ResMed Share Price at 52% Discount: Opportunity or Value Trap?

1 hr ago

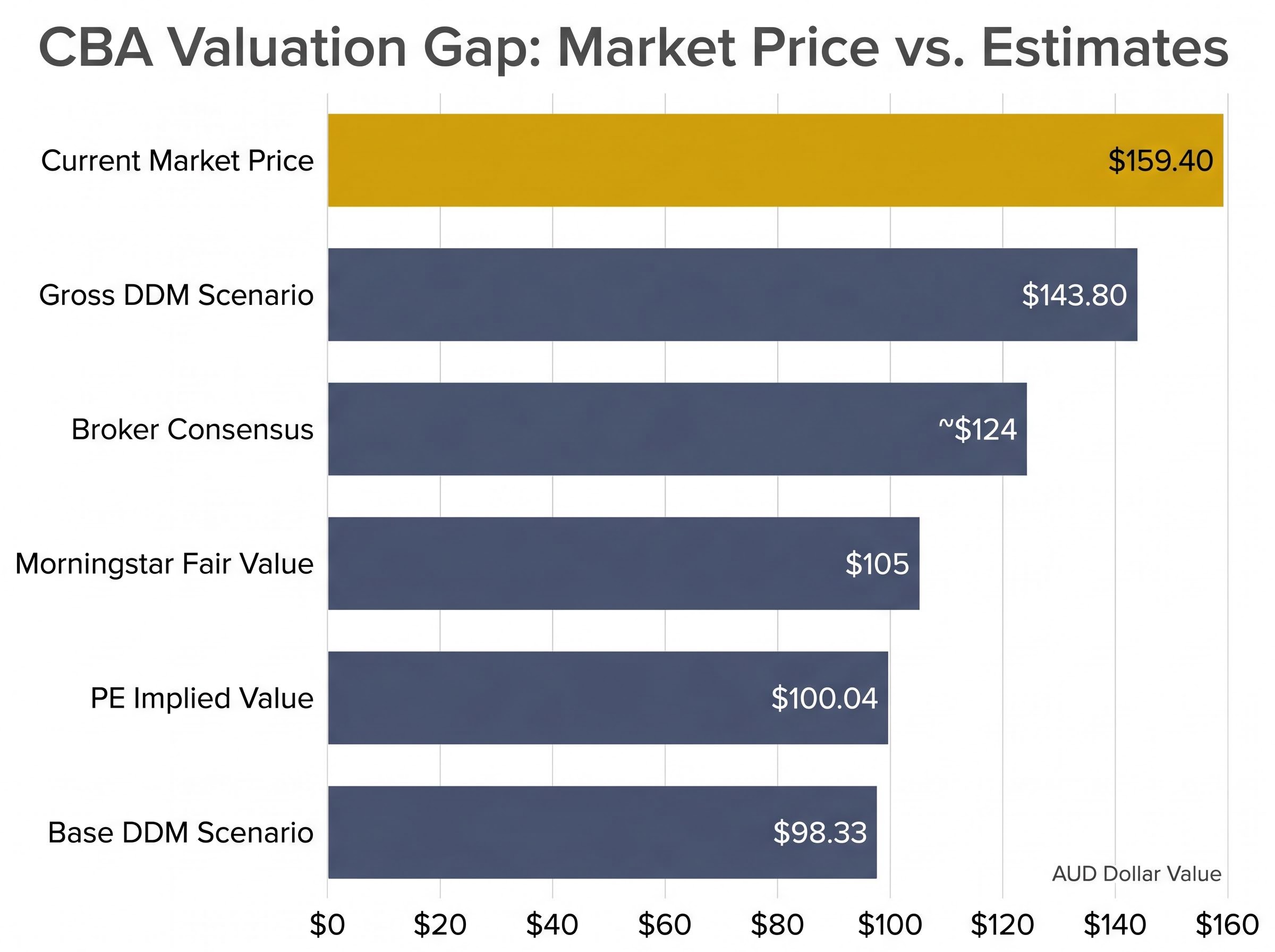

At $159.40 per share, Commonwealth Bank of Australia trades above every major analyst price target and roughly 52% above Morningstar’s latest fair value estimate of $105. For a stock that sits at the centre of millions of Australian superannuation and share portfolios, the gap between what analysts say the business is worth and what the market is charging for it is hard to dismiss as noise.

CBA is not a speculative name trading on sentiment alone. It reported $5,445 million in cash net profit for the first half of FY26, pays a fully franked dividend, and holds a CET1 ratio of 12.3%. The quality of the business is not in question. What follows is an application of two foundational equity valuation methods, the price-to-earnings (PE) ratio and the Dividend Discount Model (DDM), to CBA’s current financials. The aim is to show the inputs, the outputs, and what the distance between those outputs and $159.40 actually signals for investors weighing the stock today, 17 May 2026.

The PE valuation method takes three inputs and produces one number. For CBA, those inputs are:

| Input | Value |

|---|---|

| CBA FY24 EPS | $5.63 |

| Sector average PE | ~18x |

| Implied share price | $100.04 |

Sector-adjusted PE valuation: $100.04, an implied discount of approximately 37% to the current share price of $159.40.

The arithmetic is straightforward. At $159.40, CBA’s trailing PE sits at approximately 28.3x, more than one and a half times the sector average. Applying the sector average PE deliberately strips out CBA’s premium rather than assuming it is justified, which is the point of the exercise: to see what the earnings alone support when valued in line with comparable businesses. The $100 figure is not a price target. It is a benchmark, and the gap between it and the current share price is the territory the rest of this analysis explores.

The PE ratio measures how much investors pay for each dollar of a company’s annual earnings. A PE of 18x means the market values the stock at 18 times its most recent annual profit. The ratio is most informative when used for within-sector comparison, because businesses in the same industry face similar cost structures, regulatory pressures, and growth constraints. Comparing CBA’s PE to a technology company’s PE tells an investor very little; comparing it to ANZ, Westpac, and NAB tells them quite a lot. The peer comparison section that follows puts this tool to direct use.

The DDM values a stock based on the present value of its expected future dividend payments. The formula is:

Share value = Annual dividend / (Discount rate minus Dividend growth rate)

Three inputs drive the model:

Banks with long, consistent dividend records and stable payout ratios fit the DDM’s assumptions more naturally than growth stocks with volatile or absent dividends. CBA’s dividends are fully franked, which means Australian resident investors receive franking credits that effectively increase the pre-tax value of each payment. A gross dividend figure (cash dividend plus franking credit) can be incorporated into the model as an alternative base input.

DDM application to Australian banks is structurally more defensible than applying the same model to growth-oriented technology companies, because regulatory capital constraints and established payout histories produce the predictable dividend streams the model’s assumptions require.

Both models produce estimates, not verdicts. Qualitative factors, including franchise quality, economic conditions, and credit risk, sit outside the calculation but matter to the final investment decision. Professional analysts typically spend the majority of their research on qualitative assessment before a single number enters a spreadsheet.

The DDM produces different outputs depending on which dividend figure is used as the base input. Three scenarios illustrate the range.

| Scenario | Dividend input | Discount rate | Implied value |

|---|---|---|---|

| Base (FY cash dividend) | $4.65 | ~6.7% | $98.33 |

| Adjusted (forecast DPS) | $4.76 | ~6.7% | $100.66 |

| Gross (with franking credits) | $6.80 | ~6.7% | $143.80 |

The base scenario uses CBA’s most recent full-year cash dividend of $4.65 and a blended discount rate with a modest growth assumption, arriving at $98.33. Lifting the dividend input to an adjusted forecast of $4.76 shifts the output marginally to $100.66. The third scenario incorporates the full value of franking credits, using a gross dividend of $6.80, which produces the most generous estimate at $143.80.

The grossed-up dividend calculation uses the standard formula: cash dividend multiplied by 30, divided by 70, reflecting the 30% corporate tax already paid at the company level, which converts CBA’s $4.65 cash dividend into approximately $6.64 of pre-tax equivalent income for eligible Australian investors.

Even the most favourable DDM scenario, incorporating full franking credit value, produces an implied valuation of $143.80, which sits below CBA’s current share price of $159.40.

Across growth rate assumptions of 2-4% and discount rates of 6-11%, the DDM generates values spanning from $52.89 to $238.00. That wide spread is not a failure of the model. It reflects genuine uncertainty in the assumptions that drive it. A small change in the discount rate, even half a percentage point, can shift the implied value by tens of dollars.

The central scenarios, those using assumptions closest to market consensus, cluster well below $159.40. Reaching a DDM valuation above the current share price requires growth and discount rate assumptions that are materially more optimistic than what most analysts currently apply.

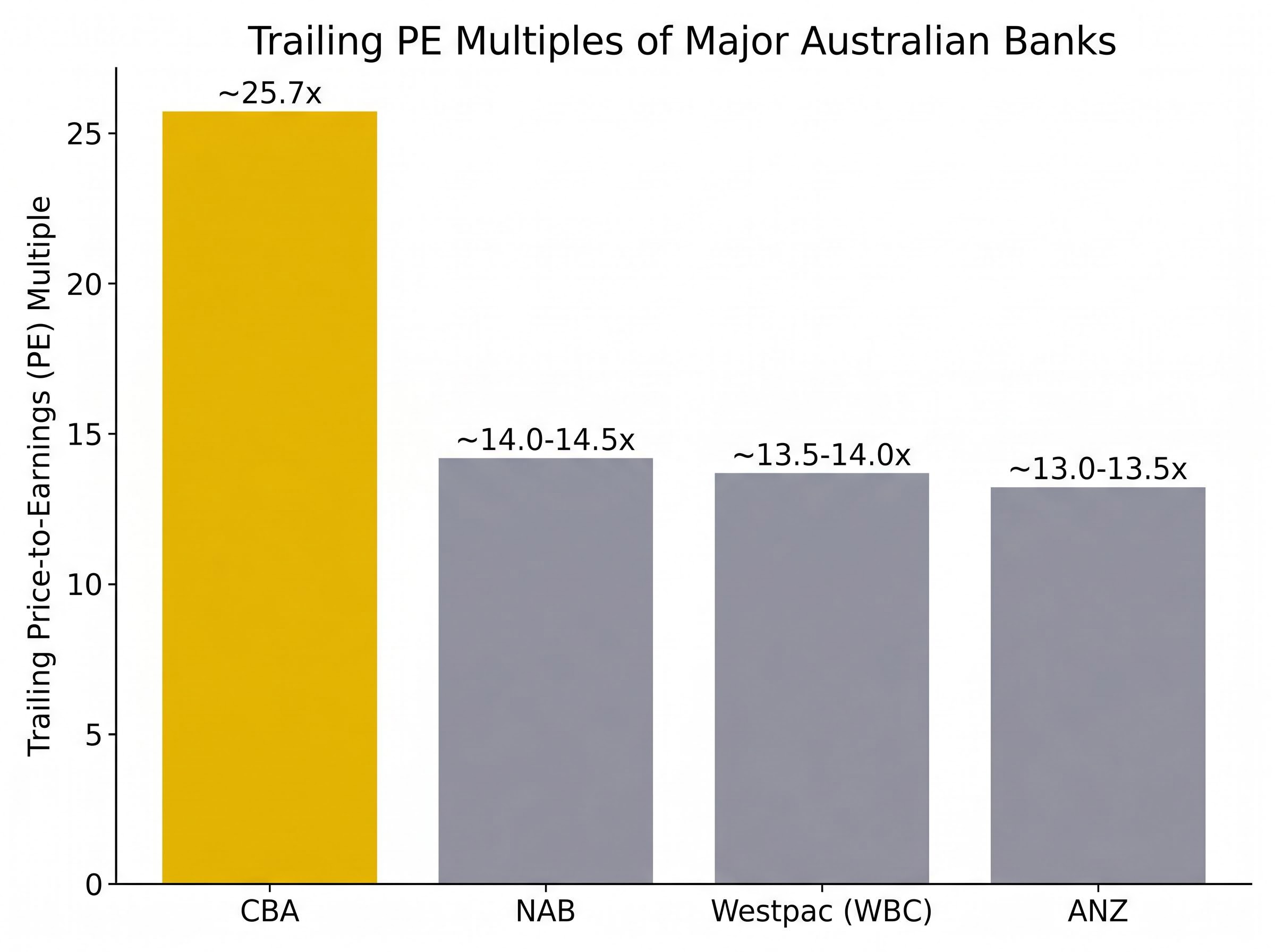

| Bank | ASX code | Trailing PE |

|---|---|---|

| Commonwealth Bank | CBA | ~25.7x |

| ANZ Group | ANZ | ~13.0-13.5x |

| Westpac | WBC | ~13.5-14.0x |

| NAB | NAB | ~14.0-14.5x |

The numbers speak before the commentary does. CBA trades at roughly 1.8-2.0x the PE multiple of its three closest peers. ANZ, Westpac, and NAB all sit in a 13-14.5x band. CBA sits at 25.7x. The market is making a choice with that gap, and it is worth understanding what that choice reflects.

The case for a structural premium rests on real competitive advantages:

The qualitative factors beyond the PE ratio, including net interest margin trajectory, regulatory fee compression, and management culture, are often the primary determinants of long-term relative returns across the major banks even when headline earnings multiples look comparable.

These factors are acknowledged by Morningstar, Morgan Stanley, UBS, and fund managers across the industry as legitimate reasons for CBA to trade above its peers.

The tension sits in the magnitude. At nearly double the sector PE, the premium prices in assumptions that go well beyond “better bank.” Morningstar analyst Nathan Zaia has described CBA as:

“Significantly overvalued versus the rest of the sector.”

Morgan Stanley and UBS, following CBA’s 1H26 results in February 2026, characterised the premium as “stretched” relative to earnings growth prospects. Fund managers on Livewire echoed the point: CBA should probably always trade at a premium to the other majors, but not at any price. The premium is justified in principle. Whether it is justified at this magnitude is the question no analyst consensus has answered affirmatively.

| Source | Fair value / Target | Rating / Assessment |

|---|---|---|

| Morningstar (May 2026) | $105 | 1-star (Rich / Sell) |

| Broker consensus (14 analysts) | ~$124 (range $90-$142) | Strong Sell / Reduce |

| CBA market price | $159.40 | Reference |

Morningstar’s fair value estimate of $105, published on 14 May 2026 by analyst Nathan Zaia, carries a 1-star rating, the lowest on the firm’s scale. Earlier in February 2026, the fair value had been set at $110 with the same “significantly overvalued” characterisation. The direction of revision has been downward.

The broker consensus target of approximately $124.42, aggregated from 14 analyst estimates, carries a Strong Sell / Reduce rating. The range spans from $90 at the low end to $142 at the high end, reflecting different views on how much overvaluation exists rather than any meaningful bullish conviction at current prices.

The implied downside is material from either reference point: approximately 22% to the broker consensus target, approximately 34% to Morningstar’s fair value.

At $159.40, CBA’s forward cash dividend yield using a forecast of $4.80-$5.00 per share is approximately 3.0-3.1%. Income alone does not compensate for the valuation risk embedded in the current price.

The ATO’s franking credit refund rules for individuals confirm that resident taxpayers can apply franking credits to reduce their overall tax liability or receive a cash refund if credits exceed the tax owed, which is the mechanism that makes the gross dividend figure a materially higher effective return for many CBA shareholders than the headline cash dividend alone suggests.

Disagreement among analysts does exist, but the range of disagreement runs from “moderately overvalued” to “significantly overvalued.” No major broker or independent valuation house has published a fair value above $142 in the current consensus.

Every analytical lens applied in this article points in the same direction. The valuation outputs range from approximately $98 to $144, and the current share price sits above all of them:

CBA’s competitive position is strong, and the arguments in favour of a structural premium are real. A CET1 ratio of 12.3%, cash net profit of $5,445 million for the first half of FY26, and a fully franked interim dividend of $2.35 per share all confirm a business operating from a position of financial strength. As Motley Fool Australia has characterised it, CBA is “a wonderful business at a not-so-wonderful price.”

The DDM is sensitive to its inputs, and a sufficiently optimistic set of growth and discount rate assumptions can produce a valuation above $159.40. That is not a flaw in the analysis; it is the investor’s decision in plain view. Justifying the current price requires assumptions that sit above the professional consensus on earnings growth, margin trajectory, and risk, and holding those assumptions carries its own risk if conditions disappoint.

Valuation models do not issue instructions. They clarify what is embedded in a price. For CBA at $159.40, the embedded assumptions are demanding. Investors considering the stock deserve to see that clearly.

For investors who want to go beyond earnings multiples and dividend models, our comprehensive walkthrough of ASX bank balance sheet metrics covers NPL ratios, CET1 capital adequacy, deposit funding composition, and price-to-book multiples across CBA, ANZ, NAB, Westpac, and Macquarie, with worked comparisons showing which metrics most reliably signal earnings resilience at each stage of the credit cycle.

This article is for informational purposes only and should not be considered financial advice. Investors should conduct their own research and consult with financial professionals before making investment decisions. Past performance does not guarantee future results. Financial projections are subject to market conditions and various risk factors.

The Dividend Discount Model (DDM) values a stock by calculating the present value of all expected future dividend payments using the formula: share value equals annual dividend divided by the discount rate minus the dividend growth rate. Applied to CBA, the DDM produces implied values ranging from $98.33 in the base scenario to $143.80 when franking credits are included, all below the current share price of $159.40.

CBA commands a structural premium due to factors including a higher sustained return on equity, the largest low-cost deposit franchise among the major banks, digital and technology leadership, a strong CET1 capital ratio of 12.3%, and a consistent fully franked dividend record. However, analysts including Morningstar and Morgan Stanley have described the current premium of roughly 1.8-2.0 times the sector PE as stretched relative to earnings growth prospects.

As of May 2026, Morningstar has set CBA's fair value at $105 with a 1-star rating indicating it is significantly overvalued, while the broker consensus across 14 analysts places the target at approximately $124, with a range of $90 to $142. No major broker or independent valuation house has published a fair value above $142 in the current consensus.

Franking credits represent corporate tax already paid by CBA at the 30% rate, and eligible Australian resident investors can apply these credits to reduce their personal tax liability or receive a cash refund. When franking credits are included in the DDM calculation, CBA's cash dividend of $4.65 converts to a gross dividend of approximately $6.64-$6.80, lifting the DDM implied valuation to $143.80, the most generous scenario in the analysis.

At $159.40, CBA's forward cash dividend yield based on a forecast of $4.80 to $5.00 per share is approximately 3.0-3.1%, which analysts note does not adequately compensate for the valuation risk embedded in the current price given the implied downside to consensus fair value estimates.