What the June Jobs Report Means for Fed Monetary Policy

1 hr ago

Two broker calls landed on the same morning on 2 July 2026 and moved two of the ASX’s largest sectors by a combined 3.4 percentage points in opposite directions. That is not routine volatility. That is professional money repositioning around a shared macro thesis.

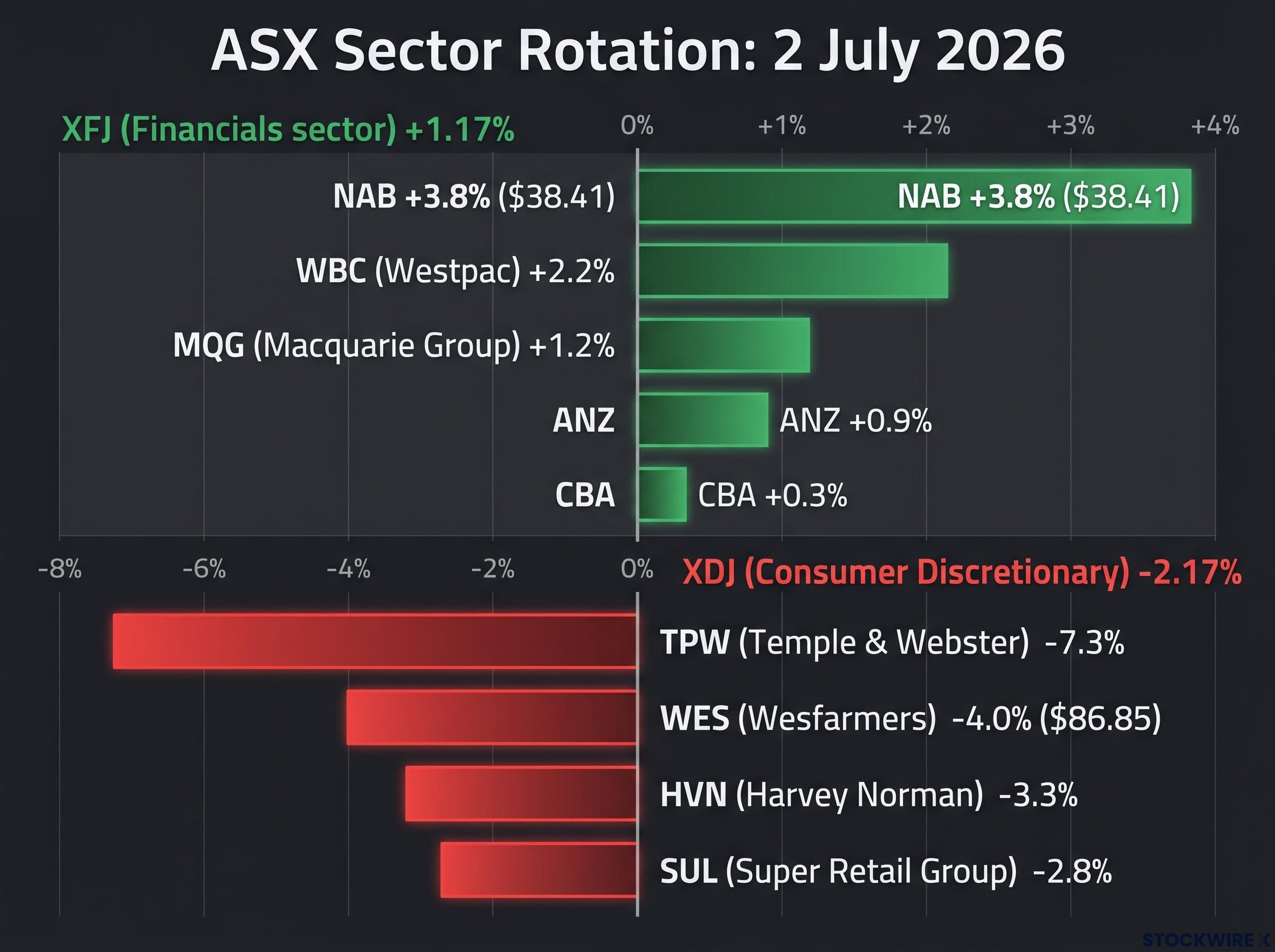

Bank of America upgraded National Australia Bank to Buy. Goldman Sachs downgraded Wesfarmers to Sell. The S&P/ASX 200 Financials index (XFJ) closed up 1.17%, Consumer Discretionary (XDJ) closed down 2.17%, and the gap between them reflected something more significant than two isolated stock opinions. Both calls were expressions of the same underlying view: that Australia’s rate and housing cycle is now sorting winners from losers at the sector level.

Here is what each broker actually argued, why the market moved so decisively in response, and what the rotation tells you about positioning in a rising-rate environment. The two calls, read together, function as a live case study in how institutional analysis moves capital and where risk is being priced right now.

The numbers arrived first. The explanation came after.

The Financials sector (XFJ) closed up 1.17%. Consumer Discretionary (XDJ) closed down 2.17%. The gap between the two, more than three percentage points in a single session, is statistically notable. Single-day divergences of that scale between two major ASX sectors typically require a catalyst with conviction behind it, not just a headline.

Two broker calls provided that catalyst: Bank of America’s upgrade of NAB and Goldman Sachs’ downgrade of Wesfarmers. Their content matters, and the next two sections unpack it. But the price action alone tells you something. Institutional investors moved with conviction, not hesitation, and understanding why matters for how you read the next catalyst.

| Stock / Sector | Price Move (%) |

|---|---|

| XFJ (Financials sector) | +1.17% |

| NAB | +3.8% to $38.41 |

| WBC (Westpac) | +2.2% |

| MQG (Macquarie Group) | +1.2% |

| ANZ | +0.9% |

| CBA | +0.3% |

| XDJ (Consumer Discretionary) | -2.17% |

| WES (Wesfarmers) | -4.0% to $86.85 |

| TPW (Temple & Webster) | -7.3% |

| HVN (Harvey Norman) | -3.3% |

| SUL (Super Retail Group) | -2.8% |

The upgrade was not enthusiasm about NAB in isolation. It was a calculated view on which bank is best positioned for this stage of the rate cycle.

Bank of America moved NAB from Neutral to Buy and lifted its price target from $38.00 to $42.50, implying approximately 10-11% upside from the 2 July close. The thesis rests on NAB’s business mix: its tilt toward business and institutional lending versus the heavier mortgage books of peers, particularly Commonwealth Bank.

Price target revision: Bank of America lifted its NAB target from $38.00 to $42.50, representing approximately 10-11% implied upside from the session close.

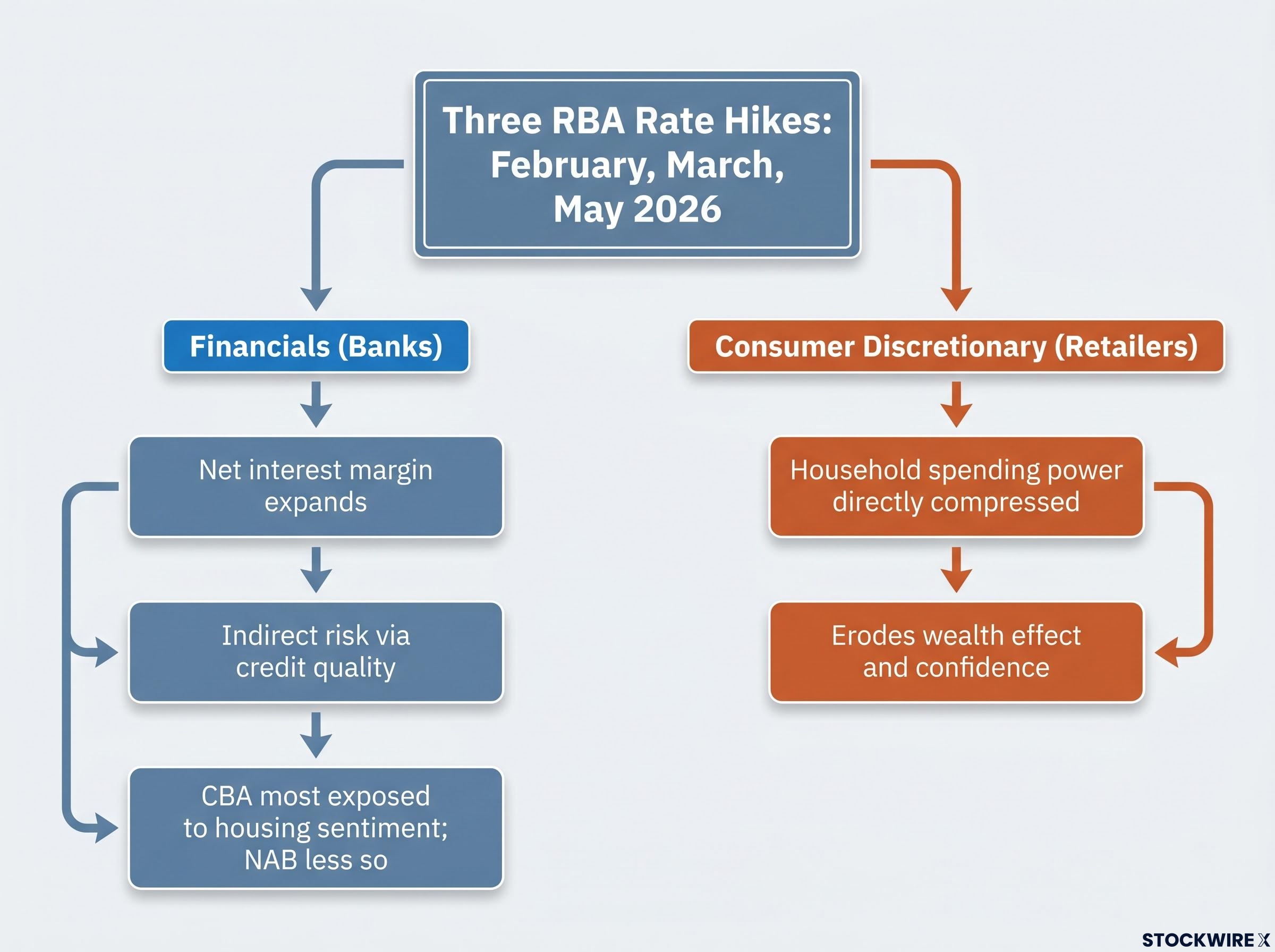

Three RBA rate hikes, in February, March, and May 2026, have put every major bank at a crossroads. Higher rates widen lending margins on one side of the ledger. On the other, they push borrowers closer to stress, raising the risk of arrears and defaults. Bank of America’s upgrade implicitly argues that NAB’s loan composition absorbs that trade-off better than its peers.

The third consecutive RBA hike, delivered in May 2026 with eight of nine Board members voting in favour, established the rate environment that both broker calls were explicitly pricing into their sector theses on 2 July.

The thesis embeds three specific conditions:

CBA’s modest +0.3% gain on the day, the weakest among the major banks, reinforces the point. Not all bank exposure is equivalent right now. The difference in how you benefit from higher rates depends entirely on what kind of lending sits on the balance sheet.

Goldman Sachs analyst Peter Marks moved Wesfarmers from Neutral to Sell. The argument was not about business quality, which was not in dispute. It was about price.

The note pointed to Wesfarmers’ strong share price run since mid-May 2026 and concluded that its valuation had stretched well beyond what Australia’s current consumer backdrop can justify, with three RBA hikes and a softening housing market leaving households in materially weaker shape than the stock’s pricing implied.

Consumer sentiment data from May 2026 showed the headline index sitting 17 points below the neutral threshold of 100, with forward-looking sub-indexes at their weakest since November 2022, a reading that supports the Goldman Sachs argument that Wesfarmers was priced for a consumer environment materially stronger than current conditions.

Goldman Sachs thesis: The market was pricing Wesfarmers as if it were operating in a significantly more buoyant consumer environment than Australia’s current data supports.

Three macro pressures formed the backbone of the downgrade:

What made the session remarkable was not the -4.0% fall in Wesfarmers itself. It was the contagion. Temple & Webster dropped -7.3%. Harvey Norman fell -3.3%. Super Retail Group lost -2.8%. None of those companies received direct coverage in the Goldman Sachs note.

The spread of the sell-off tells you that professional investors were already positioned for this rotation, waiting for a credible institutional signal to act on nervousness they had been sitting with for weeks. Temple & Webster’s -7.3% fall, the sharpest of the session, illustrates the sector sentiment risk embedded in holding high-multiple consumer names when the macro narrative shifts, regardless of individual company fundamentals.

The same three RBA rate hikes produced a bank winner and a consumer loser on the same day. That is not a contradiction. It is the mechanism working exactly as it should.

Net interest margin is the difference between what a bank earns on loans and what it pays on deposits, expressed as a percentage. When the RBA raises rates, banks can reprice loan rates faster than they adjust deposit rates, temporarily widening this margin and lifting earnings.

There is a limit. If rate hikes push borrowers into arrears or default, the margin gain is offset by credit losses. That is precisely why loan mix matters: NAB’s business lending focus versus CBA’s mortgage concentration is the variable that determines which bank captures the margin upside and which absorbs the credit downside.

For consumer-facing businesses, the mechanism runs in reverse. Higher rates reduce the disposable income of mortgage holders directly. A softening housing market erodes the wealth effect, the tendency for homeowners to spend more when their property is appreciating. Both forces compress discretionary spending.

| Rate Hike Effect | Financials (Banks) | Consumer Discretionary (Retailers) |

|---|---|---|

| Net interest margin | Expands (positive for earnings) | Not directly applicable |

| Household spending power | Indirect risk via credit quality | Directly compressed |

| Housing market sentiment | CBA most exposed; NAB less so | Erodes wealth effect and confidence |

| Sector direction on 2 July 2026 | XFJ: +1.17% | XDJ: -2.17% |

Once you understand that rates affect lenders and spenders differently, you can apply this framework prospectively. Any future RBA move will have a directional read for both sectors before a single broker note is published.

Broker ratings and price targets are calibrated for institutional portfolios with different tax positions, time horizons, and diversification constraints than yours. That does not make them useless. It makes them most valuable as reasoning, not as instructions.

The Bank of America NAB upgrade, for example, implies 10-11% upside. The useful question is not “should I buy NAB?” It is: what would have to be true for that target to be met? And what would have to change for the thesis to break?

The Goldman Sachs valuation argument (Wesfarmers priced for a more buoyant consumer environment than the data supports) is a framework you can apply to any consumer holding in your portfolio. Temple & Webster’s -7.3% fall on no direct coverage is a reminder that sentiment-driven contagion can create opportunities when names are sold down for reasons that do not apply to their specific fundamentals.

Four questions to ask when a major broker call moves the sector:

If you can identify which stocks in a sold-down sector do not actually share the downgraded company’s specific vulnerabilities, a sentiment-driven fall can create entry conditions that institutional investors have no mandate to exploit but individual investors do.

The institutional thesis implicit in both calls is clear: banks with business-tilted lending books are preferred over consumer discretionary names carrying premium valuations, given where rates and housing sit in the cycle.

ASX sector rotation of this character, where institutional capital moves decisively between financials and consumer names on a shared macro thesis, was already visible on 2 June 2026, when technology and base metals attracted flows while domestic banks and consumer staples sold off, suggesting the 2 July session was a continuation of a repositioning trend rather than an isolated event.

Three data points will tell you whether this trade continues to hold:

ABS monthly household spending data tracks discretionary versus non-discretionary expenditure at the category level, giving investors a direct empirical read on whether the consumer compression Goldman Sachs identified is accelerating or stabilising ahead of the next earnings cycle.

The same macro input, rising rates, is producing divergent sector outcomes depending on business model. That divergence is unlikely to resolve quickly.

Watching these releases before the next major broker call puts you ahead of the rotation rather than reacting to it.

The two broker calls confirmed one thing clearly: institutional analysts are now reading Australia’s rate cycle as a sector-sorting mechanism, not a rising-tide-lifts-all-boats environment. NAB’s business lending mix made it the focal point for the positive side of that thesis. Wesfarmers’ valuation stretch made it the focal point for the negative side.

What remains genuinely uncertain is the depth of the housing correction, the RBA’s next move, and how quickly consumer spending data will deteriorate. Those variables will determine whether the bank-over-consumer rotation extends or reverses.

The reusable principle from the session is the distinction between business quality and investment value. Wesfarmers remains a high-quality company. The Goldman Sachs Sell call was not a claim otherwise. It was a statement that an excellent company can be a poor investment at the wrong price, and 2 July 2026 demonstrated that institutional analysts are now enforcing that distinction across the ASX.

An excellent company can be a poor investment at the wrong price. The 2 July session demonstrated that institutional analysts are now enforcing that distinction across the ASX.

Days like this are most useful as prompts to audit your own portfolio’s rate exposure, not as direct buy or sell signals.

For investors wanting to situate the 2 July session within a longer pattern of mean reversion and momentum reversals on the ASX, our deep-dive into ASX sector rotation across FY26 covers the operating leverage mechanics that determine which beaten-down names recover and which ones face structural rather than cyclical headwinds.

This article is for informational purposes only and should not be considered financial advice. Investors should conduct their own research and consult with financial professionals before making investment decisions. Past performance does not guarantee future results. Financial projections are subject to market conditions and various risk factors.

ASX broker ratings are formal buy, sell, or hold recommendations issued by institutional research houses such as Bank of America and Goldman Sachs, often accompanied by a price target. When a major broker upgrades or downgrades a large-cap stock, institutional investors frequently reposition capital in response, which can move both the target stock and its broader sector in a single session, as seen on 2 July 2026 when Financials rose 1.17% and Consumer Discretionary fell 2.17%.

Goldman Sachs analyst Peter Marks argued that Wesfarmers' share price had run well ahead of what Australia's consumer backdrop could justify, with three RBA rate hikes in 2026 compressing household disposable income, a softening housing market eroding the wealth effect, and retail data showing pressure in discretionary categories.

Bank of America's upgrade centred on NAB's business and institutional lending mix, which it argued captures margin expansion from higher rates while carrying less mortgage deterioration risk than peers like CBA, whose heavier home loan book makes it more exposed to borrower stress as rates rise.

Rate hikes widen bank net interest margins because loan rates reprice faster than deposit rates, benefiting lenders, while simultaneously compressing household disposable income and eroding the housing wealth effect, which directly reduces spending on discretionary goods and services.

Rather than treating a broker call as a buy or sell instruction, the more productive approach is to interrogate the underlying thesis: ask what conditions would need to be true for the price target to be met, whether the downgrade thesis actually applies to your specific holding, and whether a sector sell-off is fundamentals-driven repricing or sentiment-driven contagion that may have dragged down unrelated names.