Two Index Changes on 29 June, Two Very Different Flow Stories

2 hrs ago

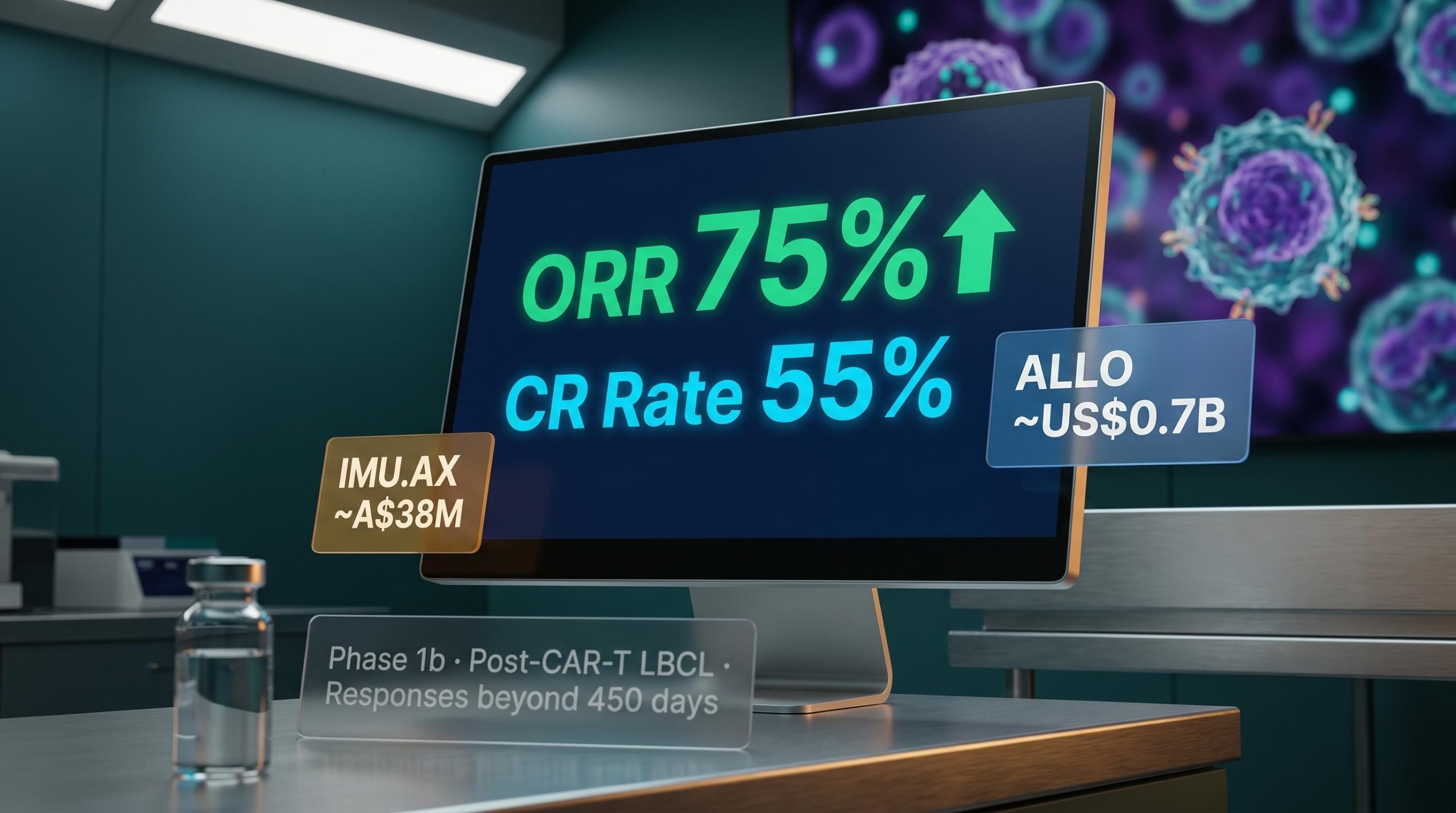

A clinical-stage allogeneic CAR-T developer with three FDA Fast Track Designations and a Phase 1b complete response rate above 55% in patients who have already failed existing CAR-T therapies. Market capitalisation: below A$38 million.

That is Imugene (ASX: IMU), and the gap between its clinical progress and its market pricing is the central tension of this analysis.

Allogeneic CAR-T, where treatments are manufactured in advance from donor cells rather than custom-built for each patient, is a field where the number of credible clinical programmes is shrinking. Several early entrants have dropped out as the science exposed persistence and efficacy limitations. At the same time, large pharmaceutical companies have demonstrated willingness to pay billions for next-generation cell therapy platforms still in development. Those two dynamics create the backdrop against which Imugene’s data and valuation exist simultaneously.

What follows is a structured walkthrough of the four inputs that together form what Diamond Equity Research characterises as an asymmetric setup: the clinical data, the peer comparison, the mergers and acquisitions (M&A) backdrop, and the structural risks that condition the entire thesis. This piece will be clear about what is confirmed data and what is probabilistic framing.

The investment characterisations in this article are sourced from Diamond Equity Research, which operates as a company-sponsored analyst for Imugene. This is not independent research. All forward-looking and valuation statements should be read in that context.

The most current publicly available data for azer-cel (azercabtagene zapreleucel) comes from the July 2025 Phase 1b update in heavily pretreated post-CAR-T diffuse large B-cell lymphoma (DLBCL) and large B-cell lymphoma (LBCL) patients. These are patients who have already failed autologous CAR-T therapy from Gilead/Kite, BMS, or Novartis, a population with very limited remaining treatment options.

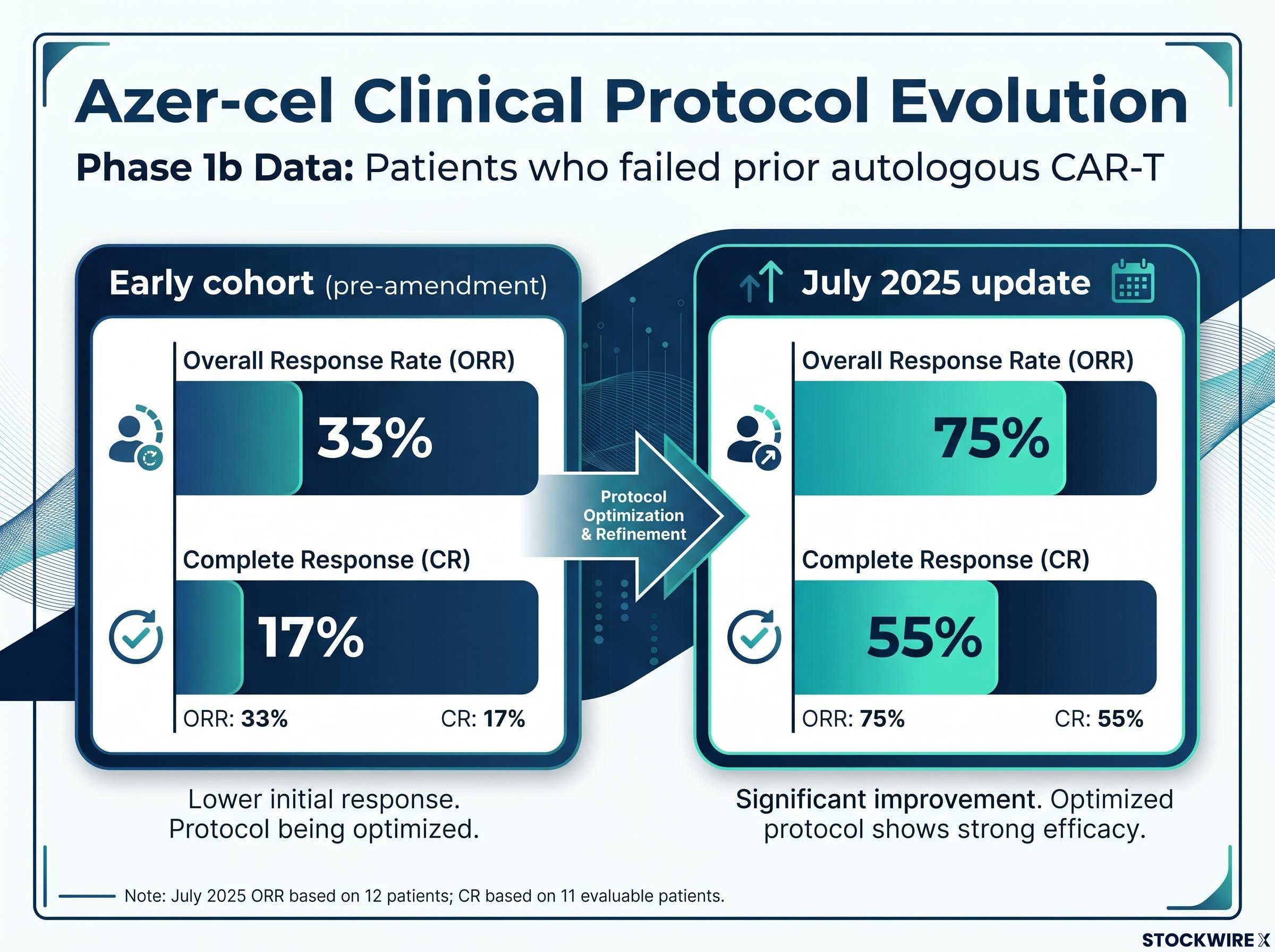

The headline figures: an overall response rate (ORR) of 75% (9 of 12 patients) and a complete response (CR) rate of 55% (6 of 11 evaluable patients). ORR measures the proportion of patients whose tumours shrank or disappeared. CR means no detectable cancer remained.

Those numbers reflect the current protocol, which includes the addition of IL-2 to the treatment regimen. Earlier cohorts treated under the pre-amendment protocol showed materially lower activity: 33% ORR and 17% CR. The protocol evolution matters because it demonstrates that the programme iterated toward a more effective dosing strategy, and the February 2025 interim data (4 CRs in 7 DLBCL patients) tracked consistently with the trajectory that culminated in the July update.

| Timepoint | Patients Evaluable | ORR | CR Rate | Durability Signal |

|---|---|---|---|---|

| Early cohort (pre-amendment) | Small cohort | 33% | 17% | Limited data |

| February 2025 interim | 7 DLBCL patients | N/A | ~57% (4 CRs) | Responses ongoing |

| July 2025 update | 12 (ORR); 11 (CR) | 75% | 55% | Responses beyond 450 days |

At least one patient has been reported cancer-free at 15 months and counting, with some responses ongoing beyond 450 days. A formal median duration of response has not yet been established; the data remain immature.

A 55% complete response rate in patients who have already exhausted autologous CAR-T is a meaningful early signal in a population where most available treatments produce transient partial responses at best. But 12 patients is not a population, and oncology history is full of promising Phase 1 signals that did not hold. That tension should sit clearly in any assessment of what comes next.

The programme’s reach beyond the post-CAR-T relapsed population is also accumulating data: azer-cel in CAR T-naive patients across six blood cancer subtypes produced an 81% overall response rate in 16 evaluable patients as of the May 2026 ASCO oral presentation, with four individual indications reaching 100% response rates.

The allogeneic CAR-T category has contracted, and that contraction matters more than the opportunity it leaves behind.

Allogeneic (off-the-shelf) CAR-T cell therapy differs from the autologous approach in three structural ways:

These advantages are real in theory. In practice, however, multiple early allogeneic programmes encountered efficacy, persistence, and safety limitations that led to discontinuation or deprioritisation. The field has shed players as the science matured, leaving a short list of programmes with credible Phase 1 signals still active.

Allogene Therapeutics and its lead asset cema-cel represent the primary clinical benchmark for azer-cel. Both target CD19 in relapsed/refractory B-cell lymphomas using the same allogeneic modality, making them directly comparable on target and approach. Cema-cel is further advanced, with larger multi-centre clinical programmes, a longer data history, and more established regulatory dialogue with the Food and Drug Administration (FDA). Allogene’s market capitalisation sits at approximately US$0.7 billion as of June 2026.

Indirect competition is also active. Autologous CAR-T retreatment strategies, bispecific antibodies (drugs engineered to bind two different targets simultaneously), and other novel targeted agents are all developing in the same post-CAR-T treatment space. Major companies with approved autologous CAR-T products, including Gilead/Kite, BMS, and Novartis, recognise the post-CAR-T LBCL population as a key unmet need, which simultaneously validates the commercial opportunity and intensifies competitive pressure.

The field contraction means the competitive ceiling for a programme with credible efficacy signals is rising even as the number of challengers falls. That is the structural backdrop that makes the peer valuation gap worth examining rather than dismissing.

Imugene: approximately A$38 million. Allogene Therapeutics: approximately US$0.7 billion. Both operating in allogeneic CD19 CAR-T.

The gap is large. It is also not self-explanatory.

Several structural factors legitimately contribute to the discount. Imugene trades on the ASX, where clinical-stage cell therapy is less familiar to the institutional investor base, sector ETF inclusion is limited, and analyst coverage is thinner. Allogene trades on NASDAQ with access to deep US biotech capital pools. That listing venue differential alone can produce a persistent valuation discount regardless of clinical merit.

ASX healthcare structural discounts operate through mechanisms that go beyond listing venue alone: the FDA has lost more than 1,300 employees since 2025, creating approval backlogs concentrated in cell and gene therapies and novel oncology products, which adds a regulatory timeline dimension to the pricing gap that global peer comparisons do not automatically capture.

Stage of development adds another layer. Azer-cel is in Phase 1b with approximately 12 patients; cema-cel has more mature datasets and clearer regulatory dialogue. Balance sheet and capital access compound this: Allogene is capitalised to execute multi-trial programmes, while Imugene must fund a registrational programme from a much smaller base, with milestone payments to Precision BioSciences of up to US$198 million additional for azer-cel adding a further balance sheet consideration.

| Metric | Imugene (IMU.AX) | Allogene Therapeutics (ALLO) |

|---|---|---|

| Market Capitalisation | ~A$38 million | ~US$0.7 billion |

| Listing Venue | ASX | NASDAQ |

| Lead Asset | Azer-cel | Cema-cel |

| Development Stage | Phase 1b | More advanced datasets |

| CAR-T Modality | Allogeneic CD19 | Allogeneic CD19 |

| Target Indication | Post-CAR-T LBCL/DLBCL | R/R NHL including LBCL |

Sponsored research attribution: The characterisation of the valuation gap as a “significant asymmetric opportunity” is sourced to Diamond Equity Research as company-sponsored analysis. This is not an independent assessment.

According to Diamond Equity Research’s sponsored analysis, the question for an investor is not whether the gap should fully close. The structural factors mean it may not. The question is whether the current discount already accounts for the clinical signals azer-cel has produced, or whether those signals remain underpriced in the ASX context.

Large pharmaceutical companies are not waiting for cell therapy programmes to reach commercialisation before acquiring them. The transaction history in this sector tells you what acquirers are willing to pay at development stage.

Gilead Sciences acquired Arcellx in a transaction reportedly valued at approximately US$7.8 billion (this figure has not been independently confirmed as to final deal terms). Eli Lilly made an acquisition move targeting Orna Therapeutics (specific transaction value not confirmed in available source material). Both transactions targeted next-generation cell therapy platforms before commercial-stage revenue.

The pattern suggests acquirers are prioritising three characteristics:

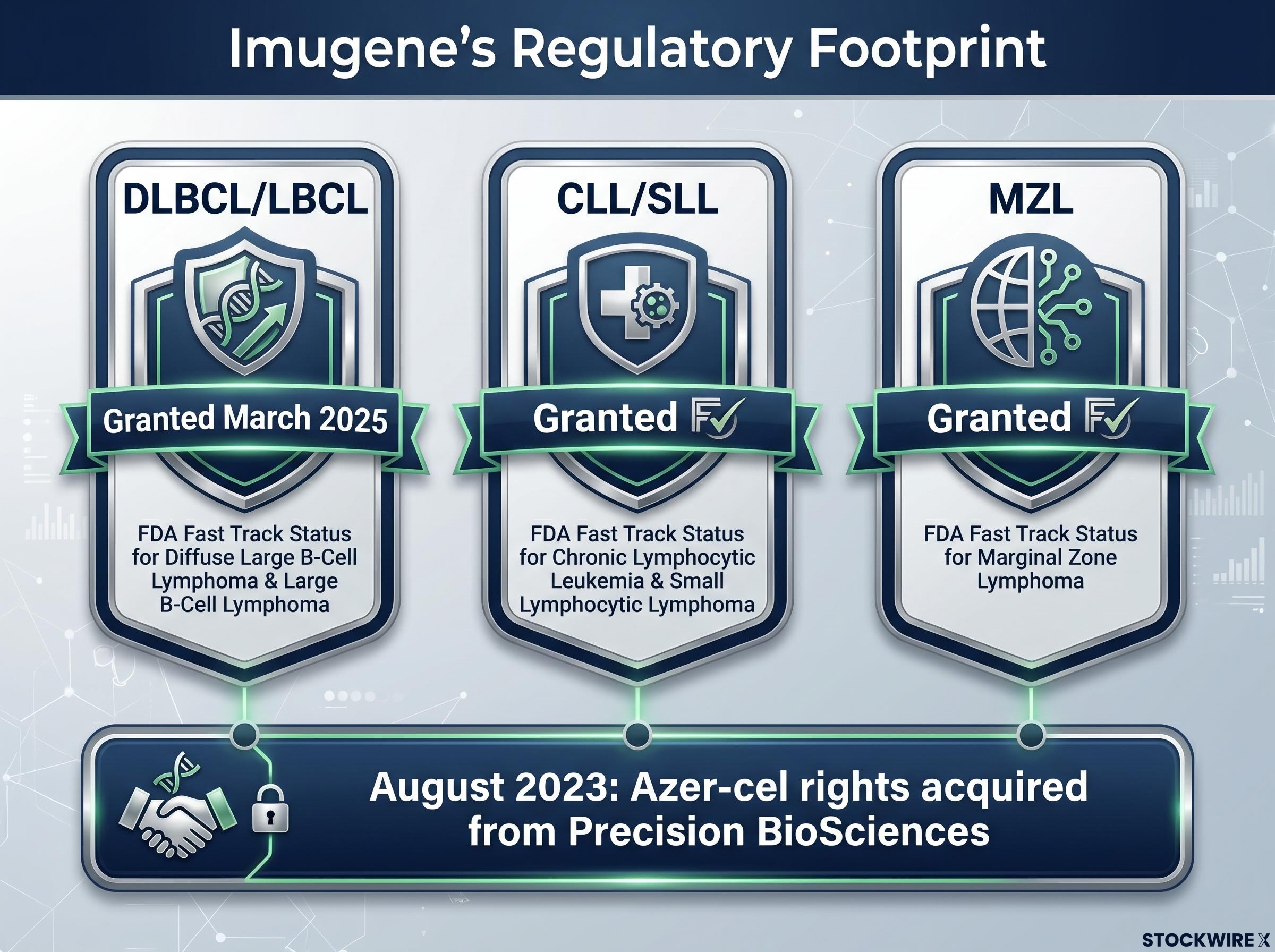

Imugene holds global rights to azer-cel plus the associated Precision BioSciences CAR-T infrastructure and team, acquired in August 2023. The post-CAR-T LBCL population is recognised across the industry as a key unmet need. As the allogeneic field thins, programmes demonstrating credible efficacy and durability signals increase in relative strategic value.

The M&A precedent tells you what acquirers have been willing to pay for platforms with credible cell therapy signals. The reader should use that context to assess whether the allogeneic CAR-T category, where azer-cel competes, is one large pharma has already demonstrated it values at acquisition.

No public source indicates any active M&A process for Imugene or azer-cel as of June 2026. The “bridge asset” and strategic optionality framing is a scenario-based characterisation from Diamond Equity Research as sponsored analysis, not a data-derived expectation.

These are not disclaimers to skim. Each risk factor represents a specific condition under which the asymmetric setup either materialises or does not.

The FDA Fast Track designation criteria establish that the programme accelerates development and review through more frequent FDA communication and rolling BLA submission eligibility, but the evidentiary standard for approval remains unchanged, meaning the clinical evidence bar for a registrational study is not lowered by Fast Track status.

Sponsored research disclosure: All forward-looking and valuation characterisations in this article are sourced from Diamond Equity Research as company-sponsored analysis and do not constitute independent financial advice.

Each of these variables represents a condition that must hold for the re-rating thesis to play out. Assessing your own tolerance for each one is the prerequisite to treating the Diamond Equity Research thesis as a basis for any investment decision.

The asymmetric setup described by Diamond Equity Research rests on four pillars: a discounted starting valuation, encouraging early clinical data, advancing regulatory dialogue, and an active M&A backdrop in the broader cell therapy sector. Each pillar strengthens the case, but the thesis is conditional on the clinical pillar continuing to hold in larger cohorts. If the data do not replicate, the other three pillars lose their foundation.

The specific catalysts that will advance or complicate the re-rating case over coming months:

Imugene holds FDA Fast Track status across three indications: DLBCL/LBCL (granted March 2025), chronic lymphocytic leukaemia/small lymphocytic lymphoma (CLL/SLL), and marginal zone lymphoma (MZL). That multi-indication breadth supports the platform framing, but each indication requires its own clinical evidence base.

The basket trial design, which evaluates azer-cel simultaneously across multiple B-cell malignancy subtypes including CLL/SLL and marginal zone lymphoma, provides multiple potential registrational pathways and allows the programme to generate clinical evidence across indications in parallel rather than sequentially.

The re-rating case is best understood as a live conditional, not a static observation. It either strengthens or weakens with each data readout, and tracking the specific variables above is more useful than holding a fixed verdict.

This article is for informational purposes only and should not be considered financial advice. Investors should conduct their own research and consult with financial professionals before making investment decisions. All investment characterisations and forward-looking statements in this analysis are sourced from Diamond Equity Research as company-sponsored analysis and do not constitute independent research. Past performance does not guarantee future results, and clinical-stage biotechnology investments carry a high degree of risk including the possibility of total loss of capital.

Allogeneic CAR-T therapy uses T-cells manufactured in advance from healthy donor cells, meaning treatments are available off the shelf without waiting weeks for patient-specific production. Autologous CAR-T requires harvesting, engineering, and returning each individual patient's own cells, which is slower and more expensive.

As of the July 2025 Phase 1b update, azer-cel achieved a 75% overall response rate and a 55% complete response rate in patients with diffuse large B-cell lymphoma who had already failed autologous CAR-T therapy from Gilead, BMS, or Novartis, with at least one patient reported cancer-free beyond 450 days.

Several structural factors drive the discount: Imugene trades on the ASX rather than NASDAQ, giving it less access to deep US biotech capital pools and thinner analyst coverage; azer-cel is at an earlier stage with a smaller patient dataset than Allogene's cema-cel; and Imugene carries milestone payment obligations to Precision BioSciences of up to US$198 million for azer-cel.

Fast Track Designation gives Imugene more frequent FDA interaction and eligibility for rolling Biologics Licence Application review, but it does not lower the evidentiary standard required for approval or guarantee an accelerated timeline. Azer-cel holds Fast Track status across three indications: DLBCL/LBCL, CLL/SLL, and marginal zone lymphoma.

The four catalysts that will most directly advance or complicate the thesis are: the outcome of the Type B End-of-Phase-1 FDA meeting on registrational trial design, expansion of the Phase 1b dataset beyond 12 patients, any further M&A activity in the allogeneic CAR-T sector, and the terms of any future Imugene capital raise.