Why Intel Is Betting on Vertical Silicon Over Commodity CPUs

41 mins ago

A ten-year cap on cash refunds sounds administratively tidy until it is mapped against a twelve-to-fifteen-year commercialisation timeline. The mismatch is not theoretical; it describes the actual development arc of the sectors most affected. Australia’s proposed changes to the Research and Development Tax Incentive (RDTI), announced in the 2026-27 Federal Budget, would restrict the refundable cash component of R&D tax offsets to a company’s first 10 years of operation. The reforms are not yet law. Draft legislation is expected in 2027, with commencement scheduled for 1 July 2028, and the Senate Economics Legislation Committee is currently reviewing submissions. What follows is an analysis of why the R&D tax cap in Australia creates a structurally different category of risk for long-cycle sectors, how that risk translates into specific portfolio and valuation considerations, and what the current Senate submissions are asking the Government to address.

The RDTI programme itself is not being abolished or capped. The change targets a single mechanism: the cash refund. Under the proposed reform, refundable R&D tax offsets would be restricted to companies in their first 10 years of operation. After that threshold, companies continue to receive a tax offset, but only on a non-refundable basis, meaning the credit is carried forward and only realises value against future taxable income.

The ATO guidance on RDTI reforms confirms seven distinct changes to the programme taking effect from 1 July 2028, with the restriction of refundable offset access to a company’s first 10 years of operation sitting alongside the revised turnover threshold and expenditure cap adjustments.

For pre-revenue companies, the distinction is the difference between a functioning cash runway and a ledger entry. A non-refundable credit has real value for an ultimately profitable company. For a firm burning cash through late-stage clinical trials or hardware scale-up with no revenue in sight, it offers no cashflow relief whatsoever.

Recce Pharmaceuticals illustrates the mechanics in practice: a non-dilutive R&D rebate of $5.3 million at the current 43.5% rate funded the company’s Phase 3 anti-infective trial without shareholder dilution, extending the runway through a critical late-stage development window that falls precisely in the years the proposed cap would affect most.

Several numerical parameters shift under the proposed structure:

| Feature | Current Rule | Proposed Rule |

|---|---|---|

| Turnover threshold (refundable offset) | $20 million | $50 million |

| Maximum eligible R&D expenditure | $150 million per year | $200 million per year |

| Minimum annual R&D spend | $20,000 | $50,000 |

| Refundable offset rate | ~43.5% cash rebate | ~48% cash rebate |

Younger firms with clearly demonstrable experimental activity may benefit from the higher rates, even as older firms lose refundability entirely.

The arithmetic makes the sector mismatch visible before any editorial framing is required. Complex clinical therapies and advanced hardware products typically require 12 to 15-plus years from discovery to commercial viability, a timeline encompassing preclinical work, Phase I through III clinical trials, and regulatory approval. The most resource-intensive phases, late-stage trials and pre-commercialisation scale-up, fall precisely outside the 10-year support window.

Software and SaaS companies commonly complete core product development in three to five years. They are more likely to reach profitability within a timeframe where the transition from refundable to non-refundable credit is manageable. The policy does not affect these sectors uniformly; it creates two distinct risk profiles from the same legislative change.

Policy commentary submitted to the Senate warns that the cap “misunderstands the long commercialisation timelines behind biotechnology and medical technology.”

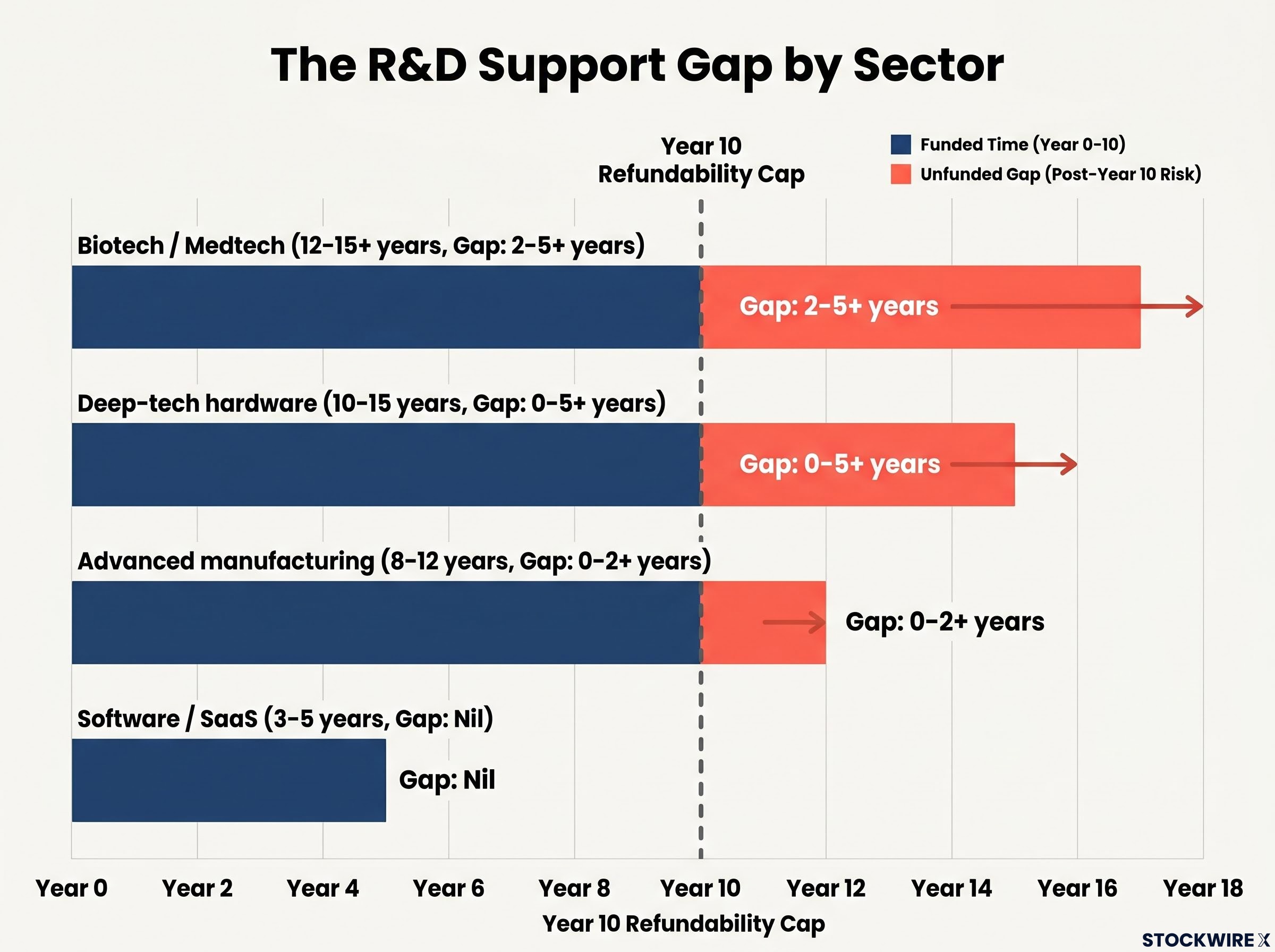

| Sector | Typical development timeline | Refundability window closes at | Years of support gap |

|---|---|---|---|

| Biotech / Medtech | 12-15+ years | Year 10 | 2-5+ years |

| Deep-tech hardware | 10-15 years | Year 10 | 0-5+ years |

| Advanced manufacturing | 8-12 years | Year 10 | 0-2+ years |

| Software / SaaS | 3-5 years | Year 10 | Nil (typically profitable) |

The gap between development timeline and support window is not marginal for biotech and medtech. It covers precisely the period when burn rates remain highest and revenue may still be years away.

Once the cash stops arriving, the question for a globally mobile founder becomes practical: what does Australia’s offering look like on a spreadsheet next to peer jurisdictions? Several countries provide refundable or super-deduction-style incentives and have been actively tuning them to attract IP-intensive activities:

Australia’s reform is explicitly designed to moderate fiscal cost growth rather than compete on generosity. The practical consequence is that the shift from refundable to non-refundable support increases reliance on external equity and venture capital during the pre-revenue phase, making Australian after-tax cashflow comparatively less attractive.

Australia’s innovation funding gap extends well beyond the RDTI: Australian startups raised approximately $5.4 billion in 2025 but 66% of those deals required at least one offshore investor, a structural reliance on foreign capital that tightens further when domestic incentive settings deteriorate relative to peer markets.

For globally mobile founders, the reform creates a real option to shift future R&D steps or holding company domicile to jurisdictions with more favourable refundable incentive structures. This is not a theoretical concern for policy commentators; it is a capital retention risk for the Australian innovation pipeline. If after-tax cashflows deteriorate relative to peer markets during the commercialisation window, the incentive to incorporate or relocate research activity offshore becomes a portfolio-level variable for investors holding Australian deep tech and medtech.

According to a formal Senate submission by Wholesale Investor and CapitalHQ (June 2026), 89% of investors surveyed reported significantly reduced appetite for funding deep tech, medtech, and life sciences sectors if the proposed 10-year cap is enacted.

The figure demands appropriate interpretive weight. Several methodological caveats apply:

If investor intent tracks this direction even partially, the effect on capital availability for pre-revenue deep tech and medtech companies would be material. Senate submission sentiment surveys carry less weight than market-wide data. In a thinly traded, illiquid asset class like early-stage deep tech, however, a documented directional shift in wholesale investor appetite is a risk signal that warrants monitoring rather than dismissal.

The reform is not yet law, but the 1 July 2028 commencement date means companies already past year five or six of operation are approaching the refundability cliff within a single investment horizon. Four distinct portfolio-level variables warrant stress-testing:

These risk dimensions are not hypothetical for investors currently deploying capital into Australian innovation assets. They are modellable variables with a defined legislative timeline.

The specific asks in the Wholesale Investor and CapitalHQ Senate submission reveal which structural failures the innovation sector considers most consequential. The submission acknowledges broad ecosystem support for housing-related tax reform while seeking to insulate productive enterprise investment from collateral damage.

The RDTI reform sits within a broader tax reform package that includes the replacement of the 50% CGT discount with cost-base indexation and a 30% minimum tax from 1 July 2027, and modelling of the CGT changes shows how the flat-discount architecture created structural distortions that a tapered alternative would have addressed without concentrating the burden on long-cycle productive investment.

Five specific recommendations were put forward:

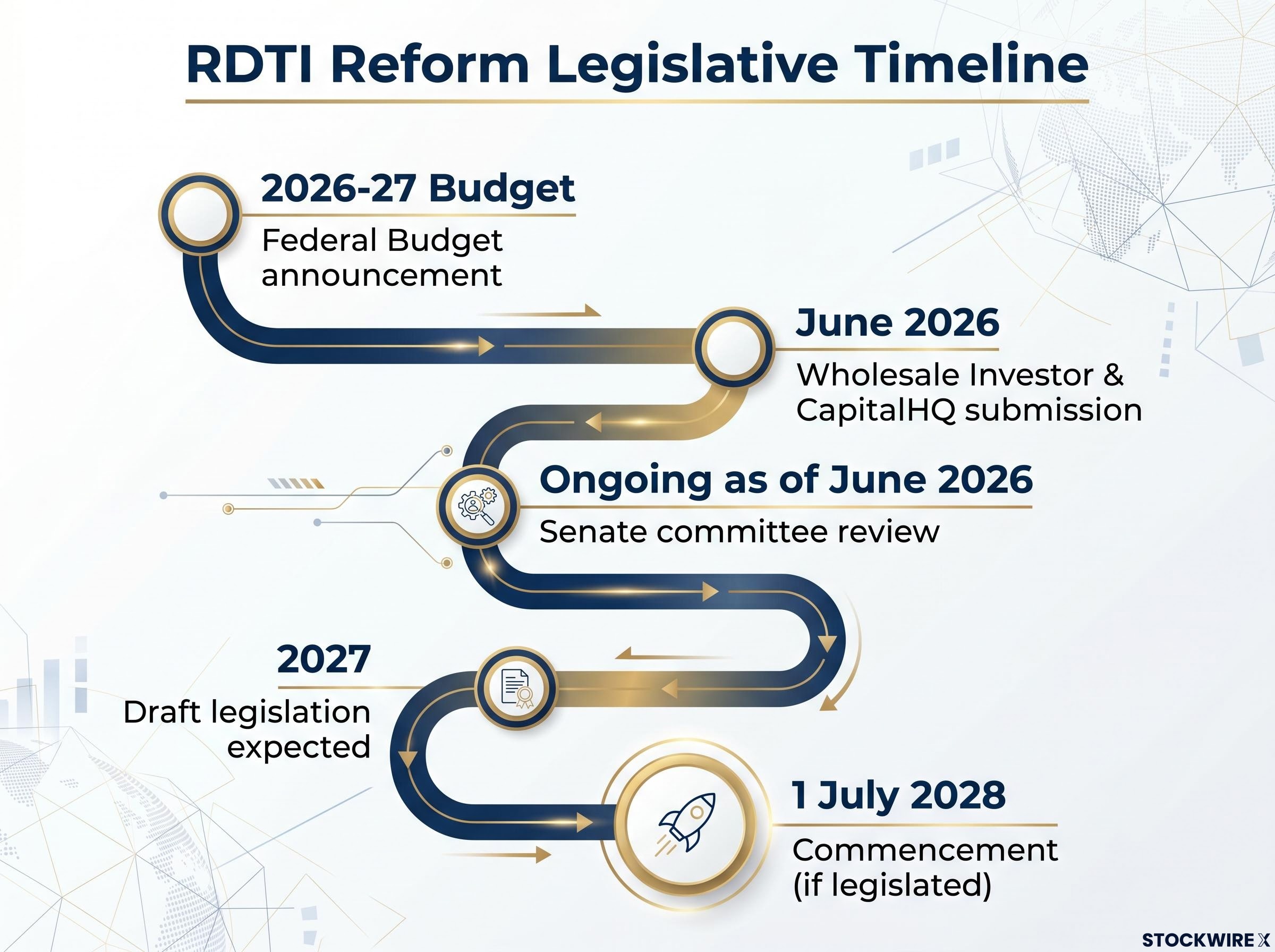

| Milestone | Date / Status |

|---|---|

| Federal Budget announcement | 2026-27 Budget |

| Senate committee review | Ongoing as of June 2026 |

| Wholesale Investor / CapitalHQ submission | June 2026 |

| Draft legislation expected | 2027 |

| Commencement (if legislated) | 1 July 2028 |

Investors do not need to be passive observers of this reform debate. Tracking whether the sector exemptions for biotech and advanced manufacturing survive the legislative process is directly relevant to portfolio positioning.

The 10-year refundability cap is not a marginal adjustment. It creates a policy-driven funding cliff at precisely the commercialisation phase where capital requirements are highest for long-cycle sectors. Fast-cycle sectors can adapt; deep tech, medtech, and life sciences face a structural mismatch between the support window and their actual development timelines.

The reform is not yet law. The Senate consultation window remains open as of June 2026, and the 1 July 2028 commencement date creates a defined horizon for portfolio review. The specific asks in the Senate submissions, particularly sector exemptions for biotech and advanced manufacturing, represent the clearest indicator of what a reformed version of this policy could look like. Whether those exemptions survive the legislative process is the single most important variable for investors with exposure to Australian innovation assets.

For investors wanting a framework to weight legislative risk before the draft legislation arrives in 2027, our dedicated guide to reading tax policy signals examines three May 2026 case studies, including Australia’s CGT reform, to show how enactment probability, implementation lag, and legislative stage combine to determine when a policy announcement becomes a portfolio-level signal rather than market noise.

This article is for informational purposes only and should not be considered financial advice. Investors should conduct their own research and consult with financial professionals before making investment decisions. These statements are speculative and subject to change based on market developments and legislative outcomes.

Australia's proposed R&D tax cap restricts the refundable cash component of Research and Development Tax Incentive offsets to a company's first 10 years of operation. After that threshold, companies still receive a tax offset but only on a non-refundable basis, meaning the credit carries forward and only realises value against future taxable income rather than providing an immediate cash refund.

The changes were announced in the 2026-27 Federal Budget, with draft legislation expected in 2027 and a commencement date of 1 July 2028, subject to the legislation passing the Senate. The Senate Economics Legislation Committee is currently reviewing submissions.

Biotech and medtech companies typically require 12 to 15-plus years from discovery to commercial viability, meaning the most resource-intensive phases such as late-stage clinical trials and pre-commercialisation scale-up fall outside the 10-year support window. Software and SaaS companies commonly reach profitability within 3 to 5 years, so the transition from refundable to non-refundable credit is far more manageable for them.

The proposed reforms raise the refundable offset turnover threshold from $20 million to $50 million, increase maximum eligible R&D expenditure from $150 million to $200 million per year, lift the minimum annual R&D spend from $20,000 to $50,000, and increase the refundable offset rate to approximately 48% (up from 43.5%), while restricting eligible activities to core experimental R&D only.

The Wholesale Investor and CapitalHQ Senate submission calls for either exempting or substantially extending the 10-year refundable R&D cap for sectors with demonstrably long development cycles, specifically naming biotech and advanced manufacturing, and also seeks to limit CGT discount changes to residential property so that innovation equity settings remain unchanged.