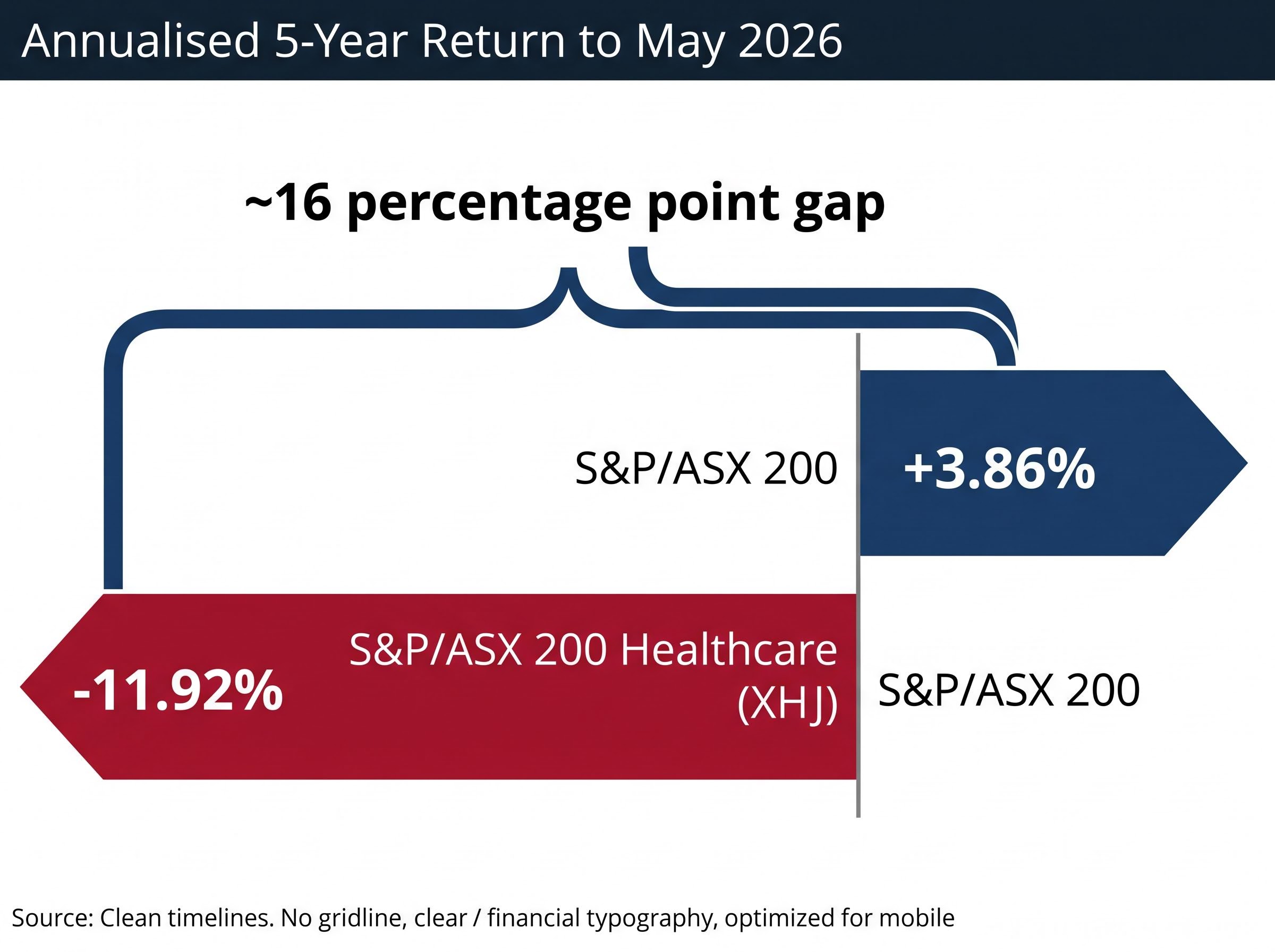

The S&P/ASX 200 Healthcare Index delivered an annualised return of -11.92% over the five years to May 2026. Over the same window, the broader ASX 200 returned 3.86% per annum. That gap, roughly 16 percentage points of annualised underperformance, makes healthcare the worst-performing major sector on the Australian market across what should have been a period of structural growth in global health spending, demographic tailwinds from ageing populations, and rising investor appetite for socially aligned assets.

The disconnect between the ASX healthcare sector’s long-run fundamentals and its medium-term market performance raises a question relevant to every Australian with a superannuation account or direct share portfolio: is this a buying opportunity, or evidence of something permanently broken? What follows works through why sectors with strong structural stories can still deliver painful returns, what specific forces drove the five-year slump, and what the global data suggest about the conditions under which a recovery becomes plausible.

A 16-percentage-point gap: how ASX healthcare fell so far behind the broader market

Healthcare is supposed to be the defensive allocation. During the Global Financial Crisis, it was the top-performing sector on the ASX, according to the Rask Invest Research Team. Demand for medical services does not disappear in a downturn. Earnings are underpinned by ageing demographics and government funding. The sector’s reputation as a safe harbour is not accidental.

The five-year numbers tell a different story.

| Index | Annualised 5-Year Return (to May 2026) | Performance Gap |

|---|---|---|

| S&P/ASX 200 Healthcare (XHJ) | -11.92% | ~16 percentage points per annum |

| S&P/ASX 200 | +3.86% |

Tens of millions of Australians hold superannuation funds with exposure to XHJ-weighted healthcare names. For those investors, this is not an abstract index statistic; it represents real capital destruction in a sector they were told would protect them. The underperformance was not driven by a single event. It was the product of multiple converging forces, each of which deserves separate examination.

When big ASX news breaks, our subscribers know first

What defensive actually means (and why it did not protect investors this cycle)

The word “defensive” describes the stability of a company’s earnings, not the stability of its share price. Healthcare companies with long, predictable revenue streams, the kind generated by CSL, Cochlear, and ResMed, are priced by the market in a way that resembles long-duration bonds. When investors can see reliable cash flows stretching years into the future, they assign a high present value to those flows, pushing price-to-earnings multiples upward.

That mechanism works in reverse when interest rates rise. Higher real yields reduce the present value of distant cash flows, compressing the multiples investors are willing to pay regardless of whether the underlying business continues to perform. From 2022 onward, central banks globally lifted interest rates at the fastest pace in a generation. The result was a systematic de-rating of long-duration growth assets, and ASX healthcare names were squarely in that category.

The discount-rate channel operates independently of whether a company’s underlying business is performing well; when long-term real yields rise, the present value of future cash flows falls mechanically, shrinking price-to-earnings multiples across any sector whose earnings are weighted toward the distant future.

Cochlear’s price-to-sales ratio stood at 2.85x in May 2026, compared with a five-year historical average of 9.18x, a compression of more than two-thirds from its longer-term norm (Rask Invest Research Team, May 2026).

This dynamic was not unique to Australia. Global healthcare equities experienced similar valuation pressure, reinforcing that the underperformance was macro-driven rather than a failure of any individual company’s business model. The distinction matters: a sector repriced by rising rates faces a different forward outlook than a sector repriced by deteriorating fundamentals.

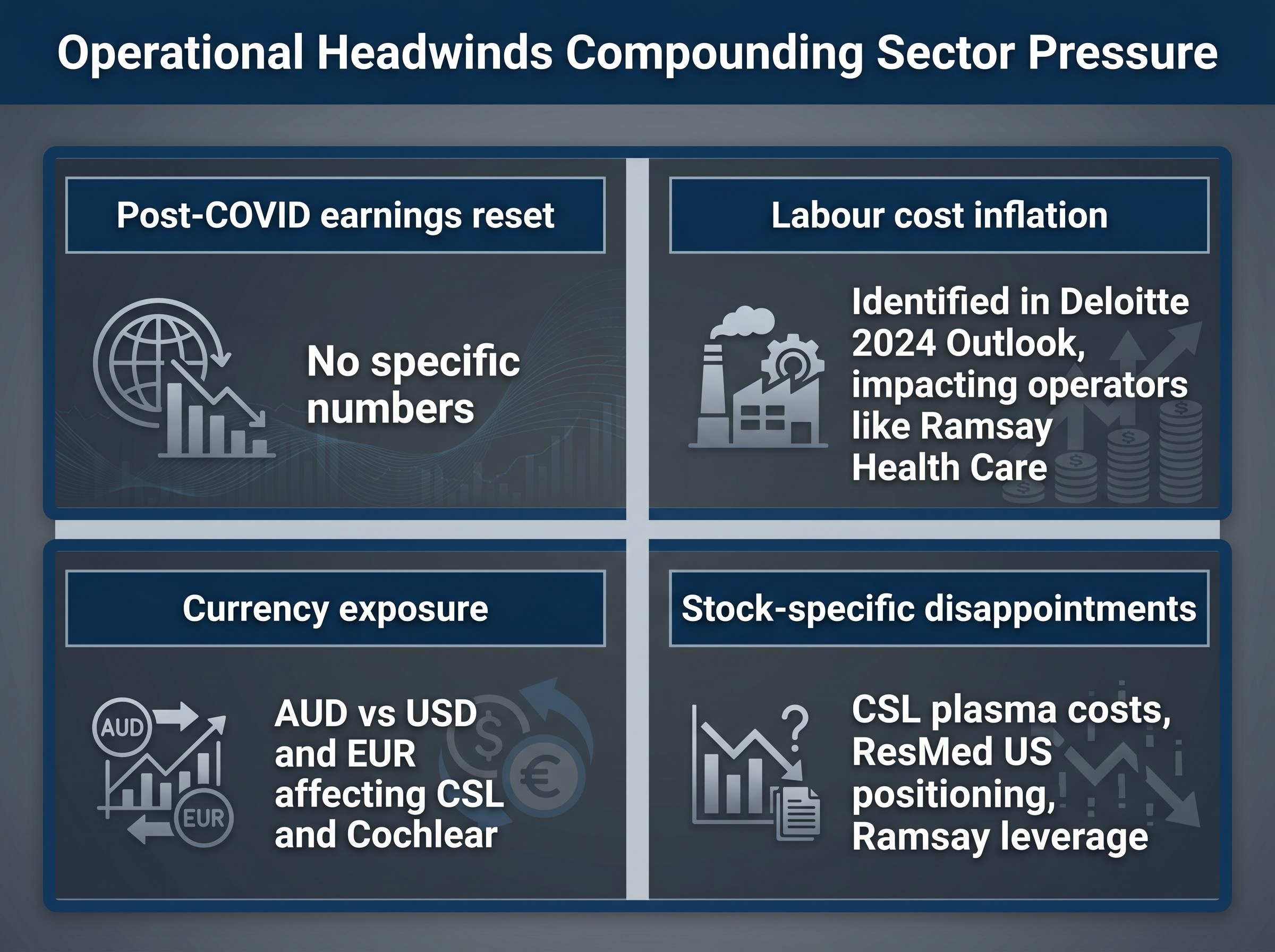

The other pressures: labour, regulation, and the post-COVID earnings reset

Rate-driven valuation compression was the dominant force, but it was not the only one. Four operational headwinds compounded the damage:

- Post-COVID earnings reset: Pandemic-era demand distortions created elevated earnings bases that subsequent years could not replicate, producing forecast misses and downward revisions across device makers, diagnostic operators, and hospital providers.

- Labour cost inflation: Staffing shortages and rising wages pressured margins for hospital and aged-care operators. Deloitte’s 2024 Global Health Care Sector Outlook identified widespread labour shortages and rising operational costs as a global post-pandemic theme, directly relevant to Australian operators such as Ramsay Health Care.

- Currency exposure: For globally oriented companies like CSL and Cochlear, movements in the AUD against the USD and EUR affected reported earnings and sentiment, adding volatility to an already difficult period.

- Stock-specific disappointments: Periodic concerns around CSL’s plasma collection costs, ResMed’s competitive positioning in the US market, and Ramsay’s leverage profile weighed on broader sector sentiment (Rask Invest Research Team, May 2026).

Elective demand sensitivity, demonstrated most sharply by Cochlear’s April 2026 guidance reset that cut FY26 profit forecasts by 30-35% and triggered a single-session share price fall of approximately 35-39%, reveals that high-multiple globally exposed names respond to consumer confidence cycles in ways that pure earnings defensiveness frameworks do not capture.

Deloitte’s 2025 Global Health Care Outlook cited efficiency, productivity, and patient engagement as ongoing priorities for healthcare executives, a signal that the sector was still working through operational normalisation rather than having completed it.

Several of these headwinds, particularly the post-COVID earnings reset and the acute phase of labour cost inflation, are time-limited rather than permanent structural impairments. Whether they are still a forward risk or a fading drag is the question that separates the diagnosis from the prognosis.

The structural tailwinds that never went away

While ASX healthcare delivered its worst five-year stretch on record, global healthcare spending accelerated.

According to the IQVIA Institute’s Global Medicine Use Trends 2026 report, global medicine spending is projected to exceed US$2.6 trillion by 2030, growing at 5-8% per year from 2024 to 2030, driven by innovative therapies in oncology, immunology, diabetes, and obesity.

That figure covers medicine spending rather than total health expenditure, but it serves as a widely cited proxy for the structural growth trajectory of the broader sector. US healthcare expenditure alone is estimated to grow at approximately 7% annually from 2022 to 2027, with total spending projected to reach US$819 billion by 2027, according to industry estimates cited by the Rask Invest Research Team.

The AIHW health expenditure data for 2023-24 confirms that domestic spending growth has continued on its long-run upward trajectory, with government and non-government funding both contributing to total health outlays, reinforcing that the structural demand underpinning ASX healthcare names has not retreated even as their share prices have.

Layered on top of this base spending growth is a technology acceleration that represents a distinct investment opportunity.

| Sub-segment | Forecast Period | Projected CAGR | Source |

|---|---|---|---|

| Global medicine spending | 2024-2030 | 5-8% | IQVIA Institute |

| Global healthcare IT | 2025-2030 | ~14.9% | MarketsandMarkets |

| Healthcare cloud computing | 2026-2031 | ~17.7% | MarketsandMarkets |

According to MarketsandMarkets, the global healthcare IT market is projected to grow from approximately US$480 billion in 2025 to approximately US$961 billion by 2030. The healthcare cloud computing sub-segment is forecast at an approximately 17.7% compound annual growth rate from 2026 to 2031.

The healthcare IT and SaaS sub-segment, projected to grow at more than 15% annually through 2030, represents a structurally distinct entry point within the broader sector, one where the growth multiple may be more defensible than in traditional hospital and pathology operators that carry higher labour cost exposure and thinner margin structures.

The demographic driver underneath all of these figures, ageing populations in Australia and across developed economies, is independent of economic cycles. It compounds year after year regardless of where interest rates sit. When the cyclical headwinds that drove five years of underperformance begin to fade, the sector they return investors to is growing faster, not slower, than it was at the cycle’s peak.

Social impact and capital flows: the ESG dimension

Healthcare companies providing essential public health services tend to score well on the social dimension of environmental, social, and governance (ESG) frameworks, the “S” that measures a company’s impact on communities and patient outcomes. That alignment positions the sector to attract a growing pool of impact-oriented capital.

According to a 2024 Morgan Stanley survey cited by the Rask Invest Research Team, more than 50% of investors indicated plans to increase their allocation to sustainable investments.

Sector-level ESG flow statistics for Australian healthcare equities are not separately reported in publicly available sources, and this data gap means the directional signal from global surveys cannot be precisely measured at the ASX level. Global trends are relevant but not directly quantifiable for XHJ-exposed names.

Deloitte’s 2025 Global Health Care Outlook reinforced the sector’s alignment with forward-looking investment themes, highlighting technology, artificial intelligence, and patient engagement as priorities that overlap with ESG scoring criteria. ESG capital is best understood as a secondary tailwind, one that could amplify a valuation recovery driven primarily by the rate cycle and earnings normalisation, rather than as the catalyst that initiates it.

What a recovery would actually need: the conditions that could turn the sector around

Understanding why the ASX healthcare sector underperformed is necessary but insufficient. The actionable question is what specific conditions would need to emerge for a meaningful recovery.

Three conditions stand out:

- Interest-rate normalisation. Falling or stabilising long-term bond yields would directly reverse the valuation compression that drove the bulk of the five-year underperformance. Since the de-rating was primarily rate-driven, rate relief is the single most important macro catalyst.

- Earnings recovery and margin stabilisation. Rate relief alone is not sufficient if underlying earnings continue to disappoint. Post-COVID demand normalisation needs to complete, labour cost pressures need to ease, and companies need to deliver forward guidance that rebuilds analyst confidence. Deloitte’s 2025 outlook suggests this process is ongoing but not yet resolved.

- Company-level catalysts. Pipeline and product developments at major index constituents, such as CSL’s plasma integration programme and Cochlear’s implant penetration growth in developed markets, could drive stock-specific re-ratings that pull the broader sector index higher. Cochlear’s share price decline of 62.7% from the start of 2025 through May 2026 (Rask Invest Research Team) illustrates how deep the drawdowns have been, while its price-to-sales ratio of 2.85x versus a 9.18x five-year average shows how much valuation headroom exists if earnings trajectory improves.

Rask Invest commentary has noted episodic stock-specific outperformance from names like Cochlear and CSL even within a subdued broader sector environment, suggesting the market is willing to reward individual catalysts when they arrive. The question is whether enough catalysts arrive simultaneously to shift the sector-level picture.

The gap between fundamentals and price may be the most interesting thing about ASX healthcare right now

The ASX healthcare sector’s worst five-year stretch on record has unfolded against a backdrop of strengthening global spending fundamentals. The gap between business reality and market price has widened rather than narrowed. The headwinds identified, rate sensitivity, post-COVID earnings resets, labour pressures, are largely cyclical and appear to be fading rather than deepening into permanent structural impairments.

None of this constitutes a timing signal. Sectors can remain undervalued for longer than expected, and the conditions for recovery (rate normalisation, earnings stabilisation, company-level catalysts) are not yet fully in place. Investors assessing their own portfolio exposure to ASX healthcare may find value in monitoring those three conditions against incoming data, rather than waiting for a re-rating already underway.

Investors wanting to understand how major superannuation funds are responding to the valuation dislocation will find our deep-dive into institutional positioning in ASX healthcare, which examines how AustralianSuper and Hostplus have been building exposure to global earners including CSL, Cochlear, and ResMed while avoiding domestically focused pathology operators that face structural Medicare rebate headwinds.

This article is for informational purposes only and should not be considered financial advice. Investors should conduct their own research and consult with financial professionals before making investment decisions. Past performance does not guarantee future results. Financial projections cited are subject to market conditions and various risk factors.