Why Off-the-Shelf CAR-T Has an Edge After BTKi Failure

37 mins ago

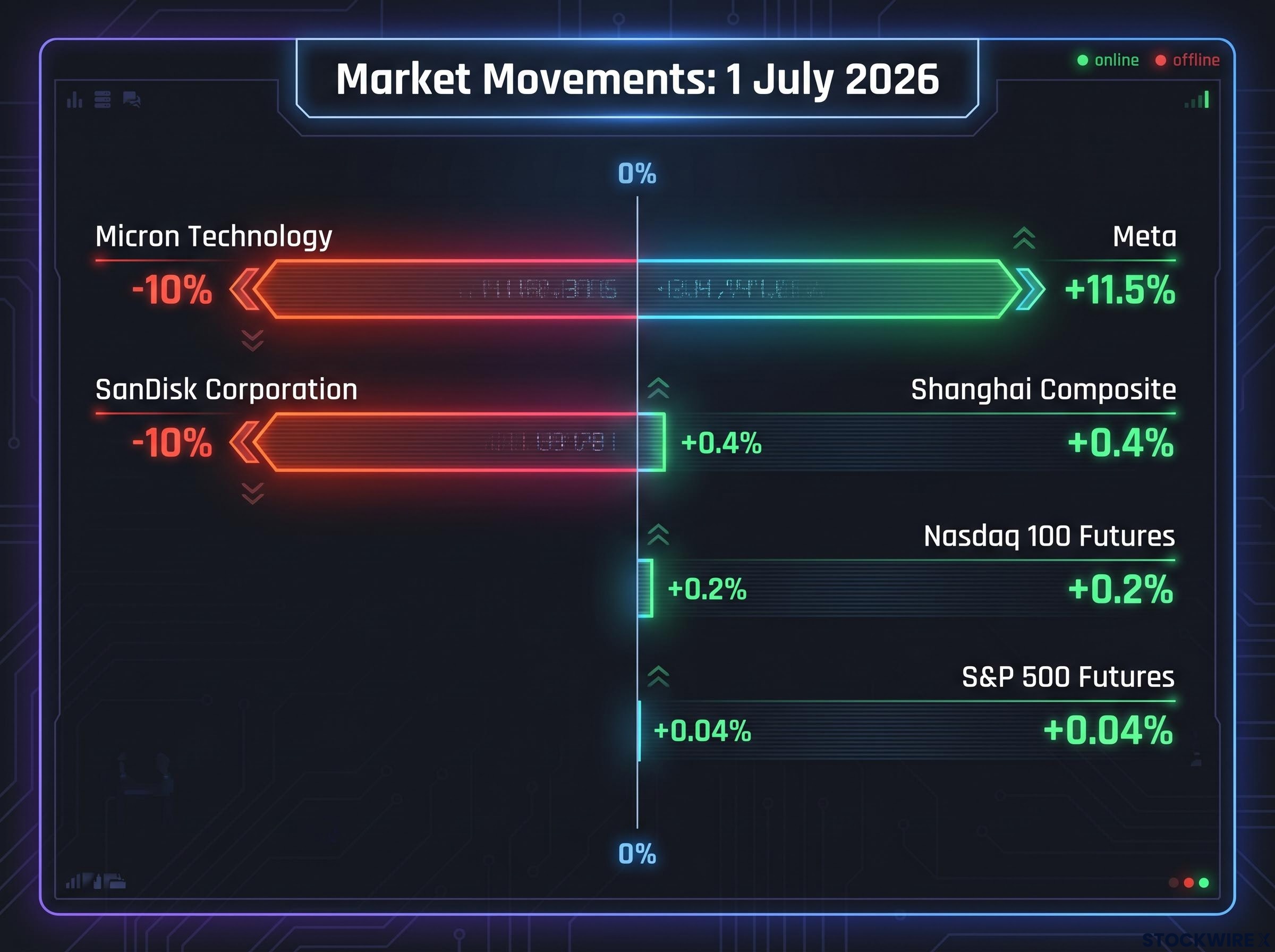

On 1 July 2026, Asian semiconductor stocks fell sharply while U.S. equity index futures rose, and the same two corporate strategy reports caused both outcomes simultaneously.

Meta Platforms and Apple did not announce product launches or earnings beats. They surfaced decisions about infrastructure strategy and supplier evaluation, and those decisions were enough to move markets across multiple continents. That asymmetry, American platforms gaining while Asian suppliers sold off on the back of American platform news, tells a precise story about where leverage in the global AI supply chain currently sits.

Here is a framework for understanding what each move actually signals, why markets in different regions responded so differently, and which variables will determine whether yesterday’s session represented a structural inflection or a temporary repricing. If you are tracking AI sector dynamics, this gives you a clearer lens for interpreting the next wave of hyperscaler strategy announcements.

Two reports circulated during the overnight U.S. session before yesterday’s Asian open: Meta’s plan to sell excess AI compute through a cloud business, and Apple’s evaluation of Chinese memory suppliers. The market response looked contradictory until you follow the logic.

The session’s regional split told the story in four data points:

U.S. hardware suppliers sold off. U.S. platform stocks firmed. Asian chip equities, which had been trading at stretched valuations following the AI supercycle rally, saw those gains unwound further. That is not irrational behaviour; it is a single coherent verdict about who controls AI economics.

The divergence maps onto a buyer-supplier power dynamic: U.S. platforms are operating as AI price setters, while Asian and U.S. hardware suppliers are increasingly positioned as AI price takers.

The platforms that own and monetise compute earn a premium. The companies supplying into that infrastructure earn uncertainty. Once that lens is in place, both Meta’s announcement and Apple’s procurement evaluation become chapters of the same story, and every regional reaction becomes legible.

According to reports, Meta is building a cloud business centred on offering its spare AI compute capacity to outside developers. That includes model access (through its Muse Spark model) and raw compute capacity, in a structure similar to AWS Bedrock or neocloud providers like CoreWeave. The plan sits on top of an infrastructure programme that was already the most aggressive in the industry.

| Year/Period | Capex Figure | Key Development |

|---|---|---|

| 2025 | ~$72.2 billion (guidance: $66-72B) | Launch of Meta Compute as top-level division; ~70% YoY increase |

| 2026 | Guided substantially above 2025 | Cloud business announcement; external compute sales |

| Through 2028 | $600 billion+ committed | Multi-gigawatt U.S. AI infrastructure buildout |

Mark Zuckerberg has stated Meta is planning to build tens of gigawatts of power this decade and hundreds of gigawatts over time, positioning infrastructure scale itself as a strategic advantage.

The cloud plan changes how capital markets interpret that capex in three specific ways.

First, monetisation converts cost to revenue. Selling spare capacity transforms what looked like potentially reckless spending into a future recurring revenue stream. Second, buyer leverage improves margins. A hyperscaler that is also an infrastructure provider has stronger incentive to negotiate harder with chip vendors, multi-source components, and accelerate custom silicon. Third, infrastructure scale becomes defensible. Owning the data centres becomes as strategically important as owning the models.

Meta’s stock rose as much as 11.5% on the day the cloud plan was reported. The same spending numbers that might have triggered overinvestment concerns before the cloud announcement now read as capacity that will be sold, not just consumed. For investors, the implication is broader than one company: if hyperscalers can monetise their data centre buildouts, every future infrastructure investment announcement carries a different valuation implication than it did two years ago.

For investors wanting the full picture on how the cloud division would operate, our dedicated guide to Meta Compute covers the two distinct revenue models under consideration, the competitive implications for AWS and CoreWeave, and why no confirmed launch date or customer pipeline has been disclosed despite Zuckerberg’s public confirmation of the plan.

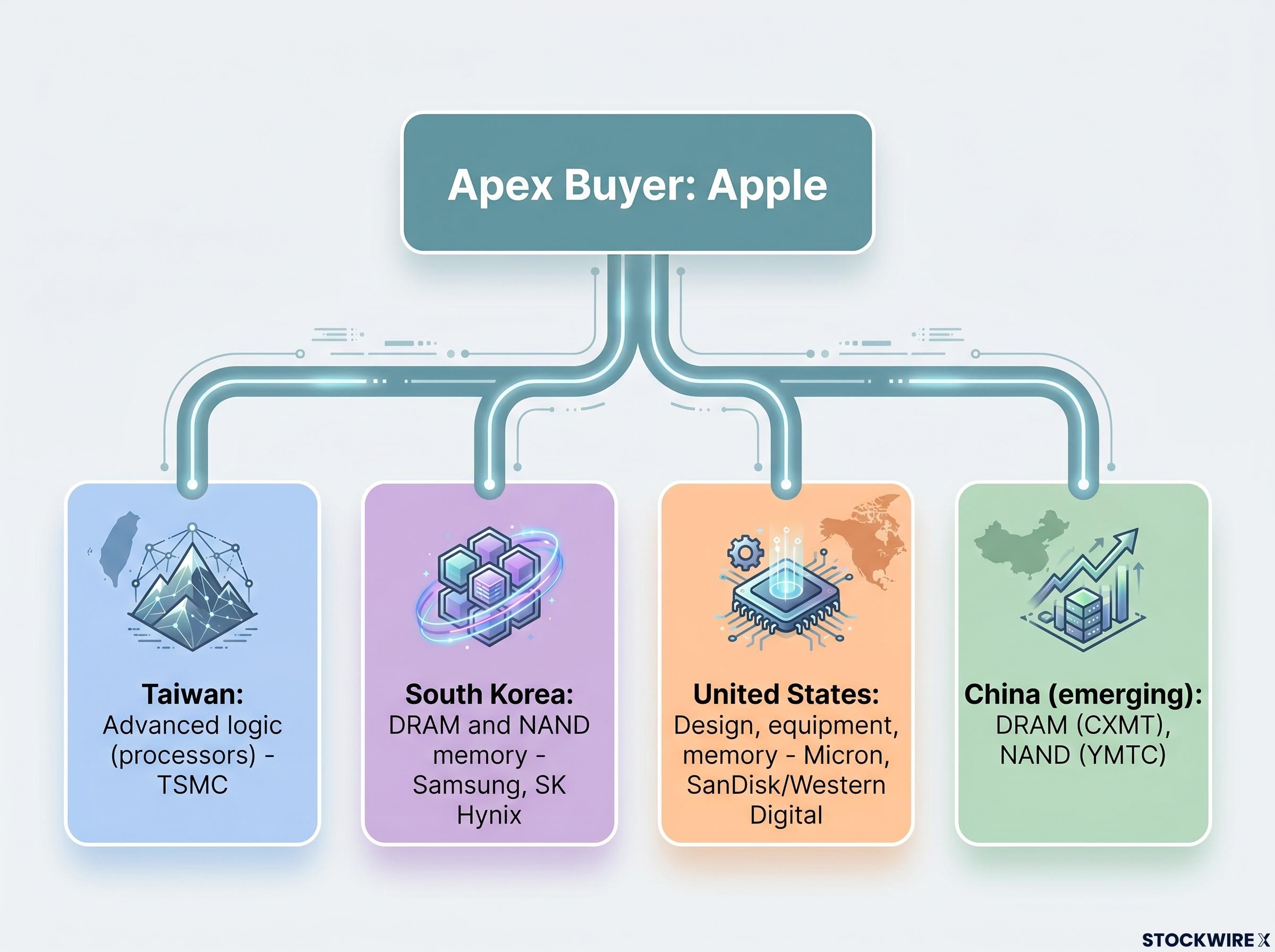

To understand why Apple’s procurement evaluation moved markets across three continents, you first need a map of who does what in the semiconductor supply chain and why it matters that a single buyer can shift the entire structure.

The global chip supply chain has historically relied on geographic specialisation. A few definitions make the architecture clearer:

| Region | Chip Category | Key Players |

|---|---|---|

| Taiwan | Advanced logic (processors) | TSMC and advanced packaging specialists |

| South Korea | DRAM and NAND memory | Samsung, SK Hynix |

| United States | Design, equipment, memory | Micron, SanDisk/Western Digital, equipment makers |

| China (emerging) | DRAM (CXMT), NAND (YMTC) | CXMT, YMTC |

Apple sits at the apex of this supply chain. As one of the world’s largest and most predictable volume buyers, its procurement decisions do not just affect Apple’s own cost structure. They move entire market segments. Samsung, SK Hynix, and Micron have historically been central to Apple’s DRAM and NAND supply.

The same memory chip stocks that posted combined gains exceeding 250% in the 30 days through 12 May 2026, driven by sold-out HBM capacity and a looming Samsung labour dispute, are now absorbing the full force of the buyer-power repricing that Apple’s procurement evaluation and Meta’s infrastructure pivot represent.

What this tells you is that a single exploratory procurement evaluation by Apple, even without a signed contract, is sufficient to move incumbent stock prices. The risk being priced is not a lost order. It is a lost pricing position.

Reports indicate that Apple has begun assessing memory components from Chinese producers, with CXMT under consideration for DRAM supply and YMTC for NAND, as part of a broader sourcing review. No formal commitment to volume production has been made public. Apple has previously evaluated YMTC for NAND supply, though U.S. export controls and political pressure complicated those earlier efforts.

The evaluation creates three distinct layers of risk for incumbent suppliers:

The geopolitical complication remains active. U.S. export controls and political pressure have historically constrained Apple’s ability to use Chinese components in flagship products, and that constraint has not been removed.

The market is not pricing a confirmed order loss. It is repricing the probability that incumbent memory suppliers will retain Apple’s volume at current margins indefinitely, and that probability is now lower than it was before this report.

For investors holding Korean or U.S. memory stocks, the evaluation introduces a scenario that was previously treated as low probability: a flagship Western OEM using Chinese memory at volume. Even an elevated probability of that scenario changes the risk profile of those positions.

Yesterday’s session was not an isolated event driven by two individual company decisions. It is a pattern that will keep producing similar market outcomes, driven by three structural forces:

The traditional division of labour, Taiwan for advanced logic, Korea for memory, the U.S. for design and equipment, is under pressure from multiple directions simultaneously. Chinese capability is growing. Hyperscalers are vertically integrating. Western industrial policy is redirecting investment onshore.

Disruption does not mean overnight displacement. It means the power balance between buyers and suppliers is shifting in ways that affect margins and market-share durability, and that shift is structural rather than cyclical.

The forces described above point in one direction, but the speed and permanence of the shift depend on observable variables. For investors building a view on semiconductor exposure, these five function as a checklist.

| Variable | What to Watch | Incumbent Outcome | Disruptor Outcome |

|---|---|---|---|

| Meta’s cloud product specifics | Raw compute vs. managed model access; share reserved for external customers | Internal-only consumption; chip demand unchanged | Large external allocation; custom silicon displaces third-party chips |

| Apple’s procurement decisions | Whether CXMT/YMTC graduate from evaluation to volume shipment | Evaluation stalls; incumbents retain Apple volume | Chinese memory ships in flagship products at scale |

| Hyperscaler capex guidance | Meta’s 2026 spend (guided above ~$72.2B 2025 actual); peer budgets | Spending plateaus or reallocates toward incumbents | Spending accelerates but routes through in-house infrastructure |

| Chinese chipmaker capability | Yield, reliability, and performance metrics at CXMT (DRAM) and YMTC (NAND) | Gap with incumbents persists; Apple evaluation stalls | Gap narrows rapidly; credible alternative at volume |

| U.S.-China policy shifts | Export control tightening or relaxation affecting component sourcing | Tighter controls block Chinese memory in Western products | Relaxation or workarounds permit Chinese supply at scale |

These variables are not independent. A tightening of export controls, for example, directly constrains whether Apple’s evaluation converts to orders regardless of YMTC’s technical progress. When more of them resolve in favour of supply chain disruption, the repricing seen on 1 July 2026 will extend. When they resolve in favour of incumbents, yesterday’s selloff was a buying opportunity.

U.S. export control durability is the single variable that most constrains whether Apple’s Chinese memory evaluation ever converts to volume orders; those controls are grounded in national-security law with bipartisan Congressional backing, placing them outside the jurisdiction of trade negotiators regardless of how bilateral diplomatic conditions evolve.

The two catalysts that moved markets yesterday express a single underlying dynamic: U.S. platforms are actively increasing their leverage over the AI supply chain, and that leverage is now being priced simultaneously from the buy side (Apple’s procurement) and the infrastructure side (Meta’s cloud pivot).

No formal contracts were signed. The market moved on strategy signals alone, which tells you how sensitively positioned Asian chip valuations had become after the AI supercycle rally. Taiwanese AI supply-chain names had already been repricing from elevated valuations; yesterday’s session accelerated an existing trend rather than creating one from scratch. The Shanghai Composite bucked the regional trend, finishing the day up roughly 0.4%, holding up comparatively well while broader Asian markets sold off.

Meta’s stock rising as much as 11.5% on the cloud announcement shows how directly U.S. platforms are rewarded for concentrating leverage. That reward, and the corresponding pressure on suppliers, is not going away.

The session did not tell investors that AI spending is slowing. It told them that the distribution of AI profits is concentrating, and that concentration matters more for portfolio positioning than the headline spending numbers do.

Investors who leave with the price-setter versus price-taker framework have a tool that will remain relevant for every subsequent hyperscaler announcement, regardless of which companies are involved or which region’s supply chain is next in scope.

For investors who want to extend the price-setter versus price-taker framework into a forward-looking portfolio view, our deep-dive into AI infrastructure positioning examines which binding constraints, power availability, cooling density, and grid interconnection timelines, are most likely to concentrate durable compounding value as the hyperscaler buildout accelerates.

This article is for informational purposes only and should not be considered financial advice. Investors should conduct their own research and consult with financial professionals before making investment decisions. These statements are speculative and subject to change based on market developments and company performance.

In the current AI supply chain, U.S. platforms like Meta and Apple control AI economics by setting demand terms and procurement conditions, while hardware suppliers in Asia and the U.S. compete for that business on the platform's terms, making them price takers with less pricing power and thinner margin durability.

Meta's cloud compute pivot signals that hyperscalers are building infrastructure at scale and monetising it internally, reducing dependence on third-party chip vendors, while Apple's evaluation of Chinese memory suppliers from CXMT and YMTC raised the probability that incumbent Korean and U.S. memory makers could lose volume or pricing power at one of the world's largest buyers.

CXMT is a Chinese DRAM manufacturer whose products Apple is reportedly assessing as part of a broader sourcing review; even without a confirmed order, the evaluation signals that Chinese memory technology is credible enough for Apple to consider seriously, which erodes the perceived durability of Micron's and Samsung's market share and pricing positions.

By selling spare AI compute capacity externally, Meta converts what previously looked like potentially reckless capital expenditure into a future recurring revenue stream, which changes how investors should interpret every future hyperscaler infrastructure spending announcement: the capex is no longer just a cost line, it is potential product inventory.

The five key variables are: whether Meta's cloud product allocates meaningful capacity externally, whether Apple's CXMT and YMTC evaluations convert to volume shipments, the trajectory of hyperscaler capex guidance, the pace of Chinese chipmaker yield and performance improvements, and whether U.S. export controls on advanced components tighten or relax.