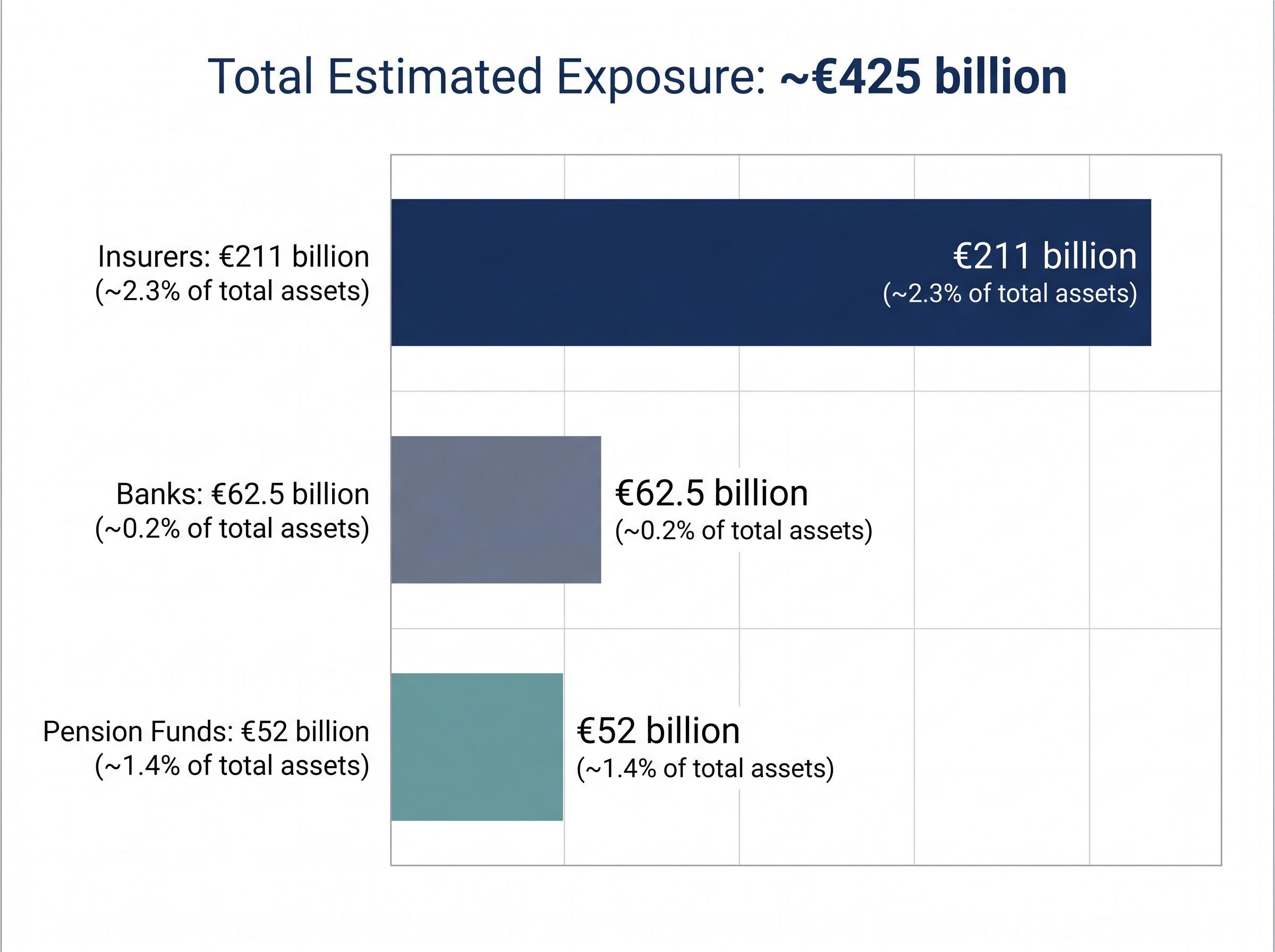

According to ECB estimates, European insurers hold an estimated €211 billion in private credit exposure. Banks carry roughly €62.5 billion. Pension funds account for another €52 billion. Together, these three institution types sit on approximately €425 billion in exposure to one of the fastest-growing and least transparent corners of global finance, and the European Central Bank’s latest assessment warns that a severe shock could trigger second-round losses well beyond the direct hit, through equity portfolio revaluations at the very institutions least equipped to absorb them quickly.

Private credit has grown at roughly 14% annually since 2010, quietly becoming a market that now rivals some public debt segments in scale. According to ECB assessments, findings arrive as US-based vehicles in the sector are already showing stress, with redemption pressures at business development companies (BDCs) and high-profile corporate defaults raising questions about whether the asset class has been mispriced at scale. What follows explains what the ECB found, why the contagion pathway matters more than the headline direct-loss figure, which institutions carry the most risk, and what the data gaps mean for investors trying to price a market that resists being priced.

Why the ECB is sounding the alarm on private credit now

The trigger was American, not European. Observable stress in the US segment of the private credit market drew the ECB’s attention before any comparable European crisis had begun to unfold.

In early 2026, several US-listed BDCs, the primary vehicles through which retail and institutional investors access private credit, faced significant investor withdrawal requests. Some funds invoked contractual provisions to limit outflows, a mechanism that signals liquidity strain even when it prevents outright failure.

Two US corporate defaults sharpened the urgency:

- According to reported accounts, BDC redemption pressures emerged, with some funds gating withdrawals under contractual provisions

- First Brands, a US auto components producer, has been reported as defaulting on private credit obligations

- Tricolor, a subprime auto lender, has been reported as entering default under its private credit facilities

These three signals made the ECB’s European exposure mapping urgent. The concern was not that Europe had already suffered losses, but that European institutions held substantial positions in an asset class whose US segment was visibly cracking.

The US default surge running beneath headline credit indices provides the quantitative backdrop for the ECB’s concern: Proskauer’s Private Credit Default Index reached 2.73% in Q1 2026, Fitch projected leveraged loan default rates of 4.5-5.0% for the full year, and capital is rotating aggressively away from legacy software and highly leveraged borrowers toward AI-focused debt, fracturing the market in ways that aggregate figures obscure.

Leveraged loan market conditions heading into mid-2026 reveal the same bifurcation dynamic at a macro level: high-rated debt has held relatively stable while CCC-rated paper faces severe pricing penalties, BDC net asset values are eroding, and institutional capital is rotating out of syndicated loans into private credit and AI-focused investments as a defensive response to the maturity walls ahead.

When big ASX news breaks, our subscribers know first

What private credit actually is, and why its growth creates structural blind spots

Private credit refers to debt financing provided by non-bank lenders directly to companies, outside public bond or loan markets. There is no exchange listing, no public pricing, and no daily mark-to-market valuation of the kind that forces investors in listed bonds to confront losses in real time.

That absence of continuous pricing is the structural feature that converts a lending model into a risk problem. Stress can accumulate invisibly inside a private credit portfolio until a liquidity event, such as a fund redemption wave or a borrower default, forces recognition. By the time losses become visible, they may already be large.

The private credit liquidity mismatch sits at the structural core of this risk: funds built on illiquid loans increasingly offer periodic redemption windows to investors, and when withdrawal requests exceed what the portfolio can satisfy without forced asset sales, gates activate and losses can spill into public equity markets through the very mechanism the ECB’s scenario models.

The market has grown at approximately 14% annually since 2010. According to ECB data, private credit funds headquartered in the euro area managed approximately €100 billion in assets under management as of 2025. The ECB explicitly noted that insufficient data availability impedes a thorough evaluation of risks across the sector.

The ECB called for stronger EU-wide data gathering and cross-border information sharing, acknowledging that regulators themselves lack the visibility needed to fully assess private credit exposures.

Why software sector concentration matters

The software sector represents the largest single subsector within global private credit by transaction volume. Deteriorating credit quality among software borrowers, combined with concentrated fund exposures to this single industry, amplifies the risk of correlated losses across multiple lenders simultaneously. If several software-focused borrowers experience distress in the same period, funds with overlapping exposures face write-downs that arrive together rather than in isolation.

The €425 billion exposure map: which European institutions carry the most risk

The ECB’s assessment identifies three institution types with material private credit holdings, each carrying a different scale of exposure and a different vulnerability profile.

| Institution Type | Estimated Exposure | As % of Total Assets | Primary Risk Channel |

|---|---|---|---|

| Insurers | According to ECB estimates, €211 billion | According to ECB estimates, ~2.3% | Direct credit losses and equity portfolio revaluation |

| Banks | According to ECB estimates, €62.5 billion | According to ECB estimates, ~0.2% | Lending exposures to private credit borrowers |

| Pension Funds | According to ECB estimates, €52 billion | According to ECB estimates, ~1.4% | Direct holdings and equity portfolio spillover |

| Total | ~€425 billion |

The percentage figures provide calibration. At 0.2% of total assets, bank exposure appears contained. At 2.3%, insurer exposure is larger in relative terms but still a fraction of balance sheets. The ECB assessed that private credit, considered independently, is unlikely to pose an immediate threat to euro area financial stability at current levels.

That assessment carries a qualifier. The capacity of euro area firms backed by private credit to cover interest obligations from operating cash flows has been declining, adding a credit quality dimension that sits beneath the volume figures and could shift the risk arithmetic if conditions deteriorate further.

What the ECB’s severe shock scenario actually shows

The ECB’s scenario analysis models what happens when a severe global shock hits private credit markets. The structure of the test reveals why the second-round number matters more than the first.

The transmission follows a four-step sequence:

- Direct private credit losses hit institutions holding the assets

- Market revaluation is triggered as losses become visible and repricing spreads

- Equity portfolio write-downs at insurers and pension funds follow, as their listed holdings in financial firms exposed to private credit decline in value

- Potential feedback into broader asset prices if the revaluation is large enough to force selling

The ECB’s scenario analysis found that broader market spillovers could generate second-round losses through market revaluation that exceed the first-round direct losses themselves.

Insurance corporations and pension funds are identified as the most vulnerable to these indirect spillover effects, specifically via their equity portfolios rather than their direct credit exposures alone. The institutions most exposed to second-round effects are the same ones the ECB flags as most vulnerable, creating a concentration of systemic fragility that makes the “contained” framing conditional on no feedback loop activating.

The next major ASX story will hit our subscribers first

What needs to change, and what investors should watch

The ECB’s policy response centres on visibility. Stronger EU-wide data gathering, cross-border information sharing, and reduced opacity in private credit reporting are the three institutional recommendations. The call for better data is itself a signal: where regulators lack visibility, investors are operating with even less.

The Central Bank of Ireland Financial Stability Review similarly flags the scarcity of information around lending practices in private credit as a core vulnerability within the euro area non-bank financial intermediation sector, reinforcing that the ECB’s data gap concerns extend across multiple Eurozone regulatory bodies.

Four specific indicators merit monitoring as conditions develop:

- Insurer solvency ratios, particularly at European life insurers with large alternative asset allocations

- Pension fund allocation disclosures, where shifts away from private credit would signal institutional reassessment

- BDC net asset value movements, the earliest visible stress indicator given that BDCs report quarterly valuations

- US leveraged-sector default counts, especially in software and subprime auto, the two sectors where stress signals have already emerged

The semi-liquid fund structures that allowed BDCs to gate withdrawals in early 2026 function as both a stabiliser and an early warning system. When gates activate, they prevent runs but confirm that underlying demand for liquidity exceeds what the portfolio can deliver without forced sales.

A sector too large and too opaque to ignore any longer

Private credit has grown large enough to matter systemically but remains opaque enough that neither regulators nor investors can fully price the risk. Insurers carry the largest share of European exposure, pension funds face the sharpest vulnerability to second-round equity spillovers, and banks hold the smallest percentage but sit at the centre of any broader funding stress.

The ECB’s assessment is a floor, not a ceiling. The data gaps it highlights mean the full picture is almost certainly larger than what is currently measurable. For investors with exposure to European financial institutions, the distinction between first-round and second-round losses is where systemic risk lives.

Investors exploring how the same contagion pathway operates in non-European jurisdictions will find our deep-dive into how private credit stress transmits across borders, which examines APRA’s May 2026 system risk assessment and the specific channels through which a stressed global private credit market reaches Australian superannuation funds and bank balance sheets despite insulation from direct European exposures.

This article is for informational purposes only and should not be considered financial advice. Investors should conduct their own research and consult with financial professionals before making investment decisions.