AstraZeneca’s £300M UK Investment Reverses 2025 Retreat

15 mins ago

Etsy shares jumped in early trading on 29 April 2026 after the e-commerce platform delivered an unexpected first-quarter revenue beat. The immediate equity valuation surge provides relief for a marketplace that has spent the past two years battling declining buyer engagement and soft discretionary demand. The stock had previously fallen roughly 78% from its pandemic highs before beginning a recent recovery phase.

Investors have eagerly awaited these results to see if the recent 26.47% one-month stock rebound is justified by underlying fundamentals. Today’s first-quarter disclosures reveal significant shifts in consumer behaviour and structural corporate changes. The market reaction suggests renewed confidence in the platform’s core operations.

This analysis examines the latest Etsy earnings details, exploring both the quarterly financial surprises and the strategic impact of offloading a major subsidiary to a competitor. Understanding these metrics provides a foundation for evaluating the company’s trajectory throughout the remainder of the calendar year.

The first-quarter financial disclosure delivered an immediate jolt to the market, driven primarily by top-line outperformance. According to early reports, total quarterly income reached $631.3 million, comfortably surpassing consensus forecasts of $621.1 million. This represents a core platform income expansion of 7.6% year-on-year, a significant achievement given the broader macroeconomic headwinds affecting consumer retail.

The official Etsy Form 8-K filing confirms these top-line figures alongside broader operational metrics, formalising the company’s financial position for regulatory authorities.

However, the optimism surrounding the revenue beat is grounded by a marginal shortfall in per-share profitability. Modified per-share profits came in at $0.60, just missing the $0.62 Wall Street target. Despite this slight miss, the company generated modified earnings of $185 million, yielding a strong 29.3% profitability ratio that demonstrates consistent operational efficiency.

The combination of top-line growth and solid overall profitability metrics triggered an immediate positive market reaction. The post-disclosure equity valuation increased by 6.3%, suggesting investors are willing to overlook the minor per-share profit miss in favour of broader revenue recovery.

| Q1 2026 Metric | Wall Street Estimate | Actual Result | Percentage Difference |

|---|---|---|---|

| Total Quarterly Income | $621.1M | $631.3M | +1.64% |

| Modified Per-Share Profit | $0.61 | $0.60 | -1.64% |

While top-line revenue can sometimes be engineered through fee increases, core volume growth proves that actual buyers and sellers are returning to the marketplace. The platform achieved positive annual expansion in total transaction volume for the first time in over twenty-four months, signalling a structural return to health. Core platform merchandise volume expanded.

This represents a sharp reversal from the 0.5% drop recorded in the final three months of 2025. The turnaround velocity highlights a genuine revival in marketplace activity rather than a superficial financial adjustment. Corporate data indicates this volume expansion is supported by broad-based operational improvements that are drawing consumers back to the platform.

Like other major consumer brands launching strategic turnaround initiatives, the company is relying on a combination of digital engagement upgrades and core product discovery improvements to rebuild long-term transaction frequency.

The return to volume growth is driven by three distinct operational achievements:

Annual increases in fresh shopper acquisition Rising active vendor participation across core categories * Higher individual purchaser spending per transaction

Understanding the long-term survival of any e-commerce platform requires distinguishing between corporate revenue and Gross Merchandise Sales. Gross Merchandise Sales measures the total dollar value of all goods sold across the platform, while corporate revenue represents only the fees and commissions the company extracts from those transactions. This distinction provides a clear framework for evaluating e-commerce stocks, as it separates the money a platform facilitates from the money it keeps.

Global market analysts apply this same framework when evaluating international e-commerce marketplace integrations, measuring how effectively unified discovery platforms can sustain gross merchandise volumes outside of heavy promotional periods.

Historical context illustrates exactly why current volume growth is a major milestone for the company. The platform reached a peak volume of $12.2 billion in 2021 before suffering a prolonged decline as pandemic-era shopping habits normalised. By the end of 2025, full-year volume had dropped to approximately $10.46 billion.

Current corporate strategies are actively attempting to align with observable shifts in consumer activity to rebuild this underlying volume. Leadership has explicitly focused on adapting platform discovery and search functions to capture changing discretionary spending patterns.

Leadership Perspective “Management notes that strategic adjustments to product discovery and promotional tools are directly aligning with evolving consumer activity shifts, laying the foundation for sustainable volume recovery.”

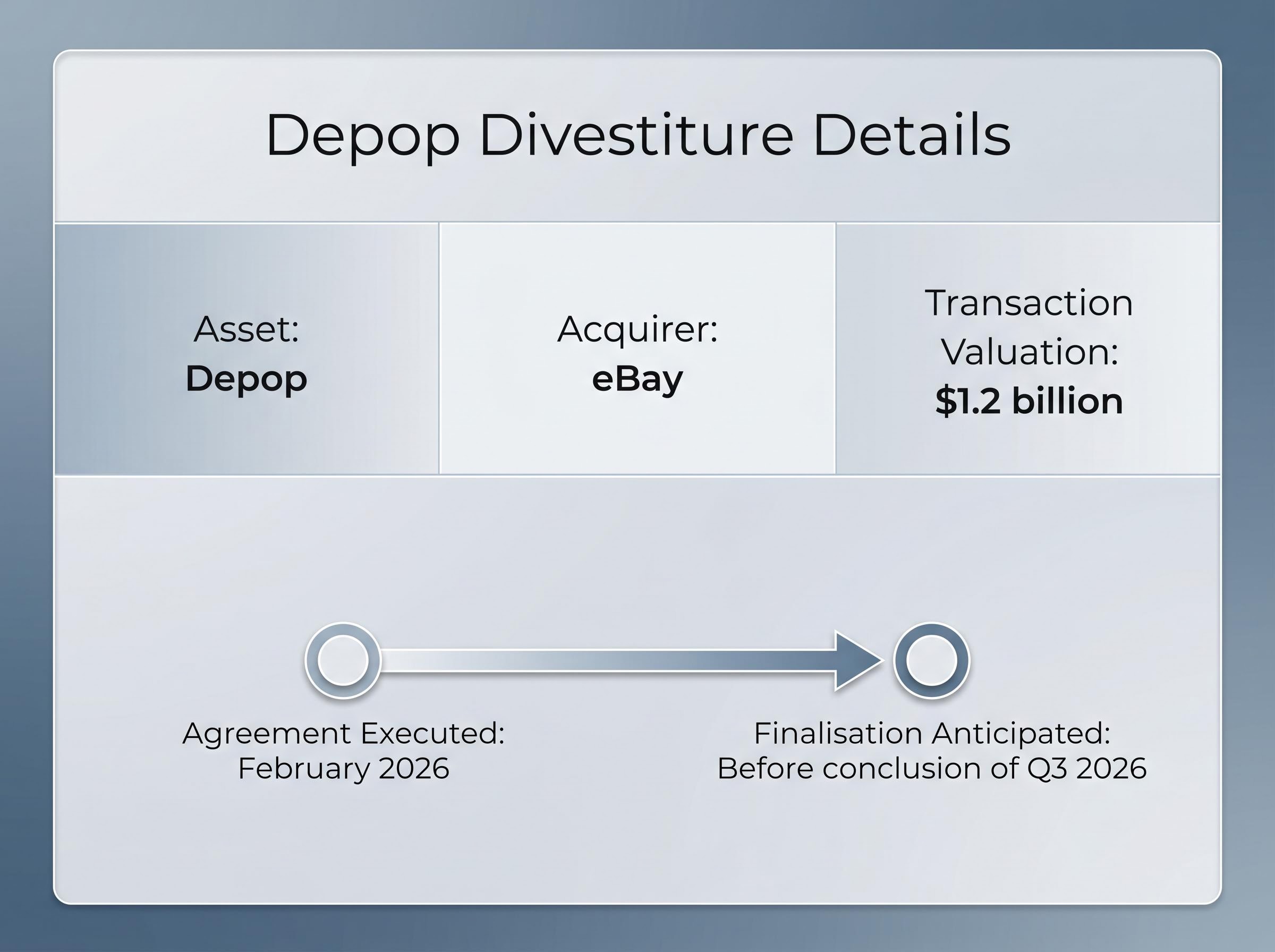

Management has paired internal platform improvements with a massive strategic divestiture designed to streamline corporate focus. The company executed a definitive agreement to transfer ownership of the secondary apparel marketplace, Depop, to competitor eBay. This major transaction effectively removes a disparate brand from the corporate portfolio, allowing leadership to direct all resources toward defending the core platform against emerging e-commerce challengers.

Securing a clean cash exit was a primary objective of the negotiation, and the official eBay acquisition announcement confirms the structure will provide immediate liquidity for core platform investments.

The current first-quarter financial reporting deliberately omits contributions from this offloaded subsidiary. Stripping away the secondary marketplace provides investors with a cleaner view of the primary platform’s fundamental performance. Raising capital through this divestiture also creates a financial buffer that strengthens the company’s balance sheet.

The definitive agreement for the sale was officially executed in February 2026, carrying a total transaction valuation of $1.2 billion. The transfer progression is currently navigating standard regulatory approval requirements for acquisitions of this size. Finalisation of the transfer is anticipated before the conclusion of the third quarter of 2026.

Forward guidance remains the primary driver of institutional investment decisions, and corporate leadership has provided a measurable roadmap for the upcoming months. The updated operational forecasts project a shift toward sustained positive volume growth, replacing the defensive corporate statements that characterised the previous two years.

The specific margin expectations demonstrate how the revived transaction volume translates directly to sustained profitability. Providing exact parameters allows retail and institutional investors to benchmark the company’s performance against historical data and peer averages.

Corporate leadership outlined the following upgraded parameters for the remainder of the calendar year:

For traders wanting to model the immediate equity pricing impact of these upgraded parameters, our comprehensive walkthrough of earnings season options pricing explains how implied volatility metrics collapse after disclosures and provides a clear framework for evaluating post-announcement market expectations.

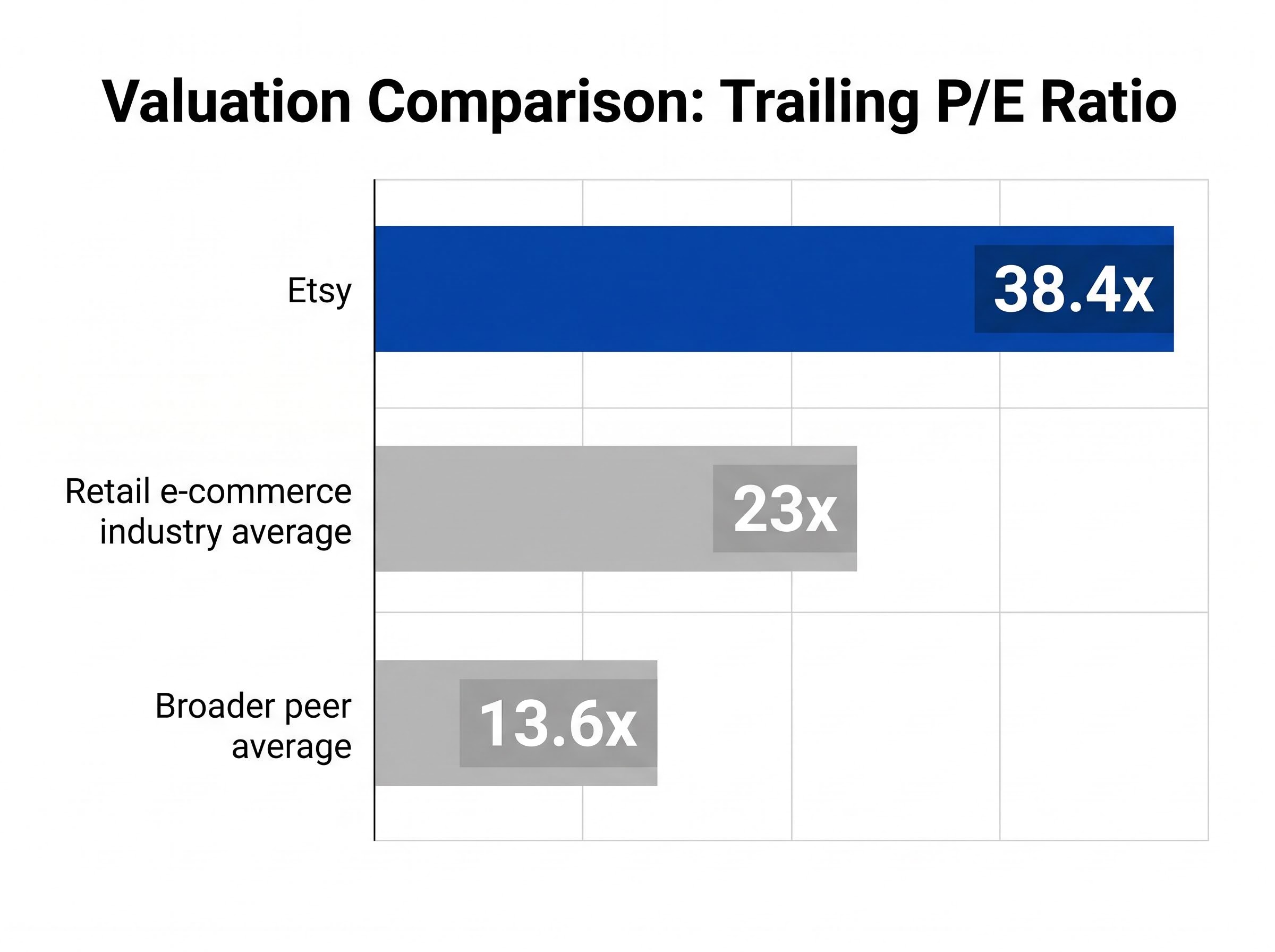

The combination of a substantial revenue beat, a return to transaction volume growth, and the strategic $1.2 billion subsidiary offload presents a cohesive turnaround narrative. However, objective analysis requires noting the stock’s current trailing valuation multiples compared to peer averages to maintain perspective amid the immediate market enthusiasm. The stock trades at a trailing price-to-earnings ratio of approximately 38.4x, which remains significantly higher than the retail e-commerce industry average of roughly 23x and the broader peer average of 13.6x.

This elevated valuation multiple suggests the market is already pricing in a flawless execution of the ongoing recovery strategy. The critical question moving forward is whether the core marketplace can sustain this momentum through the holiday season without the buffer of secondary subsidiaries.

This article is for informational purposes only and should not be considered financial advice. Investors should conduct their own research and consult with financial professionals before making investment decisions. Past performance does not guarantee future results. Financial projections are subject to market conditions and various risk factors.

Etsy's first-quarter income reached $631.3 million, surpassing consensus forecasts of $621.1 million due to a 7.6% year-on-year core platform income expansion, indicating strong top-line performance.

Etsy divested its Depop subsidiary to eBay for $1.2 billion to streamline corporate focus, directing all resources toward defending its core platform and strengthening its balance sheet with immediate liquidity.

Etsy achieved positive annual expansion in total transaction volume for the first time in over twenty-four months, reversing a previous decline and signaling a structural return to marketplace health.

Etsy projects quarterly annual merchandise volume expansion of 3% to 5% and reaffirmed full-year adjusted profitability margin targets of 28% to 30%, signaling a shift toward sustained positive growth.