on target.”

Sustained core PCE prints at or below 2.3% over multiple consecutive months, evidence of wage growth deceleration in the US and Europe, and material labour market loosening: these are the triggers investors should track rather than diplomatic announcements.

The Fed and ECB have built their current policy stances on core inflation and labour market dynamics. Geopolitical developments, however significant for crude oil markets, sit outside the reaction function that governs rate decisions. That is not a reading of the tea leaves; it is what officials have said, what institutional research supports, and what swap markets now price.

What would change the picture is not a single geopolitical event but a sufficiently large and sustained decline in core inflation driven by multiple data points accumulating over months. That process, if it occurs, is more likely to become visible in late 2026 than in the next quarter.

The data events that actually matter in the coming months are core PCE releases, US jobs reports, and eurozone wage settlement data. Not diplomatic announcements from Doha. Not naval patrol updates from the Strait of Hormuz. Investors who build rate-sensitive positions on the wrong catalyst will pay a carrying cost while waiting for a policy shift that the geopolitical narrative, by itself, cannot deliver.

For investors wanting to map how the rate path described here translates into specific positioning risk in the weeks ahead, our dedicated guide to the June 2026 central bank window examines how the ECB, Bank of Japan, Federal Reserve, and Bank of England delivering decisions within eight days creates an unprecedented compression of repricing risk across currencies, bonds, and equities, including the added complication of Kevin Warsh chairing his first Fed meeting.

This article is for informational purposes only and should not be considered financial advice. Investors should conduct their own research and consult with financial professionals before making investment decisions. Past performance does not guarantee future results. Financial projections are subject to market conditions and various risk factors.

The consensus among major institutions including Goldman Sachs, JPMorgan, and ING points to late 2026 as the earliest realistic window for a first Fed cut, contingent on core PCE falling convincingly below 2.5% on a sustained basis and evidence of labour market cooling.

Both the Fed and ECB use a 'look-through' framework for temporary, geopolitically driven oil price shocks, meaning they only adjust policy if those shocks produce second-round effects on core inflation, wages, and inflation expectations, which a crude price dip alone does not trigger.

The Fed requires sustained core PCE prints at or below approximately 2.3% across multiple consecutive months, measurable labour market cooling, and several consecutive good inflation readings before officials have indicated they would consider cutting rates.

As of late May 2026, the US two-year swap rate sits around 4.10% and the euro two-year swap around 2.55%, levels that imply only very modest easing priced in, confirming that markets have largely converged to the Fed and ECB's higher-for-longer narrative rather than pricing aggressive cuts.

Lower headline oil prices can reduce input costs and improve margins for energy-intensive sectors, but assets that depend on actual rate cuts, such as duration-sensitive bonds and highly leveraged growth equities, require a separate catalyst entirely, specifically sustained declines in core inflation and wage growth.