Why AI Is Splitting Semiconductor Stocks From the Rest of Tech

2 hrs ago

Australian investors can access some of the most consequential oncology innovation on the planet through ASX biotech stocks, yet most apply analytical frameworks built for a completely different type of company. The toolkit that works for AstraZeneca or Pfizer, revenue, margins, patent cliffs, dividend sustainability, was designed for diversified commercial enterprises generating billions from multiple on-market products. It systematically misfires when pointed at a clinical-stage cell therapy programme with no revenue, no dividends, and a value trajectory determined entirely by development milestones.

Cell and gene therapy innovation has concentrated overwhelmingly in US and European markets, where deep specialist capital pools, leading academic centres, and experienced regulatory interfaces created reinforcing structural advantages. A small number of ASX-listed programmes now operate inside that same global system, not parallel to it, engaging directly with the FDA, competing for the same conference platforms, and generating data under the same scientific standards.

Here is the framework for reading the signals that actually matter in clinical-stage ASX biotech, including what a milestone cluster like Imugene’s azer-cel programme, with its current convergence of regulatory and scientific milestones, tells an informed investor.

The instinct most investors bring to pharmaceutical analysis is earned from years of watching large-cap names. Roche reports quarterly revenue across dozens of marketed products. Pfizer navigates patent cliffs on blockbuster drugs. AstraZeneca manages pipeline breadth alongside a growing oncology franchise. In each case, valuations are anchored to a commercial base: what the company sells today, what margins it earns, and what the next product cycle adds to that base.

None of that applies to a clinical-stage ASX biotech. There is no commercial revenue to model. There are no margins to assess. Conventional financial metrics are not merely less useful; they are structurally inapplicable.

ASX healthcare risk mispricing has produced some of the sector’s most damaging investor outcomes precisely because the ‘defensive’ label attached to healthcare stocks obscures the categorically different risk profiles sitting within the same sector classification, from commercial large-caps to single-asset clinical programmes.

The analytical question shifts entirely. Instead of “what are this quarter’s earnings?” the relevant question becomes “what has changed in this programme’s development trajectory, and what does that imply about where it is heading?” Value is signalled through a progression of development milestones: regulatory interactions, clinical data readouts, conference presentations, and trial initiations. Each event carries specific information about the credibility and potential of the underlying asset.

| Dimension | Large-Cap Pharma | Clinical-Stage ASX Biotech |

|---|---|---|

| Revenue base | Billions from multiple marketed products | No commercial revenue |

| Key valuation drivers | Earnings, margins, dividend yield, patent life | Development milestones and regulatory signals |

| Relevant analytical questions | What are this quarter’s earnings? | What has changed in the programme’s trajectory? |

| Milestone materiality | Incremental upside to an established base | Foundational; can redefine the entire outlook |

In a diversified commercial pharma company, even a major clinical success typically adds incremental upside to an already substantial revenue base. The enterprise does not get redefined by a single data readout.

In a clinical-stage ASX biotech, the dynamic inverts. A single regulatory designation or high-profile conference selection can be foundational rather than incremental, because it may represent the clearest external signal yet on the programme’s primary asset. That is the structural difference investors need to internalise before reading any milestone news flow.

The concentration of cell and gene therapy activity in US and European markets did not happen by accident. It reflects a set of reinforcing structural advantages that compounded over decades:

These advantages created a gravitational pull. Capital, talent, and regulatory precedent all concentrated in the same markets, making it progressively easier for programmes based there and progressively harder for programmes based elsewhere.

Participation by an ASX-listed company in this global cycle requires deliberate construction, not just ambition:

When an ASX-listed cell therapy programme successfully builds this architecture, its milestones become globally legible. They are generated and interpreted under the same standards that govern evaluation of cell therapies worldwide. For you as an investor, distinguishing between a programme that is genuinely inside the global innovation cycle and one operating on a domestic parallel track is the single most consequential structural question to resolve before reading any milestone news.

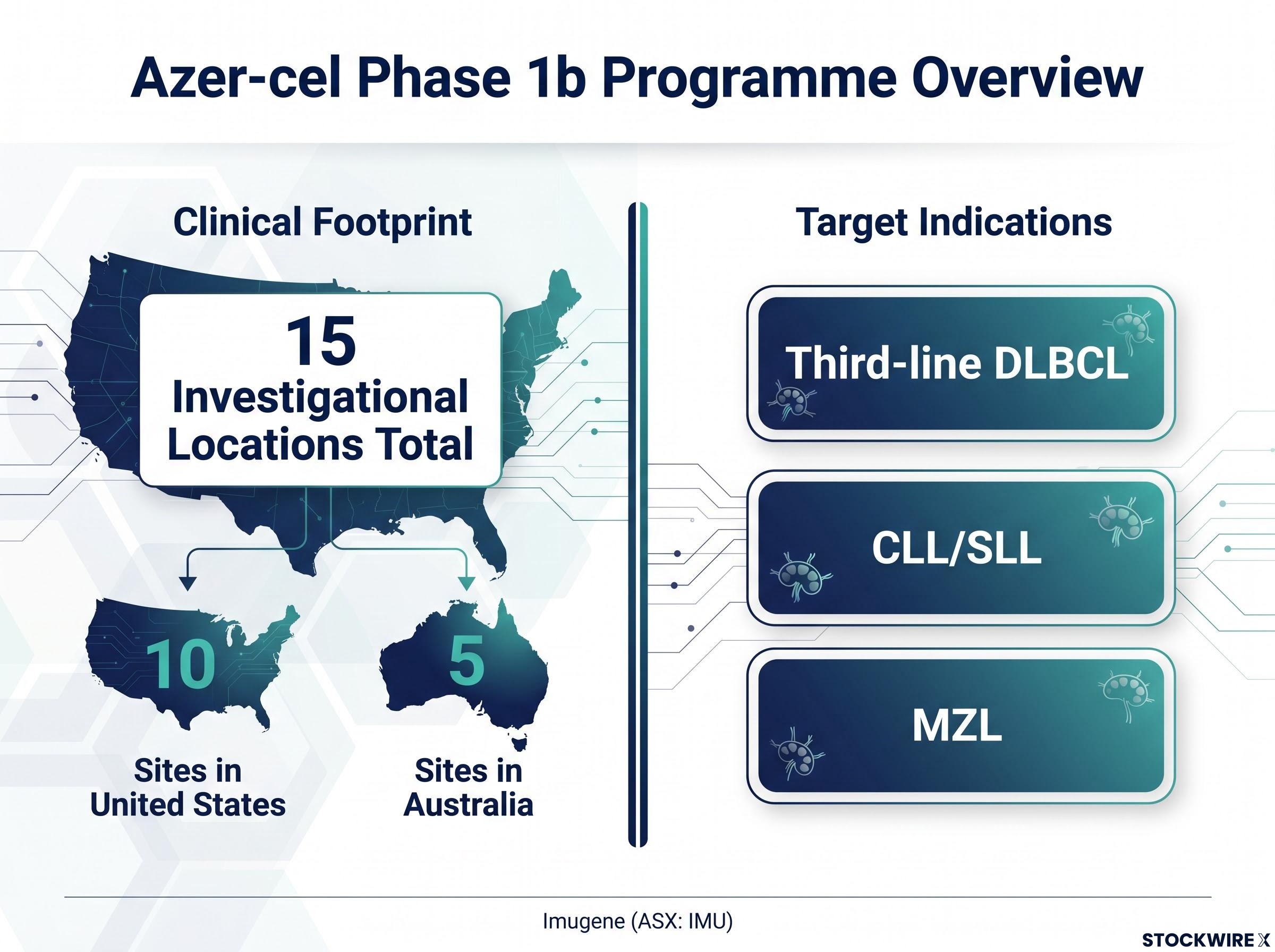

Imugene (ASX: IMU) is advancing azer-cel, an allogeneic CD19-directed cell therapy (a treatment made from donor cells, engineered to target the CD19 protein found on certain cancer cells), through a Phase 1b programme in haematological malignancies. The structure of this programme answers the questions the previous section taught you to ask.

The Phase 1b programme is active across 15 investigational locations: 10 clinical sites in the United States and 5 sites in Australia. US site participation is central rather than incidental.

10 of azer-cel’s 15 clinical sites are in the United States, anchoring the programme in the primary regulatory and commercial market and ensuring clinical data reflects patient populations and practice environments relevant to a potential US pathway.

The target indications span three well-characterised B-cell malignancies with recognised unmet need in relapsed or refractory settings:

The geographic split of the trial footprint is not an administrative detail. It is the mechanism by which this ASX-listed programme anchors itself in the primary regulatory and commercial market, making its data relevant to a potential US pathway rather than only a domestic one. That distinction is what separates a globally integrated programme from a locally contained one.

The azer-cel valuation gap relative to allogeneic CAR-T peers listed in the United States reflects a combination of factors specific to ASX listing venue, development stage, and capital access, rather than a simple discount applied to the clinical modality itself.

Azer-cel has generated a cluster of recent milestones that collectively indicate progression on multiple fronts. Each carries distinct analytical meaning, and the value for you as an investor sits not in any single event but in the cumulative weight: each milestone represents an external party with no financial stake in the outcome signalling that the programme cleared a material bar.

The American Society of Clinical Oncology (ASCO) annual meeting is one of the most influential oncology congresses globally. Abstracts are submitted openly, and only a subset is selected for oral presentation, a higher-visibility format than poster selection that reflects independent scientific prioritisation.

When more than 8,500 abstracts were submitted for ASCO 2026, azer-cel data earned selection for oral presentation in a competitive field reviewed by independent scientific committees. This is not a regulatory endorsement or a commercial signal. It tells you that independent scientific reviewers, parties with no financial stake in the stock, judged the data sufficiently compelling for prominent presentation. In a pre-revenue company where company-produced communications dominate information flow, that kind of external scientific validation carries particular informational weight.

The FDA uses structured meeting types for sponsor-agency dialogue. A Type C meeting addresses specific development questions, including trial design and the acceptability of a proposed registrational strategy (the study design a company would use to seek formal approval).

Through a Type C meeting with the FDA, Imugene reached agreement on the design of a potential registrational pathway for azer-cel targeting third-line DLBCL. This is the category of milestone that does not merely confirm existing trajectory; it alters the development path. Before this alignment, key aspects of how a registrational study could be designed remained uncertain. After it, the uncertainty converts into a defined development requirement. That is a qualitatively different kind of milestone from a conference presentation.

Separately, azer-cel has received Fast Track Designation for both CLL/SLL and MZL. Fast Track Designation is granted to investigational therapies for serious conditions where preliminary evidence suggests potential to address unmet medical need. It enables more frequent FDA interaction and potential use of expedited development and review tools. Multiple designations across distinct indications broaden the regulatory support profile of the programme and institutionalise a closer, more iterative relationship with the agency.

The FDA Fast Track Designation criteria require preliminary clinical evidence suggesting that an investigational therapy may address unmet medical need in a serious condition, a standard that makes the award of dual designations across CLL/SLL and MZL a meaningful external signal rather than a procedural formality.

| Milestone | External validator | What was assessed | Investor-relevant implication |

|---|---|---|---|

| ASCO 2026 oral presentation | Independent scientific committee | Clinical data quality and scientific interest | External peer validation of data from a non-financial party |

| FDA Type C alignment (third-line DLBCL) | FDA | Registrational pathway design and acceptability | Converts key development uncertainty into a defined requirement |

| Fast Track Designations (CLL/SLL and MZL) | FDA | Unmet need and preliminary evidence of therapeutic promise | Formalises enhanced agency engagement across multiple indications |

Cell therapies like azer-cel are generally positioned for patients who have progressed after BTK inhibitors (Bruton’s tyrosine kinase inhibitors, a class of targeted drugs that have become standard-of-care treatments for several B-cell malignancies) or are otherwise ineligible for standard options. The therapeutic territory these patients occupy is not speculative; it is commercially and clinically well-established.

Industry estimates placed the BTK inhibitor therapeutic market at around US$12.0 billion as of 2025, reflecting the scale and clinical activity of the treatment landscape into which next-generation therapies are positioned.

That figure is not a commercial forecast for any clinical-stage asset. What it tells you is something more specific about the therapeutic territory:

The size of this market matters for how you contextualise a programme like azer-cel. It confirms that FDA regulators see unmet need worth engaging with in these indications, and it explains why clinical-stage programmes targeting post-BTKi patients attract the level of external attention reflected in the milestone cluster. It does not predict commercial success for any given asset, but it validates that the therapeutic territory is both clinically important and commercially active.

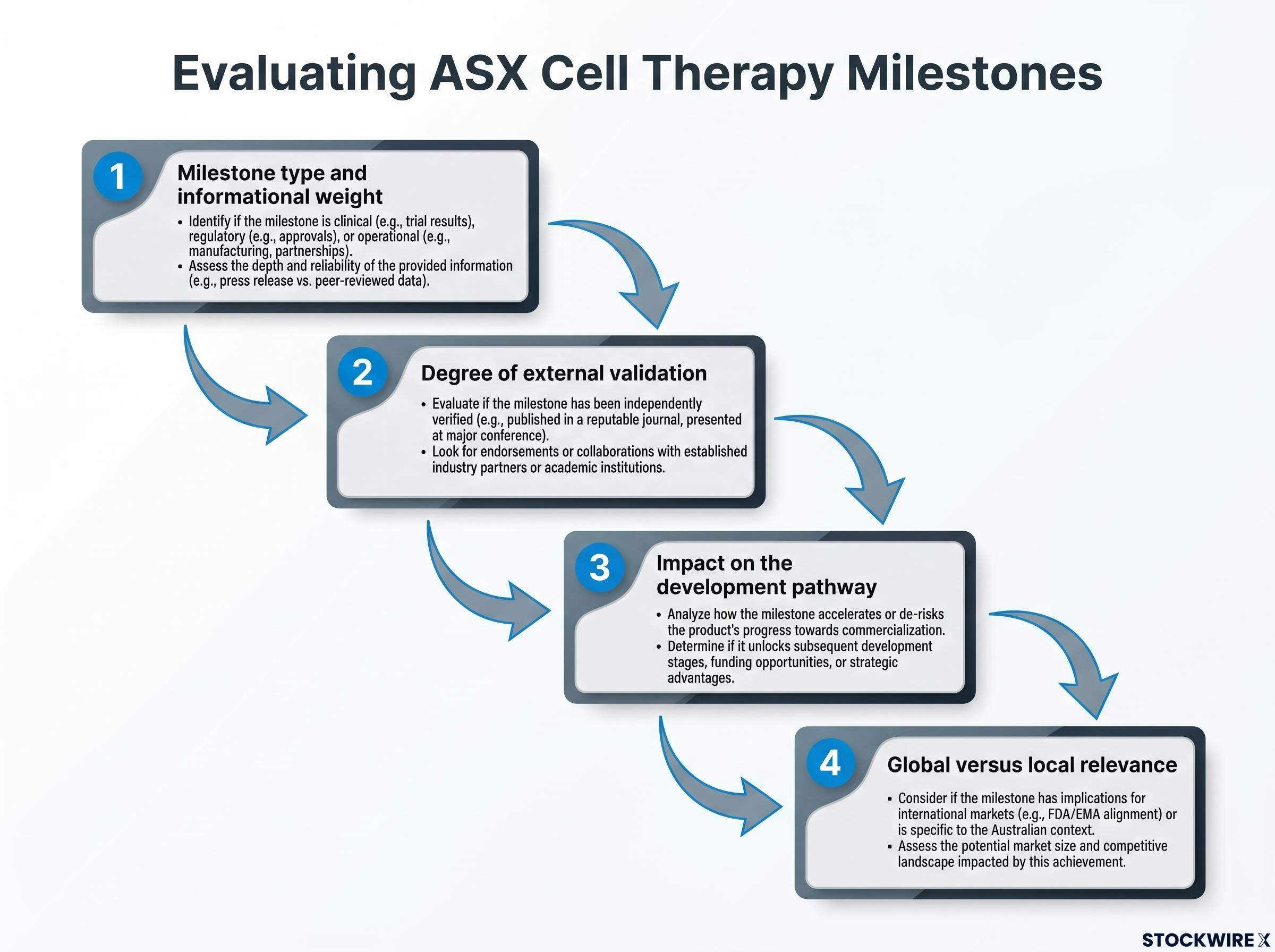

The milestone framework that emerges from this analysis gives you a practical tool for reading clinical-stage news flow, one that applies well beyond any single programme. When an ASX-listed cell therapy company announces a development, run it through four questions in sequence:

Azer-cel’s current milestone cluster, the ASCO 2026 oral presentation, FDA Type C alignment on a registrational study design, dual Fast Track Designations, and a 15-site multi-country trial, spans several high-value categories of this framework and involves multiple independent external validators.

ASX-listed cell therapy companies provide concentrated exposure to specific clinical-stage programmes, with binary outcomes at each development gate, rather than diversified pharma-like exposure with stabilising revenue floors. The analytical discipline required is meaningfully different from following a large-cap pharmaceutical name. This framework does not tell you what to do; it tells you what questions to ask. Having the right questions is the foundational requirement for reading clinical-stage news flow without systematically misreading it.

ASX biotech funding structures are under additional pressure from a proposed federal policy change that would cap refundable R&D tax offsets at a company’s first 10 years of operation, creating a structural mismatch with clinical development timelines that routinely stretch 12-15 years for cell and gene therapy programmes.

This article is for informational purposes only and should not be considered financial advice. Investors should conduct their own research and consult with financial professionals before making investment decisions. Past performance does not guarantee future results, and the clinical-stage programmes discussed involve substantial development risk and uncertainty.

Clinical-stage ASX biotechs operating inside the global cell therapy innovation cycle are a distinct investment vehicle requiring distinct analytical tools. The milestones that signal programme quality are globally interpretable when the programme has built genuine global engagement, with the same regulators, the same conference platforms, and the same agency review processes governing evaluation regardless of where the company is listed.

These are not stabilising holdings. The concentrated risk profile is real, and the analytical discipline required is meaningfully different from following diversified pharma. Cell and gene therapy remain among the most active innovation categories in oncology globally, and for ASX investors the access question is not whether the innovation cycle exists, but how to read the signals of the programmes providing that access through domestic listings.

For investors extending this analytical framework to other ASX clinical-stage programmes with defined 2026 timelines, our dedicated guide to ASX biotech binary catalyst investing examines how to size positions and pre-define exit conditions before a binary data readout arrives.

—

ASX biotech stocks, particularly clinical-stage ones, have no commercial revenue, no dividends, and no earnings to model; their value is determined entirely by development milestones such as regulatory designations, FDA meeting outcomes, and conference data presentations, making standard pharma valuation frameworks structurally inapplicable.

Fast Track Designation is granted by the FDA to investigational therapies targeting serious conditions where preliminary evidence suggests potential to address unmet medical need; it enables more frequent FDA interaction and potential access to expedited development and review tools, formalising a closer relationship with the agency.

An oral presentation at the American Society of Clinical Oncology annual meeting is selected by independent scientific committees from thousands of submitted abstracts, more than 8,500 for ASCO 2026, and represents external peer validation that the clinical data is compelling enough for prominent presentation by parties with no financial stake in the stock.

Run the announcement through four questions: what type of milestone is it, was it validated by an external party such as a regulator or independent scientific committee, does it change the development pathway or merely confirm it, and is it generated within the global regulatory and scientific system rather than only a domestic one.

BTK inhibitors are a class of targeted drugs that have become standard-of-care for several B-cell malignancies, with the market estimated at around US$12.0 billion as of 2025; cell therapies like azer-cel are positioned for patients who have progressed after these treatments, meaning a large, commercially active patient population with recognised unmet need already exists.