A $200,000 portfolio of the most popular ASX stocks purchased during COVID lockdowns would face an 82% higher tax bill under Australia’s proposed capital gains tax framework, despite the investor’s actual economic gain remaining unchanged. The 2026-27 Federal Budget, delivered on 12 May 2026, announced the replacement of the 50% CGT discount with CPI-based cost base indexation plus a 30% minimum tax on net capital gains, effective for CGT events on or after 1 July 2027. This is not a consultation paper or a policy thought bubble. The Treasury Laws Amendment (Tax Reform No.1) Bill 2026 is before Parliament now. What follows walks through actual portfolio-level numbers, exposes a structural flaw in how the new system treats gains versus losses, and assesses what the reform means for ordinary Australians who invest in shares for the long term.

What Australia’s CGT overhaul actually does from 1 July 2027

The reform replaces the existing 50% CGT discount for individuals, trusts, and partnerships with a two-part mechanism. The cost base of an asset held for more than 12 months is indexed upward using the Consumer Price Index, and a 30% minimum tax applies to the indexed net capital gain. The effect is that investors are taxed on their real (inflation-adjusted) gain rather than receiving a flat halving of the nominal figure.

Three structural changes define the new framework:

- Removal of the 50% CGT discount for assets held longer than 12 months

- Introduction of CPI-based cost base indexation, adjusting the purchase price for inflation before calculating the gain

- A 30% minimum tax floor on the indexed capital gain, regardless of the investor’s marginal rate

The approach echoes the indexation system that applied from 1985 until the Howard government replaced it with the flat 50% discount in September 1999. The stated policy objectives include promoting fairness and redirecting investment toward housing.

For investors who want to model the split-calculation rule in detail, including how pre-transition gains retain the 50% discount while post-transition gains fall under indexation, our dedicated guide to how the new CGT rules work from 1 July 2027 walks through the mechanics with specific examples for superannuation funds, trusts, and individual investors holding assets across the transition date.

Transitional rules and what is grandfathered

Gains accrued up to 30 June 2027 remain eligible for the existing 50% discount. The reform applies only to CGT events occurring on or after 1 July 2027, meaning the transitional boundary sits at the end of the current financial year.

Investors in new residential properties receive a special carve-out: they may choose between the 50% discount and the new indexation regime. Pre-CGT assets, those acquired before 20 September 1985 and previously excluded from the CGT system entirely, are brought into the regime under the new framework.

When big ASX news breaks, our subscribers know first

Analysing the Reform: A $200,000 Portfolio Example

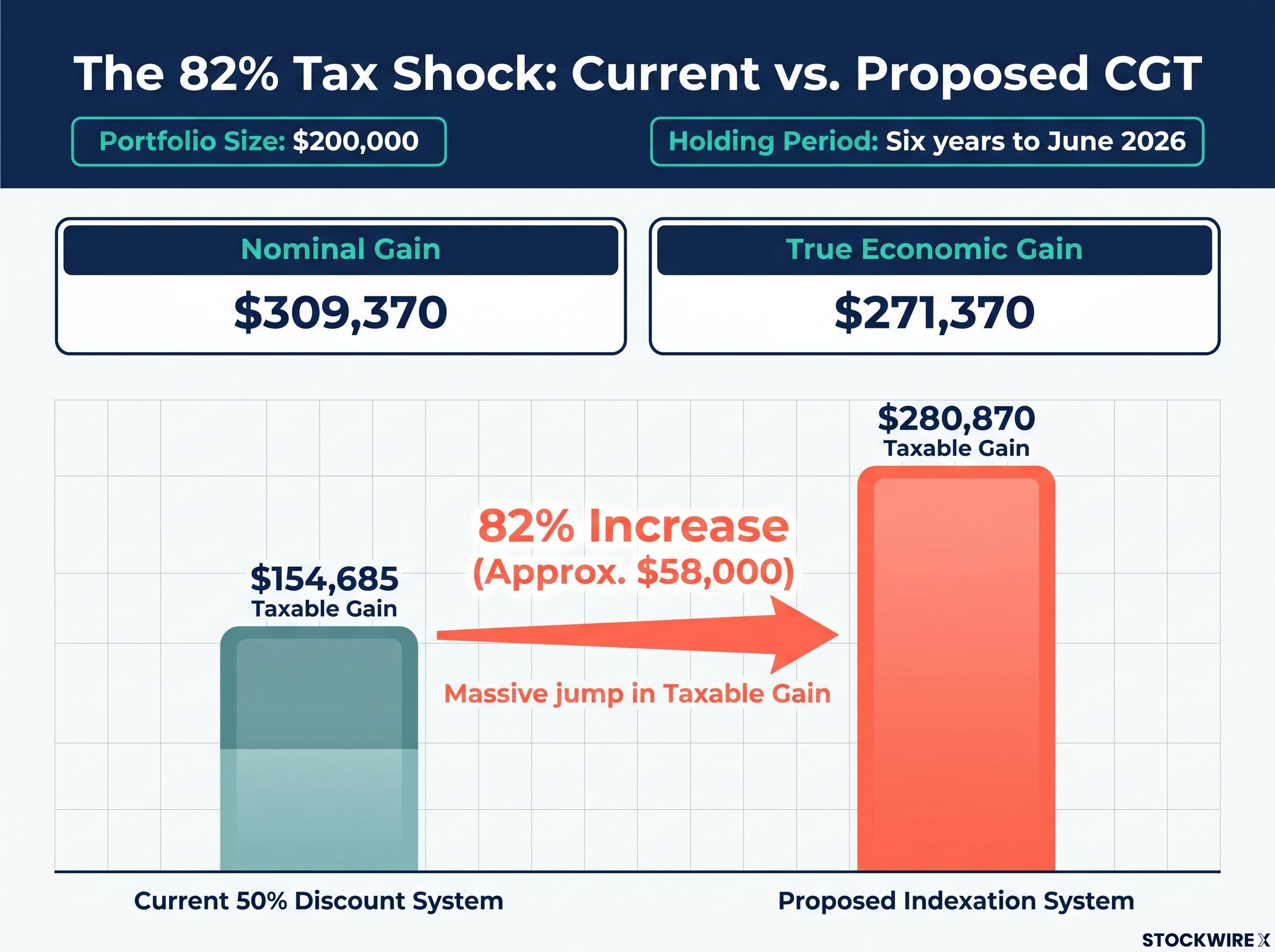

Chris Brycki, Founder and CEO of Stockspot, conducted the most detailed publicly available analysis of the reform’s impact using actual retail investor behaviour rather than a hypothetical portfolio. The methodology drew on the 20 most actively traded ASX securities among Sharesight platform users during April 2020, coinciding with one of the most significant periods of retail investing activity in recent history. Each position received a $10,000 allocation, producing a $200,000 portfolio assessed over six years to June 2026.

The portfolio was genuinely profitable. Nominal gains totalled $309,370. After adjusting for inflation, the investor’s true economic gain, the actual increase in purchasing power, was $271,370. Fifteen of 20 holdings returned above inflation. Five produced losses.

Under the current 50% discount system, the taxable gain after capital losses was $154,685. Under the proposed indexation framework, the taxable gain rose to $280,870, exceeding the investor’s total real economic gain and representing an 82% increase. The absolute increase in the tax bill was approximately $58,000.

The same portfolio, the same economic gain, and the same investor. Only the method of measuring the gain for tax purposes changed, and the tax bill rose by 82%, approximately $58,000 in absolute terms.

The five highest-impact individual holdings illustrate where the increase concentrates:

| Security | Nominal Gain | Current System | Proposed System | Increase |

|---|---|---|---|---|

| Macquarie Group | $20,682 | $10,341 | $18,782 | 82% |

| Commonwealth Bank | $24,115 | $12,058 | $22,215 | 84% |

| BHP Group | $24,682 | $12,341 | $22,782 | 85% |

| Afterpay | $18,624 | $9,312 | $16,724 | 80% |

| Vanguard International Shares ETF (VGS) | $14,262 | $7,131 | $12,362 | 73% |

The concentration of returns among a small number of strong performers is the primary driver of the increased tax burden. Under the current framework, those gains are halved. Under the proposed system, they become largely taxable in full once adjusted for inflation.

How the 50% CGT discount works and why it was introduced

The 50% CGT discount was introduced by the Howard government in September 1999 to replace the CPI indexation system that had applied since 1985. The rationale was simplicity. Rather than requiring investors to calculate an inflation-adjusted cost base for every asset, the government halved the nominal gain for assets held longer than 12 months. The discount applies to individuals, trusts, and partnerships, with the reduced gain then taxed at the taxpayer’s marginal rate.

Both the old indexation system and the discount it replaced were designed to solve the same problem: preventing the tax system from taxing inflationary gains that represent no real increase in purchasing power. Where they differ is in how they approximate that protection.

- What they share: Both attempt to ensure investors are not taxed on purely inflationary gains

- Where they differ: The 50% discount is a blunt, uniform approximation, applying the same reduction regardless of the inflation rate or the holding period. CPI indexation is a precise calculation, adjusting the cost base to reflect actual inflation over the period of ownership.

Precision, however, does not automatically mean fairness. The proposed system introduces a structural asymmetry between gains and losses that the simpler discount avoids, a problem the following section quantifies.

The structural flaw hiding inside “fairer” indexation

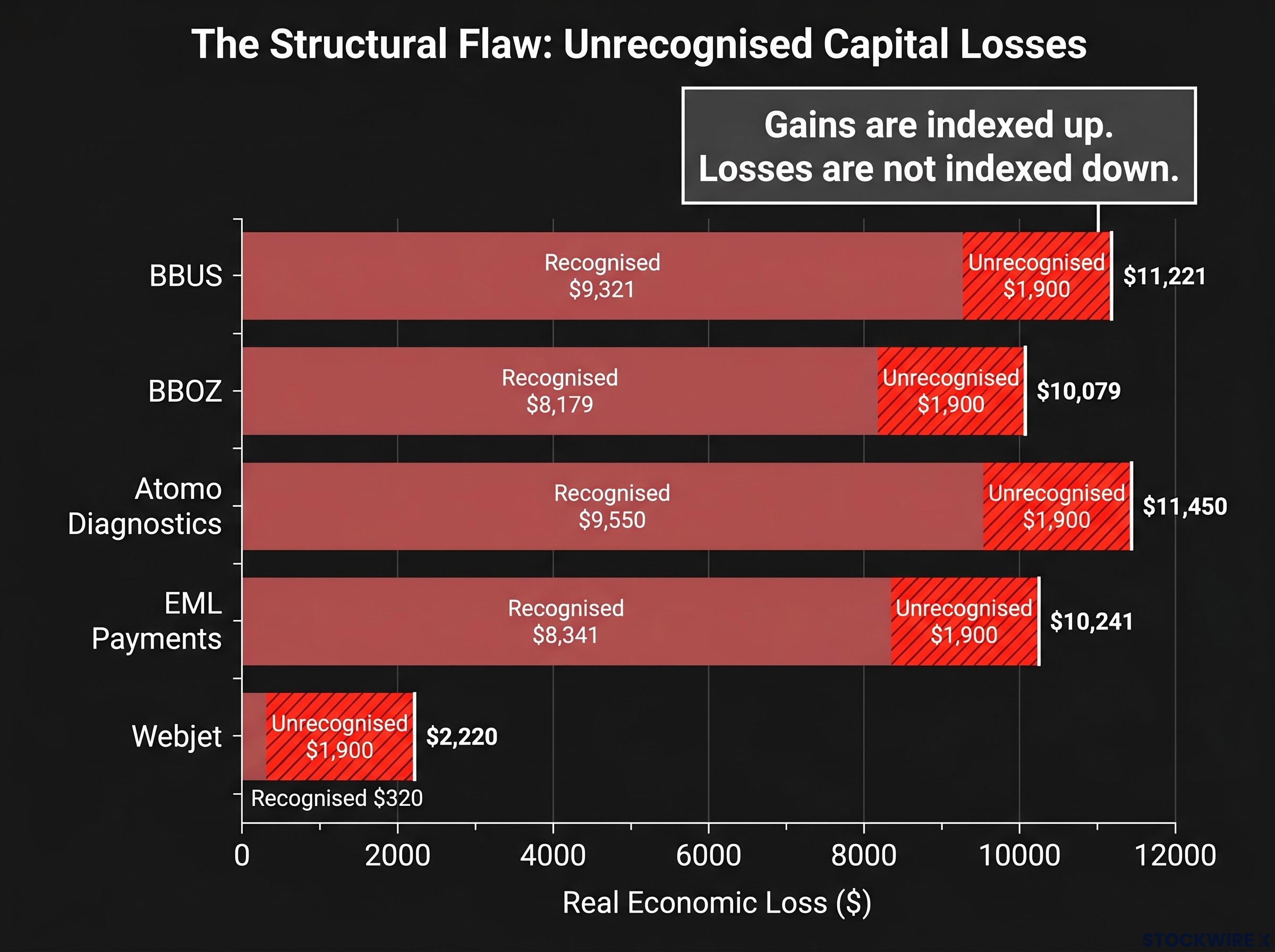

Five of the 20 holdings in the Sharesight portfolio lost money: BBUS, BBOZ, Atomo Diagnostics, EML Payments, and Webjet. Under the current system, the nominal loss is straightforward. Under the proposed framework, something less visible occurs.

| Security | Real Economic Loss | Recognised Capital Loss | Unrecognised Loss |

|---|---|---|---|

| BBUS | $11,221 | $9,321 | $1,900 |

| BBOZ | $10,079 | $8,179 | $1,900 |

| Atomo Diagnostics | $11,450 | $9,550 | $1,900 |

| EML Payments | $10,241 | $8,341 | $1,900 |

| Webjet | $2,220 | $320 | $1,900 |

Each loss-making holding generated approximately $1,900 in unrecognised real economic loss. The mechanism is straightforward: gains on winning investments are indexed upward using CPI, reducing the taxable portion to reflect only the real gain. Losses on underperforming investments, however, are recognised only at their nominal value. The investor’s real loss, which includes the erosion of purchasing power on the original capital, is partially invisible to the tax system.

Gains are indexed up. Losses are not indexed down. The system treats the two sides of the same portfolio asymmetrically.

A prior four-stock hypothetical analysis by Brycki found a 61% tax increase. The real-world Sharesight portfolio produced 82%. Different compositions, but a consistent directional result: the framework systematically increases tax burdens across portfolio types.

Diversification makes this worse, not better. A broader portfolio naturally produces a wider spread between outperformers and underperformers, amplifying both the overtaxation of gains and the under-recognition of losses simultaneously.

Who is most exposed to the asymmetry problem

Holders of small-cap equities, mining explorers, biotech stocks, thematic ETFs, and early-stage ventures face the greatest structural disadvantage. These asset classes exhibit the widest return dispersion, meaning the gap between winners and losers is larger and the asymmetry bites harder.

For biotech, technology, and early-stage resources stocks, the structural derating of growth equities is a direct consequence of the reform: these sectors derive their investment case primarily from capital appreciation rather than dividend income, and when the after-tax value of that appreciation is reduced by removing the 50% discount, the embedded CGT premium that long-term investors historically placed on high-growth ASX names compresses.

Broad market index ETFs such as VAS and VGS face less distortion. Their diversified structure behaves more like a single compounding investment, smoothing out the gap between individual winners and losers within the fund.

Treasury’s public modelling appears better calibrated to this broad-index behaviour, which may understate the impact on the millions of Australians who hold portfolios of direct equities rather than passive index funds.

What this means for Australia’s long-term investing culture

For three decades, Australian tax policy broadly rewarded patience, risk-taking, and long-term share ownership. The 50% CGT discount, superannuation concessions, and dividend imputation collectively built a culture of retail share investment that remains unusual by international standards. The proposed framework raises a question about whether that direction is being reversed.

The reform was motivated primarily by housing affordability and investment property dynamics. Negative gearing restrictions for existing residential properties were announced alongside the CGT changes. The policy logic connecting property investment behaviour to the CGT discount is coherent. The difficulty is that the same framework applies in identical form to direct equity investors, who are a structurally different group.

Three distinct investor categories face unintended consequences:

- Direct equity investors holding diversified portfolios of individual ASX shares, who face the widest return dispersion and therefore the greatest asymmetry exposure

- SMSF trustees holding concentrated positions, where a small number of large gains can produce an outsized increase in the fund’s tax liability

- Early-stage and higher-risk investors in biotechnology, mining exploration, and venture capital, where loss rates are higher and the non-recognition of real economic losses is most pronounced

As Brycki noted in commentary published in The Australian and on Livewire, the practical effect of the changes may create larger market distortions than those the reforms are designed to correct. An 82% effective increase in taxable gains is a meaningful disincentive for the next generation of Australians considering whether to invest in shares at all.

The reform is law-in-waiting, not a distant proposal. Here is what investors should do now.

The Treasury Laws Amendment (Tax Reform No.1) Bill 2026 is before Parliament as at June 2026. The commencement date is 1 July 2027, giving investors approximately 13 months to assess their positions under the transitional rules.

Investors positioning ahead of the 1 July 2027 commencement date also face the challenge of distinguishing tax policy signal from market noise: the same month Australia’s CGT announcement was made, a single social media post from a South Korean presidential advisor wiped over $300 billion in market capitalisation from chip stocks on a proposal that never reached legislative form, illustrating why the legislative stage of a tax announcement matters as much as its stated rate.

The Treasury Laws Amendment (Tax Reform No.1) Bill 2026 is before Parliament as at June 2026, with the commencement date set at 1 July 2027, giving investors approximately 13 months to assess their positions under the transitional rules.

Key dates: Gains accrued to 30 June 2027 remain eligible for the existing 50% CGT discount. The new framework applies to CGT events on or after 1 July 2027.

The transitional rules create a specific decision point. Any CGT event completed before 1 July 2027 is assessed under the existing framework. Investors holding assets with large unrealised gains face a meaningful timing question that warrants careful analysis rather than a reflexive decision.

Three sequential steps are worth considering:

- Identify holdings with unrealised gains acquired before 1 July 2027, particularly those with the largest nominal gains relative to cost base

- Model the tax outcome under both frameworks using available calculators (the Stockspot CGT calculator at stockspot.com.au/cgt-calculator provides a starting reference) or through a qualified adviser

- Make an informed decision about the timing of any disposals before the transitional boundary, factoring in both tax outcomes and the investment rationale for continuing to hold

Investors with diversified direct equity portfolios, SMSF positions, or early-stage holdings should seek professional CGT modelling before the commencement date.

This article is for informational purposes only and should not be considered financial advice. Investors should conduct their own research and consult with financial professionals before making investment decisions. Financial projections and tax calculations are subject to legislative outcomes and individual circumstances.

An 82% tax increase does not look like fairness to ordinary investors

The proposed CGT framework raises the tax bill on a representative real-world retail portfolio by 82%, producing taxable gains of $280,870 on an economic profit of $271,370. The investor is taxed on more than they actually gained in real terms. That result contradicts the reform’s stated fairness objective.

The principle behind the change is legitimate. Taxing only real gains rather than inflationary ones is sound policy. The execution, however, introduces a system that indexes gains upward for winners while leaving losses unrecognised at their nominal value, creating a structural asymmetry that penalises the very diversification and long-term risk-taking that Australian policy has spent three decades encouraging.

The question the data raises is whether a framework that systematically over-taxes diversified retail investors, particularly those who hold higher-risk and higher-dispersion assets, is compatible with Australia’s stated interest in encouraging long-term share ownership and capital formation. The numbers suggest it is not.

—