Record U.S. Equity Inflows Signal Fragility, Barclays Warns

3 hrs ago

For decades, investors treated Federal Reserve statements as a roadmap. Every clause was parsed, every adjective weighed, every dot in the Summary of Economic Projections (SEP), the Fed’s quarterly collection of individual rate forecasts, reverse-engineered into a positioning signal. On 17 June 2026, that roadmap was taken off the wall.

Kevin Warsh’s first meeting as Fed Chair produced a shorter statement, no directional lean, and an explicit rejection of the communication regime that had defined Fed policy for over a decade. His remarks at the European Central Bank’s Sintra panel on 1 July 2026, days before a pivotal July FOMC meeting, confirmed this was not a one-off recalibration. The task forces, the withheld dot, the stripped-down statement, and the deliberate refusal to signal: together they constitute the most significant overhaul of Fed communication since the central bank began publishing rate projections.

Here is a framework for understanding what has actually changed in the Fed’s relationship with markets, which parts of your analytical toolkit still work, and which ones need rebuilding before the July meeting.

Warsh was sworn in as the 17th Federal Reserve Chair on 22 May 2026, succeeding Jerome Powell. His first FOMC meeting on 17 June held rates steady, but the statement that accompanied the decision was noticeably shorter and dropped the language that had traditionally hinted at the next move. That alone would have been notable. What followed made it structural.

The conditions Warsh inherited on 22 May 2026 amplify why the communication overhaul carries the weight it does: a committee with four recorded dissents, Brent crude near $105 on Hormuz closure fears, and a rate held for three consecutive meetings amid PCE inflation running well above target.

International Journal of Central Banking analysis of SEP methodology documents how the dot plot evolved from an internal forecasting tool into a primary market anchoring mechanism, a function Warsh’s decision to withhold his own projection directly targets.

“The Fed should not be in the forward-guidance business as a general proposition.” — Kevin Warsh, 17 June 2026 press conference

That quote is the load-bearing statement. Everything else hangs from it. Since taking office, Warsh has moved through a sequence of concrete changes:

Each item on that list represents a lever investors previously used to anchor rate expectations. Losing several simultaneously does not just weaken the scaffolding investors built their positioning around. It partially removes it.

Warsh’s objection to forward guidance is not about preferring silence. It is about what happens when the Fed makes specific commitments and then data force it to reverse course.

Highly specific guidance, rate paths, dots, conditional language, invites credibility problems when the Fed must later deviate as incoming data change. Warsh has argued that this dynamic boxed previous Fed leadership into decisions shaped more by prior signals than by current conditions. Over-commitment narrows the central bank’s room to manoeuvre, and the cost of that narrowing shows up most acutely during periods of rapid data reversal.

The second pillar of Warsh’s framework is more ambitious. He has stated that markets should provide clearer signals about what policy is needed, rather than simply tracking constant Fed commentary for direction. Commentators have described this as a return toward Greenspan-era opacity, a period when markets priced risk without explicit guidance and the Fed’s footprint in day-to-day asset pricing was smaller.

His Sintra remarks reinforced an orthodox inflation focus: Warsh indicated that price pressures had eased, pointing to diminished risks linked in part to the U.S.-Iran preliminary peace accord concluded in June 2026, which had allowed oil prices to pull back toward pre-conflict levels. Guidance, in Warsh’s view, should serve price stability, not asset price management. The communication stance is itself a policy instrument, not merely a preference for quiet.

What this tells you about durability is important. A chair who has concluded that the prior communication regime actively distorted markets and policy will resist pressure to restore guidance even during periods of elevated market stress. This is not a style choice that reverses at the first equity sell-off.

Forward guidance functioned as an anchoring mechanism. When the Fed embedded directional language in its statements or published a dot plot that clustered around a specific rate path, it gave investors a framework for discount rate assumptions, credit spread models, and equity valuation bands. Portfolio managers could narrow the range of plausible rate outcomes, and that narrowing reduced the uncertainty premium embedded across asset classes.

That anchoring is now gone. In its place, Warsh has moved to a strictly data-first, meeting-by-meeting approach. Every FOMC meeting is genuinely live. No prior statement tells you whether the next move is more likely to be a cut or a hold. The replacement object of analysis is the reaction function: understanding how the Fed responds to data, rather than what it says it will do next.

The market repricing on June 18 was swift and concentrated: the two-year Treasury yield surged 18 basis points intraday to 4.22% before closing at 4.17%, with nearly half of FOMC participants in the June SEP now open to rate hikes later in 2026, a reversal not anticipated by consensus positioning entering that meeting.

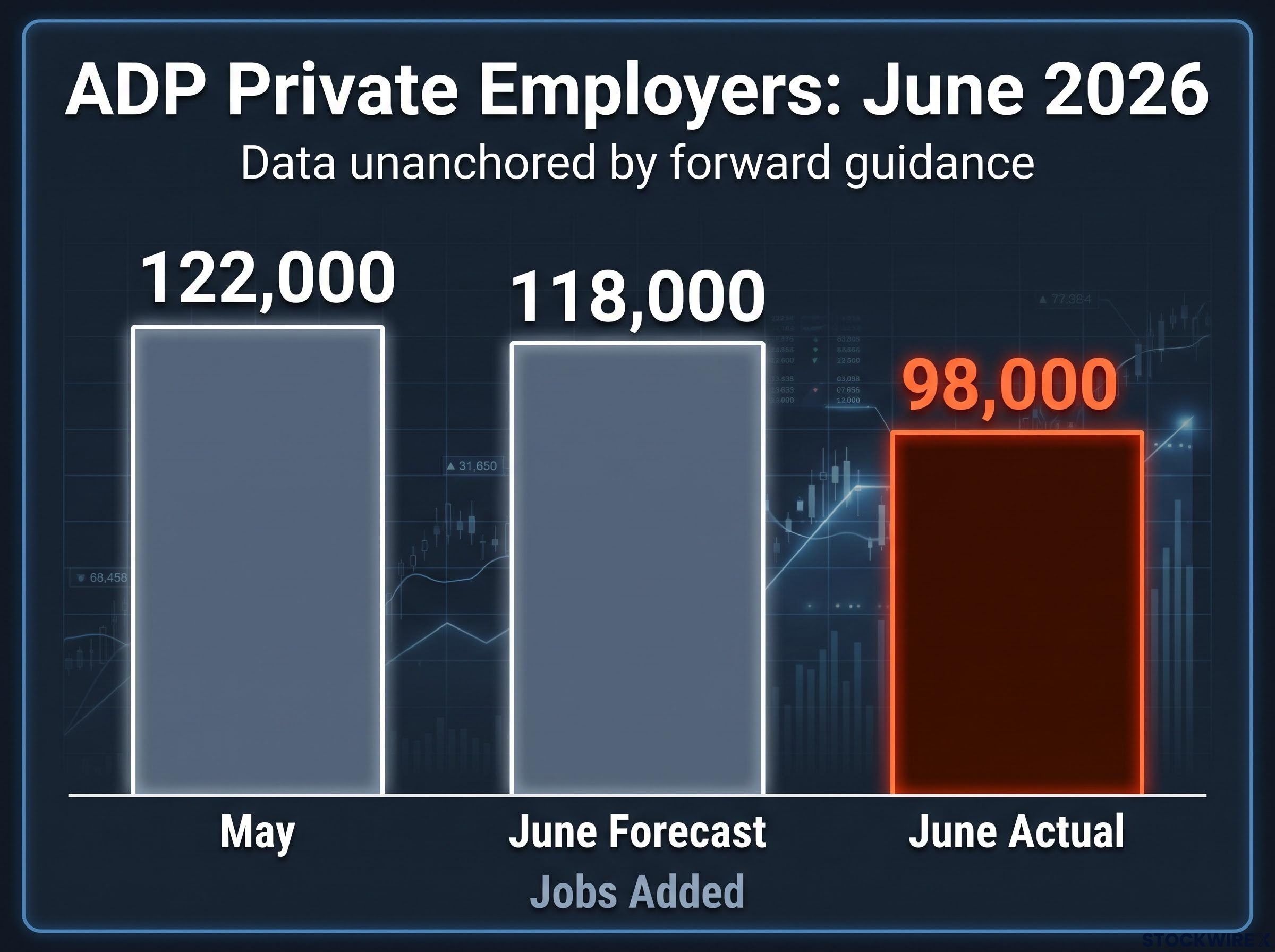

ADP June 2026: U.S. private employers recorded 98,000 new jobs in June, short of the 118,000 forecast and a step down from the 122,000 added in May. Nela Richardson, chief economist at ADP, said the figures reflected both a softening in employer demand and pockets of labour supply tightness across certain sectors.

That print is a working example of the new regime. Under the prior guidance framework, a soft labour number would have been filtered through whatever the Fed had already signalled about its rate path. Under Warsh, it lands directly on rate expectations with no buffer. There is no Fed-provided floor or ceiling to bound the interpretation. Each data release now carries more pricing weight than it did, and investors need to build that interpretive capacity themselves.

| Dimension | Guidance era | Warsh era |

|---|---|---|

| Primary signal source | Fed statements, dot plot, press conferences | Macro data releases, observable Fed behaviour |

| Meeting predictability | High; outcomes largely pre-telegraphed | Low; every meeting genuinely live |

| Key data release impact | Filtered through prior guidance | Direct, unanchored impact on rate pricing |

| Volatility profile | Suppressed between meetings | Elevated around data releases and FOMC dates |

The most immediate impact sits in rates and fixed income. Without a stated bias in the Fed’s communications, uncertainty about the near-term path of the federal funds rate increases mechanically. Expect larger moves in Fed funds futures, overnight index swaps (OIS), and 2-year Treasuries around data releases and FOMC meetings. Bid-ask spreads may widen as dealers adjust to less anchoring from Fed signals, and long-duration positions face greater tail risk of surprise moves relative to the prior regime of telegraphed outcomes.

Equities absorb the shift through the discount rate. When analysts could use narrow bands for future policy rates, equity valuations, particularly in long-duration growth and high-multiple sectors, carried less uncertainty premium. Those bands have now widened, which can compress multiples even if earnings expectations are unchanged. The most rate-sensitive sectors face the sharpest recalibration:

Options markets may also need to reprice event risk. Strategies that sold volatility on the assumption of well-telegraphed Fed decisions could face systematic underperformance in this environment.

In currency markets, the shift has already drawn attention. Lukman Otunuga, Head of Markets at FXTM, has highlighted Warsh’s communication overhaul as a driver of uncertainty, with traders reassessing how to price U.S. monetary policy against central banks that continue to employ forward guidance more actively. Rate-differential expectations become more volatile, feeding directly into FX moves. Credit investors, meanwhile, may demand a small uncertainty premium in spreads to reflect policy ambiguity, particularly in lower-quality or longer-dated issuance.

Global central bank divergence adds a further dimension to the FX volatility picture: with the ECB, Bank of Japan, Fed, and Bank of England all delivering rate decisions within a single eight-day window in June 2026, currency traders faced simultaneous repricing signals from central banks with meaningfully different communication frameworks, not just different rates.

| Asset class | Primary implication |

|---|---|

| Rates / Fixed income | Higher front-end volatility; wider bid-ask spreads; duration positioning less anchored |

| Equities | Wider discount-rate uncertainty bands; multiple compression risk; sector differentiation |

| Credit | Small uncertainty premium in spreads; complicates default and spread projections |

| FX | More volatile rate-differential expectations; carry trades lean more on macro views |

The core implication across all four classes is the same: the uncertainty premium that guidance used to suppress is now a persistent feature of the pricing environment. Portfolios sized for low event risk will be systematically underhedged.

The July FOMC meeting is the first major test of the new regime. Warsh’s Sintra signal of “substantive internal debate” means the outcome distribution is genuinely wide. Here are four strategic adaptations worth implementing before it arrives:

The five task forces, particularly the one reviewing communications and the dot plot, signal that the institutional apparatus of the old regime is under active review and may shift further. Building a model of Warsh’s reaction function from observable data will outperform waiting for guidance to re-emerge, because under this regime, guidance is not coming back as a crutch.

The prior guidance regime rested on an embedded assumption: that reduced uncertainty via Fed communication was an unambiguous good, and that the central bank should smooth day-to-day asset price volatility. Warsh has rejected both premises. His counter-thesis is that excessive guidance created market dependence, reduced policy flexibility, and fed into policy errors by making the Fed captive to its own signals.

The five task forces are evidence that institutional change is underway, not just rhetorical repositioning. The machinery of the old regime is being audited from the inside.

Markets priced risk without explicit forward guidance for decades during the Greenspan era. The skills required exist. They are just rusty.

For investors wanting a structural foundation for why Warsh’s retreat from guidance may be less destabilising than it appears, our full explainer on Federal Reserve limitations examines how the Fed directly controls only the overnight interbank rate and how Friedman’s long and variable lags make discretionary fine-tuning systematically error-prone.

There is a distinction worth holding onto here: communication opacity is not the same as policy incoherence. A quieter Fed that remains consistent with observable data and a clearly stated inflation objective is still modelable. The investor’s job is to build that model rather than wait for the Fed to provide one.

For the market relationship long term, the question is not whether Warsh is right philosophically. It is whether your current analytical infrastructure is built to generate returns in an environment where the Fed no longer provides the anchoring signal you have relied on. The near-term cost is a more uncertain policy environment. The potential long-term benefit is a market that relies less on Fed words and more on fundamentals. The investors who adapt their sourcing of market intelligence first will be better positioned than those who wait.

This article is for informational purposes only and should not be considered financial advice. Investors should conduct their own research and consult with financial professionals before making investment decisions. Forward-looking statements regarding Fed policy and market outcomes are speculative and subject to change based on economic developments and the Federal Reserve’s evolving communication framework.

Fed forward guidance is the practice of communicating the likely future path of interest rates through statements, dot plots, and press conferences, giving investors a framework for discount rate assumptions and reducing uncertainty premiums across asset classes. Under Warsh, this anchoring mechanism has been deliberately dismantled, meaning rate expectations now move directly with incoming data rather than being filtered through prior Fed signals.

Since taking office on 22 May 2026, Warsh has shortened and de-signaled the FOMC policy statement, withheld his own dot plot projection from the SEP, launched a communications task force reviewing the dot plot's future role, and explicitly stated the Fed should not be in the forward-guidance business as a general proposition.

Without a stated directional bias from the Fed, the two-year Treasury yield surged 18 basis points intraday on 18 June 2026 alone, and front-end volatility is now structurally higher around data releases and FOMC meetings, with bid-ask spreads widening as dealers lose the anchoring effect of Fed signals.

Financials, REITs, utilities, and housing-related equities face the sharpest recalibration because their valuations are most sensitive to rate surprises; wider discount-rate uncertainty bands can compress multiples even when earnings expectations are unchanged.

Investors should shift focus from parsing Fed statements to building rate scenarios directly from macro data releases such as CPI, PCE, payrolls, and ISM surveys, treat every FOMC meeting as genuinely live, and use swaptions and equity volatility instruments as central portfolio construction tools rather than supplementary hedges.