How the US Government Became Intel’s Investor and Deal Broker

50 mins ago

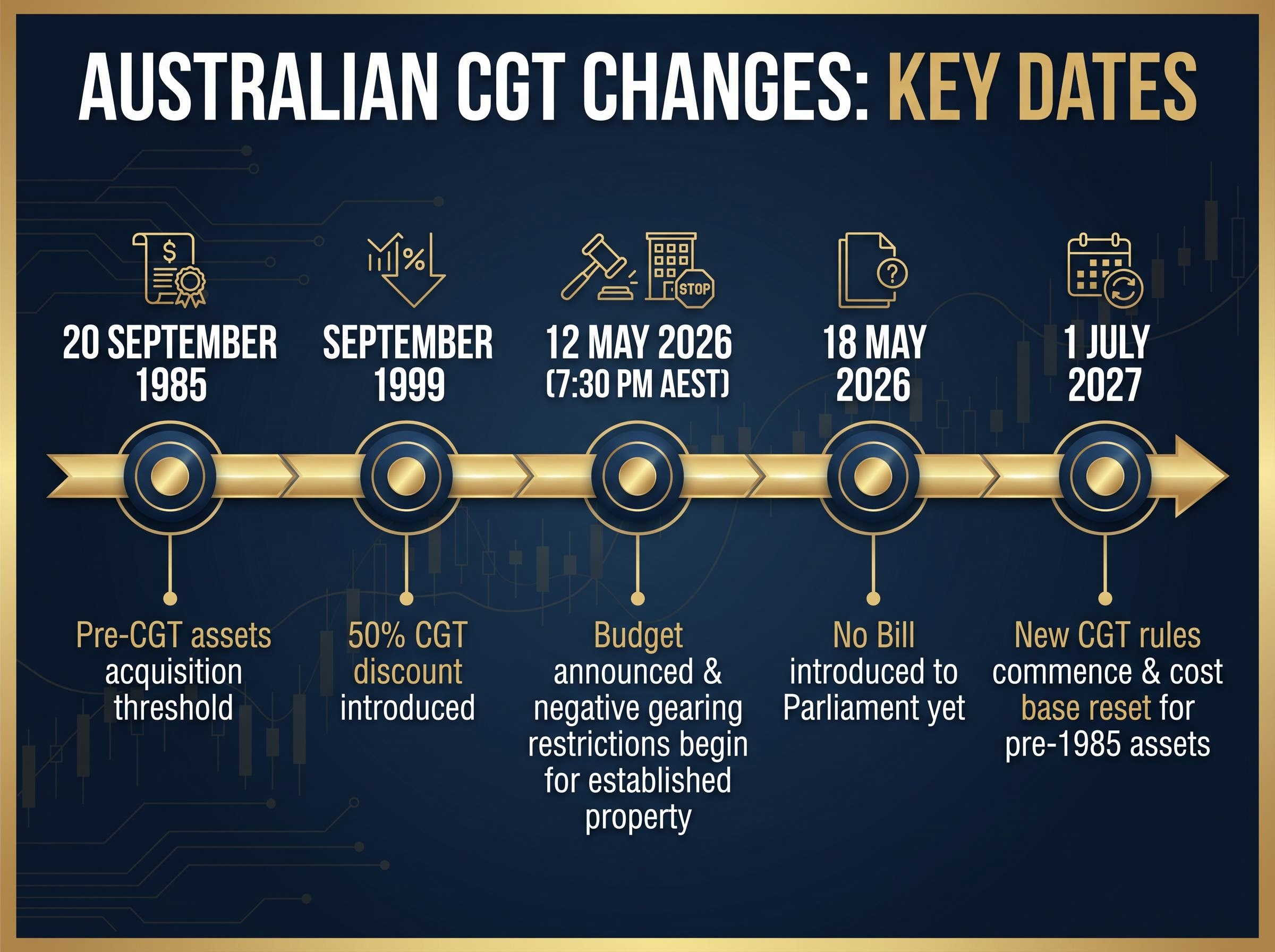

From 1 July 2027, the 50% capital gains tax discount that has shaped Australian investment strategy since 1999 will be abolished. In its place, a cost base indexation model with a 30% minimum tax floor will determine how capital gains are taxed. For ASX investors, this is not a marginal adjustment to the tax code; it is a repricing of which strategies, sectors, and holding behaviours actually deliver after-tax returns.

The 2026-27 Federal Budget, delivered on 12 May 2026, introduced the most substantial restructuring of Australian investment taxation in decades. The CGT changes in Australia sit alongside negative gearing restrictions on established residential property, creating a combined policy shift that reshapes the relative attractiveness of property and equities simultaneously. The measures are official government policy but not yet law. With the 1 July 2027 commencement date just over 13 months away, investors who act on the structural implications early are likely to be better positioned than those who wait for legislation to pass.

What follows maps the specific ways the new CGT framework is expected to redistribute capital across the ASX, identifying which sectors and strategies carry structural tailwinds, which face headwinds, and what the property-to-equities reallocation means for overall market demand.

Three changes were announced as a single package, and they operate as an interlocking system rather than three independent adjustments.

The first is the abolition of the 50% CGT discount for individuals and trusts on assets held longer than 12 months. This discount has been in operation since September 1999, approximately 27 years. The second is the introduction of cost base indexation as the replacement mechanism. Rather than halving the nominal gain, the new model adjusts the cost base upward by inflation before calculating the taxable amount. Indexation offsets the inflation component of a gain; it does not replicate the scale of tax reduction the discount provided, particularly for high-growth assets where nominal gains far exceed inflation.

The third measure is the 30% minimum effective tax rate on capital gains. This floor removes the benefit that lower-income investors previously received when the discount reduced their effective CGT rate below 30%.

The 30% minimum floor: Under the new rules, no Australian taxpayer will pay an effective tax rate on capital gains below 30%, regardless of their marginal income tax bracket. This represents a material change for investors on lower marginal rates who previously benefited most from the discount.

The combined effect is larger than any single measure in isolation. Indexation partially compensates for inflation but does not halve gains. The floor ensures even the most favourably positioned taxpayers face a meaningful rate. Together, they compress the after-tax return available from capital appreciation across every asset class.

| Asset Scenario | Current Treatment | New Treatment (Post-2027) | Effective Tax Rate Change |

|---|---|---|---|

| Short-term gain (under 12 months) | Taxed at full marginal rate | Taxed at marginal rate, minimum **30%** | Neutral to higher for low-income earners |

| Long-term moderate gain (held 5 years, gain matches inflation) | 50% discount applied; effective rate halved | Indexation offsets most of the gain; **30%** floor applies | Broadly similar for inflation-matching gains |

| Long-term high-growth gain (held 5 years, gain well above inflation) | 50% discount applied; effective rate halved | Indexation offsets inflation only; full marginal rate on real gain, minimum **30%** | Materially higher |

As of 18 May 2026, no exposure draft legislation or Bill has been introduced into Parliament. The measures remain announced policy, not enacted law.

Under the existing regime, the 50% discount created a direct financial incentive to hold assets beyond 12 months. That single threshold converted long-duration holding from a purely investment-based decision into a tax-efficient default strategy. An investor sitting on a large unrealised gain had a quantifiable reason to defer realisation: every dollar of gain held past the 12-month mark was taxed at half the nominal rate.

Without the discount, that structural incentive disappears. Indexation adjusts for inflation over time, but it does not create the step-change tax advantage that the 12-month threshold provided. An investor holding a growth stock with substantial unrealised gains no longer faces a material tax penalty for realising those gains earlier.

The expected behavioural consequence is increased portfolio turnover and shorter average holding periods, particularly in segments where unrealised gains accumulate fastest.

Growth stocks generate most of their return through capital appreciation rather than income. The CGT discount was disproportionately valuable for this category because the larger the nominal gain, the larger the absolute tax saving from halving it.

With the discount removed, the after-tax case for holding high-multiple growth stocks over long horizons weakens relative to income-generating alternatives. This does not make growth investing unviable, but it does erode the tax-based margin that made buy-and-hold the default approach for many Australian investors in this segment.

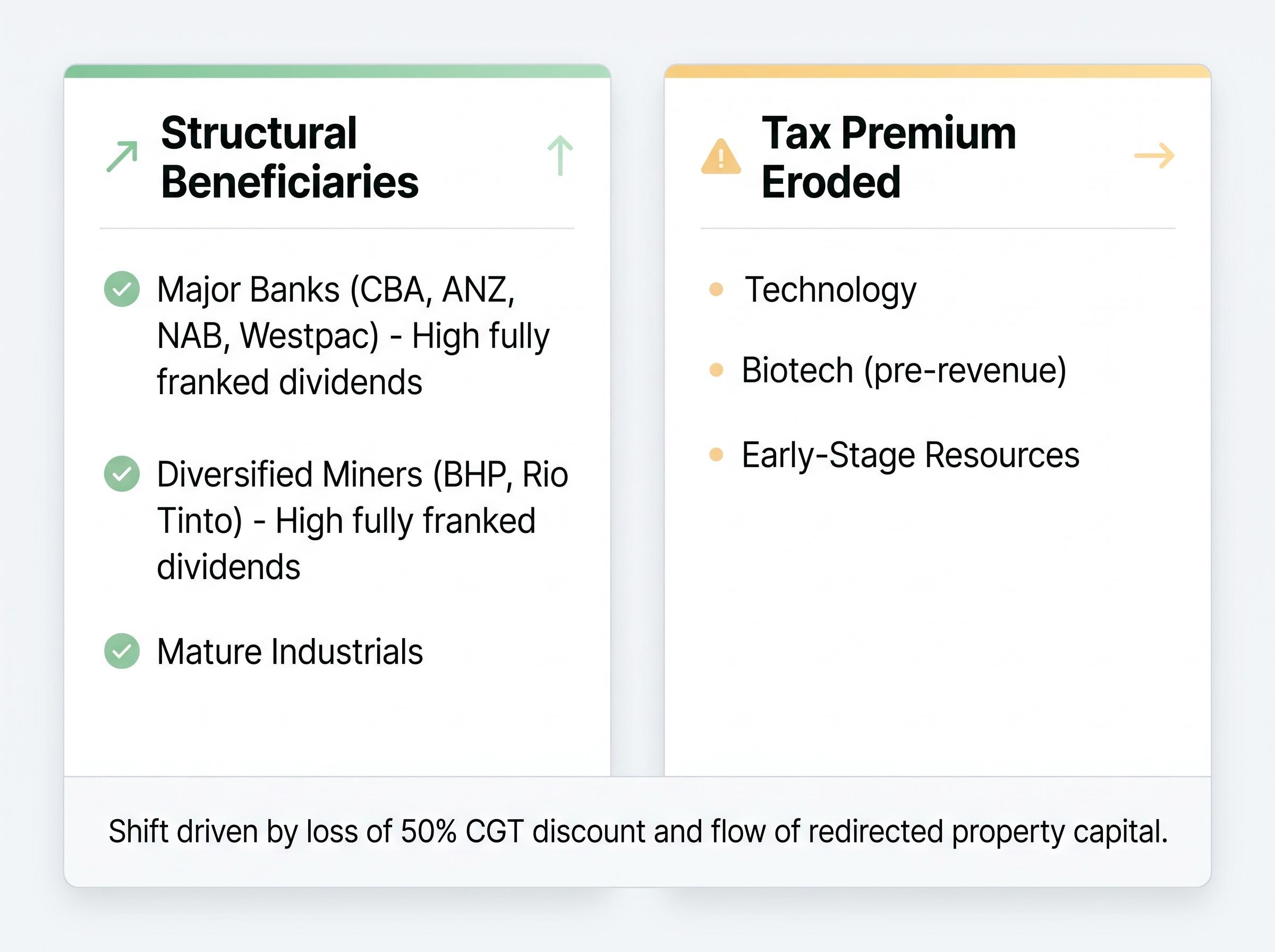

If capital gains lose their tax advantage, the question becomes: what gains it? The answer, within the Australian system, points directly to franked dividends.

Franking credits, unique to the Australian imputation system, eliminate the double taxation of company profits. When a company pays tax on its earnings and then distributes those earnings as dividends, the franking credit passes the tax already paid through to the shareholder. For Australian resident investors, the after-tax yield on a fully franked dividend is materially higher than on an equivalent unfranked payment.

Under the old regime, the 50% CGT discount meant capital growth could compete with, and in many cases exceed, franked dividend income on an after-tax basis. That arithmetic shifts from 1 July 2027. With capital gains taxed at higher effective rates, franked income becomes relatively more attractive without any change to the franking system itself.

The specific ASX sectors positioned to benefit are the established fully franked dividend payers: the major banks (CBA, ANZ, NAB, Westpac) and the diversified miners (BHP, Rio Tinto). These names offer consistent franked yield backed by mature earnings.

Structural, not cyclical: The relative advantage of franked income over capital growth under the new rules is embedded in the tax framework itself. It does not depend on market conditions, commodity prices, or interest rate settings. It persists as long as the policy persists.

The characteristics that position a stock well under the new regime include:

The CGT changes do not operate in isolation. Alongside the discount removal, negative gearing restrictions on established residential property purchased after 7:30 pm AEST on 12 May 2026 reduce the tax-subsidised return available from leveraged property investment. New builds remain eligible for negative gearing regardless of purchase date, preserving an incentive for supply-side construction investment, but the established property market faces a structural headwind.

| Factor | Pre-May 2026 Purchase | Post-May 2026 Purchase |

|---|---|---|

| Negative gearing eligibility | Fully available (grandfathered) | Restricted for established property |

| CGT treatment (post-2027) | Indexation and **30%** floor apply to future gains | Indexation and **30%** floor apply to future gains |

| Relative investment attractiveness | Protected by grandfathering | Diminished: higher tax, restricted deductions |

A pre-July 2027 sell-down window is anticipated, as investors with established property holdings may choose to realise gains under the existing CGT rules before the deadline. This is a transitional event. The longer-term shift is a reduction in investor participation in the established residential property market.

Capital displaced from property does not simply vanish. It seeks a destination. The equity market is the most likely recipient, but the nature of the inflow matters. Investors who previously held leveraged property for yield and capital growth are expected to apply similar criteria to equities: they will favour clear dividend yield, earnings quality, and capital preservation over speculative growth.

This dynamic reinforces the structural advantage identified for banks and diversified miners. Large-cap, dividend-paying industrials and financials match the yield-and-quality profile that incoming property investors are most likely to apply. Small-cap or speculative growth names are less likely to attract this capital.

The window for action is defined and finite. Three specific considerations emerge from the policy mechanics.

Assets acquired before 20 September 1985 (pre-CGT assets) require particular attention. Under transitional rules, these assets receive a deemed cost base reset to market value at 1 July 2027. Gains accruing before that date remain exempt from CGT. Gains accruing after 1 July 2027 become taxable under the new indexation and 30% floor regime. The market value established at the transition date determines the starting point for all future taxable gains.

Pre-CGT transitional rule: For assets acquired before 20 September 1985, only gains accruing after 1 July 2027 will be taxable. A formal valuation at or near the transition date is the documented mechanism to establish the cost base and shelter historical appreciation from the new regime.

The sequenced pre-2027 actions for consideration are:

This article is for informational purposes only and should not be considered financial advice. Investors should conduct their own research and consult with qualified tax professionals before making investment decisions. The analytical framework presented does not constitute personal financial or tax advice. These measures are announced government policy and not yet law; the legislative path and final form of the rules may differ from the announced framework.

The individual threads of this analysis converge on a single picture. Growth sectors that rely on capital appreciation for the majority of their shareholder return, including technology, biotech, and early-stage resources, face a structural derating of the tax premium embedded in their valuations. The CGT discount made holding these names tax-efficient at a system level. Without it, the after-tax return model shifts.

Yield sectors carry the tailwind. Banks, diversified miners, and mature industrials offering fully franked dividends benefit from two reinforcing dynamics: the domestic CGT shift makes their income relatively more attractive, and redirected property capital is expected to flow toward exactly the quality and yield characteristics these sectors offer.

| ASX Sector | CGT Discount Impact | Franked Dividend Profile | Post-2027 Structural Outlook |

|---|---|---|---|

| Major Banks | Moderate (income-driven returns) | High, fully franked | Structural beneficiary |

| Diversified Miners | Moderate | High, fully franked | Structural beneficiary |

| Technology | High (growth-driven returns) | Low to nil | Tax premium eroded |

| Biotech | High | Nil (pre-revenue) | Tax premium eroded |

| Early-Stage Resources | High | Nil to low | Tax premium eroded |

| Mature Industrials | Low to moderate | Moderate to high, often franked | Structural beneficiary |

The measures were announced on 12 May 2026 with a proposed commencement of 1 July 2027. As of 18 May 2026, no Bill has been introduced. Investors monitoring the legislative path have a further data point on timing certainty.

The original 50% CGT discount was introduced in September 1999, nearly 27 years ago. Its removal represents one of the most significant changes to ASX sector dynamics from a tax policy perspective since the discount itself reshaped investment behaviour. Investors who position portfolios to reflect the post-2027 regime before it is priced in by the broader market may capture a structural advantage. Those who wait for consensus to shift may find valuations have already adjusted.

Past performance does not guarantee future results. These statements are based on announced policy that is not yet law and are subject to change based on the legislative process and broader market developments.

The 2026-27 Federal Budget, delivered on 12 May 2026, announced the abolition of the 50% capital gains tax discount for individuals and trusts, replacing it with cost base indexation and a 30% minimum effective tax rate on capital gains, with the changes commencing 1 July 2027.

Under the new rules, no Australian taxpayer will pay an effective tax rate on capital gains below 30%, regardless of their marginal income tax bracket, which particularly affects lower-income investors who previously paid less than 30% due to the 50% discount.

Major banks (CBA, ANZ, NAB, Westpac) and diversified miners (BHP, Rio Tinto) are positioned as structural beneficiaries because their high fully franked dividend yields become relatively more attractive once capital gains lose their 50% discount tax advantage.

Investors should consider obtaining formal valuations on long-held and pre-CGT assets to establish a documented cost base, model after-tax return scenarios for positions with large unrealised gains, and review portfolio allocation toward franked dividend payers ahead of the commencement date.

Negative gearing on established residential property purchased after 7:30 pm AEST on 12 May 2026 is restricted, and combined with the removal of the CGT discount from 1 July 2027, the policy package significantly reduces the after-tax return available from leveraged established property investment.