Finfluencer Rules Won’t Work Until the Penalty Beats the Profit

2 hrs ago

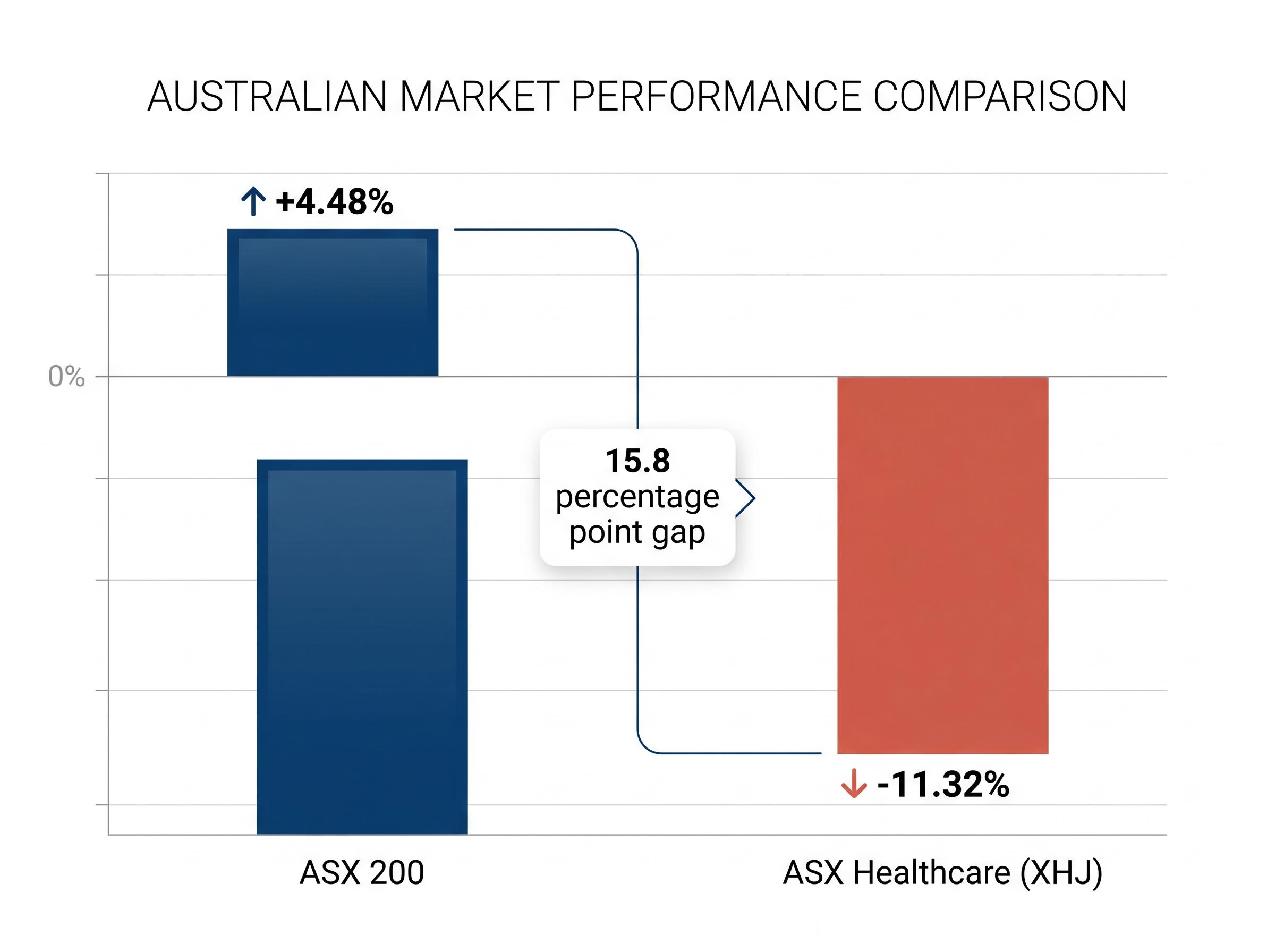

The ASX healthcare sector delivered an annualised return of -11.32% over the past five years. Over the same period, the ASX 200 returned +4.48%. For a sector that earned its reputation as the market’s strongest defensive allocation, and that held the title of top-performing sector during the Global Financial Crisis, this is not a minor deviation. It is a 15.8 percentage point annual gap that demands a precise explanation.

Australian investors now face a genuine analytical tension. Healthcare’s long-run credentials remain structurally sound: ageing populations, chronic disease prevalence, and technology adoption continue to expand demand. Yet the near-term track record has empirically contradicted the defensive label that underpinned a decade of capital allocation. What follows traces the specific mechanisms behind the underperformance, tests them against company-level evidence from CSL, ResMed, Ramsay Health Care, and Sonic Healthcare, and constructs the conditional framework for evaluating whether the current dislocation represents a cyclical reset or a genuine opportunity.

The numbers are stark enough to earn a second look.

The gap: The S&P/ASX 200 Healthcare Index (XHJ) returned -11.32% annualised over five years. The ASX 200 returned +4.48% annualised over the same period.

During the GFC, healthcare was the ASX’s best-performing sector. Predictable demand, lower cyclicality, and stable cashflows delivered exactly what defensive positioning promises in a credit-driven crisis. The same attributes that generated that outperformance became the problem in the 2022-2024 rate hiking cycle.

The mechanism was a “bond-proxy unwind.” Healthcare stocks with stable, long-duration cashflows had been priced like bonds throughout the low-rate era, carrying premium multiples justified by yield scarcity. When bond yields rose, that premium reversed. Investors rotated capital into cyclicals and resources, and the very predictability that had attracted a decade of inflows became a reason to sell.

Three forces drove the drawdown simultaneously:

The attributes that made healthcare the GFC’s winner are not mythological. They are real. But they operate in one direction during credit crises and in the opposite direction during rate-driven tightening cycles.

The macro story is clean. The company-level reality is messier, and more instructive.

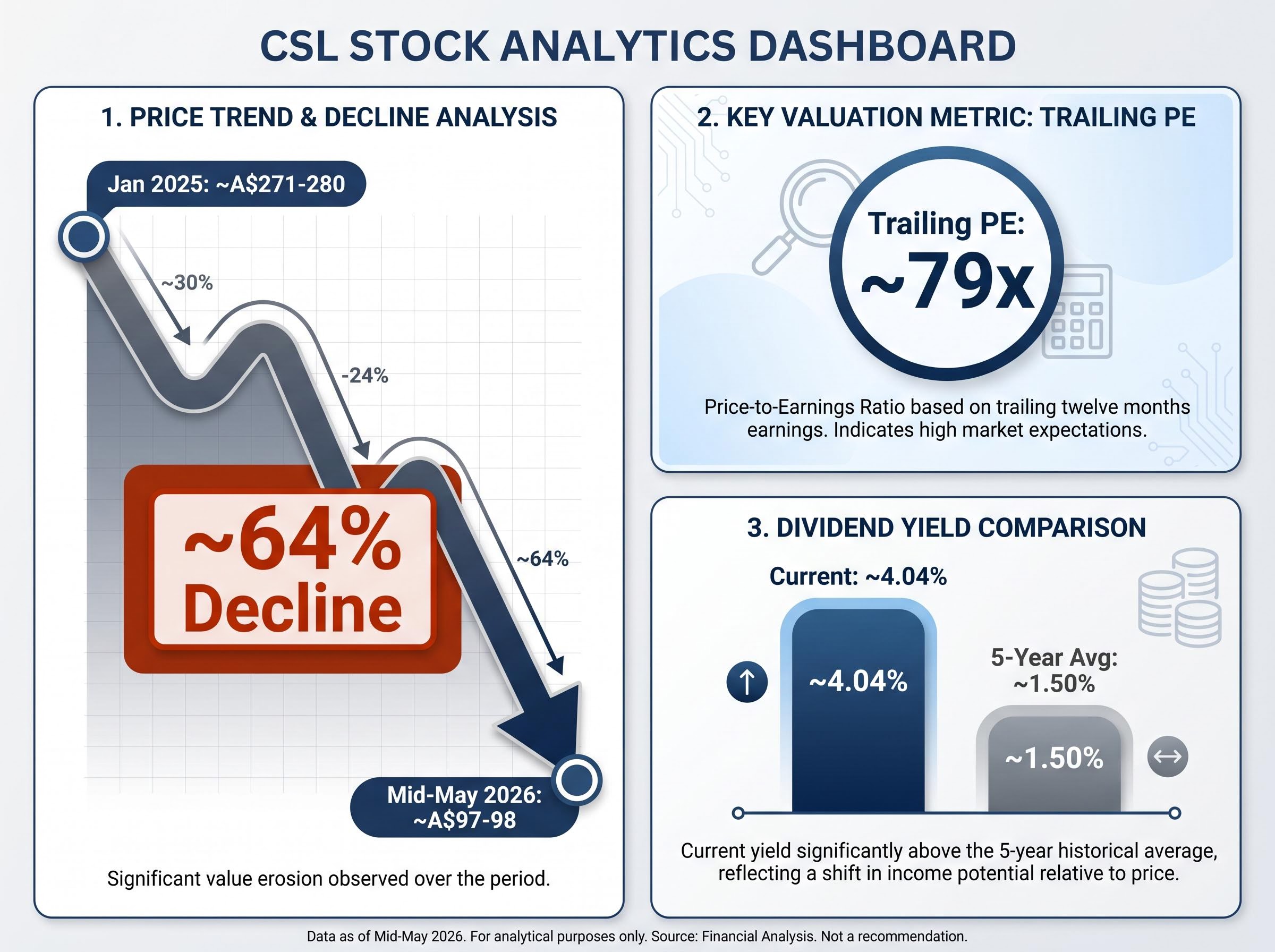

CSL entered January 2025 trading at approximately A$271-280. As of mid-May 2026, the share price sits at approximately A$97-98, a decline of roughly 64%. The trailing price-to-earnings ratio (PE), which measures how much investors pay per dollar of company earnings, stands at approximately 79x. That elevated multiple despite a steep price decline tells a specific story: earnings per share (EPS) have contracted materially alongside the share price. This is not a simple valuation reset on stable earnings. It is dual compression, both multiple and earnings, and any recovery thesis depends on genuine EPS improvement.

CSL’s guidance revision, which cut FY26 revenue expectations by approximately $650 million across three discrete headwinds in US immunoglobulin channel inventory, China albumin pricing, and competitive pressure on Vifor iron products, illustrates why the dual compression of multiple and earnings is not a single event but a sequence of overlapping operational challenges.

CSL’s trailing dividend yield has risen to approximately 4.04%, compared with a five-year historical average of approximately 1.50%, reflecting the price decline rather than increased payouts.

ResMed faced a different headwind. Market concerns around GLP-1 obesity drugs (including Ozempic and Wegovy) potentially reducing long-term sleep apnoea incidence drove a significant de-rating. ResMed management has consistently argued in results presentations that GLP-1 drugs will have minimal medium-term impact on the addressable market, with only potential long-tail effects. The tension between market fear and management’s stated position remains unresolved.

ResMed’s valuation de-rating is a cleaner example of multiple compression than most: the company reported 11% revenue growth and 21% non-GAAP EPS gains in Q3 FY2026, yet the ASX CDI price fell roughly 21.7% from January 2025 highs, a divergence that isolates GLP-1 sentiment and discount rate effects from underlying business performance.

Ramsay Health Care and Sonic Healthcare share a different set of headwinds. Post-COVID revenue normalisation removed the cyclical tailwinds that had inflated near-term earnings. Nursing and energy cost inflation compressed margins. Private health insurer pricing discipline constrained revenue growth. Broker commentary from firms including Morgans and Ord Minnett has pointed to FY24-FY25 as a potential profitability trough for domestic hospital and pathology operators.

| Company | Primary headwind | Key data point | Recovery dependency |

|---|---|---|---|

| CSL | Dual EPS and multiple compression | Trailing PE ~79x despite ~64% price decline | Genuine EPS recovery via plasma efficiency and Vifor synergies |

| ResMed | GLP-1 disruption fear | Significant de-rating on addressable market concerns | Clinical and real-world GLP-1 data clarity |

| Ramsay | Labour costs and insurer pricing | Elective surgery recovery slower than expected | Cost curve stabilisation and volume normalisation |

| Sonic | COVID revenue normalisation | Base pathology growth offset by wage inflation | Margin recovery as COVID-era comparables fade |

A sector earns a defensive reputation through three characteristics: predictable demand that persists regardless of economic conditions, spending that is difficult for consumers or governments to defer, and lower revenue cyclicality relative to sectors like resources and financials. Healthcare ticks all three. People require medical treatment in recessions. Governments fund public health systems through downturns. Elective procedures may defer, but the baseline demand curve is structurally upward-sloping.

These characteristics create a specific market dynamic. When bond yields are low, investors treat stable-cashflow sectors as substitutes for fixed income, paying premium multiples for earnings predictability. This is the bond-proxy relationship. It works powerfully in the sector’s favour during credit crises, where earnings stability is scarce and highly valued.

The relationship inverts when yields rise. Duration, meaning the sensitivity of a long-dated cashflow stream to changes in discount rates, becomes the dominant variable rather than earnings quality. Concentration within the XHJ amplifies this effect: CSL’s significant index weight means a single-name drawdown translates into an index-level drag that overstates the breadth of the underperformance.

Duration risk in rate-sensitive assets operates by a straightforward but often underestimated arithmetic: a fund or stock with an effective duration of 17 years loses approximately 17 cents of capital value for every 1 percentage point rise in yields, regardless of how attractive its income stream appears on paper.

Healthcare’s defensive attributes become a liability in rate-driven downturns rather than growth-driven downturns. The same cashflow predictability that commands a premium when yields are scarce becomes a duration penalty when yields are abundant.

The sequential logic is:

The re-rating case rests on four conditions, each observable and none guaranteed. The RBA’s rate trajectory is the first. If markets price in rate cuts, the bond-proxy dynamic that punished healthcare could reverse, supporting multiple expansion for long-duration cashflow stocks. The second is CSL’s EPS trajectory: with a trailing PE of approximately 79x, normalisation requires genuine earnings growth rather than a simple sentiment-driven re-rating on flat earnings.

The RBA’s May 2026 rate decision and accompanying forward guidance on inflation provide the most current signal for assessing whether the bond-proxy headwind that compressed healthcare multiples is approaching a turning point or remains entrenched.

GLP-1 clarity represents the third condition. As more clinical and real-world data emerge on GLP-1 drug utilisation and sleep apnoea outcomes, the uncertainty discount applied to ResMed could narrow. The fourth is domestic margin stabilisation for Ramsay and Sonic as wage pressures ease and elective surgery volumes recover.

Ramsay’s margin trajectory has shown early evidence of the stabilisation the recovery thesis requires, with 40 basis points of Australian hospital margin improvement and a 6.3% dividend increase in the most recent reporting period, though broker commentary has consistently framed FY24-FY25 as a trough rather than a confirmed recovery.

The macro backdrop supports the ceiling, if not the trigger. US healthcare spending is projected to grow at approximately 7% annually through 2027, potentially reaching US$819 billion. Healthcare IT, data solutions, and software-as-a-service (SaaS) platforms are forecast to grow at more than 15% per year from 2024 through 2030, offering a higher-growth entry point for investors seeking more aggressive exposure within the healthcare thematic.

Fund manager commentary from firms including Platinum, Hyperion, and Wilson Asset Management has described the current environment as offering selective opportunities following the de-rating, though positioning remains cautiously constructive rather than outright bullish.

| Catalyst | What needs to happen | Observable signal to watch |

|---|---|---|

| Rate direction | RBA signals or delivers rate cuts | RBA meeting statements and forward guidance |

| CSL EPS recovery | Plasma efficiency and Vifor synergies lift earnings | Quarterly and half-year EPS prints versus consensus |

| GLP-1 clarity | Clinical data narrows addressable market uncertainty | GLP-1 real-world utilisation studies and sleep apnoea outcome data |

| Domestic margin stabilisation | Wage inflation moderates; volumes normalise | Ramsay and Sonic margin guidance in FY25-FY26 results |

Healthcare is broadly compatible with environmental, social, and governance (ESG) mandates due to its social impact characteristics. Australian responsible investment managers generally classify the sector as ESG-positive or neutral. As sustainable assets under management grow, healthcare stands as a plausible beneficiary of mandate-driven allocation.

A Morgan Stanley survey found more than 50% of investors intended to raise their sustainable investment exposure in 2024, indicating the directional trend in allocator intent.

That directional signal warrants careful calibration. No publicly available data isolates sector-level ESG flows specifically into Australian healthcare. The Responsible Investment Association Australasia (RIAA) publishes aggregate responsible investment benchmarks, but healthcare-specific allocations are not broken out in open reports.

RIAA’s Responsible Investment Benchmark Report for Australia provides aggregate data on the size and growth of the domestic responsible investment market, though it does not break out healthcare-specific allocations, which limits the precision with which sector-level ESG flow estimates can be made.

Healthcare’s ESG profile is also not straightforward:

Available evidence suggests that institutional underweights in healthcare are driven primarily by valuation and earnings factors rather than ESG screening. ESG compatibility is a real but secondary consideration; performance and macro conditions dominate positioning decisions.

Two interpretations of the underperformance compete for investor attention. The cyclical reset interpretation holds that rate-cycle headwinds, post-COVID normalisation, and temporary company-specific fears drove the drawdown, and that these factors will reverse as conditions shift. The structural opportunity interpretation goes further: it argues that the de-rating has created entry points into high-quality compounders with intact secular demand at valuations not seen in a decade.

The variables that distinguish these outcomes are observable. If CSL’s EPS trajectory inflects upward and the trailing PE compresses toward historical averages on rising earnings, the opportunity thesis gains evidence. If EPS continues to deteriorate and the elevated trailing multiple persists, the reset thesis weakens. GLP-1 clinical data, RBA rate decisions, and domestic cost curve trajectories each provide testable signals.

Fund manager commentary from Platinum, Hyperion, and Wilson Asset Management frames the underperformance as cyclical within a strong secular growth story. The sector’s structural demand drivers, including an ageing Australian and global population, rising chronic disease prevalence (diabetes, obesity, cardiovascular conditions), and healthcare technology adoption, remain intact and are not in serious dispute.

Healthcare’s defensive reputation was built on real performance in a real crisis. The GFC outperformance was not a statistical anomaly. The secular demand drivers, ageing populations, chronic disease, and technology adoption, have not weakened. Global healthcare spending growth projections remain intact.

The five-year underperformance reflects specific, identifiable, and in several cases reversible conditions: a rate regime that punished bond-proxy characteristics, post-COVID earnings normalisation, and company-level headwinds that coincided with the macro shift. Whether these conditions reverse is not a matter of belief. It is a matter of tracking observable signals: EPS prints, rate decisions, GLP-1 data, and domestic margin trajectories.

The investor’s task is not to make a binary call on the sector’s future based on its recent past. It is to track the conditional catalysts this analysis has identified, update the assessment as evidence arrives, and recognise that timing and valuation entry will determine whether the sector’s next five years look like the last five or the decade that preceded them.

This article is for informational purposes only and should not be considered financial advice. Investors should conduct their own research and consult with financial professionals before making investment decisions. Past performance does not guarantee future results. Financial projections are subject to market conditions and various risk factors.

The bond-proxy effect occurs when investors treat stable-cashflow sectors like healthcare as substitutes for fixed income, paying premium valuations for earnings predictability. When interest rates rise, this premium reverses because the long-duration nature of healthcare cashflows becomes a liability, compressing multiples and dragging sector returns lower.

Three overlapping forces drove the underperformance: rising interest rates compressed the bond-proxy premium built into healthcare valuations, capital rotated toward cyclicals and resources with better near-term earnings leverage, and company-specific headwinds at CSL, ResMed, Ramsay, and Sonic coincided with the macro shift.

Market concerns that GLP-1 obesity drugs could reduce long-term sleep apnoea incidence drove a significant de-rating of ResMed, even as the company reported 11% revenue growth and 21% non-GAAP EPS gains in Q3 FY2026. ResMed management has argued the medium-term impact on its addressable market will be minimal, but the uncertainty discount remains unresolved.

Four observable catalysts frame the recovery case: RBA rate cuts that could reverse the bond-proxy headwind, genuine EPS improvement at CSL to justify its elevated trailing PE of approximately 79x, clinical data clarifying GLP-1 drug impacts on sleep apnoea outcomes, and domestic margin stabilisation at Ramsay and Sonic as wage pressures ease and elective surgery volumes normalise.

Despite a share price decline of roughly 64% from January 2025 levels to approximately A$97-98 in mid-May 2026, CSL's trailing price-to-earnings ratio remains elevated at approximately 79x, reflecting that earnings per share contracted alongside the price. This dual compression of both multiple and earnings means a recovery thesis depends on genuine EPS improvement rather than sentiment alone.